The following is from the TPVG Deep Dive that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

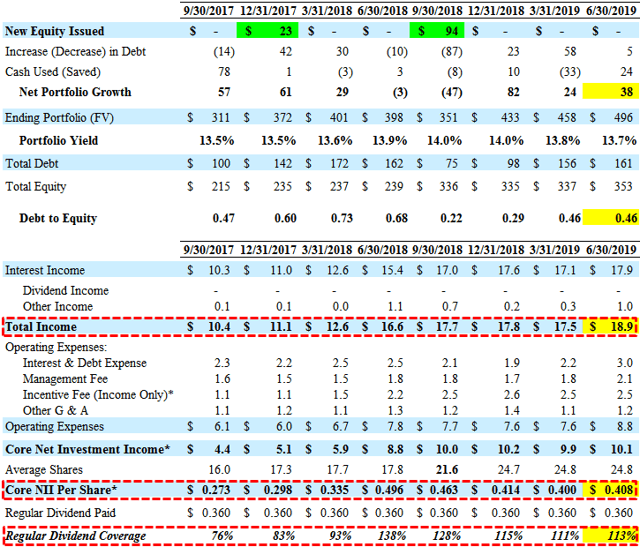

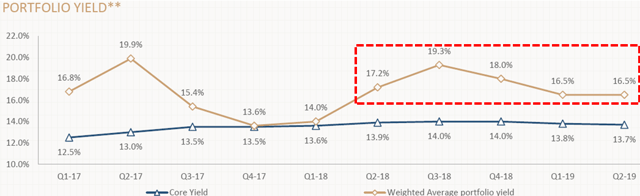

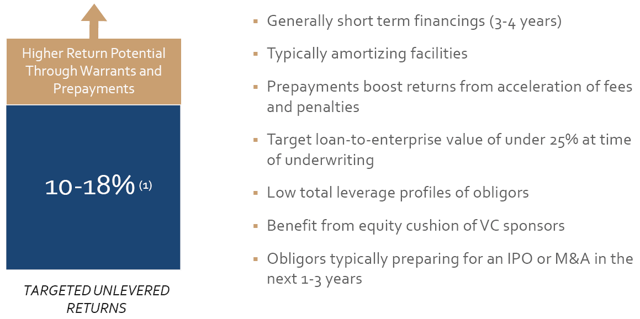

For calendar Q2 2019, TriplePoint Venture Growth (TPVG) beat its best case projections covering 113% of its dividend due to continued prepayment-related income driving an effective yield of 16.5% (same to the previous quarter) as shown in the following chart.

Jim Labe, Chairman and Chief Executive Officer: “Our results for the second quarter demonstrate the earnings power of our investment platform. We delivered substantial quarterly investment income, generated meaningful unrealized gains, and grew our investment portfolio for the third quarter in a row.”

—————–

During Q2 2019, FDUS funded 17 debt investments totaling $72.5 million to 13 companies, acquired warrant investments valued at $0.7 million in 10 companies and made equity investments of $1.7 million in 5 companies. FDUS had $43 million of early prepayments. The weighted average portfolio yield on debt investments for the second quarter was 16.5%, including the impact of prepayments and other activity, and 13.7% excluding the impact of prepayments and other activity.

“During the quarter, we had $42.5 million in portfolio company prepayments, which contributed to our 16.5% overall weighted average quarterly portfolio yield. Without prepayments, our portfolio yield was 13.7%. As a lender, we’re always happy to get our capital back. Prepayments are one way and we had a meaningful amount last quarter but we’re also pleased that our portfolio generates between $2 million and $3 million of natural principal amortization per month.”

—————–

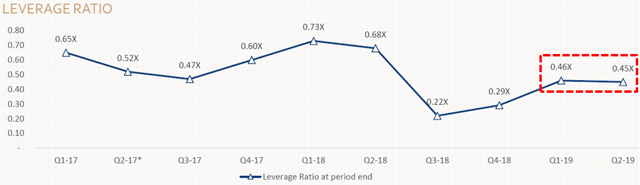

TPVG remains underleveraged but the company will likely cover its dividend. This is part of TPVG’s business model and dividend coverage will continue to be “lumpy but positive in the coming quarters”. On a previous call, management discussed “possible increases in our dividend policy on a go-forward basis” driven by higher use of leverage and/or additional prepayments:

“Looking back, we had at least one prepay every single quarter over the past two years and 10 in the past 12 quarters. In fact, we’ve already had two here in 2019. We expect to see that pattern of one on average per quarter in 2019, and along with our expected originations and increased leverage, is something our board is taking into consideration as we consider possible increases in our dividend policy on a go-forward basis.”

