Summary

- There has been plenty of ‘good news’ for TSLX shareholders since my previous article which is likely responsible for the continued stock price increase and out-performance compared to the others.

- On October 8, TSLX held a special meeting and shareholders overwhelmingly approved the proposal to allow the company to increase leverage.

- On August 30, 2018, PennEnergy Resources, LLC agreed to acquire substantially all the assets of Rex Energy Corporation for a cash purchase price of $600.5 million driving “approximately $0.05 per share to next quarters income.”

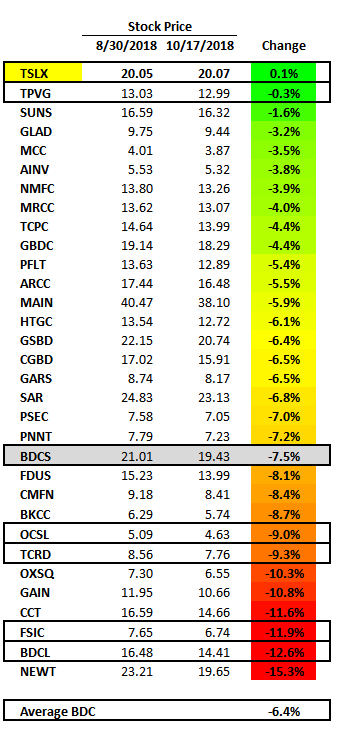

- BDC pricing has been volatile over the last 2 to 6 weeks but higher quality companies such as TSLX have outperformed. However, I am expecting continued volatility.

- TSLX will be paying additional special dividends for the reasons discussed in this article.

The following is a quick update that was previously provided to subscribers of Premium Reports along with target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs (including this one) please see Deep Dive Reports.

TSLX Article Follow-Up:

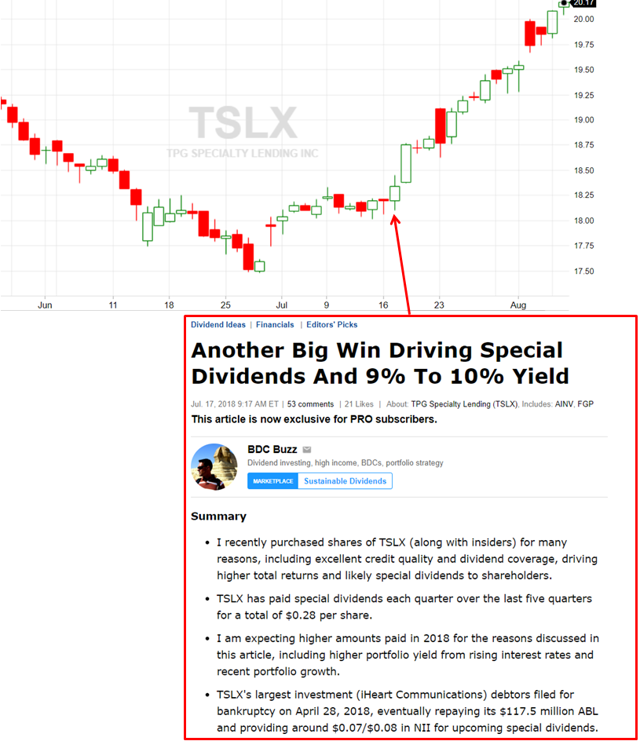

As shown in the following chart, TSLX’s stock price rebounded after my public article “Another Big Win Driving Special Dividends And 9% To 10% Yield” that discussed my reasons for purchasing shares at $17.46, after the March 2018 ex-dividend and as the Relative Strength Index or RSI dipped near 30.

There has been plenty of ‘good news’ for TSLX shareholders since my previous article (and personal purchase of additional shares) which is likely responsible for the continued rise in stock price and out-performance compared to the other BDCs.

As mentioned in “Recent Volatility for BDCs“, BDC pricing has been pulling back and likely for the reasons discussed in previous updates.

