The following is a quick TCPC Update that was previously provided to subscribers of Premium Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

TCPC Dividend Coverage Update:

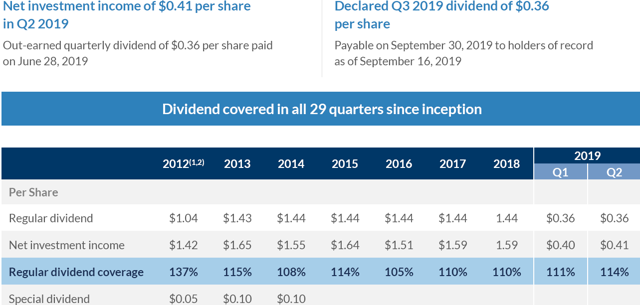

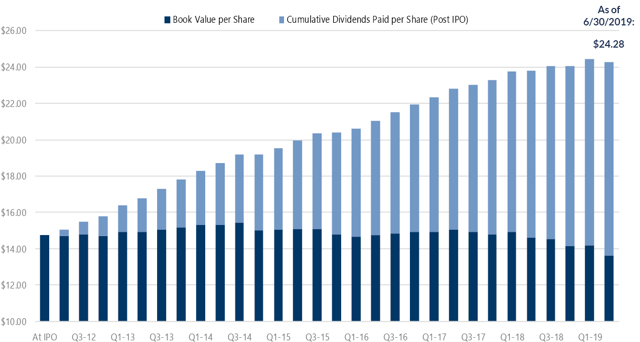

BlackRock TCP Capital (TCPC) continues to consistently over-earn its dividend growing its undistributed taxable income to almost $39 million spillover or $0.66 per share.

“We generated net investment income in the second quarter of $0.41 per share again exceeding our dividend of $0.36 per share. This extends our more than seven-year record of covering our regular dividend every quarter since we went public. Over this period on a cumulative basis, we’ve out-earned our dividends by an aggregate $39 million, or $0.66 per share based on total shares outstanding at quarter end.”

Dividend coverage for TCPC is not reliant on fee and dividend income, some of which is amortized over the life of the investment, reducing the potential for “lumpy” earnings results.

“Our income recognition follows our conservative policy of generally amortizing upfront economics over the life of an investment, rather than recognizing all of it at the time the investment is made.”

Previously, management indicated that the company will likely retain the spillover income and use for reinvestment and growing NAV per share and quarterly NII rather than special dividends:

“As we talked with shareholders we reached the conclusion although opinions weren’t universal on this that most people didn’t seem to value them that much and we thought that retaining the spill-over income seem to be better received.”

“So while we do look at our dividend from time-to-time and want to make sure it’s an appropriate level, our primary focus is on continuing to make sure that we keep up that record of covering our dividend each quarter.”

However, management indicated that the recent shareholder approval to increase leverage will likely drive higher earnings and “will continue to assess our dividend policy going forward”:

“As you’re aware, our shareholders just voted overwhelmingly to give us the ability to increase leverage, and we’ve been earning our dividend very comfortably without that. So as we talk about our board we will continue to assess our dividend policy going forward. As our balance sheet and income statement may change over time, we will continue to analyze that have discussions with our board reflect the views of other important constituents and continue to reassess our dividend policy. ”

For the quarter ended June 30, 2019, TCPC reported between base and best case projections covering its dividend by 113% that included $0.05 per share of income related to prepayment premiums and accelerated original issue discount amortization. However, there was a meaningful increase in the amount payment-in-kind (PIK) income (from 5% to 10% of total income) and needs to be watched.

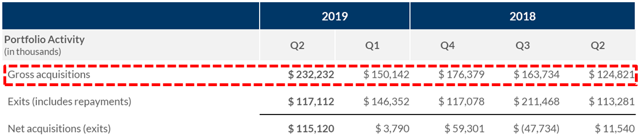

Howard Levkowitz, TCPC Chairman/CEO: “We out-earned our dividend for the 29th consecutive quarter, generating strong investment income and robust originations in the second quarter. Originations totaled $232 million for the quarter. We leveraged our existing relationships with borrowers and deal sources as well as the BlackRock platform’s resources to deepen relationships with existing clients and to engage new borrowers.”

