The following is from the TCPC Deep Dive that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

- Each quarter, I go through the results for each BDC assessing ongoing/upcoming credit issues for risk rankings and target prices as I recently did for TCPC discussed in this update.

- TCPC’s largest new investment during Q3 2019 was Juul Labs which produces electronic cigarettes/vaping products that have been under recent pressure from the Food and Drug Administration (“FDA”).

- The FDA has issued a ban on most flavored vaping products, with the exception of tobacco and menthol.

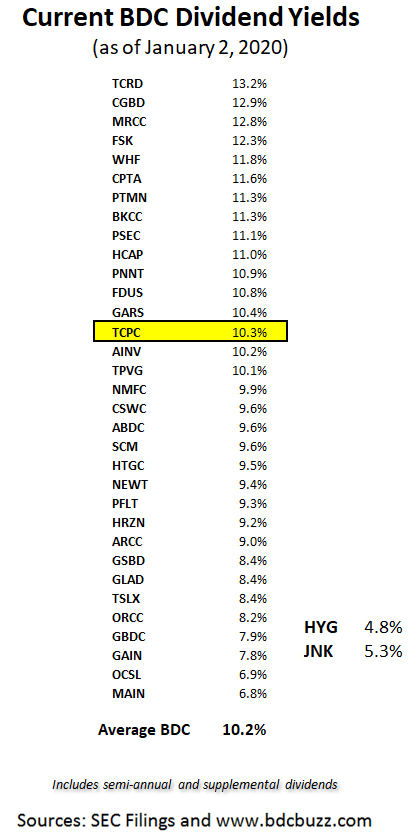

This update discusses BlackRock TCP Capital (TCPC) currently yielding over 10% annually. As mentioned below, each quarter I go through the results for each BDC assessing ongoing or upcoming credit issues to asses risk rankings and target prices as I recently did for TCPC some of which are presented in this update.

TCPC Risk Profile “Quick Update”

During Q3 2019, TCPC’s net asset value (“NAV”) per share declined by $0.05 or 0.4% (from $13.64 to $13.59) due to unrealized losses from previously discussed ‘watch list’ investments mostly offset by overearning the dividend and markups of Edmentum and Snaplogic, Inc.:

Leading portfolio gains was a $5.2 million increase in the value of our investment in Edmentum. As we have previously discussed, we have been working alongside the Edmentum management team to improve operations and we are pleased to see meaningful ongoing improvements to the Company in our holdings as a result of those efforts. We also recognized $4 million in gains and prepayment income on the payoff of our loan to SnapLogic during the third quarter.”

