Summary

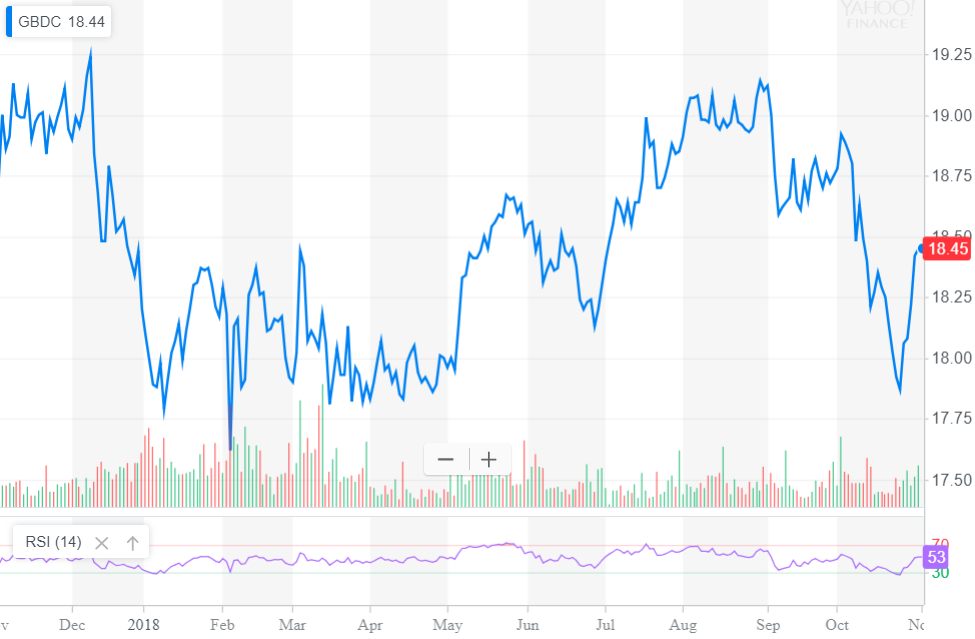

- GBDC continues to outperform the market and other BDCs likely for the reasons discussed in previous updates provided to to subscribers of Premium Reports on August 7, 2018.

- I have been making purchases of ‘higher quality’ BDCs this year, including GBDC due to consistent dividend coverage, NAV per share growth, and special dividends, delivering higher returns to shareholders.

- GBDC has better-than-average positioning for rising interest rates with a potential for a 10% increase in annual NII for each 100 basis point increase in the underlying rate.

- I believe that GBDC will continue to pay special dividends to avoid excise tax and will raise capital through accretive equity offerings as needed.

- Credit quality remains strong with low non-accruals at 0.8% of the portfolio and include the recently added PPT Management and Uinta Brewing. SUNS also has a position in PPT Management that was discussed on the recent call and will likely be added back to accrual.

- NAV per share hit a new high, increasing by 0.2% (from $16.11 to $16.15) and has increased 23 out of the last 24 quarters, after excluding the impact from previous special dividends.

You can read the full article at the following link:

The following is a quick update that was previously provided to subscribers of Premium Reports along with target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs (including this one) please see Deep Dive Reports.

- GBDC: Over 7% Dividend Yield Supported by Rising Rates & Quality Portfolio (published on Seeking Alpha on August 15, 2018)

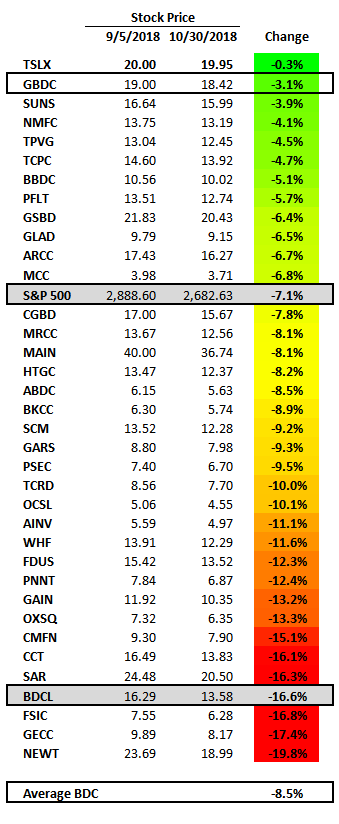

Since my article 14.5% Yielding ETN: Time To Buy Or Take Profits?, the average BDC has declined by 8.5% compared to NMFC down only 4.1%. However, there has been a wide range of recent performance from TPG Specialty Lending (TSLX) down less than 1% for the reason discussed in “TSLX: Upcoming Special Dividends & Shareholders Overwhelmingly Approve Increased Leverage” compared to NEWT down almost 20%.

Business Development Company (“BDCs”) have been pulling back for the reasons discussed last week in “BDC Sector Volatility Driving 10.5% Average Yield“. As mentioned in the article, the recent declines in BDC stock prices has not been driven by fundamentals especially as high-yield default rates continue to decline as mentioned this morning in “Corporate debt levels and default rates diverge“. I am expecting a rally in BDC pricing later this quarter and likely through Q1 2019.

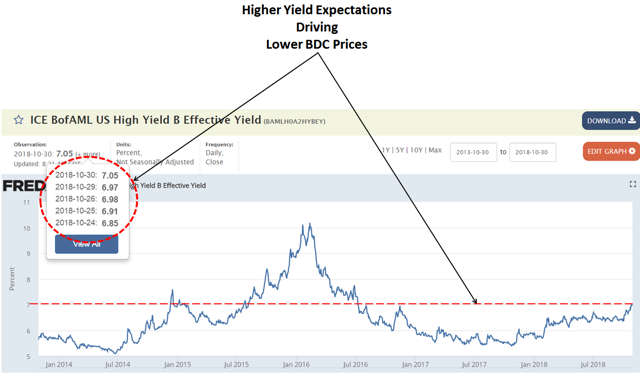

The recent drop in GBDC’s stock price is not due to underlying fundamentals, but likely investor expectations of higher yields, which is not necessarily tied to higher expected defaults given the strong economic fundamentals. In fact, there is a good chance that the recent widening of yield spreads will be discussed on the upcoming earnings call as a positive tailwind for new investments and earnings in the coming quarters.As shown below, the ‘BofA Merrill Lynch US Corporate B Index’ (Corp B) yield continues to rise and is now at its highest level since November 2016:

For target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs (including this one) please see Premium Reports.

Can I get a sample of your special reports on GBDC to evaluate? I’ve subscribed to some well known services before, each of whom were going to provide “valuable services” tuned to my goals. They didn’t. They provided up to 4 daily e-mails regarding the latest direction on their favorite stock.

I really don’t want to be a day trader. I want to buy good companies that pay good dividends at a good price and hold them for a long time. I want companies that are well managed by people I don’t have to second guess with every new situation that “might” affect the market

The best thing to do would be to sign up for a shorter term and see if it meets your needs. I’m a hold and buy more on the dips investor and there are 3 to 4 email updates per week. However, you are provided with a link to access all reports from the previous quarter as soon as you sign up.