Summary

- On June 15, 2018, GSBD shareholders overwhelmingly approved the application of the reduced asset coverage requirements allowing the company to double its leverage.

- Management has agreed to reduce its base management fee from 1.50% to 1.00% which would be among the lowest in the sector to help offset potentially lower yielding assets.

- As shown in this article, the increased leverage and reduced fees will likely result in higher earnings (and dividends) over the coming quarter even with lower yielding and ‘safer’ investments.

- I consider GSBD to a higher quality BDC for the reasons mentioned in this article and I purchased shares near the recent lows.

You can read the full article at the following link:

Recently Reduced Asset Coverage Ratio:

On June 15, 2018, Goldman Sachs BDC (GSBD) held its 2018 Annual Meeting of Stockholders and shareholders overwhelmingly approved the application of the reduced asset coverage requirements as disclosed in the recent 8-K filing:

Proposal 3: By the vote shown below, the stockholders approved the application of the reduced asset coverage requirements in Section 61(a)(2) of the Investment Company Act of 1940, as amended, to the Company, which permits the Company to double the maximum amount of leverage that it is permitted to incur by reducing the asset coverage requirement applicable to the Company from 200% to 150%. Approval of Proposal 3 required a majority of the votes cast by all stockholders present, in person or by proxy, at the Annual Meeting.

Borrowings & Fitch Credit Rating

On June 28, 2018, GSBD announced that it had priced an offering of $40 million of 4.50% convertible notes due 2022. Also, the company recently upsized its revolving credit facility to $695 million and extended the maturity date to February 2023.

Source: GSBD Earnings Call Slides

On June 18, 2018, GSBD announced that Fitch Ratings (“Fitch”) has assigned the company an investment grade rating of BBB-; the rating outlook is stable.

“We are pleased to receive an investment grade rating from Fitch, which we believe reflects both the quality of GSBD’s investment portfolio and the strength of Goldman Sachs Asset Management’s (“GSAM’s”) platform. We are particularly gratified by Fitch’s acknowledgment of GSAM’s differentiated risk management and proprietary loan sourcing capabilities in its assessment.” said Brendan McGovern, CEO of the Company.

Reduced Fee Structure & Lower Risk Portfolio

Management has agreed to reduce its base management fee from 1.50% to 1.00% which would be among the lowest in the sector to help offset potentially lower yielding assets and/or increased borrowing expenses as discussed on the May 4, 2018 earnings call:

“the company’s investment advisor will reduce its base management fee from 1.5% of gross assets to 1% of gross assets beginning immediately following shareholder approval. In addition the Board and GSAM considered that borrowing cost may increase as additional leverage incurred while asset yields may decline as the company pursues lower risk first lien assets. In an effort to support the increased returns on equity, that are the objectives of the proposed increasing leverage, both the Board and GSAM believe reduction in the base management fee is appropriate.”

Also discussed, was the ability to invest in a higher amount of first-lien loans with lower risk:

“we believe that the added balance sheet flexibility will allow us to pursue increased returns on shareholder equity, while also allowing us to invest in lower risk, lower yielding loans. Based on our existing maximum permitted debt-to-equity ratio of just these lower risk, low yielding loans are currently dilutive to our targeted shareholder returns. We expect that over time, our asset mix will shift toward a higher percentage of first lien loans that may have lower yields, but which we believe also carry a lower risk. Finally a lower asset coverage requirement gives the company an enhanced ability to make distributions to shareholders that are required under tax regulations”

Increased Leverage & Dividend Coverage Potential

I have recently used this analysis for Medley Capital (MCC), Oaktree Specialty Lending (OCSL) and Prospect Capital Corp. (PSEC) in the following articles:

- MCC – “This High-Yield BDC Will Be Cutting Its Dividend Soon“

- OCSL – “Expected Dividend Cut Of 20% To 36% This Week“

- PSEC – “Expected Dividend Cut Of 20% To 30%“

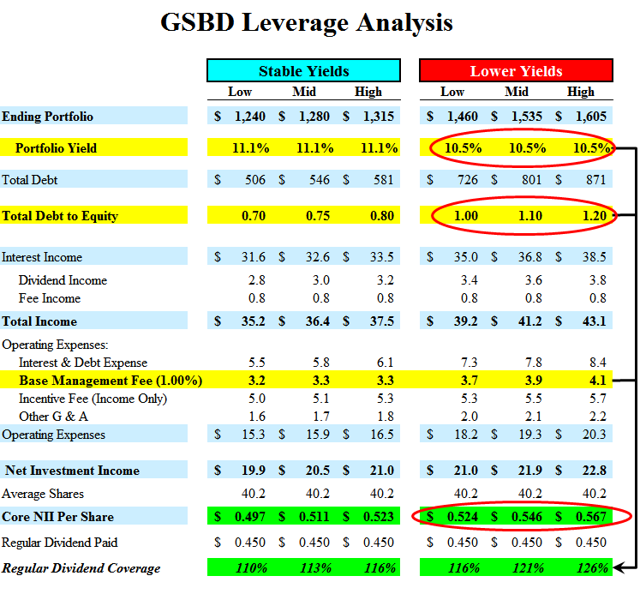

The following table shows six different scenarios with various amounts of leverage, using the current portfolio yield of 11.1% and a lower yield of 10.5%to determine the impacts on dividend coverage. Each of these scenarios assumes a full quarter of benefits from interest income but also a full quarter of interest expenses, incentive and 1.00% management fees. However, I have used conservative debt-to-equity ratios of 1.00 to 1.20 for the lower yield analysis compared to the potential 2.00 allowed with the reduced asset coverage ratio.