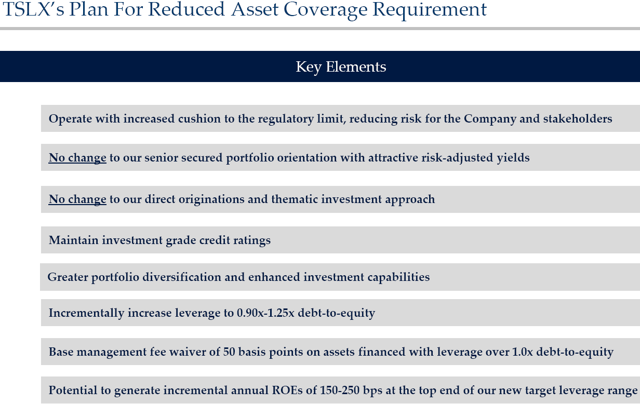

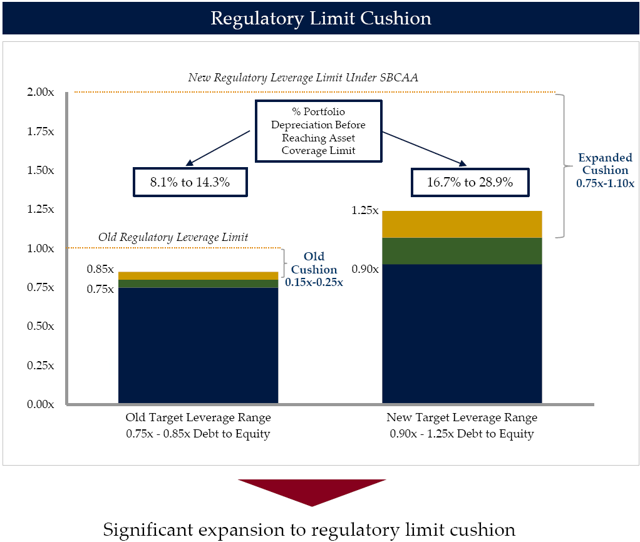

TSLX Reduced Asset Coverage Ratio

On October 8, 2018, TSLX held a special meeting and shareholders overwhelmingly approved the proposal to allow the company to increase leverage by approving the application to the company of a minimum asset coverage ratio of 150% effective October 9, 2018:

Source: 8-K Filing

Management gave the following reasons for the ability to increase leverage:

- Increase the regulatory cushion through a lower minimum asset coverage requirement; reduces risks for the Company and stakeholders

- Maintain investment grade ratings with revised financial policy of 0.90x-1.25x debt-to-equity; continued access to diversified debt funding sources

- The relative benefits of increasing the fundamental earnings power of the business outweighs the potential risks associated with greater leverage

- Track record of strong performance; greater investment capabilities from additional flexibility to manage capital resources and enhance the diversification profile of the portfolio

TSL Advisers, LLC intends to waive a portion of the fees by reducing the management fee on assets financed using leverage over 200% asset coverage (in other words, over 1.0x debt to equity):

“Pursuant to the waiver, the Adviser intends to waive the portion of the Management Fee in excess of an annual rate of 1.0% (0.250% per quarter) on the average value of the Company’s gross assets as of the end of the two most recently completed calendar quarters that exceeds the product of (1) 200% and (2) the average value of the Company’s net asset value at the end of the two most recently completed calendar quarters.”

Source: 10-Q Filing

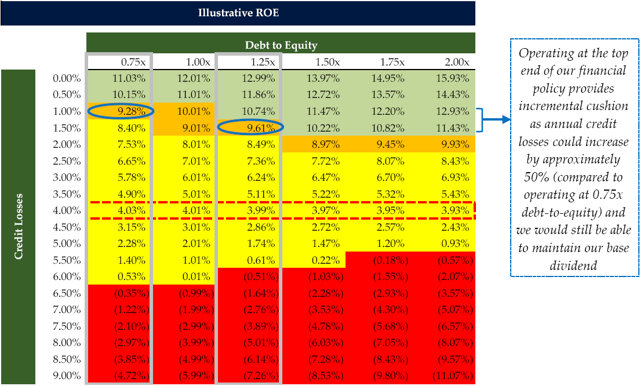

Upon the effectiveness of the lower minimum asset coverage ratio requirement, the company’s revised financial policy is to increase its target debt to equity range from 0.75x-0.85x to 0.90x-1.25x.

