The following is from the MRCC Deep Dive that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

The following are excerpts from an article that will come out on Sunday, January 26, 2020.

Why Investors Are Selling 12% Yielding Monroe Capital

- I have recently suggested to my subscribers to sell or at least trim current positions of MRCC and wait for the company to report Q4 results.

- On January 7, the WSJ reported “Creditors are seeking to force ECA into chapter 11…filed papers claiming the company isn’t paying debts. ECA/NECB account for 3.1% of MRCC’s NAV.

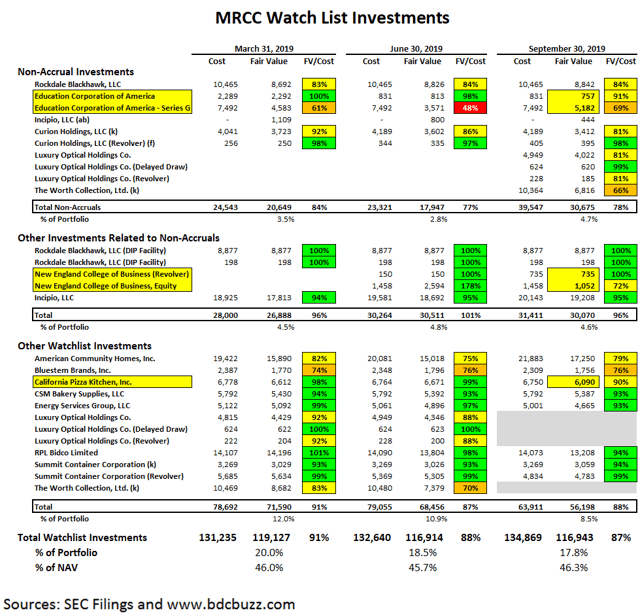

- Also, I’m expecting California Pizza Kitchen ($6.1 million or $0.30/share and 2.4% of NAV) to be placed on non-accrual status in Q4 2019 for the reasons discussed in this report.

- My primary concerns are additional markdowns and non-accruals related to its ‘watch list’ that currently account for almost 18% of the portfolio and 46% of NAV.

- On the last call, management was asked about “sustaining the current dividend” and mentioned “we’ll be in a much better position to respond to that question at the following quarter”.

The information used in this article was as of January 23, 2020, and pricing has changed as I suggested that subscribers of Premium BDC Reports to sell or at least trim current positions of MRCC and wait for the company to report Q4 results (see dates below). The stock was headed down on the morning of January 24, 2020:

MRCC Risk Profile Update

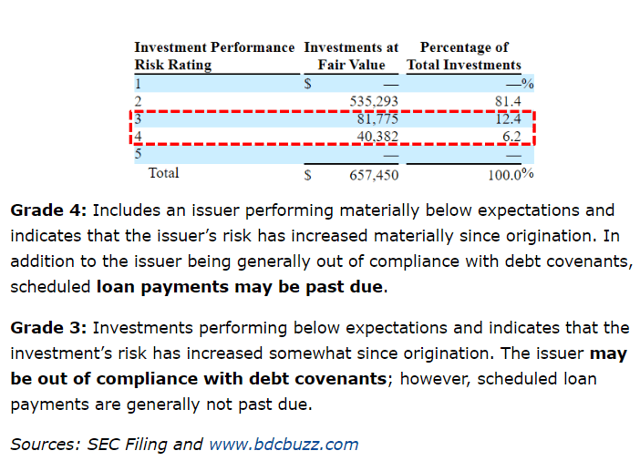

MRCC was previously downgraded in my Risk Rankings due to continued credit issues including adding Education Corporation of America (“ECA”) to non-accrual status, previous markdowns of Rockdale Blackhawk and realized losses from TPP Operating, Inc. During Q3 2019, MRCC’s net asset value (“NAV”) decreased by $0.18 or 1.4% (from $12.52 to $12.34) mostly due to additional markdowns in previously discussed ‘watch list’ investments including Luxury Optical Holdings Co. and The Worth Collection that were added to non-accrual status during Q3 2019. Also added to non-accrual were its loans to Curion Holdings as its promissory notes were already on non-accrual. The total fair value of investments on non-accrual increased to $30.7 million and account for around 4.7% of the portfolio fair value and $1.50 per share or around 12.2% of NAV.