—————–

During July 2019, TPVG had only funded another $11 million of new investments but entered into another $130 million of additional term sheets. Management seems confident in the ability to grow the portfolio given the current pipeline and unfunded commitments:

“Alongside our record level investment portfolio, we have a strong backlog that provides great visibility into potential near-term portfolio growth over the next few quarters. At the end of Q2, our unfunded commitments totaled roughly $350 million to 25 companies of which $91 million is dependent upon the company’s reaching milestones before the capital becomes available to them. $162.7 million of our unfunded commitments will expire during 2019, $157.3 million will expire during 2020 and $30 million will expire in 2021, if not drawn prior to expiration.”

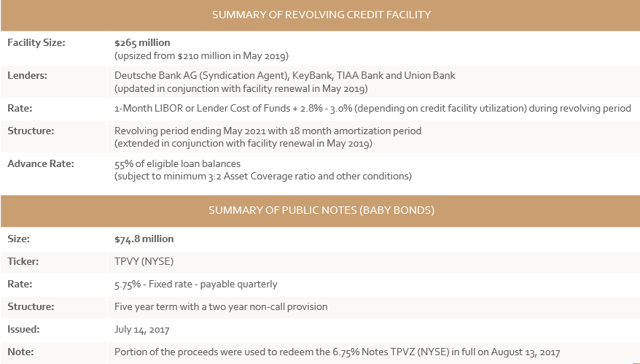

As of June 30, 2019, TPVG had $24 million of cash and $179 million of available capacity under its revolving credit facility for upcoming portfolio growth. On August 27, 2019, TPVG amended its Credit Facility increasing the capacity from $265 million to $300 million with an accordion feature which allows up to $400 million.

“We anticipate tapping into the accordion in Q3 as we look to lock-in additional variable rate funding capacity to take advantage of movements by the Fed. As we utilize our warehouse and lever up, we will look to use long-term debt as the way to free up capacity, diversify our balance sheet and approach one times leverage.”

In June 2018, TPVG obtained shareholder approval to reduce its asset coverage ratio to potentially increase its leverage (debt-to-equity) to a maximum of 2.00x. However, the company continues to experience early repayments and will likely remain under 1.00x.

“In general we expect and have always given guidance of one to two prepayments per quarter and it’s going to be part of our activity and part of our yields, but we always can get down to you know specific crystal ball vision next 30, 60 days necessarily. But I would say in general, there’d be a decrease if there’s not a lot of prepays.”

From previous call: “In the guidance that we gave when we got shareholder approval on our expectation for target leverage, right, we don’t need to lever the business out more than 1 to 1, given the return profile of our assets. But having said that, we did say that, during periods where portfolio growth in between capital raises to optimize when we raise equity, we would expect to go north of 1 to 1 to take advantage of that in building portfolio and then waiting for prepays and for the capital markets to cooperate.”

On March 28, 2018, TPVG received an exemptive order from the SEC to permit co-investment with TriplePoint Capital LLC (“TPC”) and/or investment funds, accounts and investment vehicles managed by TPC that continues to provide opportunities for portfolio growth and diversification.

“We continue to make progress in diversifying our portfolio, thanks in part to overall portfolio growth, as well as utilization of our co-investment capabilities. Since receiving our exemptive order, TPVG has made 10 co-investments with TPC’s proprietary vehicles, and this gives us meaningful financial flexibility as we scale the business”

From previous call: “Given our strong outlook for portfolio growth, we are grateful to our shareholders for approving a lower asset coverage requirement, which will enable us to take advantage of using leverage to serve as the primary source of funding portfolio growth for us here in 2019, plus, we intend to continue to take advantage of our exemptive relief order, which we received in 2018 as well to coinvest with other entities in the TriplePoint platform and further diversify as we scale.”

Previously, the company reduced its effective borrowing rates that most recently included reducing its unused facility fees from 0.75% to 0.50%. In July 2017, TPVG issued $65 million of 5.75% notes due 2022 trade on the NYSE under the symbol “TPVY” (included in the BDC Google Sheets) with the proceeds used to refinance the previous notes “TPVZ” at 6.75% resulting in lower borrowing rates. The company ultimately issued $74.8 million of notes (includes over-allotment).