Source: TCPC Q3 2019 Results – Earnings Call Transcript

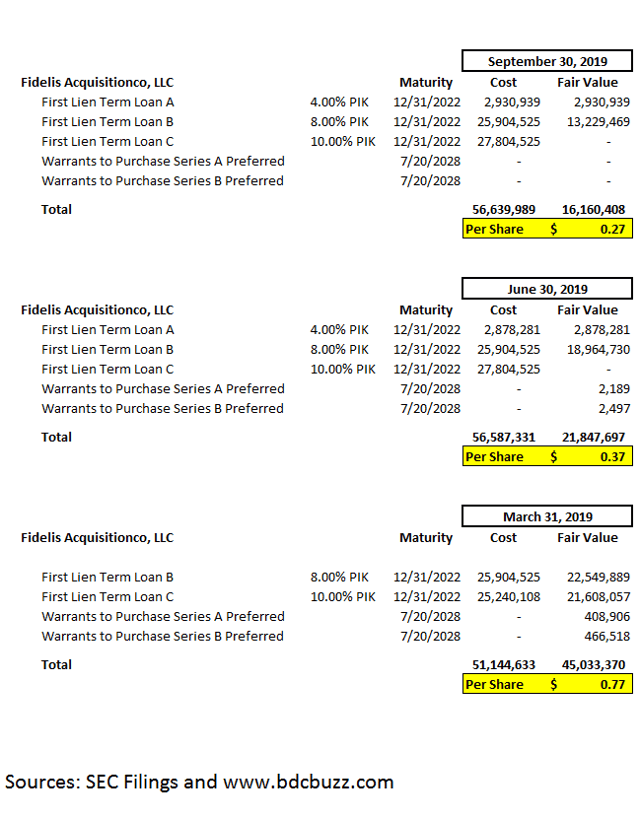

Similar to the previous quarter, the largest markdown was its investment in Fidelis Acquisitions, LLC (“Fidelis”) that was added to non-accrual in Q2 2019 and marked down another $5.7 million during Q3 2019. Fidelis still accounts for around 1.0% of the portfolio and $0.27 per share of NAV and has been discussed in previous reports.

The largest markdown in the quarter was a $5 million markdown of our investment in Fidelis, driven in large part by an ongoing liquidity shortfall at the company. We are actively engaged with management and potential co-investors to both address the shortfall and to proactively deal with the issues that drove the under-performance in the past. As discussed on last quarter’s call, we expect the value of this investment to be volatile, as we work toward a solution to strengthen the balance sheet and we plan to provide updates as appropriate.”

Source: TCPC Q3 2019 Results – Earnings Call Transcript

Management discussed Fidelis on the recent call including bringing on additional financing that would likely result in a restructuring driving realized losses in the coming quarters but also put back on accrual status:

Q. Can you guys provide any update on Fidelis?”

A. This is obviously a very important, but I would say isolated position and that we’re dealing with the company. We continue to see some benefit both topline and as well as the outlook for the business based on the work we’ve done over – going back over a year-ago in terms of switching out management and making some changes. But there is an ongoing liquidity need and we are actively working to address that and hopefully resolve it and that may ultimately include us with the financing partner taking over the business or it might be an alternative. Where I parsed the business outlook from the liquidity outlook and it’s an ongoing activity that we will just continue to try to update you all on.”

Source: TCPC Q3 2019 Results – Earnings Call Transcript

Most of the previous NAV declines were due to 5 investments discussed in previous reports including Real Mex, Kawa Solar, AGY Holding, Green Biologics and most recently Fidelis.

- Its loan to Real Mex was part of the legacy pre-IPO strategy and had generated significant income. During Q4 2018, TCPC exited this investment resulting in $25.8 million of losses with no further impact to NAV.

- Kawa Solar Holdings was previously on non-accrual but restructured in Q3 2018 and is now in the process of “winding down”.

- Its debt investments in Green Biologicswere restructured into common equity and mostly written off with no further impact to NAV.

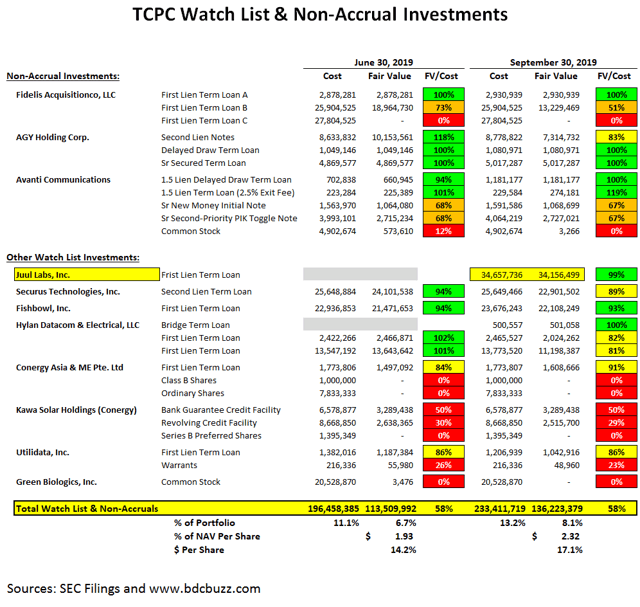

Along with Fidelis, TCPC has loans to AGY Holding (“AGY”) and Avanti Communications on non-accrual status account for around 1.4% of the portfolio fair value.

