The following is an update that was previously provided to subscribers of Premium Reports providing target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

![]()

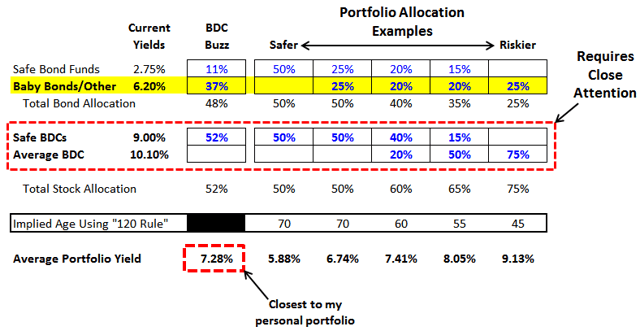

Over the coming weeks, I will be spending more time discussing Baby Bonds that currently yield around 6% and much less volatile than stocks even during extreme scenarios experienced in December 2018 where I made multiple purchases of BDC stocks, bonds, and preferred shares. My personal portfolio includes various other bonds some of which are tax-related and likely not applicable to most but included in “Other” along BDC Baby Bonds shown below. Together these investments account for around 37% of my portfolio and this report will discuss all of my recent purchase and returns.

Subscribers of Premium Reports will receive real-time announcements of all upcoming purchases of BDC Baby Bonds and preferred shares but please be aware that these have lower returns and are not expected to outperform the S&P 500 or upcoming BDC stock purchases. However, these investments will easily outperform during volatility and/or downturn while continuing to provide a relatively safe and stable yield as they are senior to the common stocks. Also, I am constantly monitoring the balance sheets of BDCs which provide insight for bond risk measures including portfolio credit quality, changes to leverage, interest coverage ratios and redemption risk such as GAINM as discussed in the GAIN Deep Dive report.

