Summary

- The following is a quick update that was previously provided to subscribers of Premium Reports on August 28, 2018.

- The good news is that I have upgraded PSEC and increased its ST target price. However, portfolio mix and credit quality continue to decline.

- As predicted, there were large markdowns in Pacific World and InterDent offset by larger markups in the riskier portions of the portfolio including “real estate, CLO, consumer finance”.

- During calendar Q2 2018, PSEC’s NAV per share increased by $0.12 primarily due to over ever-earning the dividend by $0.04 and continued markups in NPRC and First Tower. NPRC is marked $312 million over cost.

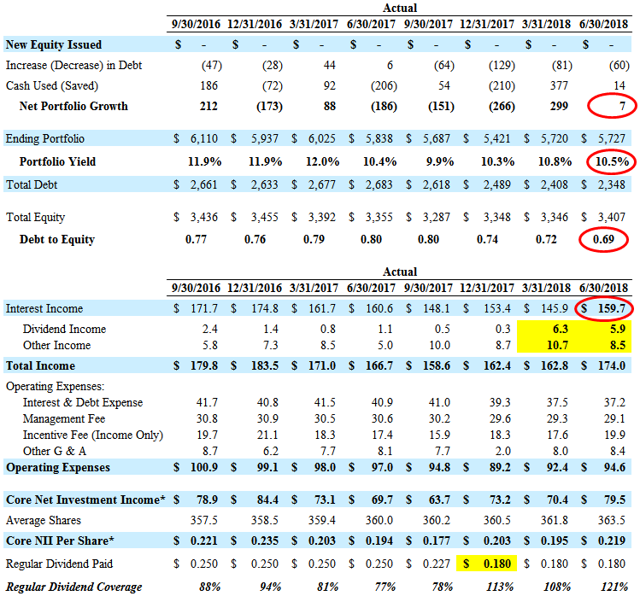

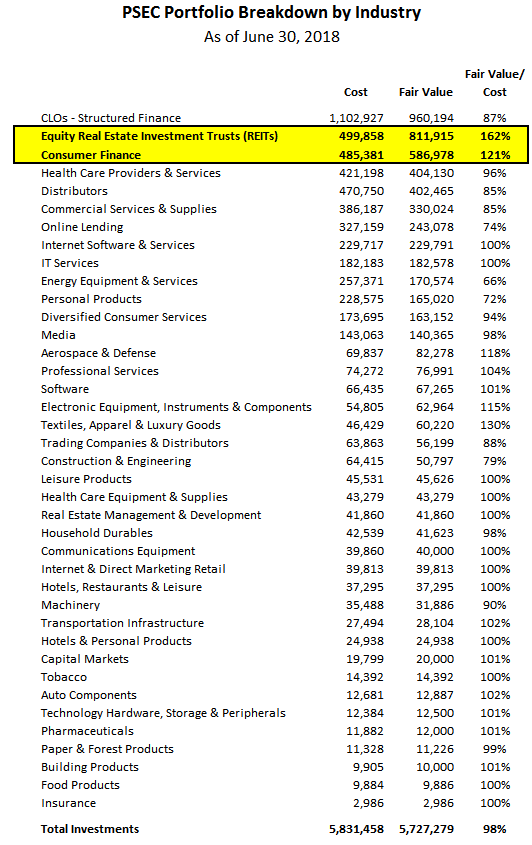

- Dividend coverage improved mostly due to the expected increase in yields from its CLOs related to the resets/refinancings, driving higher net interest margins. Also, CLOs now account for almost 17% of the portfolio.

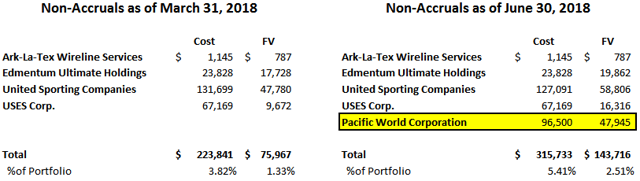

- Non-accruals increased to 5.4% of the portfolio cost (2.5% at FV) mostly due to adding a portion of Pacific World which needs to be watched along with InterDent as these account for $1.00 or 11% of NAV per share.

