The following is from the CGBD Deep Dive that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

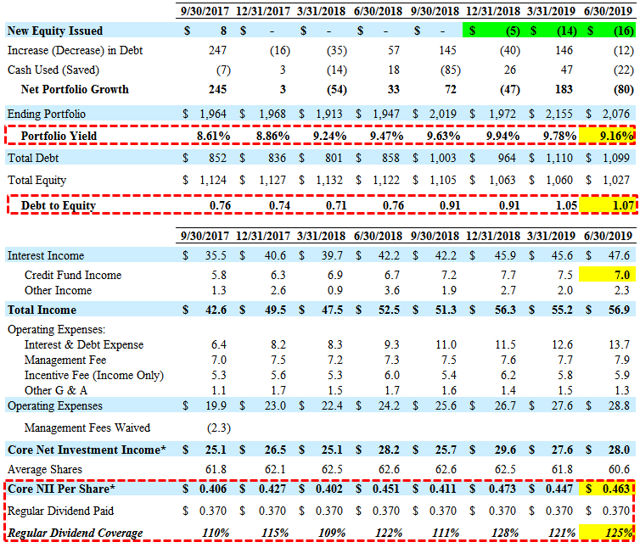

For calendar Q2 2019, TCG BDC Inc. (CGBD) covered its dividend by 125% reporting just below its best-case projections. Over the last four quarters, its average earnings have been almost $0.45 per share compared to its quarterly dividend of $0.37 per share.

“We generated net investment income of $28 million or $0.46 per share, $0.01 higher than the $0.45 we produced in the first quarter. We declared a regular $0.37 dividend and as we previewed last quarter, we also declared a $0.08 special dividend for a total of $0.45 in dividends declared in the quarter. Our Company has consistently produced net investment income in excess of our quarterly dividend and we expect to continue this trend going forward.”

The company still has $0.21 per share of undistributed income available for a special dividend that will likely be announced in Q4 2019:

“We will consider additional future special dividends with some regularity as appropriate and as our core earnings allow. At the end of the second quarter, we had approximately $0.21 per share in spillover income to fund special dividends in future periods.”

The company has covered its dividend by an average of 118% over the last 8 quarters due to continued increases in recurring sources of income implying the potential for an increase to regular quarterly dividend and was discussed on a previous call:

“Given the consistency of our NII performance, we’ll be considering an increase to our stated quarterly dividend as well.”

The company repurchased another 1,089,559 shares during Q2 2019 at $14.91 per share (14% discount to previous NAV) resulting in accretion to net assets per share of $0.04. On November 5, 2018, the Board approved a $100 million stock repurchase program at prices below reported NAV per share through November 5, 2019, and in accordance with the guidelines specified in Rule 10b-18 of the Exchange Act. The stock is still trading at 15% discount to NAV and there will likely be additional accretive repurchases including another 427,141 so far in Q3 2019.

“As of today, we have $58 million remaining on our $100 million repurchase authorization implemented during the fourth quarter of 2018. We will continue to repurchase shares at or near our current valuation as we do not believe our current share price accurately reflects the strength of our investment platform.”