We had loans to three portfolio companies on non-accrual status, Fidelis, AGY and Avanti, representing 1.4% of the portfolio at market value and 3.8% at cost. We placed Fidelis on non-accrual last quarter and Avanti has been challenged for some time. AGY is a fundamentally good company, whose valuation is currently less than its debt.

Source: TCPC Q3 2019 Results – Earnings Call Transcript

Its equity investments in AGY were previously written off with no further impact to NAV but the second-lien notes were marked down by $3 million. Management discussed AGY including “weakness on the international front” due to “record high commodity prices for certain raw materials” and “some customers slowdowns due to international trade uncertainty”:

Additionally, we took mark downs of $3 million on each of our investments in Hylan and AGY, both for company-specific reasons. AGY continues to be a fundamentally good company that has faced a series of external challenges, including record high commodity prices for certain raw materials, particularly rhodium, as well as some customers slowdowns due to international trade uncertainty. AGY is a fundamentally good business. We’ve had a couple of markdowns in that, we’ve been disappointed. It’s a maker of high-end resins that go into a series of sophisticated end-use products. The markets for most of these have been strong. This quarter we saw some weakness on the international front, due to what we think is trade uncertainty and the Company was significantly impacted as some of its raw materials, particularly rhodium has soared and is at record price levels. As a result this, our valuation providers decreased the value of the Company to a level lower than where the instrument was valued and we thought that it called into question the collectability of the PIK to a sufficient point that it belonged on non-accrual.”

Source: TCPC Q3 2019 Results – Earnings Call Transcript

The other large markdown during the quarter was its watch list investment Hylan Datacom & Electrical that contributed around $2.7 million of unrealized losses during the quarter:

Hylan is a leading telecom and wireless engineering and construction company whose customers are experiencing project delays in certain end markets, including from delayed 5G projects.”

Source: TCPC Q3 2019 Results – Earnings Call Transcript

The following table shows the ‘watch list’ investments that account for around 8.1% of the total portfolio fair value. The updated watch list includes its new investments in Juul Labs, Inc. as discussed next.

The largest new investment during Q3 2019 was Juul Labs, Inc. (JUUL) which produces electronic cigarettes/vaping products that have been under recent pressure from the Food and Drug Administration (“FDA”).

On January 2, 2020, the FDA issued a ban on most flavored vaping products, with the exception of tobacco and menthol. Under the new rule, companies that do not stop the distribution of fruit and mint flavors within 30 days are at risk of regulatory action by the FDA. However, Juul stopped selling its mint and fruit-based flavors in Q4 2019 and continues to sell flavors based on tobacco and menthol. Also, there are other issues including various lawsuits but TCPC management mentioned “we believe this is a well-structured and well-covered loan” with “multiple sources of repayment, including a very low loan-to-value, cash well in excess of our debt and successful business operations in multiple locations”:

They include a $35 million senior secured loan to Juul Labs and investment generated from a relationship we had through our private funds. We made this investment in early August, and while we are aware of the recent headlines about Juul, we believe this is a well-structured and well-covered loan.”

Q. Can you maybe talk a little bit about how your investment in Juul Labs? That deal was source to you and then maybe specifically with Juul, but also just broader, that obviously company has some controversy to it. So how do you guys get comfortable making investment, would you guys obviously view as an attractive risk-adjusted return, but potentially could have some reputation risk there?”

A. As we mentioned about half our investments come from existing sources, and this is one of those. It wasn’t an investment in the BDC that was a company that we had been involved with in one of our private funds, no longer involved within that capacity. And so, we had a pre-existing relationship. I think it’s always difficult to answer a hypotheticals. But we invested in Juul in early August. On the premise that the company has developed an alternative to combustible cigarettes, that could dramatically reduce cigarette consumption. And our investment was based on fundamentally sound underwriting, which includes multiple sources of repayment, including a very low loan-to-value, cash well in excess of our debt and successful business operations in multiple locations. Having said that, we’re very conscious of the headlines and the circumstances surrounding the company and we continue to monitor.”

