Summary

- HTGC is currently yielding 10% with RSI of 25 indicating ‘oversold’ and will rebound at some point, especially given the potential for a dividend increase as discussed in this article.

- Recent SEC filings for HCXY included updated portfolio information indicating slightly lower-than-expected portfolio growth and higher amounts of accretive share issuances.

- The BDC sector has been pulling back and I have started to make purchases of select BDCs but still hoping for lower prices in the coming weeks.

- As predicted, HTGC’s NAV per share recently increased by 5.1% due to previous share issuances and equity position in DOCU. Special Meeting for shareholders to approve higher leverage will be held on December 6, 2018.

- On September 6, HTGC announced that the SBA issued a “green light” letter for a third SBIC license for access to additional growth capital of $175 million. Final approval is anticipated to occur by the Q1 2019.

You can read the full article at the following link:

Please read the full article at the link provided above or sign up for Premium Reports that includes updated Deep Dive Reports on each BDC including this one.

Quick HTGC & BDC Buzz History

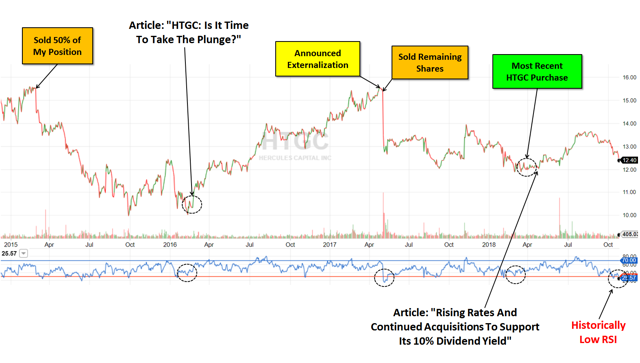

As many readers know, I am typically a ‘Buy and Hold’ investor making additional purchases during general market pullbacks (including this one) and only selling if there are serious issues. I have been investing (on and off) in Hercules Capital (HTGC) over the last 10 years and writing public articles on Seeking Alpha discussing the stock for over 5 years. Some of the most recent public articles were:

- February 19, 2016 – “Is It Time To Take The Plunge?” discussing my previous sale of HTGC at $15.02 and looking to repurchase shares. HTGC was trading at $10.56 with lower RSI as shown below.

- May 8, 2017 – “Hercules Capital: External Management Analysis” discussing the reasons for selling all my shares in HTGC due to the company seeking to be externally managed and the ‘math’ of reduced dividend coverage.

- April 30, 2018 – “Rising Rates And Continued Acquisitions To Support Its 10% Dividend Yield” discussing reasons to purchase higher quality BDCs including HTGC (no longer seeking externalization) that was trading lower with lower RSI as shown below.

- July 29, 2018 – “Upcoming 3% To 4% Book Value Growth For This 9.2% Yielding BDC” discussing upcoming the anticiapted increase in book value (or NAV) for HTGC.

It should be noted that I have not made additional purchases of HTGC since March 26, 2018, at $12.03.

Quick BDC Market Update

As shown above, HTGC’s stock price has pulled back, along with other Business Development Company (“BDCs”), for the reasons discussed earlier this week in “BDC Sector Volatility Driving 10.5% Average Yield“. I am expecting continued lower BDC prices for the reasons discussed in the article including the general widening of rate spreads. Please see the end of this article for the recent changes in stock price for each BDC including HTGC that is down 8% over the last two months compared to the average BDC at a 10% decline. However, there has been a wide range of recent performance from TPG Specialty Lending (TSLX) down less that 2% for the reason discussed in “TSLX: Upcoming Special Dividends & Shareholders Overwhelmingly Approve Increased Leverage” to NEWT down almost 25%.

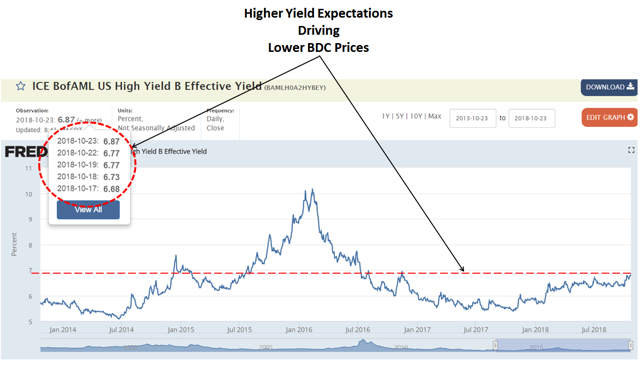

As shown below, the ‘BofA Merrill Lynch US Corporate B Index’ (Corp B) yield continues to rise and is now at its highest level since November 2016:

Source: FRED

The recent drop in HTGC’s stock price is not due to underlying fundamentals, but likely investor expectations of higher yields, which is not necessarily tied to higher expected defaults given the strong economic fundamentals. In fact, there is a good chance that the recent widening of yield spreads will be discussed on the upcoming earnings call as a positive tailwind for new investments and earnings in the coming quarters. HTGC will be reporting results next week and most of my personal trades are based on actual or projected changes in portfolio credit quality and dividend coverage.

Obviously, timing is important when investing, but especially with BDCs for many reasons, including opaque reporting standards, general sector volatility, and being largely retailed owned. The opaque and inconsistent reporting for BDCs often results in retail investors making poor decisions. Focusing on simple coverage of the dividend with the previous quarter net investment income (“NII”) or changes in net asset value (“NAV”) are not enough.

BDCs will begin reporting calendar Q3 2018 results this week. Please sign up for Premium Report to receive real-time notifications of changes in risk profile and dividend coverage potential for each company as they report results.