“New investments during the quarter had a weighted average effective yield of 9.7% and the investments we exited had a weighted average effective yield of 12.3%. While our average new investments were lower-yielding than the investments we exited this quarter, we would caution against viewing any one quarter as a trend. The overall effective yield on our debt portfolio at quarter end was 11% compared to 11.4% at the end of the last quarter. If you look at the overall change in yields about half of that is just decreases in LIBOR. And some of the rest of it particularly the pronounced difference on the exits include a couple of higher-yielding things like Envigo that we mentioned earlier.”

The non-accrual loans to Fidelis Acquisitions, LLC (discussed later) were partially taken out of investment income during Q2 2019 and was easily offset by higher-than-expected portfolio growth and dividend income during the quarter.

Q. “Is a full quarter taken out of the second quarter earnings, or is only a partial quarter of Fidelis taking out of quarterly earnings?”

A. “We stopped accrual at the end of May. So there’s two months of Fidelis. But I would note, when we computed the incentive fees it was excluding, anything that we accrued.”

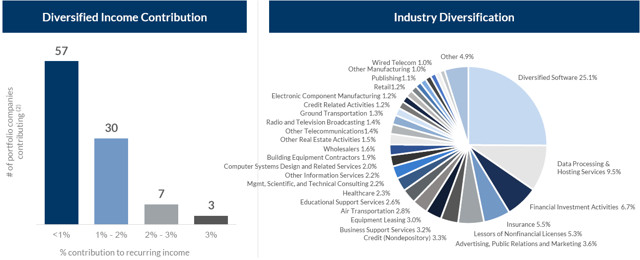

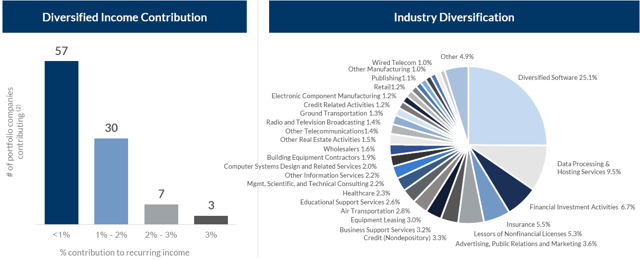

As shown below, TCPC’s portfolio is highly diversified by borrower and sector with only three portfolio companies that contribute 3% or more to dividend coverage:

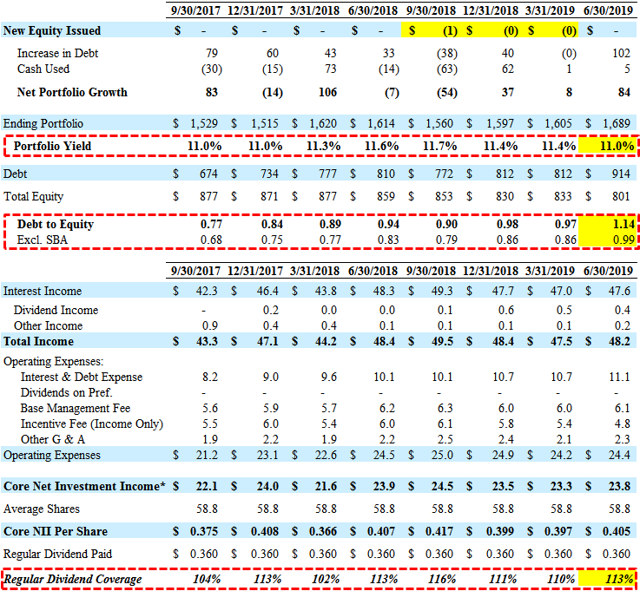

On August 6, 2019, the Board re-approved its stock repurchase plan to acquire up to $50 million of common stock at prices below NAV per share, “in accordance with the guidelines specified in Rule 10b-18 and Rule 10b5-1”. During Q1 2019, there were only 9,000 shares repurchased and in 2018, the company repurchased only 73,416 shares for a total cost of $1.0 million. There is a good chance that the company will repurchase additional shares if the stock price declines below NAV again which is now $13.64 (reduced asset coverage ratio and higher leverage can be used for accretive stock repurchases).