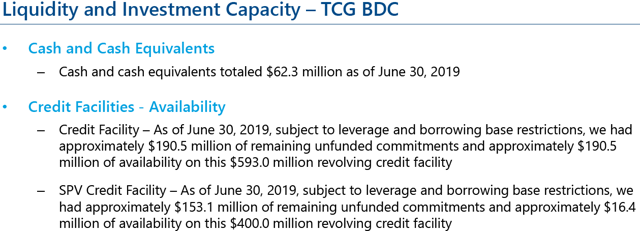

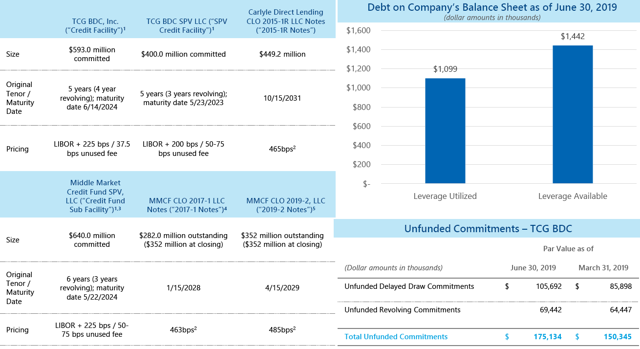

The company has been increasing its use of leverage that will likely continue. Previously, CGBD received shareholder approval to reduce its asset coverage requirement to 150% effective June 7, 2018, and the Board approved a 0.50% reduction in the 1.50% annual base management fee on assets financed using leverage in excess of 1.0x debt to equity. As of June 30, 2019, CGBD had cash and cash equivalents of $62 million and $207 million available for additional borrowings under its revolving credit facilities. Management guided for active portfolio growth in Q3 2019 due to “a steady originations pipeline combined with more modest repayments expected this quarter” and is taken into account with the updated projections:

“During the quarter, we increased commitments under our revolving credit facility by another $80 million. So we had about $340 million of total unused commitments under our credit facility. Statutory leverage was 1.07, generally in line with prior quarter giving you the growth in the portfolio. However, we do see this level increasing more meaningfully by the end of the third quarter due to a steady originations pipeline combined with more modest repayments expected this quarter. And given them more favorable rate environments for issuers, we anticipate exploring additional financing transactions in the near-term to increase our operational flexibility we’ll be looking at all areas of the market including the private and public capital markets.”

CGBD has a lower cost of borrowings including its previously reset 2015 CLO Notes and the credit facilities at around LIBOR + 200/225.

“Regarding our liabilities, we continue to benefit from the association with one of the premier CLO platforms in the world. This quarter, we priced our fourth middle market CLO further diversifying our sources of financing and reducing our overall cost of debt. We continue to be one of the few BDCs that has an investment portfolio anchored in first-lien senior secured loans with the scale and diversification necessary to support the issuance of CLOs. This not only provides our BDC and our shareholders with lower cost of debt relative to our peers but perhaps more importantly, it provides us with non mark-to-market term financing which we feel is highly valuable in markets with increased volatility.”

Middle Market Credit Fund, LLC (“Credit Fund”):

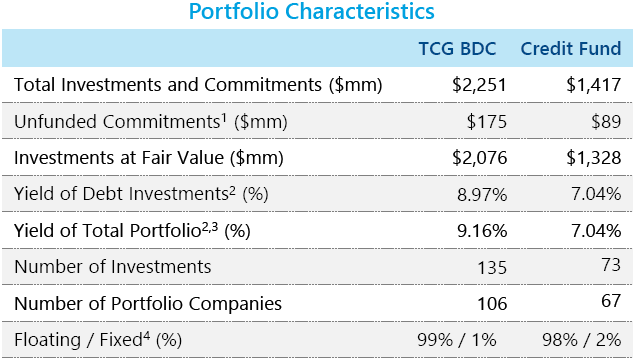

Investments in the Credit Fund increased from $1.26 billion to $1.33 billion during Q2 2019 producing a 12.7% annualized yield. The Credit Fund’s new investment fundings were $121 million for the quarter with sales and repayments of $43 million.

“Moving onto the JVs performance, the dividend yield on our equity in the JV was about 13% for the second quarter. As previewed on last quarter’s call in late May, we closed our second CLO at the JV, which resulted in an overall reduction in the JVs cost of capital by about 20 basis points.”

Similar to other BDCs, CGBD has added asset-based lending (“ABL”) to its portfolio which will likely provide higher risk-adjusted returns:

From previous call: “Our thesis was and remains that an ABL strategy is complementary to our core cash flow middle markets, sponsor finance business. Asset based loan performance and recovery rates have been strong and consistent across the market cycles. ABL’s have better structural protections in the form of borrowing bases and covenants and cash flow loans and adding an ABL underwriting capability creates more defensive and diversified company across more asset classes with potentially lower correlation. This quarter, we made two investments in the strategy at attractive yields. We expect to grow the strategy meaningfully which should drive higher ROE for the BDC.”