The following is a quick update that was previously provided to subscribers of Premium Reports on August 28, 2018. For target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs (including this one) please see Deep Dive Reports.

For Q2 2018, PSEC reported between my base and best case projections with quarterly NII of $0.219 covering 121% of its monthly dividends for the quarter. There was lower-than-expected net portfolio growth of only $7 million with an expected decline in its portfolio yield from 10.8% to 10.5%. However, there was a meaningful increase in interest income mostly due to higher yields from its CLOs:

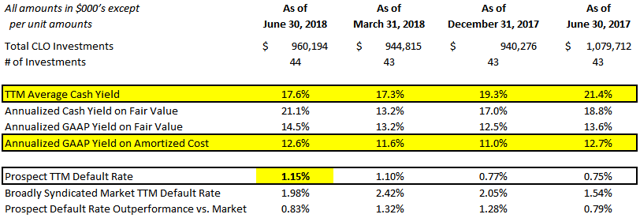

As shown in the following table and discussed below, there was an increase in the yields from its collateralized loan obligation (“CLO”) residual interests mostly due to the expected resets/refinancings driving higher net interest margins:

“Since June 30, 2017 through today, one of our structured credit investments [CLOs] has completed a refinancing to reduce liability spreads, and 19 additional structured credit investments have completed multi-year extensions of their reinvestment periods (with most resulting in reduced liability spreads as well as higher asset spread possibilities from longer weighted average life tests). We believe further upside exists in our structured credit portfolio through additional refinancings and reinvestment period extensions, and are actively working on such transactions.”

It should be noted that the rate of defaults for PSEC’s CLO investments continue to increase but are still below the average:

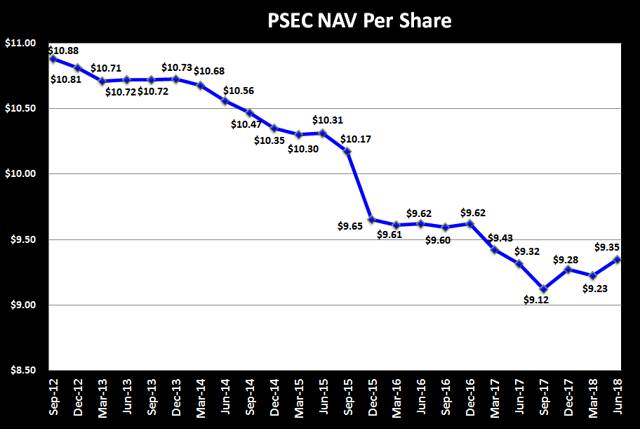

Net asset value (“NAV”) per share increased by 1.3% or $0.12 per share (from $9.23 to $9.35) due to over-earning the dividend by $0.04 and net unrealized gains of almost $41 million. A majority of the markups (over $37 million) during the quarter were related to the riskier portions of the portfolio including “real estate, CLO, consumer finance” offset by expected markdowns in Pacific World Corporation and InterDent, Inc. as discussed later:

“For the June 2018 quarter, our net increase in net assets resulting from operations was $114.3 million, or $0.31 per share, an increase of $0.17 from the March 2018 quarter as a result of an increased NII and a net increase in the fair value of our portfolio, including investments in the real estate, CLO, consumer finance, and other sectors.”