While we are pleased with the growth in our portfolio, an increase of $26.6 million during the quarter, and the continued coverage of our dividend by net investment income, we are not happy with the slight decline of 1.4% in our per share NAV. Over the past several quarters, we have seen some idiosyncratic credit issues with a few borrowers. We do not believe these isolated issues are representative of our portfolio as a whole. We feel we are on the right track in resolving some of these credit issues and we hope to be able to see the results of our efforts in the coming quarters.

Source: MRCC Q3 2019 Results – Earnings Call Transcript

Other non-accruals include Incipio, LLC third lien tranches, and Rockdale Blackhawk, LLC (“Rockdale”). However, the Curion promissory notes and the Incipio third lien tranches were obtained in restructurings during 2018 for no cost. The company has identified around $122 million or 18.6% of the portfolio as 4 and 3 ratings: “loan payments may be past due” or “may be out of compliance with debt covenants”. It should be noted that The Worth Collection was and still has an investment risk rating of 3 as discussed on the recent call:

Q. “What were the ratings on Worth and Luxury at the end of last quarter?”

A. “Worth was a 3-rated credit, which has not changed and Curion is a 4-rated credit, and Luxury Optical’s also a 4-rated credit, which has not changed.”

Source: MRCC Q3 2019 Results – Earnings Call Transcript

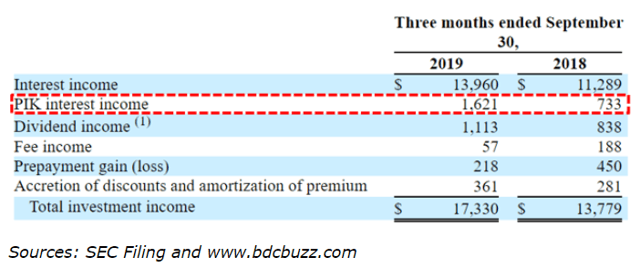

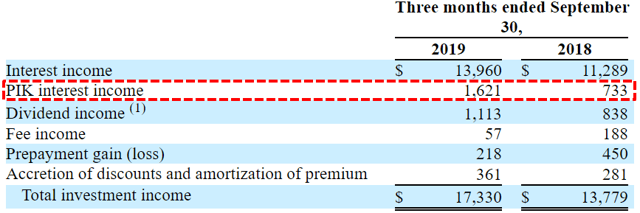

Another issue that needs to be watched is the amount of payment-in-kind (“PIK”) that continues to increase from 5.3% of total income in Q3 2018 to 9.4% during Q3 2019:

My primary concern is the potential for additional non-accruals and markdowns of the investments listed in the previous table that currently account for almost 18% of the portfolio and 46% of NAV per share. The worst-case projections take into account additional credit issues that could result in a dividend reduction of around 25% as discussed at the end.

We’re in an uncertain market and things are happening very often beyond our control as investors. And some of the things that happen from time to time that are beyond our control very really affect industries, in particular, companies in those industries, and it’s very hard to predict. So, we’re going to continue to do that, and we’ll be back to you next quarter with a report. Hopefully, we’ll see more stability in world affairs and other things that are happening that are the more uncontrollable factors.