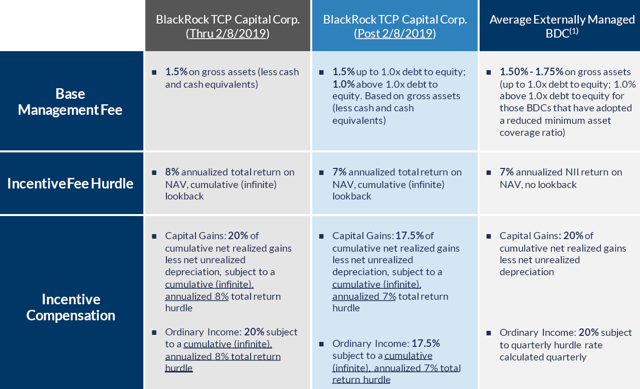

On February 8, 2019, shareholders approved the reduced asset coverage ratio allowing higher leverage and reduced management fee to 1.00% on assets financed using leverage over 1.00 debt-to-equity, reduced incentive fees from 20.0% to 17.5% and hurdle rate from 8% to 7% as well as “continue to operate in a manner that will maintain its investment grade rating”.

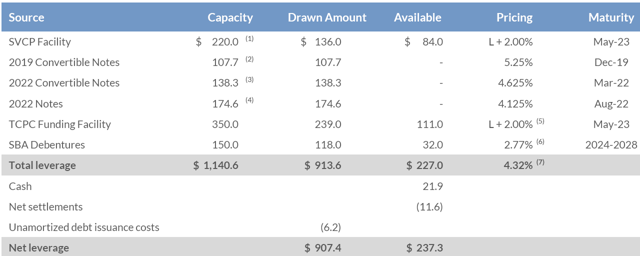

TCPC continues to lower its cost of capital and in May 2019, expanded its credit facilities by $50 million each for a total increase in capacity of $100 million as well as reducing the rate on its SVCP Facility by 0.25% to LIBOR + 2.0% and extended its maturity to May 6, 2023.

“During the second quarter we also reduced the interest rate on our SVCP facility by 25 basis points to LIBOR plus 200, and extended the maturity of both facilities to May 2023. The increased capacity reduced cost and extended maturities of our credit facilities further expand our diverse leverage program which includes two low-cost credit facilities, two convertible note issuances, a straight unsecured note issuance and an SBA program.”

As of June 30, 2019, available liquidity was $237 million, including $227 million in available leverage capacity and $22 million in cash and cash equivalents, reduced by approximately $12 million in net outstanding settlements of investments purchased. However, effective August 6, 2019, the company expanded the total capacity of its SVCP Facility by $50.0 million to $270.0 million. On November 7, 2018, Moody’s Investors Service initiated an investment grade rating of Baa3, with stable outlook. On November 8, 2018, S&P Global Ratings reaffirmed its investment grade rating of BBB-, with negative outlook. Both ratings include consideration of the Company’s reduced asset coverage requirement.

“We had total liquidity of $237 million at quarter end. This included available leverage of $227 million and cash of $22 million reduced by net pending settlements of $12 million. Since the beginning of the second quarter, we have expanded our credit facility capacity by a total of $150 million, which includes an incremental $50 million on our SVCP facility that we added earlier this week.”

“Outstanding draws on our $150 million SBA program increased to $118 million at June 30 as we added two new portfolio companies to the SBIC. The increased leverage flexibility following shareholder approval of our reduced regulatory coverage ratio allowed us to take advantage of attractive investment opportunities during the quarter.“Regulatory leverage at quarter end which is net of SBIC debt was 0.99 times common equity on a gross basis and 0.98 times net of cash and outstanding trades. Our investment-grade rating was reaffirmed by Moody’s in June and we’re proud to continue to be one of only three BDCs with both 2:1 leverage flexibility and an investment-grade rating from both Moody’s and S&P.”