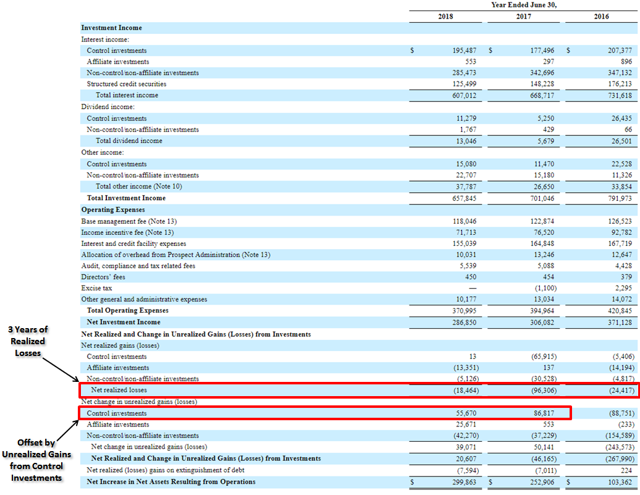

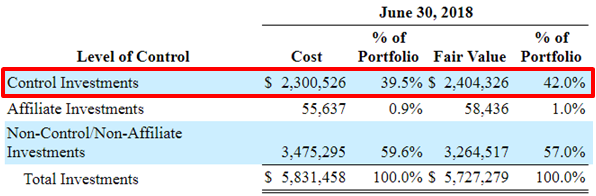

As mentioned in the recently updated BDC Risk Profiles report, changes in NAV per share are not always a clear indicator of credit issues because there are many items that impact NAV. Also, it is important to recognize the difference between “realized” and “unrealized” gains and losses. PSEC continues to have net realized losses each year offset by unrealized gains, historically from control investments as shown below:

As shown in the following table, control investments on average are marked well above cost compared to the rest of the portfolio:

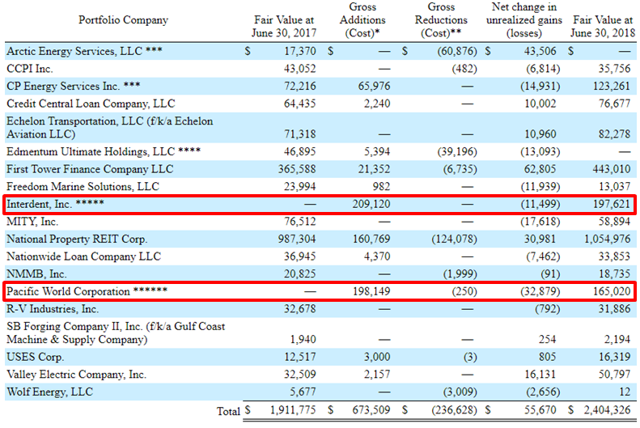

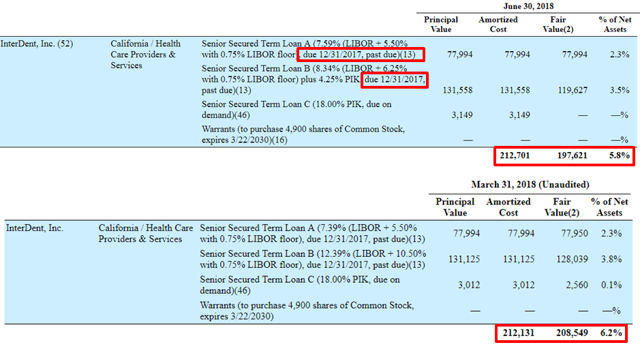

As predicted in the previous report, PSEC had meaningful markdowns in its investments of Pacific World Corporation and InterDent, Inc. during the recent quarter and were among the few control investments were meaningful unrealized losses for the year. However, these investments still account for around $363 million or $1.00 of the current NAV per share.

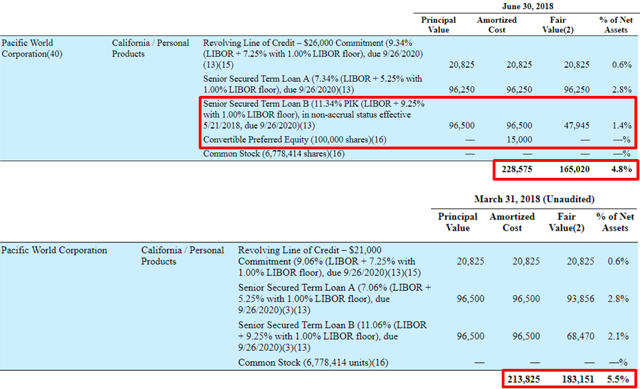

Also predicted, PSEC marked down its Term Loan B with Pacific World Corporation by another $21 million and added it to non-accrual status. However, the revolving credit line and Term A loan are still accruing and contributing to dividend coverage and need to be watched. Previously, PSEC marked down its Term A and B loans to Pacific World and on June 15, 2018, made a $15 million convertible preferred equity investment (marked to zero fair value) in the company which is now considered a “controlled investment”.