Obtaining regulatory relief in conjunction with a revised financial policy of 0.90x-1.25x debt-to-equity will allow TSLX to drive incremental ROEs while maintaining an investment grade ratings profile.

The table below illustrates the impact on ROEs at differing levels of leverage (debt-to-equity) and levels of credit losses, and highlights scenarios at which ROEs exceed book dividend yield (including and excluding the supplemental dividend), and scenarios at which ROEs are below the current base book dividend yield.

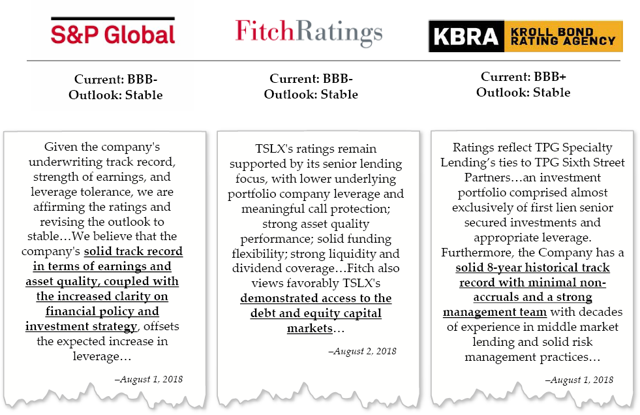

Changes to TSLX Investment Grade Ratings

The following are the investment grade ratings from Fitch, S&P and Kroll under new target leverage range of 0.90x-1.25x debt-to-equity.

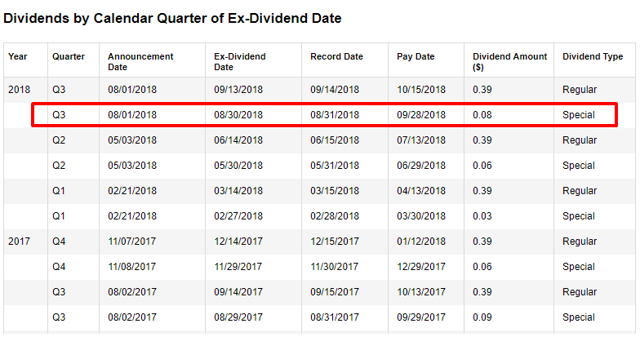

Continued And Upcoming TSLX Special Dividends

As predicted in the article linked above, TSLX recently paid a special/supplemental dividend of $0.08 per share payable in September which was above my ‘best case’ projected special dividend of $0.07 per share.

“Our Board also declared a Q2 supplemental dividend of $0.08 per share to shareholders of record as of August 31st payable on September 28. Since introducing our variable supplemental dividend framework in Q1 of 2017, we’ve declared a total of $0.36 per share as an incremental dividend as net investment income per share exceeded based dividends per share in each of the past six quarters.”

The company has covered its regular dividend by an average of 133% over the last four quarters, with undistributed taxable income and capital gains of around $70 million or $1.06 per share after taking into account supplemental dividends. I am now expecting at least $0.20 per share (previously $0.10) of supplemental dividends paid in 2018 that will most likely be higher, especially given the likelihood of “other fees” associated with the upcoming repayments. Management increased its 2018 net investment income (“NII”) guidance to $1.85 and $2.00 which is likely conservative, similar to 2017 guidance.

“Year-to-date we have generated strong annualized ROEs based on both net investment income and net income of 13.3%. We believe this reflects our strong originations platform, our ability to embed economics into our portfolio, as well as our continued focus on optimizing our capital structure through the lowest funding costs we can obtain. Given our strong year-to-date ROEs and our outlook for the remainder of 2018, we are updating the upper end of our full year 2018 NII guidance from a $1.85 per share to $2 per share.”