TCPC management continues to take a higher quality approach including selective portfolio growth, with adequate protective covenants, at higher yields for improved dividend coverage. I am expecting the company to maintain its portfolio yield over the coming quarters:

“Both new and exited investments during the quarter co-incidentally had a weighted average effective yield of 10.1%. The overall effective yield on our debt portfolio at quarter end remained unchanged from the prior quarter at 11.4%.”

TCPC currently does not have a “joint venture” or “senior loan program” that uses off-balance sheet leverage to increase its overall portfolio yield. BDCs are allowed a maximum of 30% of investments to be considered ‘non-qualified’ that would include these types of investments:

From previous call: “We may consider doing some other things with 30% bucket. We’ve just have a very cautious approach to how we use that and wanted to make sure that it’s something that really fit with our strategy. So, the way we think about it is, it really is a continuation of what we’ve been doing, albeit with the resources of the world’s largest asset manager in many ways to help us do what we’ve been doing.”

Previously, TCPC completed a direct equity offering of 2.3 million shares in an effort to increase the ownership of longer-term institutional investors similar to the converted $30 million note and institutional support from CNO Financial Investments Corp. (CNO). CNO is an NYSE listed insurance holding company with over $30 billion in assets and is committed to investing more than $250 million of capital that will be deployed over time in TCP’s managed funds.

TCPC Risk Profile Update:

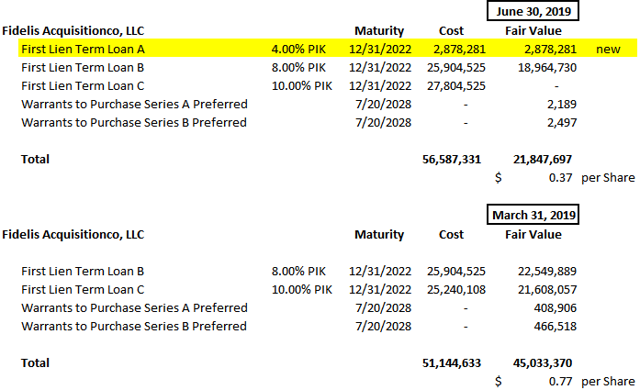

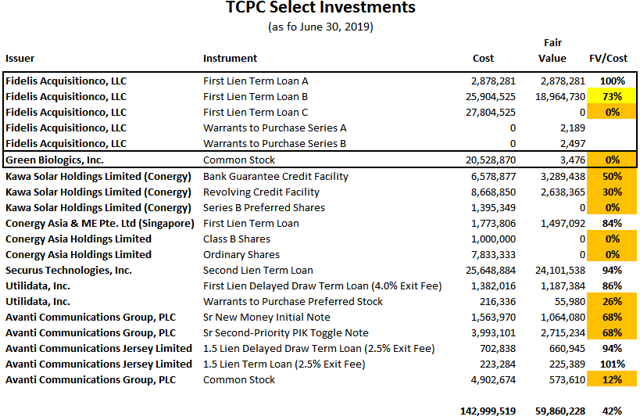

TCPC’s net asset value (“NAV”) per share declined by $0.54 or 3.8% (from $14.18 to $13.64) mostly due to unrealized losses related to adding Fidelis Acquisitions, LLC (“Fidelis”) to non-accrual resulting in $28.6 million or $0.49 per share of losses. Previously discussed Green Biologics was marked down an additional $3.2 million or $0.05 per share. Fidelis still accounts for around 1.3% of the portfolio and $0.37 per share of NAV.

Howard Levkowitz, TCPC Chairman and CEO: “While our overall portfolio is strong, our net asset value declined 3.8% in the quarter, almost entirely due to one underperforming investment. Looking ahead, we have a solid pipeline of new investment opportunities and believe we are well-positioned to continue to deliver attractive risk-adjusted returns to our shareholders.”

