The following is from the SUNS Deep Dive that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

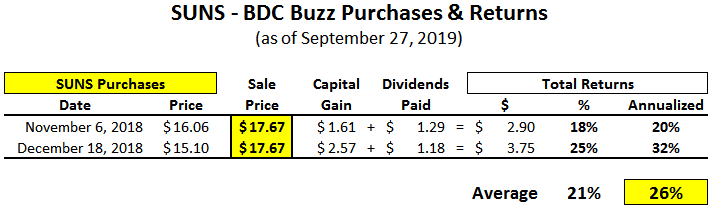

On September 27, 2019, I sold my position in SUNS at an average price of $17.67 for the reasons mentioned in the updated SUNS Deep Dive report including likely NAV per share decline of 1.7% related to American Teleconferencing Services, increased reliance on fee waivers, current pricing well above its short-term target price and RSI of over 70 as shown in the BDC Google Sheets.

SUNS Risk Profile Update

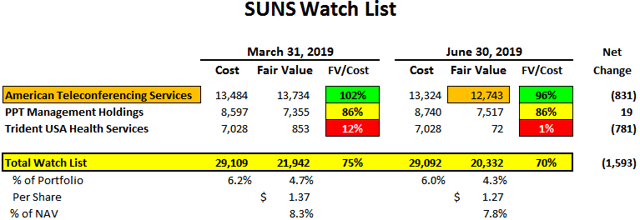

During Q2 2019, SUNS’s net asset value (“NAV”) per share decreased slightly by $0.06 to $16.34 per share due to net unrealized losses including additional markdowns of its investment in American Teleconferencing Services and mostly writing off its only non-accrual investment Trident USA Health Services. SUNS had net realized gains of $0.1 million primarily related to the exit from its investment in Mavenir Systems, Inc.

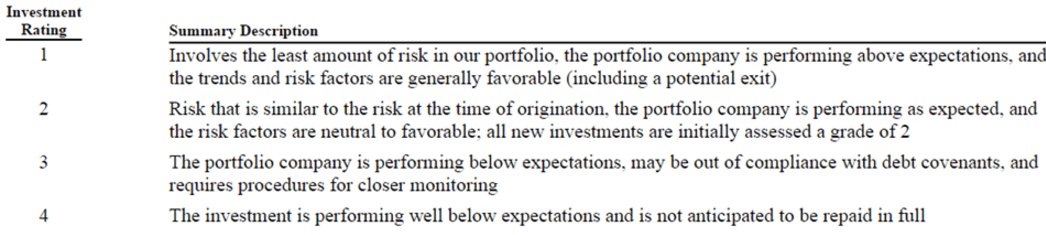

Trident USA Health Services (cost of $7.0 million, fair value of $0.1 million) was previously added to non-accrual status and mostly written off during the recent quarter. Trident now accounts for 0.0% of portfolio fair value and is the only portfolio company with an “Internal Investment Rating 4” implying that the investment is “performing well below expectations and is no anticipated to be repaid in full.”

From previous call: “Trident is a health care provider in the mobile diagnostics business. To your point, it is a small position for us but we treat every position as if it’s our only position. And so we have been working this one. We’ve been an investor for a few years early on. We actually were a second lien lender a number of years ago. And in the health care sector, they’re not facing anything that is systematic to either the economy or the health care sector, they just have had some headwinds in terms of what’s going on at home health and some of the competitive dynamics there as well as some billing and collection issues, which we have seen from time to time in some of these health care rollouts. So it is very specific to Trident. And is not in any way an indication of what’s going on either in our portfolio, the economy or the health care sector broadly.”

The following is from the recent earnings press release and my primary concerns are the “Internal Investment Rating 3” which are investments “performing below expectations, may be out of compliance with debt covenants”:

“Our internal risk assessment maintained an approximately two rating when measured at fair market value based on our one to four risk rating scale with one representing the least amount of risk. And at June 30, our watch list represented approximately 4% of our portfolio.”

—

The following table shows my watch list investments which are likely the same “Internal Investment Rating 3” investments included in the previous table.

—

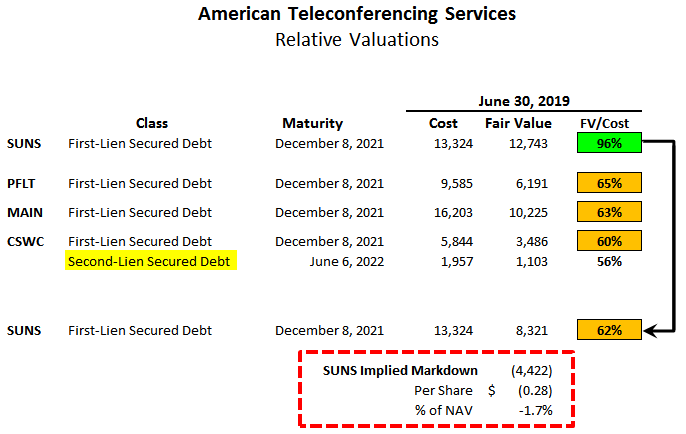

There is a good chance that American Teleconferencing Services (“ATS”) is still overvalued as other BDCs have the same investment valued at an average of 62% of cost compared to SUNS at 96% of cost. I am expecting additional unrealized losses in Q3 2019 related to this investment which will likely result in a 1.7% decline in NAV per share unless there are positive developments with this investment. However, it should also be pointed out that CSWC, MAIN and PFLT have conservative valuation practices as mentioned in their respective reports.

As discussed in the recently updated CWSC Deep Dive report, ATS operates as a subsidiary of Premiere Global Services (“PGi”), offering conference call and group communication services. On January 28, 2019, Moody’s downgraded PGi’s debt to Caa2:

Moody’s: “The downgrade of the CFR reflects Moody’s view that PGi’s EBITDA will deteriorate significantly over the next 12 months. Given PGi’s challenges, Moody’s believes that the company’s ability to meet covenants beyond 2Q 2019 is highly uncertain and the capital structure is unsustainable. The risk of default and debt impairment is high given the continuing erosion in revenues and EBITDA. PGi has proposed amendments to its existing credit agreements to waive the total leverage covenant for 2Q 2019 and a potential going concern qualification requirement in its 2018 financial statements. The company also expects to complete the sale of certain non-core assets in the near term, which management believes, along with the equity support, will provide the company adequate liquidity through 2019 to execute on its plans to commercially offer a new UCaaS offering. The continuing support from financial sponsors’ is credit positive. However, Moody’s believes that the proposed amendment and equity infusion will only improve PGi’s liquidity on a short-term basis.”

This information was previously made available to subscribers of Premium BDC Reports, along with:

- SUNS target prices and buying points

- SUNS risk profile, potential credit issues, and overall rankings

- SUNS dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.