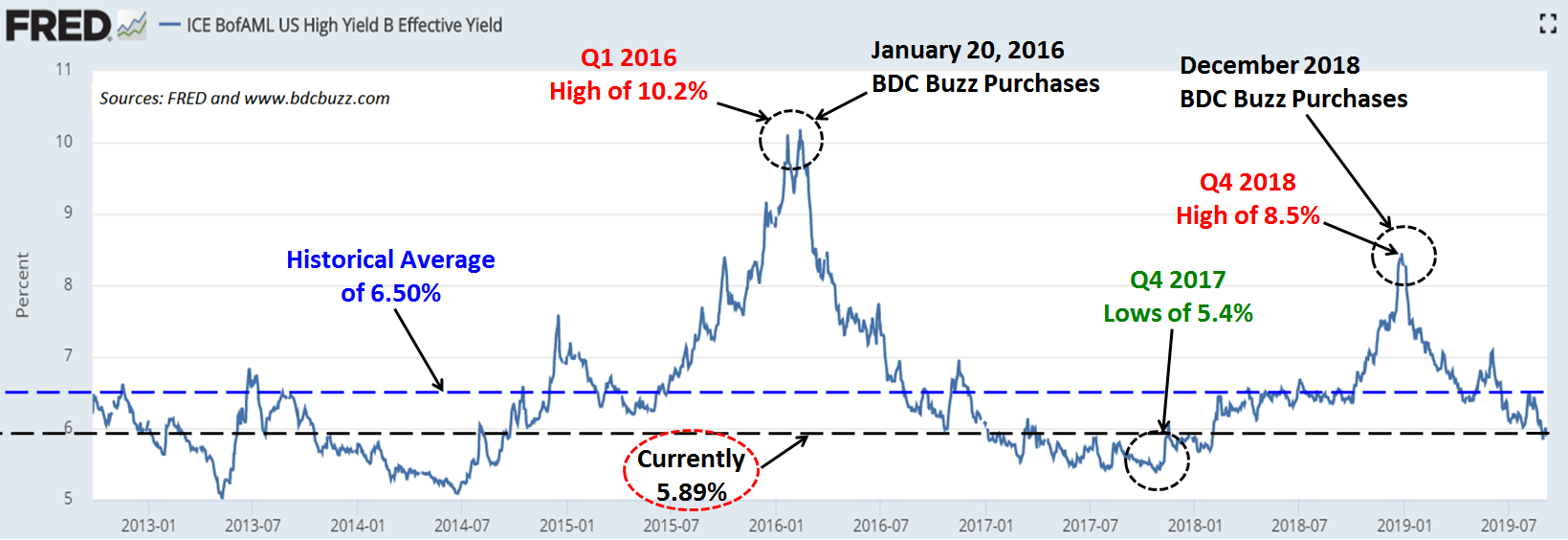

Bond pricing is closely correlated to expected investment yields including other non-investment grade debt and ‘BofA Merrill Lynch US Corporate B Index’ (Corp B) that previously increased to 8.45% on December 26, 2018.

As discussed in previous updates, these yields have been declining in 2019 and are currently around 5.89%. This is meaningful for many reasons but mostly due to indicating higher (or lower) yields expected by investors for non-investment grade debt.

Baby Bonds Basics:

- BDC Baby Bonds trade “dirty” which means that there is a certain amount of accrued interest in the market price. I have included the amount of accrued interest that updates daily.

- The ‘effective yield’ is based on the current price less accrued interest.

- Investors should use limit orders when purchasing exchange-traded debt such as Baby Bonds.

- You need to own the Baby Bond one trading day before the ex-dividend date to be eligible for the full quarter of interest.

- It is important to take into account which BDCs are “callable” and the potential for capital losses during the worst-case scenario.

- I do not actively cover some of the BDCs with baby bonds, especially if they are thinly traded.

I will discuss various details related to investing in Baby Bonds and preferred shares over the coming weeks including redemption risks and the timing of purchases as well as my upcoming purchases and limit orders. One of the metrics used to analyze the safety of a debt position is “Interest Expense Coverage” ratio which measures the ability to pay current borrowing expenses. From Investopdia:

“The interest coverage ratio is used to determine how easily a company can pay their interest expenses on outstanding debt. The ratio is calculated by dividing a company’s earnings before interest and taxes (EBIT) by the company’s interest expenses for the same period. The lower the ratio, the more the company is burdened by debt expense. When a company’s interest coverage ratio is only 1.5 or lower, its ability to meet interest expenses may be questionable.”

“The ratio measures how many times over a company could pay its outstanding debts using its earnings. This can be thought of as a margin of safety for the company’s creditors should the company run into financial difficulty down the road. The ability to service its debt obligations is a key factor in determining a company’s solvency and is an important statistic for shareholders and prospective investors.”

I have included the “Interest Expense Coverage” ratio in the Leverage Analysis and financial projections for GLAD and GAIN using net investment income before interest expense divided by interest and debt expenses for each quarter. GLAD has a historical ratio between 3.2 and 3.8 and projected to be between 3.1 and 3.4 in the coming quarters. It should be noted that this is higher than GAIN historically between 2.0 and 3.3 and projected to be between 2.4 and 3.0 in the coming quarters.

Over the coming weeks, I will include this ratio for all BDCs that have Baby Bonds so that subscriber can compare.

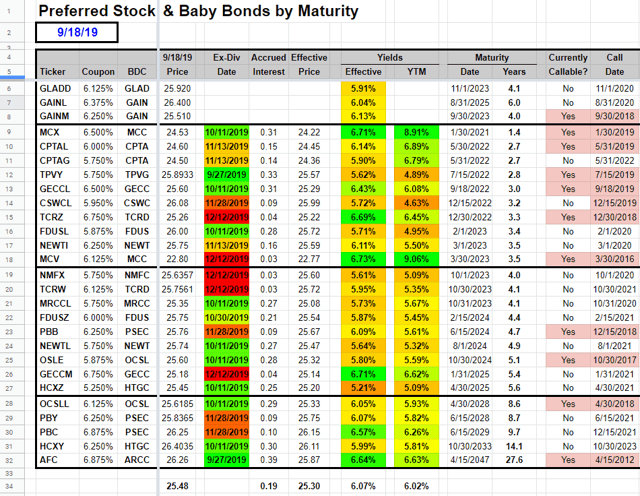

BDC Baby Bonds and Preferred Stocks are currently averaging 6.07% yield as shown in the following table including some that are considered investment grade. Please read “Baby Bonds For BDCs: Price Stability” for previous discussions and information about these investments.