“Net unrealized losses of $34.6 million or $0.59 per share were primarily attributed to the write-down of our investment in Fidelis, most of which we placed on non-accrual during the quarter and which comprised 1.1% of our portfolio at fair value at June 30. No other loans were on non-accrual at quarter end and the credit quality of our portfolio is strong.”

Management discussed Fidelis on the recent call including making changes to management:

“While our investment portfolio remained strong overall, our net asset value declined 3.8% during the second quarter. This decline was almost entirely due to a write-down of our investment in Fidelis, a cyber security solutions provider that has significantly underperformed our expectations. Our initial investment in Fidelis, which we made in 2015 was at a relatively low loan-to-value and was made alongside a well-regarded private equity firm whose cash equity investment was nearly three times our debt. Fidelis initially performed to plan, but subsequently struggled in an increasingly competitive sector. After implementing several growth initiatives, customers are reacting favorably and sales have increased. However, liquidity is challenging, as revenue growth has yet to outpace costs. During the second quarter, it became clear, that notwithstanding several add-on investments from the sponsor, the company’s liquidity position no longer support its valuation. As a result, we recorded a $28.6 million unrealized loss and place the loans on non-accrual. We are disappointed by this result and are continuing to work closely with management and the sponsor to maximize value. The credit quality of the remainder of our portfolio is strong. Across the middle market, we are seeing mostly isolated credit events that appear to be more idiosyncratic and not indicative of widespread issues.”

“The company faced some challenges. Partly this was the marketplace, but to be honest a lot of it was self-inflicted issues from management. And leveraging our sort of experience and working with companies from our such a situation heritage and the owners we really worked to improve those shortfalls. And that included a change in management. That included several additional fundings on the business. And what we have seen since that time over the last several quarters is the impact — the positive impact on that from improvements in revenue bookings all the things you want to see happen on the income statement. The challenge and really to answer your question is the balance sheet challenges and the impact of that shortfall on continuing this recovery was notable and perhaps during the quarter became more evident and more pronounced where one impacts the other. And this isn’t a valuation that hasn’t changed over time.”

“It has changed over the last several years, but really where you saw the impact — where it’s less evident was in the equity of the junior tranches. And this quarter with the mitigation of our coverage and actually reduction of our coverage in the junior tranche — the C tranche you’re seeing a more pronounced and disproportionate effect in our piece, but the valuation has declined over time partly due to performance and partly due to just the market multiples which have also come down. So I think it’s harder to see that in any one quarter because of what we disclosed and what the overall valuation decrease has been. But you are seeing in this quarter a more notable impact where we’re affected in a straight waterfall to your point that over time where the equity has eaten more of the valuation deterioration. The term loan C; the increase is a function of PIK interest. Part of our — one of our latest efforts with the company and a restructuring of our position had us have a PIK position that is accretive into the C. So we did fund some additional money into the business but that is in the term loan A. So but specifically to your question on the amount of the C that was written down, that was not new funding. That was accretion. ”

The overall credit quality of the portfolio remains strong, with 92% of the portfolio in senior secured debt (mostly first-lien positions) and low non-accruals and low concentration risk:

“Our largest position represented only 3.2% of the portfolio and taken together our five largest positions represented only 14.9% of the portfolio. Furthermore, as the chart on the left side of slide 6 illustrates, our recurring income is distributed across a diverse set of portfolio companies. We are not reliant on income from any one portfolio company. In fact, on an individual company basis well over half of our portfolio companies, each contribute less than 1% to our recurring income. We have been pleased and surprised, in fact, with how little we’re hearing from companies about the impact of tariffs. In fact, there’s only one company that was directly citing it as being a material issue for their business. Now having said that, it’s still early in this next round and it’s not always immediately clear to people. And sometimes the impacts may be two or three layers away, and so it may take a while to filter through. But so far our emphasis on non-cyclical companies with a more domestic focus, I think, has benefited us pretty significantly with respect to tariffs.”