—————–

Part of management’s optimism is related to the large amounts of VC equity capital that have been raised and will likely be leveraged using debt capital from companies such as TPVG:

“As we look ahead, momentum in our market remains strong and the demand for venture lending at venture growth stage companies continues to be brisk as evidenced by our large and growing pipeline. There’s no lack of deal flow. We plan to capitalize on this pipeline and build upon the achievements of these first two quarters of 2019, for the remainder of this year and the years well beyond. Our performance speaks for itself. This is about results, not words.”

—————–

TPVG Risk Profile Update:

TPVG provides financing primarily to venture capital (“VC”) backed technology companies at the venture growth stage (see the end of this report), similar to HTGC and HRZN. TPVG’s portfolio includes warrant positions in high growth sectors that continues to drive NAV per share growth and/or special dividends.

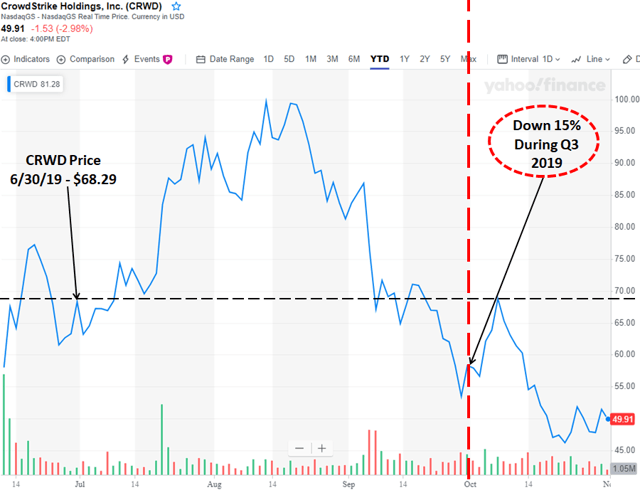

“We had a notable unrealized gain this quarter from an IPO at one of our portfolio companies and we actually had another IPO within our portfolio occur as well just after the close of last quarter. The recent IPOs at CrowdStrike and Medallia greatly contribute to our unrealized gains. As of yesterday’s close Medallia’s stock price was nearly double its IPO price. Aside from these IPOs, we continue to also have positive developments in many other portfolio companies with several raising new rounds of capital or getting acquired. During Q2, we also had six portfolio companies raised over $600 million of equity in private rounds.”

As discussed in previous reports, TPVG has historically had portfolio concentration risk and management is actively working to diversify the portfolio using the ability to co-invest across the broader platform and likely one of the reasons for the previous equity offering. The top five positions currently account for around 37% of the portfolio compared to 44% in December 2018 and 57% in early 2018.

“As of quarter-end, our top five positions represented 36.5% of the total debt investment portfolio on a fair value basis, down from 50.9% in Q2 2018. We continue to make progress in diversifying our portfolio, thanks in part to overall portfolio growth, as well as utilization of our co-investment capabilities.”

During Q2 2019, NAV per share increased by 4.4% or $0.60 per share (from $13.59 to $14.19) due to $15.1 million or $0.61 per share of unrealized gains from its equity investment in CrowdStrike, Inc. (CRWD).

“As discussed earlier on the call, the mark-to-market appreciation was primarily due to price appreciation in our publicly traded equity holdings and CrowdStrike, and was somewhat offset by fair value marks across the portfolio. During the second quarter, CrowdStrike completed its IPO on June 12. It opened trading at $63.50 after pricing its IPO at $34 this year, which was above the high-end of its expected range. The company raised more in $600 million, while we are under a six month lockup period as of the end of the quarter, the unrealized gain on our investment was $18 million.”

However, the stock has pulled back recently including a 15% decline during Q3 2019 which will have an impact of around $2.8 million of unrealized losses and a negative impact on its NAV per share by around $0.11 or 0.8%. TPVG’s shares of CRWD are currently in a six-month lockup and are not tradable until December 2019.

—————–

—————–

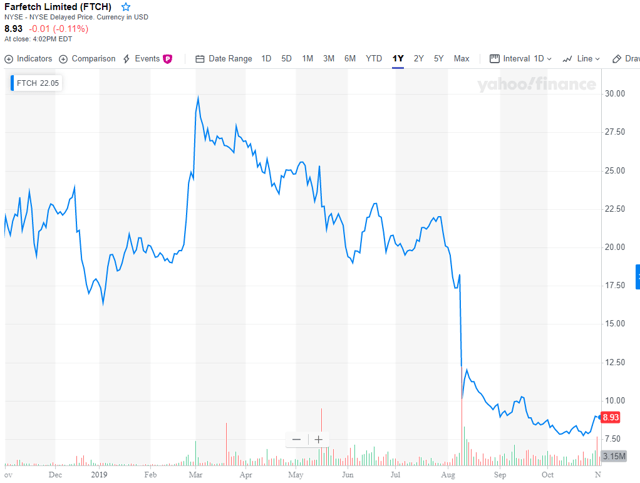

As discussed in the previous report, the unrealized gains from CRWD during Q2 2019 were partially offset by unrealized losses in Farfetch Ltd. (FTCH) that has continued to decline:

—————–

—————–

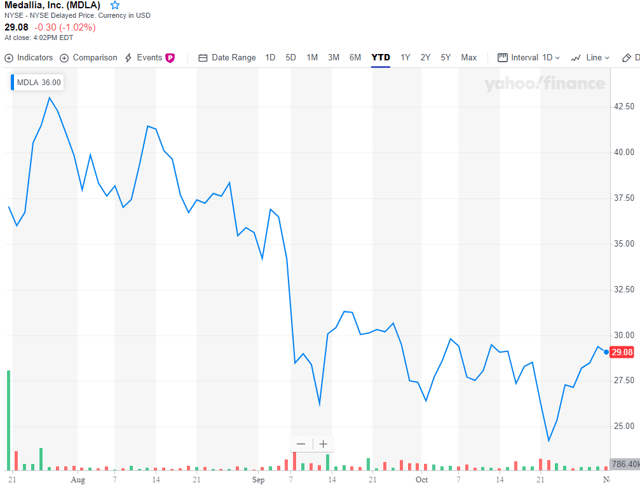

Its preferred shares in Medallia, Inc. (MDLA) were marked up by $0.5 million during Q2 2019 as the company recently completed its $326 million IPO and could drive additional gains in Q3 2019 depending on stock pricing that has also recently been pulling back as shown below.

“After the close of the quarter, as I mentioned, another portfolio company Medallia, they priced an IPO at $21 a share and raised over $325 million. As of yesterday’s close Medallia’s stock price was nearly double its IPO price. Aside from these IPOs, we continue to also have positive developments in many other portfolio companies with several raising new rounds of capital or getting acquired. Since the IPO occurred prior to the publishing of the financial statements, we were able to give some factor in a little bit, the outcome of the IPO and coming up in striking as fair value mark at quarter end.”

—————–

—————–

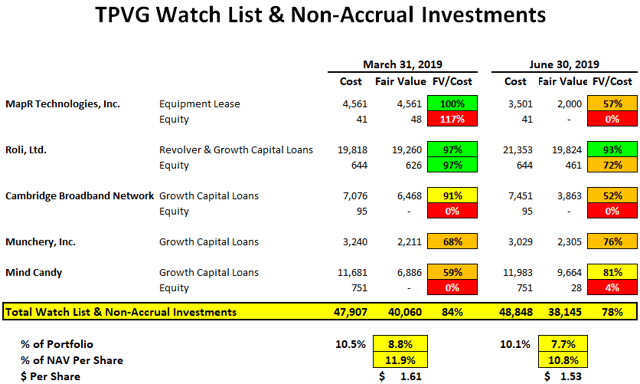

Credit quality declined slightly during Q2 2019, including Roli, Ltd’s ($21.4 million cost; $19.8 million FV) and Mind Candy Limited’s ($12.0 million cost; $9.7 million FV) obligations that became past due and TPVG is in the process of renegotiating the terms. Also, Roli, Ltd. and MapR Technologies, Inc. ($3.5 million cost; $2.0 million FV) were added to non-accrual status during Q2 2019. Management discussed Roli and Mind Candy on the recent call:

Q. “Question on a couple of the portfolio names downgraded Roli and Mind Candy. You footnote that part of those loan structures have become past due. On the ground level, what sort of game plan you’d have for a company, that still holds some value according to your mark but is obviously past due on the loan per se.”

A. “Generally, when there are delays in fundraising activity, we collaborate with the sponsors and be helpful where we can. And in certain situations that may be delaying payment or deferring payment and then our expectations are for either full catch up of the payment post – strategic event occurring or those may get added to principal balance. So generally that’s our rule of thumb is we may delay or defer payments during those extended periods for the rounds or the strategic processes to happen. And then once they do caught up and then occur.”

Q. “On MapR do you know – I understand that it’s in some sort of a sale process, but do you know what the residual value of the equipment that is under the equipment lease is compared to what the valuation is that you’re carrying it at the end of the quarter?”