“As of June 30, 2018, Prospect’s investment in Pacific World is classified as a control investment. As a result, the valuation methodology for the TLA changed to remove the income method approach and incorporate the waterfall approach. The fair value of our investment in Pacific World decreased to $165,020 as of June 30, 2018, a discount of $63,555 to its amortized cost, compared to a discount of $30,216 to its amortized cost as of June 30, 2017. Our investment in Pacific World declined in value due to a decrease in revenues and profitability, as well as a decrease in comparable company trading multiples.”

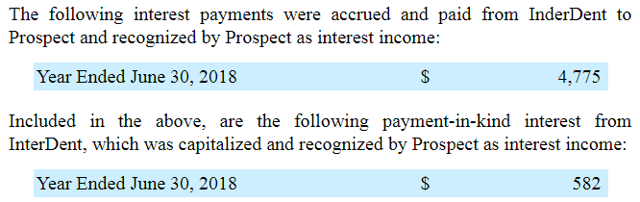

It should be noted that PSEC recognized $4.8 million of interest income through June 30, 2018, and on August 1, 2018, purchased from a third party $14 million of “First Lien Senior Secured Term Loan A and Term Loan B Notes issued by InterDent, Inc.” at par.

“Following our assumption of assuming control, Prospect exercised its rights and remedies under its loan documents to exercise the shareholder voting rights in respect of the stock of InterDent, Inc. and to appoint a new Board of Directors of InterDent, all the members of which are our Investment Adviser’s professionals. As a result, as of June 30, 2018, Prospect’s investment in InterDent is classified as a control investment.”

As mentioned in the previous report, PSEC recently extended its loans to InterDent which were past due as well as being marked down during the previous quarter “but still marked near cost and likely overvalued”. During calendar Q2 2018, PSEC assumed control of Interdent and marked it down an additional $11 million.

“As of June 30, 2018, Prospect’s investment in InterDent is classified as a control investment. As a result, the valuation methodology changed to remove the income method approach and incorporate the waterfall approach. The fair value of our investment in InterDent decreased to $197,621 as of June 30, 2018, a discount of $15,080 to its amortized cost, compared to a discount of $1,268 to its amortized cost as of June 30, 2017. The decline in fair value was due to lower projected future earnings as a result of customer attrition.”

Non-accruals increased to 5.4% of the portfolio at cost and 2.5% at fair value mostly due to adding a portion of its investment in Pacific World as discussed earlier as well as recent markups in United Sporting Companies, Edmentum Ultimate Holdings and USES Corp. as shown below.

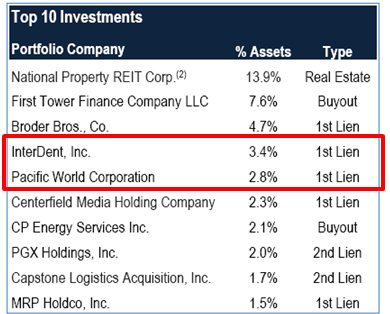

PSEC has portfolio concentration issues including its top 10 investments accounting for around 42% of the portfolio. However, this is an improvement from the recent quarter due to the sale of $180 million of its senior notes with Broder Bros., Co. during the recent quarter but still accounts for 4.7% of the portfolio:

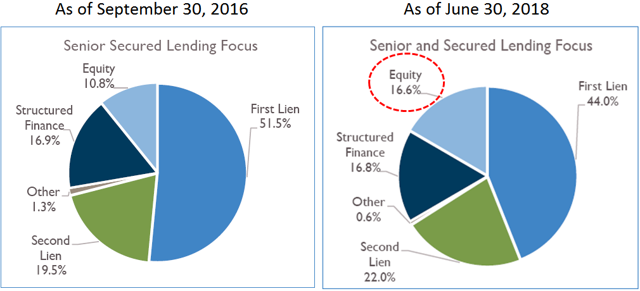

One of my primary concerns is the amount of equity investments that continues to increase accounting for almost 17% of the portfolio:

PSEC continues to grow its REIT portfolio, National Property REIT Corp.(“NPRC”), and currently has a fair value of $312 million or 162% over cost basis which has helped to offset previous losses from other portfolio investments.

