The following is a quick PSEC Update that was previously provided to subscribers of Premium Reports along with revised target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all business development companies (“BDCs”) please see Deep Dive Reports.

United Sporting Companies (“USC”) filed for bankruptcy today due to falling gun sales and tightening credit lines. The company plans to liquidate, hurt by falling sales after President Donald Trump was elected and as Dick’s Sporting Goods began moving away from firearms. In a court filing, Chief Executive Officer Bradley Johnson said USC boosted inventory before the 2016 White House race, expecting the higher sales that historically follow a Democrat’s election.

Other reasons for its Chapter 11 filing were excessive debt (including PSEC with $127 million at cost) and discounting caused by excess inventory. In its petition filed with the U.S. bankruptcy court in Wilmington, Delaware, USC said it had between $100 million and $500 million of liabilities. It plans to keep operating during the wind-down.

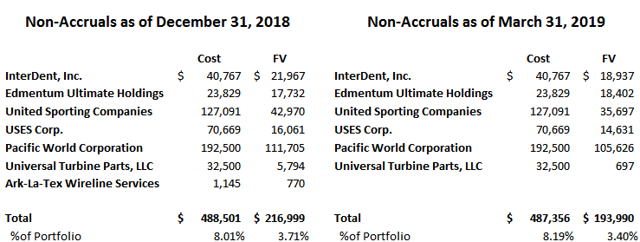

The amount of investments that PSEC had on non-accrual status declined from seven to six due to Ark-La-Tex Wireline Services written off during the quarter. Non-accruals remained around 8.2% of the portfolio at cost and declined to around 3.4% at fair value (previously 3.7%) mostly due to markdowns (discussed later) in calendar Q1 2019.

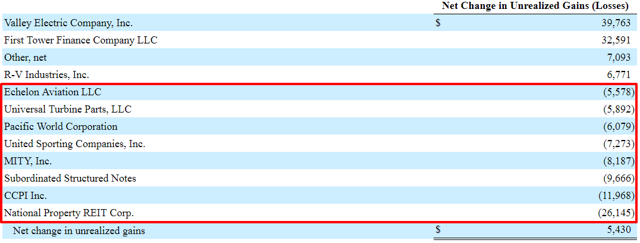

Similar to the previous quarter, many of the investments on non-accrual status were recently marked down including Pacific World, Universal Turbine Parts, LLC and United Sporting Companies. Other meaningful markdowns include its CLOs, National Property REIT Corp (“NPRC”) and CCPI Inc. However, these were offset by large markups in Valley Electric Company (similar to previous quarter) and First Tower Finance:

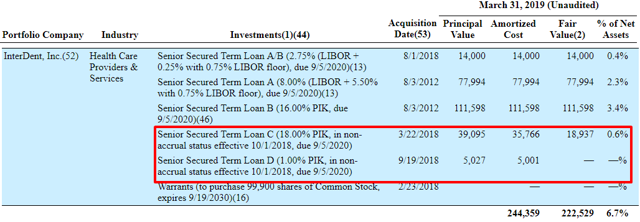

During calendar Q4 2018, PSEC added two of its loans to InterDent, Inc. and another one of its loans to Pacific World to non-accrual status. As mentioned in the previous report, some of my primary concerns include portfolio concentration issues including its “top 10 investments accounting for over 40% of the portfolio” and the amount of equity investments that continues to increase “accounting for over 16% of the portfolio”. Also mentioned was that “InterDent remains one of its largest investment and needs to be watched.” Previously, PSEC extended its loans to InterDent, which were past due as well as being marked down “but still marked near cost and likely overvalued”. During calendar Q2 2018, PSEC assumed control of InterDent and marked it down an additional $11 million and during Q3 2018 made additional investments.

As shown below, PSEC only placed around $41 million of the $244 million loans with InterDent on non-accrual. There is a chance that the other loans could be placed on non-accrual that would have a meaningful impact upcoming to dividend coverage. Also, InterDent still accounts for around $0.61 per share or 6.7% of NAV.

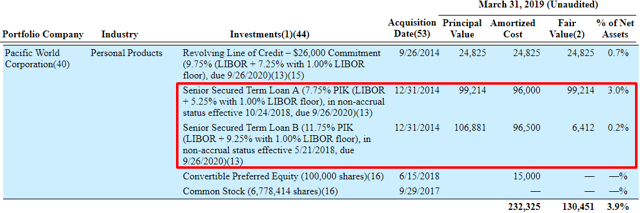

In October 2018, a $96 million loan to Pacific World was added to non-accrual status but is still marked up above cost as shown below and this investment accounts for around $0.36 per share or 3.9% of NAV.

