The following information was previously provided to subscribers of Premium BDC Reports along with:

- AINV target prices/buying points

- AINV risk profile, potential credit issues, and overall rankings

- AINV dividend coverage projections and worst-case scenarios

Summary

- I have updated the projections for AINV to take into account the recently reported results and guidance from management on the earnings call yesterday (see below).

- AINV’s recurring interest income declined to its lowest level over the last 15 years and the company would have only covered around 87% of dividends if incentive fees were paid.

- Management guided for earnings to “fluctuate” over the coming quarters due to upcoming incentive fees hopefully offset by increasing leverage, portfolio rotation, and Merx Aviation.

- There is a chance of a downgrade to ‘Level 3’ (implying the potential for a reduction) depending on the progress of rotating out of “non-earning and lower-yielding assets” and improved results/income from its investment in Merx.

- AINV is likely fully priced at these levels and continues to have among the highest leverage (1.37) in the sector combined with exposure to Merx (13%) and “non-core” investments (8%).

AINV Distribution Update

On May 20, 2021, the Board of Directors declared a distribution of $0.31 per share payable on July 7, 2021 to shareholders of record as of June 17, 2021. On May 20, 2021, the Company’s Board also declared a supplemental distribution of $0.05 per share payable on July 7, 2021 to shareholders of record as of June 17, 2021.

Since 2018, the distributions to shareholders have been covered only through fee waivers and not paying the full incentive fees. However, the company will likely start paying incentive fees during the September 30, 2021, quarter which will have a meaningful impact on dividend coverage and was discussed on the recent call:

“Given the total hurdle feature in our fee structure and the net losses recorded during the look-back period, we have not paid an incentive fee since the quarter ended December 2019. Given the significant recovery in the portfolio over the past several quarters, we wanted to make sure everyone is aware that we may begin paying a partial incentive fee in the quarter ending September 2021. The exact timing and amount may vary based upon future gains and losses as well as the level of the net investment income.”

Management is working to improve dividend coverage through the “redeployment of non-earning and lower-yielding assets from non-core and legacy assets, as well as an increase in yield we received from our Merx investment”:

“We said that we believe a $0.31 base distribution reflects a conservative estimate of the long-term earnings power of our core portfolio, and that the supplemental distribution would be a function of the redeployment of non-earning and lower yielding assets from noncore and legacy assets, as well as an increase in yield we received from our Merx investment. We remain constructive on each of these drivers, although we expect some of the benefits of these drivers will occur after we start accruing incentive fees. As a result, net investment income may fluctuate over the next few quarters as we continue to reposition out of noncore and legacy assets and grow the portfolio to within our target leverage range.”

As discussed later, AINV’s recurring interest income has recently declined to its lowest level over the last 15 years and the company would have only covered around 87% of the quarterly dividends if the full incentive fees had been paid. Investors should expect dividend coverage to “fluctuate” over the coming quarters but management seems committed to paying the regular quarterly distribution of $0.31 plus the supplemental distribution of $0.05 through March 31, 2022, as discussed on the call:

“That said, we currently intend to declare a quarterly distribution of $0.31 and a quarterly supplemental distribution of $0.05 for the next four quarters.”

Q. “On the maintaining the $0.05 per quarter for the next four quarters, does that include the one that you announced today? So, it’s three after this, or it’s four into the future?”

A. “No, it’s four, including the one that we announced today.”

There is a chance that AINV could be downgraded to ‘Level 3’ dividend coverage (implying the potential for a reduction in the amount of total dividends paid) depending on the progress of rotating out of “non-earning and lower-yielding assets” and improved results/income from its investment in Merx Aviation (discussed later). Management is also actively growing the portfolio with the use of higher leverage which is already among the highest in the sector which is currently averaging around 0.94 debt-to-equity (net of cash).

I have updated the projections for AINV to take into account the recently reported results as well as guidance from management on the recent call.

“Looking ahead to fiscal year 2022, we will continue to seek to optimize and de-risk our portfolio and rotate out of our remaining noncore and second lien assets into core assets. The noncore assets are generating about a 4% or 5% return. So, as we generate cash off those assets and redeploy them into our current yield and we get Merx back to a level of producing income, not to where it was before, but to sort of a new moderated level, we can generate enough income after the incentive fee to cover that dividend.”

“As we look ahead, we are confident in our ability to grow our portfolio and operate within our target leverage range, given the tremendous need for creative and flexible private capital, and the unique and robust nature of the Apollo and MidCap platform.”