Source: Previous MRCC Earnings Call

Education Corporation of America (“ECA”) was added to non-accrual status during Q4 2018 and MRCC’s series G equity portion was marked up by $1.6 million in Q3 2019 as shown in the previous table. However, this was partially offset by marking down its equity portion of New England College of Business (“NECB”). During Q2 2019, MRCC participated in a credit bid to acquire the assets of NECB, which was a subsidiary of ECA resulting in a 20.8% equity stake in NECB in exchange for a $1.5 million reduction of secured loan position in ECA as well as a follow-on revolver commitment to NECB. MRCC’s investments in ECA/NECB were valued at $7.7 million or $0.38 per share and 3.1% of NAV. Management discussed on the recent call:

on a net basis, it ended up around flat, when you think about the two pieces. And it really had to do with some — in the case of NECB, there was some buying interest in the company, which faded a little bit, which impacted the value negatively. And as applies to the ECA, it gets into a little bit of specifics, but there was a change in, sort of, how we calculated the recovery based on some negotiations with the trustee in that case, which impacted the value a little bit. But I think what we said in the past, which we continue to believe, is we don’t expect there to be much resolution on this case for some period of time because a lot of the recovery, particularly applied to ECA is related to some longer-term legal settlements that could be occurring.”

Source: MRCC Q3 2019 Results – Earnings Call Transcript

However, on January 7, 2020, the Wall Street Journal reported:

“Creditors are seeking to force defunct Education Corp. of America into chapter 11 more than a year after the for-profit college chain shut down, leaving roughly 20,000 students in the lurch. A lender, a landlord and a crisis communications firm filed papers in the U.S. Bankruptcy Court in Wilmington, Del., claiming the company isn’t paying its debts as they come due. Monroe Capital LLC, BSF Richmond LP and Reputation Partners LLC said in the filing they are owed a total of $3.0 million.”

Another investment that is included in MRCC’s watch list is California Pizza Kitchen, Inc. which was marked down in Q3 2019 but still valued at $6.1 million or $0.30 per share and 2.4% of NAV. Many of these locations have recently been closed often due to higher rents.

January 14, 2020 – Chicago’s Only California Pizza Kitchen Closes in River North: “International chain California Pizza Kitchen has closed its only city of Chicago restaurant inside the Shops at North Bridge, according to a recorded phone message, and wiped any mention of the 52 E. Ohio Street location from its website.”

October 20, 2019 – California Pizza Kitchen closes in Westbury, NY: “The Oct. 20 closure of the restaurant after 25 years of serving a variety of pizzas, soups, salads, pastas and more was confirmed by a restaurant representative, who said its “lease term has concluded.” No other details were provided.”

August 6, 2019 – California Pizza Kitchen Will Close Its Last Two Washington Locations on Thursday: “the 34-year-old franchise famous for its chicken barbecue pies — will close its locations in the Northgate Mall and Bellevue on Thursday, currently the only two CPK restaurants left in the entire state (there was another location in Tukwila that closed last year). A rep for the chain confirmed the news to Eater Seattle but did not reveal a reason for the closures. Those two particular branches ran into difficult circumstances: Northgate Mall is turning into a ghost town, and Bellevue’s rents continue to skyrocket.”

July 2019 – California Pizza Kitchen – Cherry Hill, NJ: “Pizza franchise California Pizza Kitchen closed its Cherry Hill Mall restaurant in July. A sign on the door said its “lease term has concluded. Now, the closest franchise of the nationwide chain is located on the outskirts of Philadelphia on City Avenue. The closest location in New Jersey is 48 miles away in Bridgewater.”

May 21, 2019 – California Pizza Kitchen’s Only Manhattan Location Will Close on Friday: “California Pizza Kitchen will stop serving its famed Barbecue Chicken pie in Midtown later this week. The 12-year-old branch will shut its doors on Friday, leaving zero outposts of the American pizza chain in Manhattan. The lease is up for the big, highly visible corner space at 440 Park Avenue South, on East 30th Street, and the rising costs are forcing it to close, a spokesperson says. “Despite our strong performance here, rising rent costs have simply become too high to continue in this specific location,” he says.