CGBD Risk Profile Update:

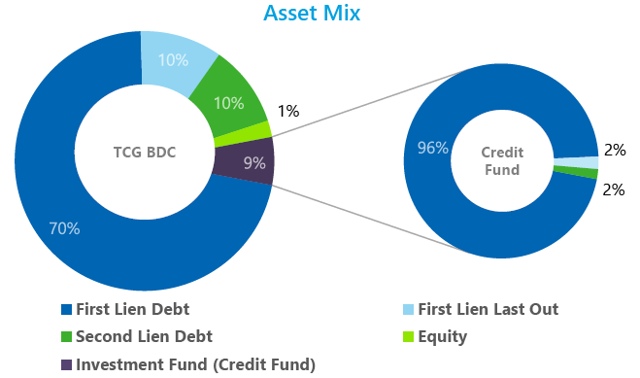

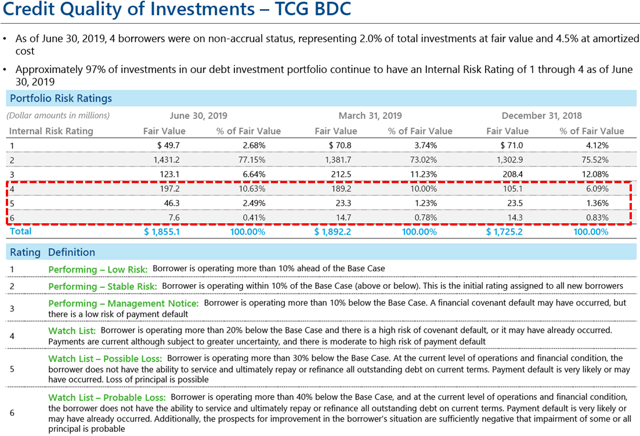

CGBD has a lower risk portfolio due to 89% of the portfolio in first-lien assets (including Credit Fund) highly diversified by borrower and sector, access to an experienced credit quality platform and historically low non-accruals.

“We consider our BDCs portfolio to be extremely well positioned fundamentally against this macroeconomic backdrop. We have 70% of our portfolio in true first lien instruments. A high degree of investment diversification and significant under weights to more cyclical industry exposures, all of which we believe will be long-term benefits to our shareholders. We’re acutely aware that we’re investing in what could be late cycle and therefore we remain ultra-selective. Carlyle’s credit investment platform has over 100 investment professionals that have the expertise to evaluate opportunities across the capital stack, company sizes, sectors and market cycles all with the lens and relative value and fundamental credit investing.”

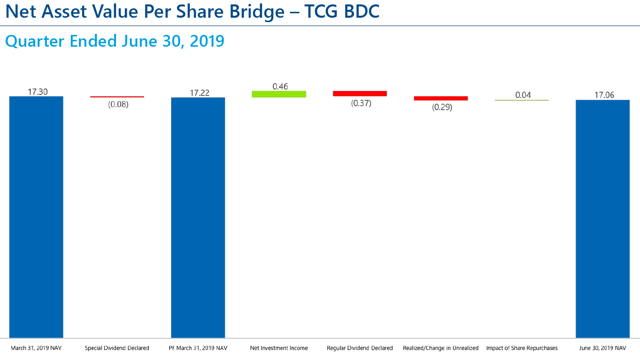

During Q2 2019, net asset value (“NAV”) per share decreased by 1.4% or $0.28 per share due to net realized/unrealized losses of $0.29 per share partially from additional non-accruals (discussed later) and paying a special dividend of $0.08 per share, partially offset by accretive share repurchases adding $0.04 per share and over-earning the dividend. Management mentioned that the recent credit issues are “idiosyncratic credit issues, not indications of either thematic risk concentrations in our portfolio or broad economic weakness”:

“The one controllable area which fell short of expectations in Q2 was the progression of our NAV, which was impacted by higher realized and unrealized losses than we would expect to see in normal course. We have dug into each situation and ascertained they represent idiosyncratic credit issues, not indications of either thematic risk concentrations in our portfolio or broad economic weakness. As you would expect, these loans are a significant focus for our team and we have committed the necessary resources to maximize shareholder value. For the most part, for the names that are on our watch list or on non-accrual, they’re idiosyncratic situations. But one thing we can point to is that within the healthcare services space, where we’re seeing companies do more aggressive types of roll-up transactions that those come with more challenges.”

As mentioned in the previous report, “my primary concern is two investments that were added to ‘Internal Risk Rating 4’. However, management discussed these investments on the recent call as “these are temporary performance issues” and “our goal remains full recovery”:

“The weighted average internal risk rating remained 2.3. However, total watch list loans again increased this quarter with a net addition of three borrowers. With the overall theme is that in most cases we believe these are temporary performance issues. Sponsors have been supportive with additional capital. We’ve closed their negotiated credit enhancing amendments and our goal remains full recovery.”