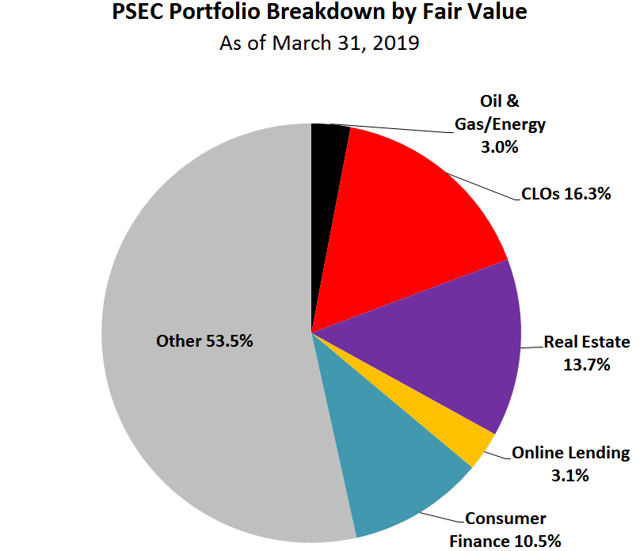

I consider PSEC to have a higher risk portfolio due to the previous rotation into higher yield assets during a period of potentially higher defaults and later stage credit cycle concerns, CLO exposure of 16% combined with real-estate 14%, online consumer loans of 3%, consumer finance of 11% and energy, oil & gas exposure of 3%. As mentioned in previous reports, Moody’s and S&P Global Ratings also considers the CLO, real-estate and online lending to be riskier allocations that currently account for over 33% of the portfolio.

Moody’s Investors Service/Standard & Poor’s Global Ratings:

Moody’s Investors Service: Baa3/ Outlook Stable

On February 26, 2019, Moody’s Investors Service (Moody’s) assigned a rating of to Prospect Capital Corporation’s (“PSEC”) senior unsecured convertible notes due 2025. The outlook for PSEC’s ratings is stable.

Moody’s could upgrade PSEC’s ratings if the company: 1) decreases debt/tangible equity to not more than .7x, doesn’t increase its structured credit and real estate exposures as a proportion of total investments, further enhances financial flexibility by obtaining prior shareholder consent to issue shares at a price below net asset value, and generates profitability that consistently compares well with BDC peers, taking into consideration differences in investment strategies.

Moody’s could downgrade the ratings if PSEC increases the ratio of net debt to equity to more than .85x, increases structured credit and real estate equity investments without decreasing leverage, pays dividends that exceed net investment income on a regular basis, or generates profitability that is weaker than expected compared to peers.

Standard & Poor’s Global Ratings: Credit Rating: BBB-/Outlook Stable

On October 12, 2018, S&P Global Ratings affirmed its ‘BBB-‘ issuer credit rating on Prospect Capital Corp. (“PSEC”) and previously removed the ratings from CreditWatch, where they were placed on April 3, 2018, with negative implications. The negative outlook was due to “PSEC’s leverage near the upper end of our expectations for the ratings and our view that certain of its investments may have more volatile valuations than typical BDC investments.” The stable outlook reflects S&P Global Ratings’ expectation that Prospect Capital Corp. (PSEC) will maintain reported debt to equity below 0.85x and will not adopt a modified asset coverage requirement from the current 200%. We expect PSEC will maintain investment portfolio results consistent with other BDCs that we rate investment grade.

We could lower the ratings over the next 12-24 months if:

- Reported debt to equity rises to 0.85x or higher or debt to ATE rises to 1.50x or higher

- The investment portfolio’s risk increases or performance deteriorates, as indicated by rising realized or unrealized losses or nonaccruals

We could raise the ratings if debt to ATE declines below 1.0x on a sustained basis and if PSEC substantially reduces its exposure to investments that we view as subject to greater volatility, particularly CLO equity. The ratings reflect PSEC’s broad capabilities as the second-largest BDC, with diversified origination channels, as well as its favorable funding profile. The company’s debt to equity leverage is low, but debt to ATE is higher than other BDCs we rate. We believe certain of PSEC’s investments may have more volatile valuations than typical BDC investments, particularly its investments in collateralized loan obligation (“CLO”) residual interests, online consumer loans, and real estate, all of which we deduct from ATE.

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.

For updated PSEC target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs please see Premium Reports.