Summary

- I am predicting another monthly dividend increase to $0.195 per month to be announced before the company reports earnings on August 2, 2018, for the reasons discussed in this article.

- MAIN is the top-rated BDC by S&P Global Ratings that continues to grow its “per share” economics, including earnings and book value driving higher total returns to shareholders.

- This article also discusses increased NAV per share in Q2 2018 and when to purchase additional shares of this best-of-breed “sleep well at night” high-yield investment.

- Semiannual dividends continue to be supported with realized gains including the recent exits of Hydratec, Inc. and Soft Touch Medical Holdings for realized gains of $7.9 million and $5.2 million, respectively.

You can read the full article at the following link:

Reasons to Buy MAIN:

MAIN is clearly one of the best-managed BDCs for many reasons (some are discussed in this article) as the company continues to deliver higher total returns to investors through:

- Maintaining a much lower operational cost structure to maximize distributions to shareholders.

- Managing an efficient lower cost capital structure with conservative leverage.

- Well-timed highly accretive equity offerings.

- Conservative valuation and dividend policy with consistent coverage from NII and semiannual supplemental dividends.

- Quality of the origination/credit platform to build a portfolio to deliver consistent returns to shareholders while protecting the capital invested.

- No plans to seek “externalization” or higher leverage through reduced asset coverage ratio.

- Management is an active purchaser of shares each quarter, currently holding over $115 million.

- Continued involvement in regulatory aspects of the sector: “we’ve been much more focused on our legislative agenda with respect to BDC modernization, getting an SBIC bill passed in the House and Appropriations Bill has some really good language in it. The House Appropriations Bill that cleared the committee, real good in it language on the AFFE issue, which could reinstate us back into the indices.”

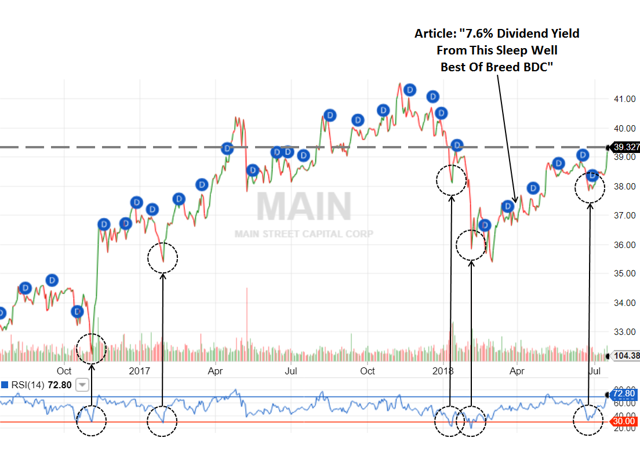

Purchasing Additional Shares of MAIN

As mentioned earlier this week in “Another Big Win Driving Special Dividends And 9% To 10% Yield,” I have been buying additional shares of higher quality business development companies (“BDCs”), especially given the oversold conditions driving higher yields. Many BDCs have been rallying over the last three to four months, likely for the reasons discussed in previous articles including:

- Rising interest rates and portfolio yields

- Poorly managed BDCs taken over and turned around

- Recent insider purchases

- Relaxed regulations and tax reform

Once I have selected a BDC that fits my personal risk profile (there are over 50 publicly traded BDCs, please be selective), I use momentum indicators such as Relative Strength Index or (“RSI”) from my BDC Google Sheets to help determine if a stock is ‘oversold’ or ‘undervalued.’ Most of my previous purchases of MAIN were when the stock had an RSI of 30 or below. The following definition of RSI is from Investopedia:

Traditional interpretation and usage of the RSI is that RSI values of 70 or above indicate that a security is becoming overbought or overvalued, and therefore may be primed for a trend reversal or corrective pullback in price. On the other side of RSI values, an RSI reading of 30 or below is commonly interpreted as indicating an oversold or undervalued condition that may signal a trend change or corrective price reversal to the upside.”

Over the last two years, MAIN has been near or below 30 multiple times and typically a good buying point: