The following is from the GLAD Update that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

GLAD Update Summary:

- GLAD hit base case projections covering its dividend that remains stable but reliant on continued management fee waivers.

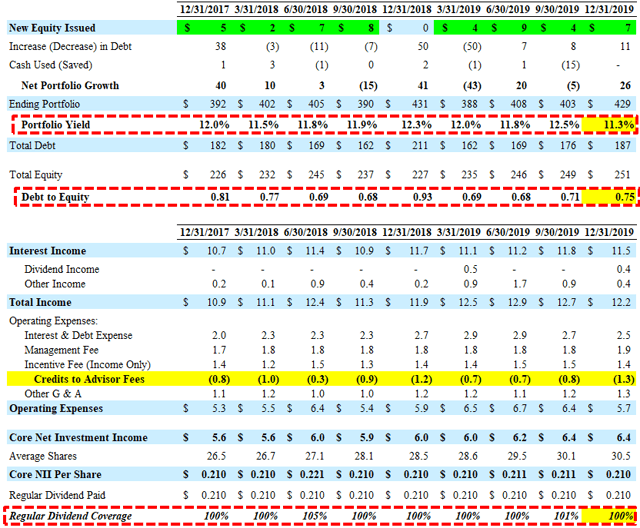

- There was a meaningful decline in its portfolio yield from 12.5% to 11.3% and its debt-to-equity remains near historical levels.

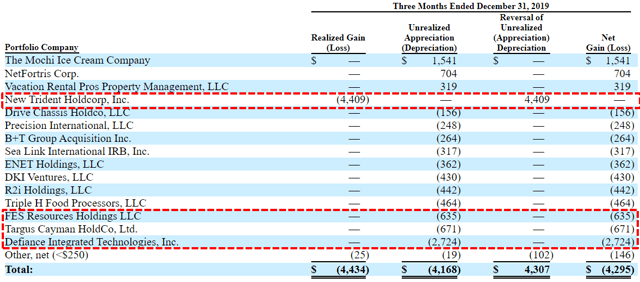

- NAV per share decreased by $0.14 or 1.7% (from $8.22 to $8.08). Most of the largest markdowns during the quarter were equity investments including Defiance Integrated Technologies that was previously marked $3.7 million above cost.

- As predicted, New Trident and Meridian Rack & Pinion were exited resulting in realized losses but did not impact NAV due to being mostly written off.

- The company sold 705,031 shares at a weighted-average price of $10.37 (26% premium to previous NAV) through its ATM program.

- In October 2019, GLAD redeemed its Series 2024 Term Preferred Stock and completed a public debt offering of $38.8 million of 5.375% Notes due 2024 for net proceeds of approximately $37.5 million.

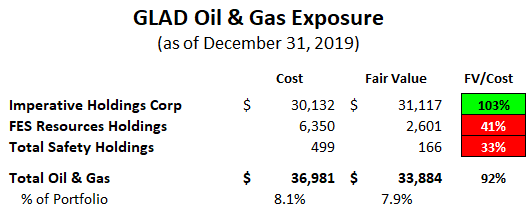

- First-lien debt accounts for around 50% of the portfolio and oil & gas investments now account for around 7.9% (previously 8.7%) of the portfolio fair value due to markdowns and increased overall portfolio size.

December 31, 2019 Results:

Gladstone Capital (GLAD) hit its base case projections covering its dividend due to continued management fee waivers. There was a meaningful decrease in its portfolio yield from 12.5% to 11.3% and its debt-to-equity remained near historical levels. The company sold 705,031 shares at a weighted-average price of $10.37 (26% premium to previous NAV) through its at-the-market (“ATM”) program. In October 2019, GLAD redeemed its Series 2024 Term Preferred Stock and completed a public debt offering of $38.8 million of 5.375% Notes due 2024 for net proceeds of approximately $37.5 million.

Bob Marcotte: “We started fiscal 2020 on a strong note with a healthy level of net originations and a reduction in our financing costs on the quarter which combined to lift our core net interest income despite the pressure associated with the decline in LIBOR. Today, our modest leverage and the added flexibility of BDC leverage relief (with the recent preferred stock redemption), afford us the opportunity to continue to grow our investment portfolio and lift our net interest earnings in the coming quarters to enhance the returns to our shareholders.”

For the three months ended December 31, 2019, net asset value (“NAV”) per share decreased by $0.14 or 1.7% (from $8.22 to $8.08) with realized losses of almost $6 million or $0.19 per share mostly due to exiting New Trident (cost of $4.4 million, fair value of $0.0 million). Also, in January 2020, GLAD exited its non-accrual investment in Meridian Rack & Pinion, Inc. (cost of $5.6 million, fair value of $0.0 million) and realized a loss of $5.6 million or $0.18 per share offset by the sale of its investment in The Mochi Ice Cream Company, which resulted in a realized gain of approximately $2.5 million or $0.08 per share.

Most of the largest markdowns during the quarter were equity investments including Defiance Integrated Technologies that was previously marked $3.7 million above cost but marked down by $2.7 million:

Secured first-lien debt increased from 44% to 50% of the portfolio fair value:

Management previously indicated that it would slowly increase its targeted debt-to-equity ratio from 0.80 to 1.00. In January 2020, GLAD invested:

- $5.5 million in Lignetics, Inc., an existing portfolio company, through a combination of secured second lien debt and preferred equity.

- $3.0 million in Edge Adhesives Holdings, Inc., an existing portfolio company, in the form of preferred equity.

Oil & gas investments declined to 7.9% (previously 8.7%) of the portfolio fair value due to marking down FES Resources Holdings again as well as a larger overall portfolio.

As discussed in previous reports, Francis Drilling Fluids (“FDF”) was restructured in December 2018 upon emergence from Chapter 11 bankruptcy protection. As part of the restructure, its $27 million debt investment in FDF was converted to $1.35 million of preferred equity and common equity units in a new entity, FES Resources Holdings, LLC (“FES Resources”). GLAD also invested an additional $5.0 million in FES Resources through a combination of preferred equity and common equity and was marked down by $3.1 million during calendar Q3 2019.

In March 2019, two of its energy-related portfolio companies, Impact! Chemical Technologies, Inc. (“Impact”) and WadeCo Specialties, Inc. (“WadeCo”), merged to form Imperative Holdings Corporation (“Imperative”). In connection with the merger, GLAD received a principal repayment of $10.9 million and its first-lien loans to Impact and WadeCo were restructured into one $30.0 million second lien debt investment in Imperative.

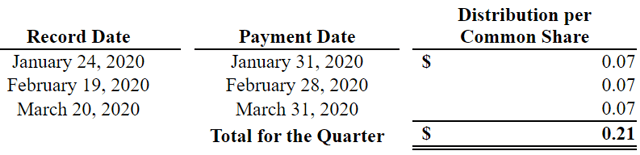

Distributions and Dividends Declared:

In January 2020, the Board of Directors declared the following monthly distributions to common stockholders and monthly dividends to preferred shareholders:

This information was previously made available to subscribers of Premium BDC Reports, along with:

- GLAD target prices and buying points

- GLAD risk profile, potential credit issues, and overall rankings

- GLAD dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.