American Community Homes, Inc. was marked up slightly but remains discounted at 79% of cost and discussed on the recent call including the potential for improvement due to lower interest rates. Hopefully, this investment will be marked up in Q4 2019 offsetting likely markdowns including ECA, NECB, and California Pizza Kitchen.

“with our independent third-party value of the company this quarter, there was a belief that we shared that the company is improving and the valuation, therefore, on a fair value basis increased. The company has got a new management team in place. They are — they’re in the mortgage origination and mortgage servicing business for residential mortgages. So they’re impacted clearly in a negative way by the decline in rates as it applies to their MSR book, which is effectively an interest rate IO. But they benefit from an increase in refi volume on the origination side. So this company has a bit of a natural hedge. And they’ve taken advantage of the market and their turnaround strategy by bringing over additional teams, in most cases, at no cost into their origination engine, which drives both origination volume, therefore, fee income, as well as additional mortgage servicing rights, which have value that are valuable and can trade. So we’re just seeing some benefits, some trends that are positive. And that’s why this company’s mark went up, and that’s why this company is still on accrual status. And that’s why this company we think should continue to generate a positive recovery for us.”

Source: MRCC Q3 2019 Results – Earnings Call Transcript

MRCC Dividend Coverage Update

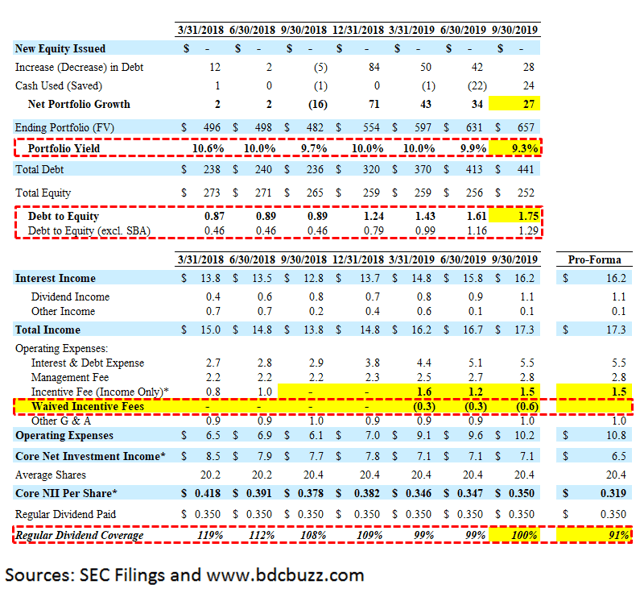

MRCC was previously downgraded due to continued credit issues driving increased reliance on fee waivers to cover its dividend. Over the last four quarters, the company has covered its dividend only due to the ability to use higher leverage through its SBIC license and management willing to waive incentive fees to ensure dividend coverage. Previously, MRCC had higher dividend coverage only due to the ‘total return requirement’ driving no incentive fees paid.

On November 4, 2019, the Board approved a change to the Investment Advisory Agreement to amend the base management fee structure:

Effective July 1, 2019, the base management fee is calculated initially at an annual rate equal to 1.75% of average invested assets (calculated as total assets excluding cash, which includes assets financed using leverage); provided, however, the base management fee is calculated at an annual rate equal to 1.00% of the Company’s average invested assets (calculated as total assets excluding cash, which includes assets financed using leverage) that exceeds the product of 200% and the Company’s average net assets. For the avoidance of doubt, the 200% is calculated in accordance with the asset coverage limitation as defined in the 1940 Act to give effect to the Company’s exemptive relief with respect to MRCC SBIC’s SBA debentures. This change has the effect of reducing the Company’s base management fee rate on assets in excess of regulatory leverage of 1:1 debt to equity to 1.00% per annum.