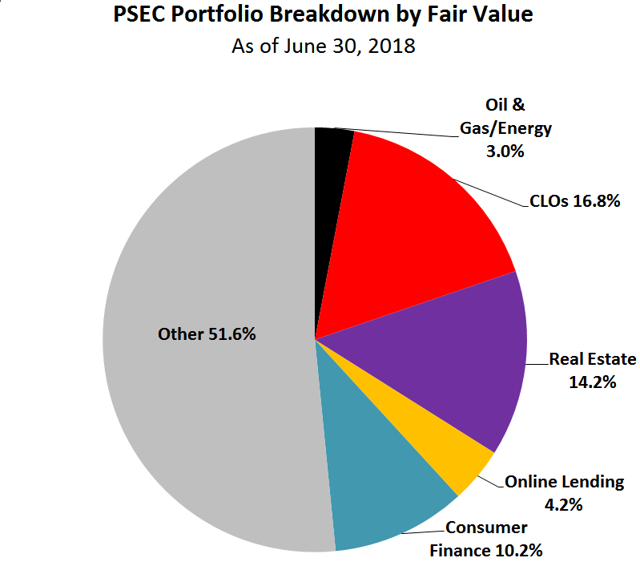

I consider PSEC to have a higher risk portfolio due to the previous rotation into higher yield assets during a period of potentially higher defaults and later stage credit cycle concerns, CLO exposure to 16.8% combined with real-estate 14.2%, online consumer loans of 4.2%, consumer finance of 10.2% and energy, oil & gas exposure of 3.0%. As mentioned in previous reports, S&P Ratings also considers the CLO, real-estate and online lending to be riskier allocations that currently account for over 35% of the portfolio.

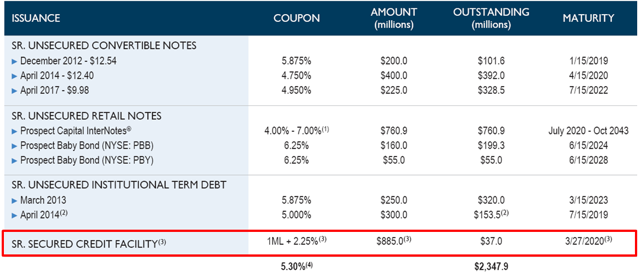

On August 1, 2018, PSEC extended its secured credit facility and slightly reduced the pricing from LIBOR+2.25% to LIBOR+2.20%. However, the company does not typically use its lower cost facility with only $37 million outstanding as of June 30, 2018.

“On August 1, 2018, we completed an extension of the Revolving Credit Facility (the “New Facility”) for PCF, extending the term 5.7 years from such date and reducing the interest rate on drawn amounts to one-month Libor plus 2.20%. The New Facility, for which $770 million of commitments have been closed to date, includes an accordion feature that allows the Facility, at Prospect’s discretion, to accept up to a total of $1.5 billion of commitments. The New Facility matures on March 27, 2024. It includes a revolving period that extends through March 27, 2022, followed by an additional two-year amortization period, with distributions allowed to Prospect after the completion of the revolving period. Pricing for amounts drawn under the Facility is one-month Libor plus 2.20%, which achieves a 5 basis point reduction in the interest rate from the previous facility rate of Libor plus 2.25%. Additionally, the lenders charge a fee on the unused portion of the credit facility equal to either 50 basis points if more than 60% of the credit facility is drawn, or 100 basis points if more than 35% and an amount less than or equal to 60% of the credit facility is drawn, or 150 basis points if an amount less than or equal to 35% of the credit facility is drawn.”

Other Subsequent Events:

“During the period from July 13, 2018 to July 16, 2018, we made follow-on first lien term loan investments of $105,000 in Town & Country Holdings, Inc., to support acquisitions.”

Goοd day! I could haᴠe ѕᴡorn I’ve visіted tһis site before but after going through many of the articles I realized it’s

neԝ tߋ me. Regardleѕs, I’m certainly pleased I found it and

I’ll be bookmarking it and checҝing back frequently!