As mentioned in the previous report, its debt investments in Green Biologics were restructured into common equity and discussed on a previous call: “Green Bio missed projections, but received an equity infusion from its strategic owner during the quarter.” Kawa Solar Holdings was previously on non-accrual but restructured in Q3 2018 and is now in the process of “winding down”. Other investments that need to be watched include Securus Technologies, Inc., Conergy, Utilidata, Inc. and Avanti Communications Group.

As mentioned earlier, management has been slowly growing the portfolio (or shrinking if needed) and only investing in “the right type of structures with protections including covenants”.

“The direct relationships we form with borrowers as part of this process help to protect TCPC and its shareholders. The BlackRock TCP team is structured so that deal team members source, structure and monitor investments to ensure interests are aligned over the life of an investment. And finally, our team has deep experience in both performing and distressed credit, and we draw upon this expertise to structure deals that are downside protected. In closing, we remain relentlessly focused on generating superior risk adjusted returns for our investors, while preserving capital with downside protection.”

![]()

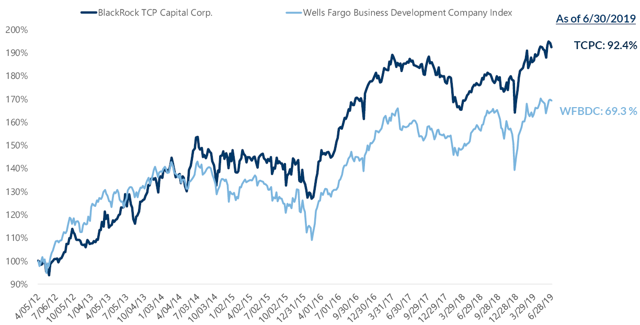

“TCPC has outperformed the Wells Fargo BDC Index by 33% over the same period. Over the past few years we have seen many new entrants into direct lending and substantially more capital seeking investment opportunities in the middle market. Against this backdrop being part of the world’s largest global asset manager greatly enhances our ability to source deals and build upon TCP’s successful 20 year track record in direct lending.”

Quality of Management & Fee Agreement:

The primary advantages for TCPC investors are its investor-friendly fee structure protecting total returns to shareholders on a cumulative basis by taking into account capital losses when calculating the income incentive fees (“total return hurdle”) and lower cost of capital, which have resulted in superior dividend coverage, previous special dividends and growing undistributed ordinary income.

As mentioned earlier, on August 6, 2019, the Board re-approved its stock repurchase plan to acquire up to $50 million of common stock at prices below NAV per share, “in accordance with the guidelines specified in Rule 10b-18 and Rule 10b5-1”. During Q1 2019, there were only 9,000 shares repurchased and in 2018, the company repurchased only 73,416 shares for a total cost of $1.0 million. There is a good chance that the company will repurchase additional shares if the stock price declines below NAV again which is now $13.64 (reduced asset coverage ratio and higher leverage can be used for accretive stock repurchases).

From previous call: “With our stock trading at a small discount to NAV during the quarter we made modest share repurchases under our algorithm based share repurchase program.”

The company has the ability to issue shares below NAV but I do not see this as a “red flag” given the quality of management.

“Consistent with prior years and in line with many of our BDC peers, we have included in our proxy a proposal for shareholder approval to issue up to 25% of our common shares on any given date over the next 12 months at a price below net asset value. The purpose of the below NAV issuance proposal in our proxy is to provide flexibility. To be clear, at this point, we do not intend to issue equity below NAV, and certainly not unless it is accretive to our shareholders. This is basically an insurance policy, which our shareholders have approved every year since we went public.”

I consider TCPC to have higher quality management for many reasons including its updated fee agreement, conservative dividend and accounting practices (recognizing fee income over the life of the investment), insider ownership, strong underwriting standards and measured approach when raising and deploying capital.

This information was previously made available to subscribers of Premium BDC Reports, along with:

- TCPC target prices and buying points

- TCPC risk profile, potential credit issues, and overall rankings

- TCPC dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.