Source: SEC Filing

The reduced rate will not have a meaningful impact to dividend coverage as it only applies to regulatory leverage (debt-to-equity) over 1.00 which excludes SBA debentures. The new rate became effective in Q3 2019 and the management fee increased from $2.7 million to $2.8 million with a blended rate of around 1.67% compared to 1.75%. If management would have been paid the full fee of 1.75%, it would have been less than $0.1 million higher for the quarter implying that this is not a long-term solution for dividend coverage. As of September 30, 2019, MRCC had regulatory leverage of 1.29 which is near the high end of its targeted debt-to-equity ratio to 1.25 to 1.30:

We intended to go above 1:1 and continue to expect to grow our regulatory leverage over the next couple of quarters, I’d say. I don’t know where we’ll wind up. It really depends on how the portfolio shakes out in the new origination shakeout, but I’d say think of it as maybe up to 1.25 to 1.3 times kind of regulatory leverage as a next target.”

Source: MRCC Q3 2019 Results – Earnings Call Transcript

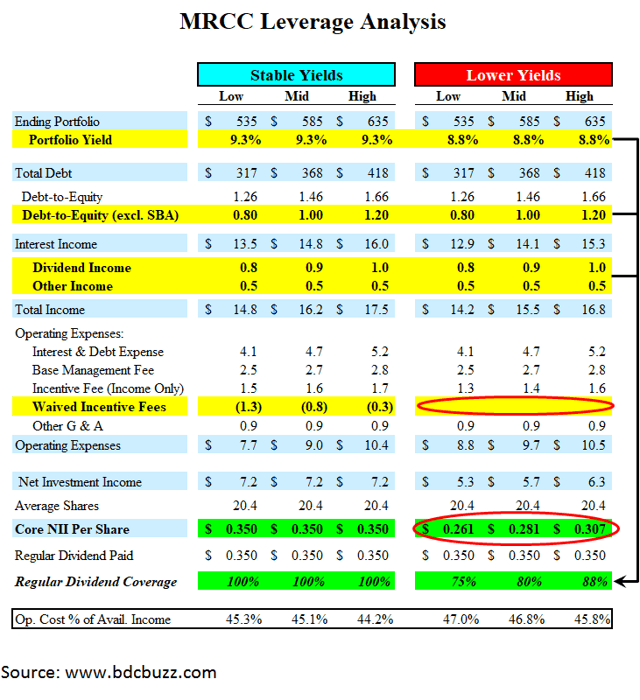

For Q3 2019, MRCC hit its base-case projections due to continued fee waivers to cover the current dividend. As shown below, dividend coverage would have been around 91% without fee waivers even after taking into account in the reduced base management fee.

The last four quarters of higher-than-expected portfolio growth have driven its debt-to-equity ratio from 0.89 to 1.75 and its regulatory debt-to-equity ratio (excluding SBA debentures) has increased from 0.46 to 1.29. MRCC’s leverage is now approaching the highest in the sector and is partly due to continued declines in NAV including another 1.4% in Q3 2019. However, dividend coverage has not improved due to additional non-accruals.

At the end of the quarter, our regulatory leverage was approximately 1.29 debt to equity. This is nearing the top end of the targeted leverage range we have guided you to on prior quarters. This higher level of leverage was temporary as we were aware of a couple of portfolio paydowns that were expected to close shortly after quarter end, which have since occurred. Since quarter end, both total assets, as well as our total leverage, have decreased with total repayments of $38.6 million received since September 30. We would expect to reinvest a portion of these prepayments in the fourth quarter of 2019.”

Source: MRCC Q3 2019 Results – Earnings Call Transcript

As mentioned earlier, my primary concern is the potential for additional non-accruals and markdowns of certain investments (including ECA, NECB, and California Pizza Kitchen) that currently account for almost 18% of the portfolio and 46% of NAV per share.

We continue to believe that our adjusted NII can cover our dividend assuming no other material changes in our portfolio.