Source: TCPC Q3 2019 Results – Earnings Call Transcript

As mentioned in previous articles, its debt investments in Green Biologics were restructured into common equity and discussed on a previous call: “Green Bio missed projections, but received an equity infusion from its strategic owner during the quarter.” Kawa Solar Holdings was previously on non-accrual but restructured in Q3 2018 and is now in the process of “winding down”. Other investments that need to be watched include Securus Technologies, Inc., Conergy, Fishbowl, Inc., Utilidata, Inc. and Avanti Communications Group. TCPC has investments in 105 portfolio companies and a certain amount of credit issues are expected.

It’s important to note that on a combined basis, these investments account for a very small percentage of our portfolio. We are focused on maximizing their value along with the rest of the portfolio and our team has a strong long-term track record and experience working through challenging situations, as demonstrated by the increase in value of our investment in Edmentum and the gains we realized on SnapLogic.”

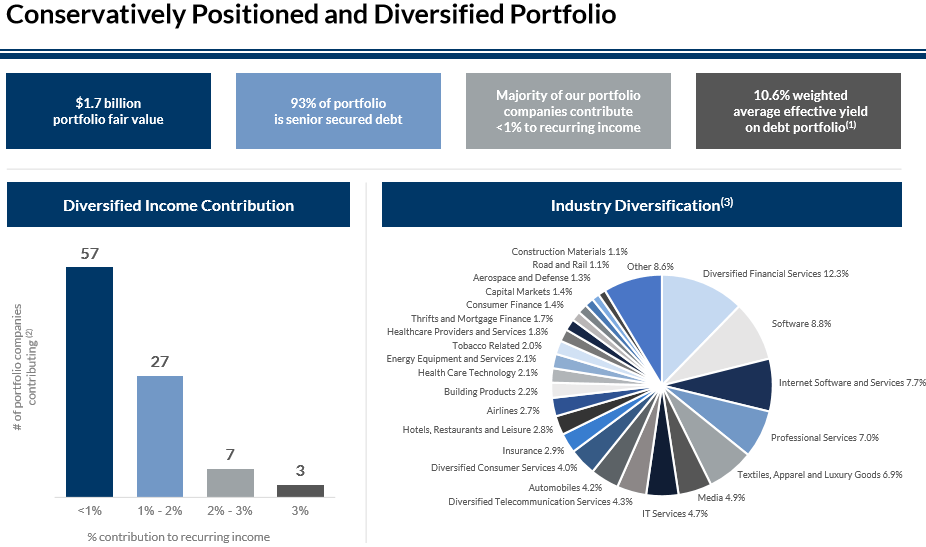

As of September 30, we held investments in a record 105 companies across a wide variety of industries. Our largest position represented only 3.8% of the portfolio and taken together, our five largest positions represented only 15.8% of the portfolio.”

Source: TCPC Q3 2019 Results – Earnings Call Transcript

Source: BlackRock TCP Capital Corp 2019 Q3 – Results – Earnings Call Presentation

The overall credit quality of the portfolio remains strong, with 93% of the portfolio in senior secured debt (mostly first-lien positions) and low non-accruals and low concentration risk:

At quarter-end, our portfolio had a fair market value of $1.7 billion, 93% of which was in senior secured debt. In constructing our portfolio, we have consistently focused on seniority as well as diversification. As of September 30, we held investments in a record 105 companies across a wide variety of industries. Our largest position represented only 3.8% of the portfolio and taken together, our five largest positions represented only 15.8% of the portfolio. Our recurring income is distributed across a diverse set of portfolio companies. We are not reliant on income from any one portfolio company. In fact, on an individual company basis, well over half of our portfolio companies each contribute less than 1% to our recurring income. ”

This information was previously made available to subscribers of Premium BDC Reports, along with:

- TCPC target prices and buying points

- TCPC risk profile, potential credit issues, and overall rankings

- TCPC dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.