TSLX management continues to produce higher returns by investing in distressed companies through excellent underwriting standards that protect shareholders during worst case scenarios including call protection, prepayment fees and amendment fees backed by first-lien collateral of the assets. As predicted in the previous report, there was another meaningful increase in “other fees” income which includes prepayment fees and accelerated amortization of upfront fees associated with the bankruptcy and planned reorganization/repayment of its $117.5 million asset-based loan (“ABL”) with iHeart Communications at LIBOR+4.75.

My ‘base case’ projections do not include large amounts of fee and other income related to early repayments. However, management mentioned around $0.05 to $0.06 per share of fee income reserves that will likely be recognized in Q3 2018 related to iHeart and Rex Energy that I have included in the updated projections:

“Note that our fee income this quarter reflects reserves totaling $0.05 per share or $0.06 per share on a post incentive fee basis related to two investments that Josh referenced in his opening remarks. Again we expect these reserves will be recognized into income in our Q3 results as we reach resolution on these two investments.”

iHeart Communications Update:

“As shared on the last call iHeart follows the Chapter 11 in late April and in June we refinance our asset based loan upon the funding of the company’s new debt in possession financing. Along with the repayment of our loan principal, we received cash payment on post-petition interest and prepayment fees totaling 3.6 million which included 592,000 of certain interest income that we reserve against. In July unsecured credit committee of iHeart had objection of certain portions of income received, which we believe to be meritless. A hearing on that objection is currently scheduled for the fall and we’re optimistic that we will be able to recognize our reserve portion of interest income of approximately $0.01 per share upon resolution of the issue pertaining to the committee’s objection.“

Rex Energy Update:

On August 30, 2018, PennEnergy Resources, LLC agreed to acquire substantially all the assets of Rex Energy Corporation for a cash purchase price of $600.5 million driving “approximately $0.05 per share to next quarters income.”

“On May 18th Rex Energy filed a voluntary petition for relief under Chapter 11 of the bankruptcy code with the restructuring and support agreement between the company’s first lien inventory to the second lien. The agreement stipulates among other things that proceeds from the sale of substantially all of the company’s assets would benefit the entirety of the pre-petition firstly and obligations including ABL. Since we do not have any visibility on financial proceeds of asset sale of process during Q2, our income reflects a reserve of $3.1 million related to a portion of the Rex prepayment fee. The final bit of the sale process were due likely with an auction scheduled for August 16th. We’re optimistic that we have what it take our fee reserve off during Q3 which will contribute approximately $0.05 per share to next quarters income.”

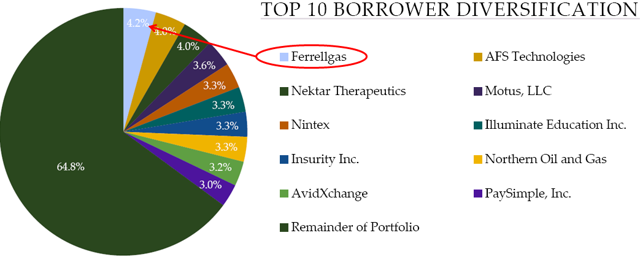

Also predicted in the previous article, TSLX made a sizable investment in Ferrellgas Partners, L.P. (NYSE:FGP) of $82.5 million during Q2 2018 which is now its largest investment and will likely drive another large special dividend.

“We continue to be thematic in our approach to originations, focus on opportunities that correspond to our platform sector expertise and relationships, as well as opportunities arising from market dislocations where our competitive advantage of size and scale given our SEC exempted release allows us to underwrite attractive risk rewards. A good example of this is the $575 million senior secured credit facility that we completed for Ferrellgas during the quarter which Josh referenced on our last call. Ferrellgas is a publicly traded distributor of propane with an enterprise value of $2.3 billion. The company has a defensive core business with high return on invested capital and a strong management team but faced refinancing difficulties given the challenging regulatory environment for banks. Due to our ability to provide a fully underwritten financing solution through co-investments from affiliated funds we were able to structure a first lien last out position at a low attach point of 0.2X at a low net leverage of 1.7X with highly attractive adjusted returns. Further as we size down our originations amount to the target hold of our portfolio we are able to drive additional economics for our shareholders through syndication income. At quarter-end our investment in Ferrellgas represented our largest position at 4.2% of the portfolio fair value.”