Source: Previous MRCC Earnings Call

The worst-case projections take into account additional credit issues and could result in a dividend reduction of around 25%. On the last call, management was asked about “sustaining the current dividend” and mentioned “we’ll be in a much better position to respond to that question at the following quarter”:

Q. “Given all the headwinds, particularly the interest rate headwinds, do you think that the business model can sustain the current dividend? And management is willing to do whatever it takes to support the dividend through waivers and all that other stuff?”

A. “We’re going to look at everything here. But at the end of the day, we’re going to try and do what we can to generate the best overall returns for our shareholders, both in terms of dividends, NAV, value accretion. And we’ve got a couple of things that we’re going to work on in the next quarter. And I think we’ll be in a much better position to respond to that question at the following quarter. So I guess, just hold on to that.”

Source: MRCC Q3 2019 Results – Earnings Call Transcript

Also mentioned earlier, there has been a meaningful increase in the amount of non-cash payment-in-kind (“PIK”) interest income from around 5.3% to 9.4% and included many of the “watch list” investments discussed earlier

Source: SEC Filings

Summary & Recommendations

As shown in the Leverage Analysis below, the dividend is stable mostly only due to management waiving incentive fees to ensure dividend coverage.

However, if there are continued credit issues and management decides to reset the dividend as discussed later in this report without fee waivers and/or change in the management fee, the quarterly dividend will likely be reduced to between $0.25 and $0.30. This is also shown in the worst-case projections that take into account continued credit issues likely from the investments discussed later in this report.

BDCs are not CEFs

Many investors do not understand business development companies (“BDCs”) and use price-to-NAV as a measure of valuation. I find this to be simplistic at best and maybe it is okay for closed-end fund (“CEF”) but not for BDCs as it does not take into account operating cost structures, quality of management, borrowing rates, portfolio credit quality, potential declines in book value, expected returns, etc.

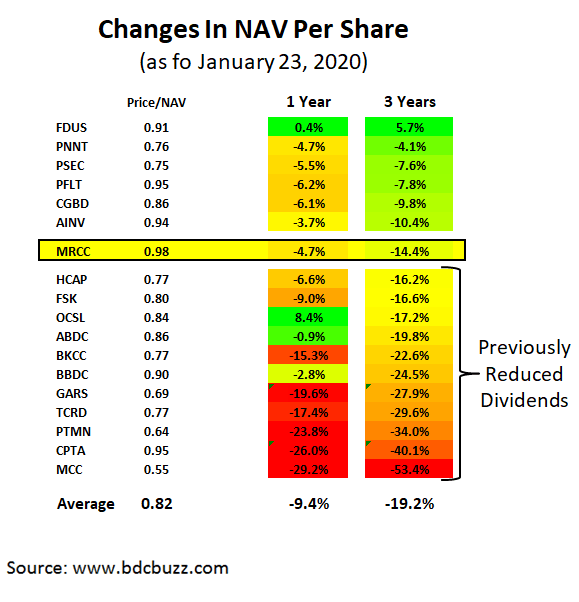

That said……the following table is for simple investors and indicates that MRCC is overpriced relative to other BDCs that trade below NAV:

