Summary

- For Q2 2018, GSBD beat best case projections covering its dividend by 112% (average coverage of 113% over the last 8 quarters).

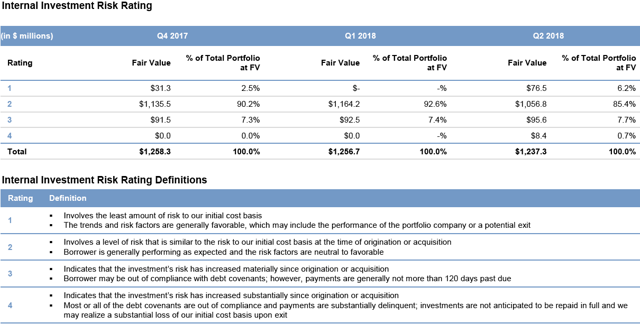

- Its $9 million first-lien position in Kawa Solar Holdings was added to non-accrual and marked down by $0.7 million during Q2 2018 and is the only investment with ‘Rating 4’.

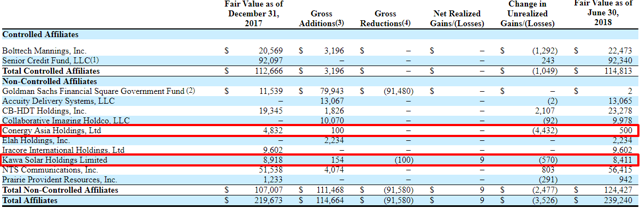

- Conergy Asia Holdings was also marked down by around $5.3 million in Q2 2018 “due to its capital condition” contributing to the slight decline in NAV per share.

- On June 15, 2018, shareholders approved the reduced asset coverage ratio of at least 150% potentially allowing a debt-to-equity of 2.00.

- Management has agreed to reduce its base management fee from 1.50% to 1.00% which would be among the lowest in the sector and I will include in the updated projections.

The following is a quick update that was previously provided to subscribers of Premium Reports on August 2, 2018. For target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs (including this one) please see Deep Dive Reports.

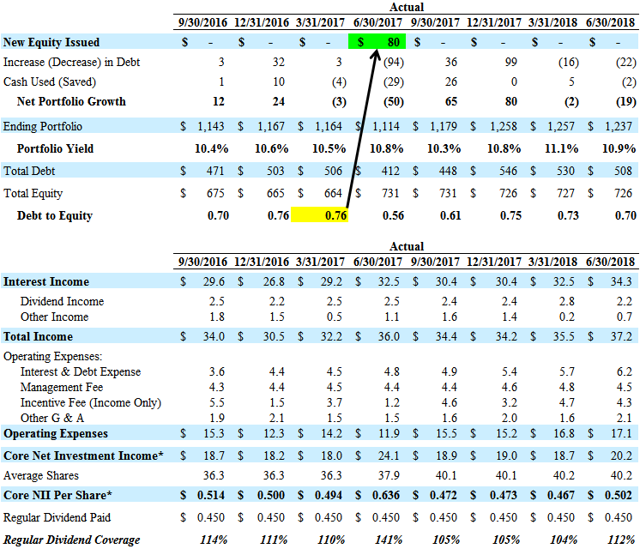

For Q2 2018, Goldman Sachs BDC (GSBD) beat my best case projections covering its dividend by 112% with a slight decline in portfolio investments and yield (from 11.1% to 10.9%). GSBD has covered its dividend by an average of 113% over the last 8 quarters and is now below its previous target leverage of 0.75. On June 15, 2018, shareholders approved the reduced asset coverage ratio of at least 150% potentially allowing a debt-to-equity of 2.00.

Management has agreed to reduce its base management fee from 1.50% to 1.00% which would be among the lowest in the sector to help offset potentially lower yielding assets and I will include in the updated projections.

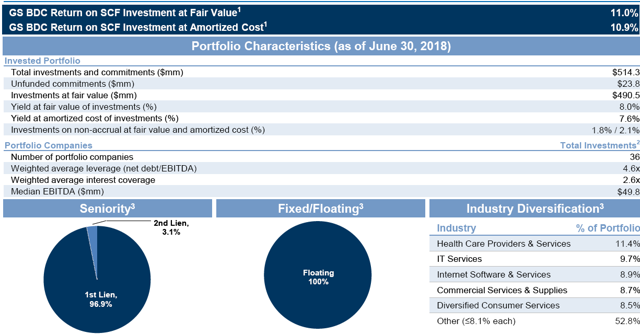

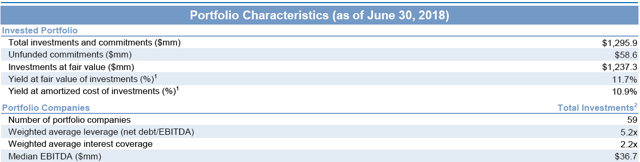

Is Senior Credit Fund (“SCF”) return on investment declined to 11% (previously 12%) and the overall size of the SCF portfolio remained mostly stable and continues to be the company’s largest investment at 7.5% of total investments at fair value.

![]()

Credit quality remained stable and non-accruals remain low at 0.7% and 0.8% of the portfolio fair value and cost, respectively. Its $9 million first-lien position in Kawa Solar Holdings was added to non-accrual and marked down by $0.7 million during Q2 2018 and is the only investment with a ‘Rating 4’ in the following table:

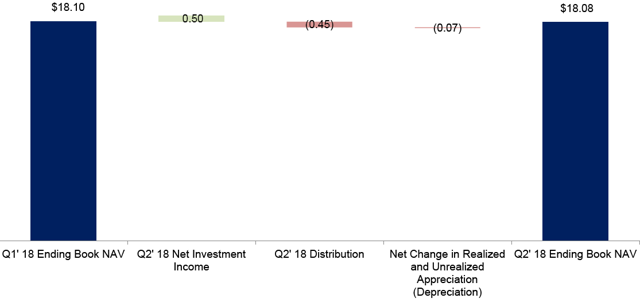

Conergy Asia Holdings was also marked down by around $5.3 million in Q2 2018 “due to its capital condition” contributing to the slight decline in net asset value (“NAV”) per share from $18.10 to $18.08. However, this investment has now been mostly written off with a current fair value of $0.5 million as shown in the table below.

From 10-Q: “Net change in unrealized appreciation (depreciation) in our investments for the three and six months ended June 30, 2018 was primarily driven by the unrealized depreciation in Conergy Asia Holdings, Ltd. due to its capital condition.”

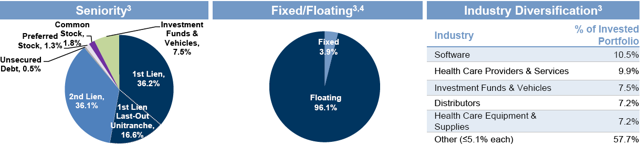

The portfolio remains heavily invested in first-lien debt including its SCF as shown below:

For target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs (including this one) please see Deep Dive Reports.