“From April 1st to May 18th, we’ve made new commitments of approximately $193 million, all of which were first lien corporate loans. Gross fundings have totaled $157 million; sales and repayments have totaled $149 million, including $57 million of second lien corporate lending positions.”

AINV was previously upgraded to ‘Level 2’ due to the expected dividend reduction and the strong likelihood that the company would not be paying incentive fees over the coming quarters. Previously, AINV was considered a ‘Level 4’ dividend coverage BDC implying that a dividend reduction was imminent and on August 6, 2020, the company announced a decrease in the regular quarterly dividend per share from $0.45 to $0.31.

From previous call: “Turning to our distribution, in light of the challenges and uncertainty created by the COVID-19 pandemic and our plans to further reduce the funds leverage, we have reassessed the long-term earning power of the portfolio and included that as a prudent to adjust the distribution at this time. We believe that distribution level should reflect the prevailing market environment and be aligned with the long-term earnings power of the portfolio. Going forward in addition to a quarterly based distribution, the company’s Board expects to also declare supplemental distribution and an amount to be determined each quarter. We believe a $0.31 distribution reflects the long-term earning power of the core portfolio including Merx.”

Full BDC Reports

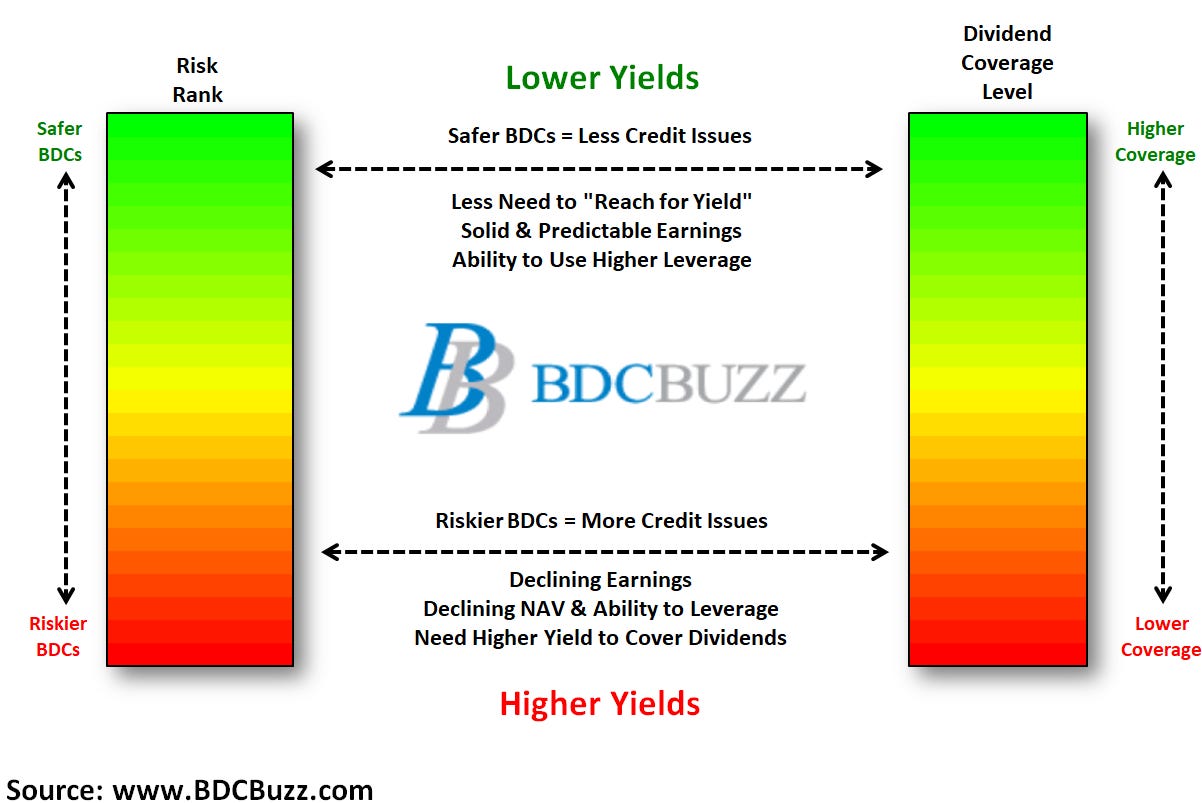

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.