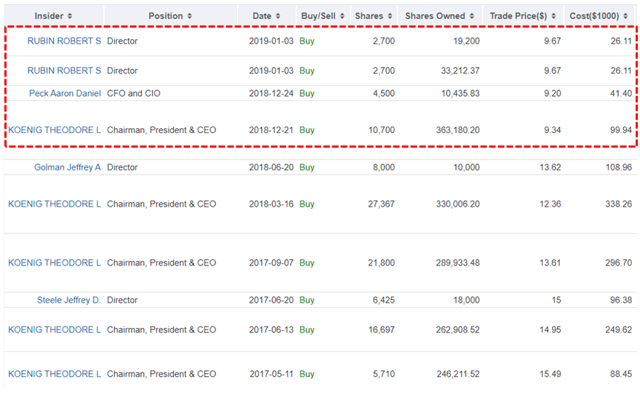

Previous Insider Purchases

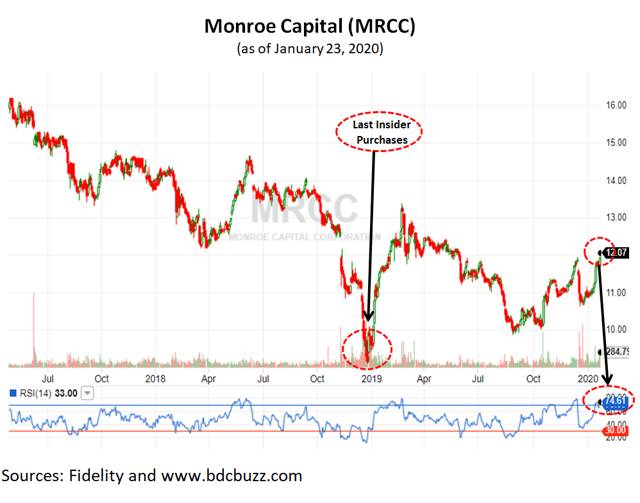

It should be noted that the most recent insider purchases were at prices below $10.00 when the stock was trading at a 25% discount to the reported NAV per share which was $12.95 (at that time).

Source: GuruFocus

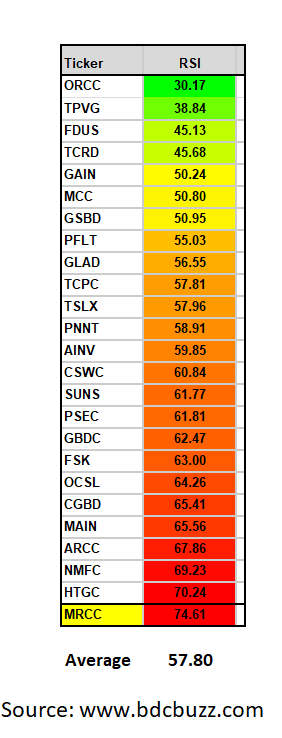

As of January 23, 2020, MRCC had a relative strength index (“RSI”) of almost 75 indicating overbought conditions:

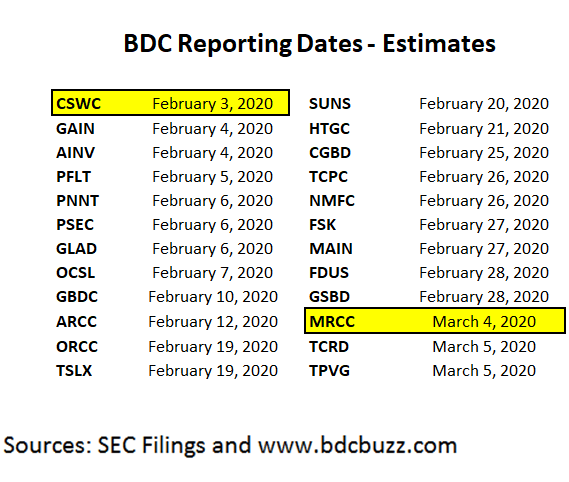

The following chart is not pretty if you are a long-term investor in MRCC and I have recently suggested to my subscribers to sell or at least trim current positions and wait for the company to report Q4 results (see dates below).

As BDCs start to report results two weeks from now starting with CSWC that was discussed in “DGI Capital Southwest Yielding 9.5% Before Upcoming Increases” and easily a better choice compared to MRCC.

Investors should be watching for potential portfolio credit issues that could lead to credit rating downgrades. Lower ratings would likely drive higher borrowing expenses that could put downward pressure on net interest margins and dividend coverage over the coming quarters.

This information was previously made available to subscribers of Premium BDC Reports, along with:

- MRCC target prices and buying points

- MRCC risk profile, potential credit issues, and overall rankings

- MRCC dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.