Summary

- PFLT continues to rally since my previous article and up almost 10% since March 1, 2018. I am expecting improved dividend coverage for the reason mentioned in this article.

- PFLT’s portfolio yield continues to rise partially due to being invested in 100% floating rate assets driving higher earnings as shown in my Interest Rate Sensitivity Analysis.

- Similar to other higher quality BDCs, PFLT’s management is focused on capital preservation and “underwriting as if we’re at the peak of the credit cycle”.

- Management purchased additional shares at the recent lows and mentioned: “Our growing portfolio, increases in LIBOR, and the doubling of PSSL should provide a strong tailwind to growing our earnings stream”.

- PFLT is trading under book value with first-lien senior secured investments at floating rates for investors that want solid returns without the typical amount of BDC-related risk.

You can read the full article at the following link:

Recent BDC Performance:

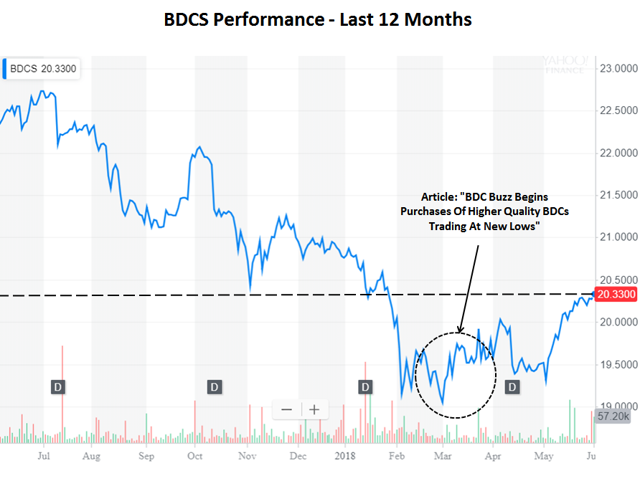

The stock price for PennantPark Floating Rate Capital (PFLT) has continued to rally since my previous article “First-Lien Portfolio Currently Paying A 9% Dividend Yield” discussing reasons to buy including rising portfolio yield and dividend coverage over the coming quarters.

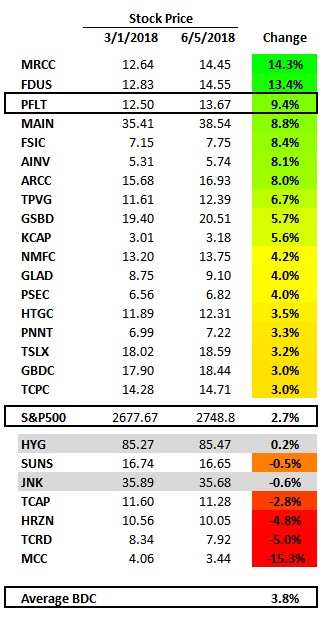

As mentioned in previous articles, most business development company (“BDCs”) have outperformed the S&P 500 since March 1, even before taking into account dividends paid:

PFLT insiders were purchasing additional shares near the recent lows:

I am expecting BDCs to continue higher for many reasons, including the recently announced strong Q1 2018 results reported by most BDCs, with higher portfolio yields and management guidance for increased portfolio growth potential in 2018. Also, many BDCs reported higher-than-expected earnings and dividend coverage with increased net interest margins.