“During the quarter, we repurchased 1.1 million shares of stock for over $16 million, which was $0.04 per share accretive to NAV. Stabilizing and growing our NAV via our integrated platform approach will be the major focus area for me and the team over the next few years.”

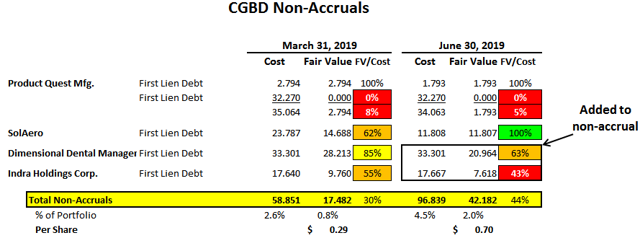

During Q2 2019, non-accruals increased due to adding Dimensional Dental Management and Indra Holdings Corp. (Totes Isotoner) during the quarter resulting in NAV decline of almost $0.16 per share. Totes hired Houlihan Lokey, which specializes in restructurings and CGBD exited this investment during Q3 2019 which will result in additional realized losses and a slight decline in NAV due to exiting at “a bit lower” value:

“The level of non-accruals increased this quarter from 0.8% to 2% based on fair value with the addition of two borrowers. We exited one of these positions [Totes] post quarter end at a level a bit lower than our 6/30 mark, driven by our developing view on the potential downside to our recovery in that investment. For the other non-accrual transactions these continue to be fluid and developing situations. Given the status of ongoing negotiations between the various parties we’re limited in providing additional color, but we hope to have updates over the next couple of quarters.”

SolAero Technologies Corp. has been discussed in previous reports and was restructured during Q2 2019 driving most of the realized losses of almost $9.1 million or $0.15 per share:

“The roughly $8 million realized loss this quarter has two primary components. First, a $9 million realized loss for our recapitalization of SolAero and that was primarily reversal of prior period unrealized losses. And second, a $2 million gain on an equity co-investment in imperial date.”

Product Quest Manufacturing, LLC remains on non-accrual and was written down due to “operational and liquidity challenges” and its smaller first-lien loan was added to non-accrual in Q1 2019. On a previous call, management mentioned that all lenders (including CGBD) have provided an additional credit facility to support the working capital needs and will provide updates on future calls. I am expecting Product Quest to be completely written off resulting in realized losses of $34 million or $0.57 per share but has already been mostly written off and will not materially impact NAV per share. Non-accruals accounted for around 2.0% of the portfolio fair value and $0.70 of NAV per share:

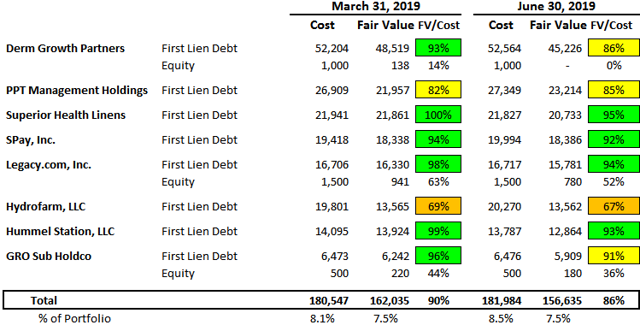

Some of the other investments that have been discussed in previous reports and/or that I am watching closely include Derm Growth Partners, PPT Management Holdings, Superior Health Linens, SPay, Inc., Legacy.com, Hydrofarm, Hummel Station, and GRO Sub Holdco. Most of these investments were marked down during Q2 2019 with the exception PPT:

It is important to note that CGBD has higher quality management that conservatively values its portfolio each quarter:

“When we held our initial earnings call as a public company back in August of 2017, I highlighted that based on our robust valuation policy, each quarter you may see changes in our valuations based on both underlying borrower performance as well as changes in market yields and that movement evaluations may not necessarily indicate any level of credit quality deterioration.”

Indra Holdings Corp. (Totes Isotoner) was its only investment with an ‘Internal Risk Rating 6’ and has been exited as discussed earlier.

This information was previously made available to subscribers of Premium BDC Reports, along with:

- CGBD target prices and buying points

- CGBD risk profile, potential credit issues, and overall rankings

- CGBD dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.