On May 4, 2018, FGP executed a new $575 million senior secured credit facility to replace its credit facility that was scheduled to mature in October 2018. This new facility consists of a $300 million revolving line of credit supported by commitments from TPG Specialty Lending, Inc. and PNC Bank, National Association, as well as a $275 million term loan, both priced at LIBOR + 5.75% and maturing May 4, 2023. This new senior secured credit facility is secured with substantially all of the operating partnership and its subsidiaries’ asset and FGP and the general partner’s partnership interests in the operating partnership and contains various covenants and default provisions, as well as requirements with respect to the maintenance of specified financial ratios and limitations on the making of loans and investments. It is important to note that this was another complex transaction that required TSLX’s excellent underwriting skills likely with appropriate call protection, prepayment fees and amendment fees backed by first-lien collateral of the assets and covenants some of which were detailed in the related 8-K filed by FGP.

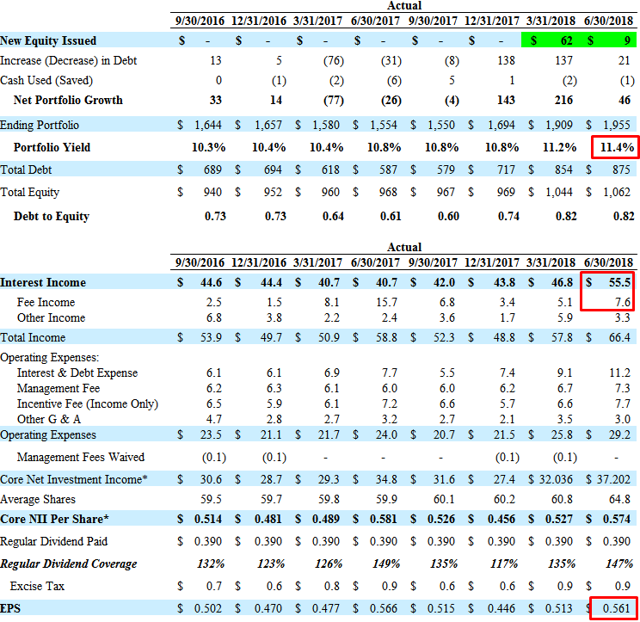

For the quarter ended June 30, 2018, beat my best case projections covering its dividend by 147% due to increased portfolio yield from 11.2% to 11.4% and higher fee and “other income” as discussed earlier.

TSLX’s credit platform continues to outperform on many levels including much higher-than-expected portfolio growth during Q2 2018 driving higher earnings. As shown in the table below, the company experienced lower amounts of sales/repays.

Some of the primary reasons for historically higher returns include strong financial covenants and call protections that protect shareholders during higher amounts of prepayments and worst case scenarios.

“Despite recent competitive dynamics we remain committed to high documentation standards and meaningful terms that provide robust downside protection. At quarter-end we maintained effective voting control on 84% of our debt investments, an average of 2.3 financial covenants per debt investment consistent with historical levels. As for managing prepayment risk, the fair value of our portfolio as a percent of call protection is 95.6% which means that we have protection in the form of additional economics so our portfolio get repaid in the near term.”

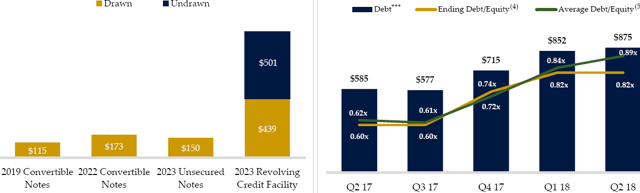

However, it also important to point out that the company is able to cover dividends with recurring sources as discussed by management on previous calls. The company is currently near the higher end of its targeted leverage (debt-to-equity of 0.75 to 0.85) with $501 million available on its credit facility for portfolio growth in the coming quarters.