A. “We’re financing mission critical equipment, servers, furniture, hardware, data center equipment. And so the fair value mark that we put for the quarter is our expected recovery factoring in, residual value, payments from potential M&A and things of that nature. But generally speaking, hardware residuals are anywhere from 10% to 30% of original costs if you look at the historic hardware lease financing data.”

As discussed in previous reports, Cambridge Broadband Network ($7.5 million cost; $3.9 million FV) was added to non-accrual status during Q4 2018 and was marked down again in Q2 2019. Also, Munchery, Inc. ($3.0 million cost; $2.3 million FV) remains on non-accrual status and previously downgraded to Category 5 indicating “serious concern/trouble due to pending or actual default”. Mind Candy is a video game developer for kids and was still on accrual status according to the 10-Q.

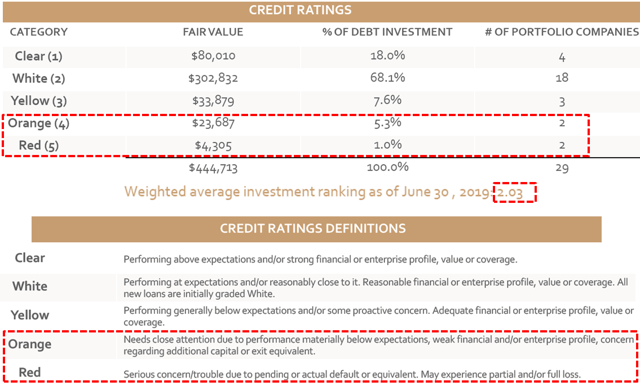

“Moving onto credit quality, the weighted average investment ranking of our debt investment portfolio was 2.03, as compared to 1.95 at the end of the prior quarter. As a reminder, under our rating system, loans are rated from one to five with one being the strongest credit rating and new loans are initially generally rated two. Mind Candy was upgraded from Orange 4 to Yellow 3 due to continued improvement in capital raising activities. Cambridge Broadband and Roli were downgraded from Yellow 3 to Orange 4 due to delays in fundraising or strategic activities as well as general performance below plan. MapR Technologies, a company where we have only equipment financing outstanding was downgraded from White 2 to Red 5 during the quarter. As reported in the press, MapR is in active M&A discussions.”

—————–

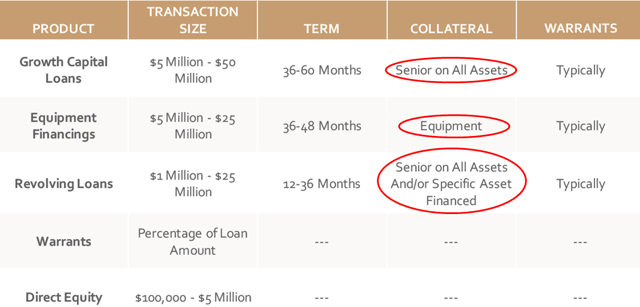

I consider TPVG to have a safer-than-average risk profile due to mostly 1st lien positions with VC equity support. Its portfolio is 90% debt investments structured as ‘growth capital loans’ or ‘equipment financing’ and mostly backed by a senior position on all assets (see below), typically with warrants that provide upside potential. Also, almost 26% of growth capital loans are with borrowers that have other facilities in a senior position to TPVG:

From 10-Q:“Growth capital loans in which the borrower held a term loan facility, with or without an accompanying revolving loan, in priority to our senior lien represent approximately 25.5% and 14.0% of the debt investments at fair value as of June 30, 2019 and December 31, 2018, respectively.”

—————–

A large part of the BDC Risk Profiles report takes into account the need to “reach for yield” as well as the need to grow the portfolio. As mentioned in previous reports, the company is frequently impacted by “higher-than-anticipated prepayments driving higher onetime prepayment-related income” but lower portfolio growth and dividend coverage from recurring interest income. One of my concerns is the accrual of the end of term (“EOT”) payment that ranges from 2% to 12% and provides higher effective yields as discussed earlier. EOT payments provide upside potential when loans are repaid earlier including the previous repayments from Simplivity, Inc., Fuze, Jet.com, Hayneedle, Inc., Thrillst Media Group and EndoChoice. However, this contractual payment is accrued and added to income but not paid in cash until the loan is repaid. It should be noted that there are non-cash expenses related to amortization of credit facility fees to ease concerns of non-cash portions of income.

This information was previously made available to subscribers of Premium BDC Reports, along with:

- TPVG target prices and buying points

- TPVG risk profile, potential credit issues, and overall rankings

- TPVG dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.