The following is from the BDC Google Sheets and is what I use to make purchases when increasing allocations:

How much of your portfolio should be in stocks and bonds?

Your portfolio allocations depend on a few factors including your age. Historically, investment advisors used the “100 minus your age” axiom to estimate the stock portion of your portfolio.

- For example, if you’re 50, 50% of your portfolio should be in stocks.

That has been updated to 110/120 due to the change in life expectancy and lower interest rates for risk-free and safer investments. Today, 10-year treasury-bill yields just over 2% annually compared to 10% in the early 1980s. Please see Bloomberg article “U.S. Is Heading to a Future of Zero Interest Rates Forever“.

The previous table uses 120 as I believe interest rates will remain low given the changes to various policies from central banks and investors will continue to have equity investments for an adequate yield from their portfolios.

- For further reading on allocations, try stock allocation rules from Investopedia and Determining Asset Allocation By Age

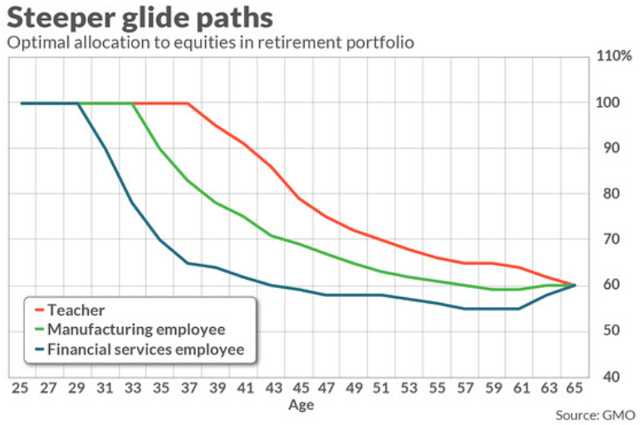

The following chart uses a different approach that seems more aggressive and is discussed in “Is your retirement portfolio too heavily invested in equities?” from MarketWatch.

General Bond Funds

There are plenty of choices when it comes to bonds including government bonds such as treasuries, municipal bonds, or corporate bonds. Within each of those categories, there is a wide variety of maturities to select from, ranging from a matter of days to 30 years or more. And there is a full range of credit ratings, depending on the strength of the bond’s issuer.

To make it easy, many investors use a bond-based mutual fund or ETF that fits their needs. The primary reasons for allocating a portion of your portfolio to bonds are to offset the stock volatility and a reliable income stream as compared to capital gains or beating the market.

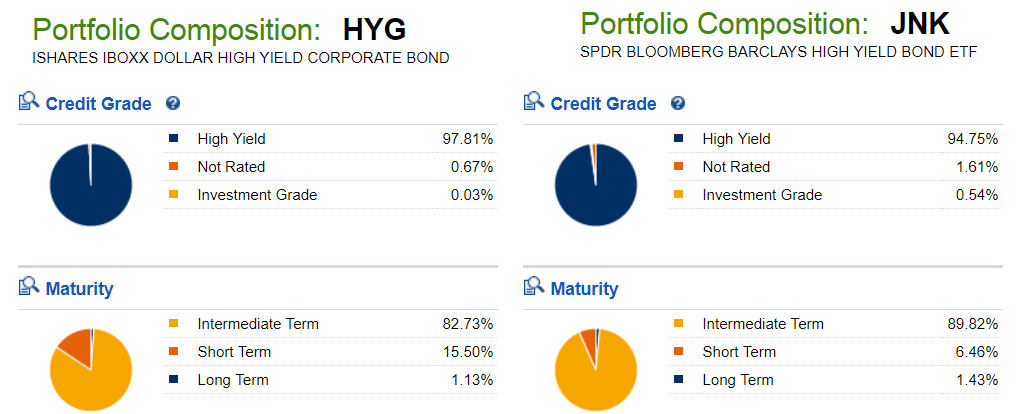

There are plenty of higher yield bond funds that typically invest in non-investment grade assets such as HYG and JNK that were discussed in a previous article “Search For Yield: Bond Funds Vs. BDCs Paying 10%+“. Currently, HYG and JNK are yielding 5.2% and 5.6%, respectively.

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.