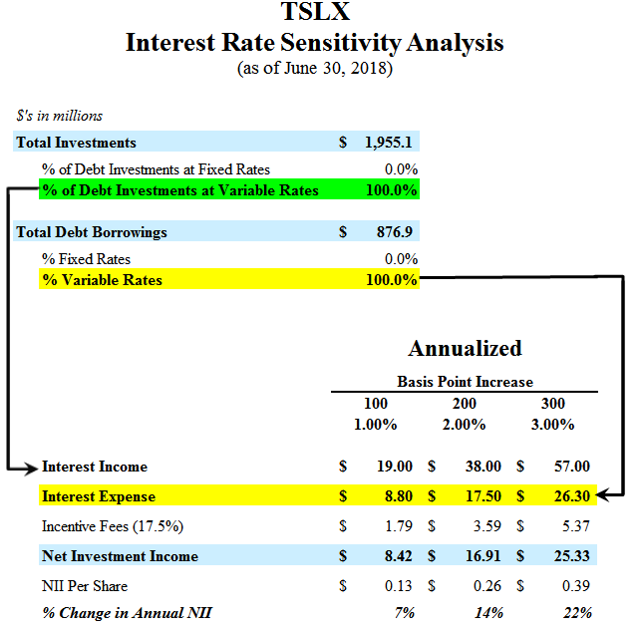

Interest Rate Sensitivity Analysis

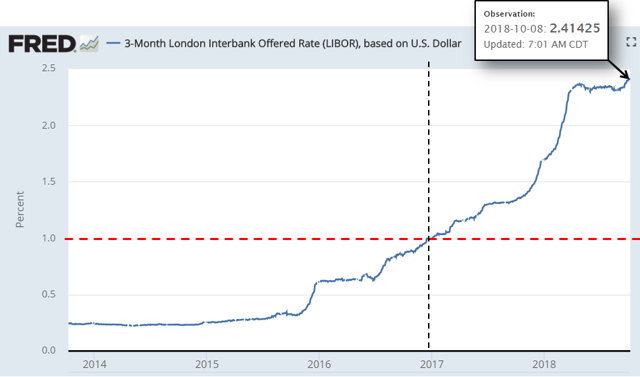

Interest rate sensitivity refers to the change in earnings that may result from changes in interest rates. Most BDCs continue to experience higher portfolio yields mostly due to the rising LIBOR that should improve (or at least maintain) net interest margins and dividend coverage for the sector in the coming quarters.

Source: FRED

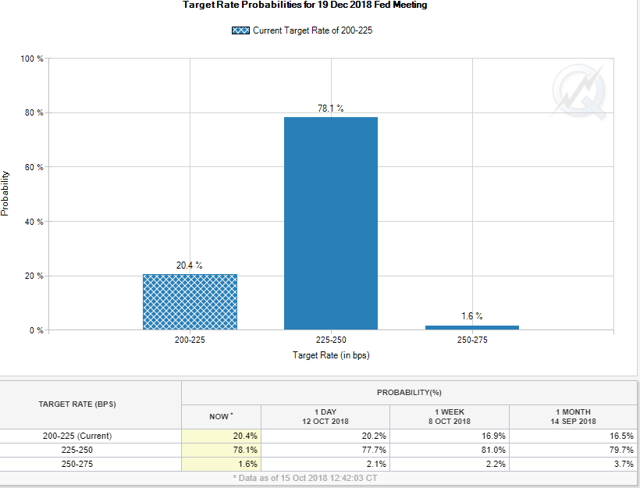

The Fed is still expected to hike rates again on December 19, 2018, and it is important to note that there is lag/delay between the rise in the underlying interest rate of a loan and higher interest income received by the BDC as discussed on the previous Apollo Investment (AINV) call:

The weighted average yield on our portfolio at cost increased by 20 basis points to 10.7%, primarily due to increases in LIBOR, partially offset by the repayment of higher yielding assets. During the quarter, one-month LIBOR increased approximately 30 basis points and ended the quarter at 1.9%. Since we’ve more floating rate assets than floating rate liability, an increase in LIBOR generally is positive for us. However, as LIBOR increases, there is usually a lag effect before we see the full impact of the interest than we received from our borrowers as borrowing rates generally reset monthly or quarterly.

Source: CME Group

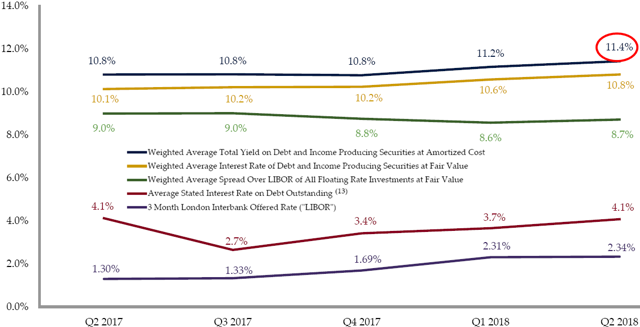

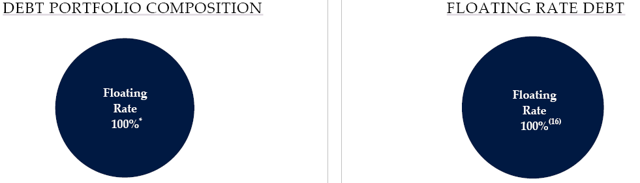

As of June 30, 2018, 100% of TSLX’s portfolio debt investments bore interest at variable rates, most of which are subject to interest-rate floors. During Q2 2018, there was another increase in portfolio yield (from 11.2% to 11.4%) due to increased LIBOR and higher yields on new investments compared to sales and repayments:

At June 30th the weighted average total yield on our debt and income producing securities at amortized cost was 11.4% compared to 11.2% at March 31st. This increase was due to the upward movement and the effective LIBOR on our portfolio — debt portfolio as well as the impact on high yields on new versus exited debt investments. The weighted average yield that amortize cost on new and exited debt investments during the second quarter were 11.2% and 10.5% respectively.

However, 100% of borrowings were also at variable rates. During Q2 2018, the company increased the amounts of its unsecured 2022 notes to $172.5 million likely in preparation of reducing its asset coverage ratio. In February 2018, the company reduced the pricing on its revolving credit facility (from LIBOR + 2.00% to LIBOR + 1.875 and in January 2018, the company issued $150 million of 4.50% five-year senior unsecured notes. It should be noted that 100% of TSLX’s borrowings are at variable rates (based on LIBOR) but the company is adequately positioned for rising interest rates due to ‘match funding’ with 100% of debt investments at variable rates.

This quarter on the debt side opportunistically reopening our 2022 convertible notes and increasing the total principal amount outstanding from $115 million to $172.5 million. The transaction price to the slight premium to par resulting in a swap adjusted pricing on the upsized portion of LIBOR of approximately 160 basis points which is well inside the swap adjusted spread on both the original notes and the spread on our secured revolver. We executed this transaction because it allowed us to improve our unsecured funding mix with no material impact on our weighted average cost of debt and therefore minimal drag on our pro forma ROEs.

I consider TSLX to have average–positioning for rising interest rates.

TSLX Summary

I will continue to purchase additional shares of TSLX (especially during general market pull backs) for many reasons, including excellent credit quality and dividend coverage driving higher total returns and additional special dividends to shareholders over the coming quarters due to:

- October 8, shareholder approval for increased leverage.

- Increased portfolio yield and growing net interest margins.

- $0.05/$0.06 per share of fee income reserves that will be recognized in Q3 2018 related to iHeart Communications and Rex Energy.

- Continued higher-than-expected portfolio growth.

- Its “opportunistic” investment in Ferrellgas Partners that will likely drive another large special dividend.

For target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs (including this one) please see Premium Reports.