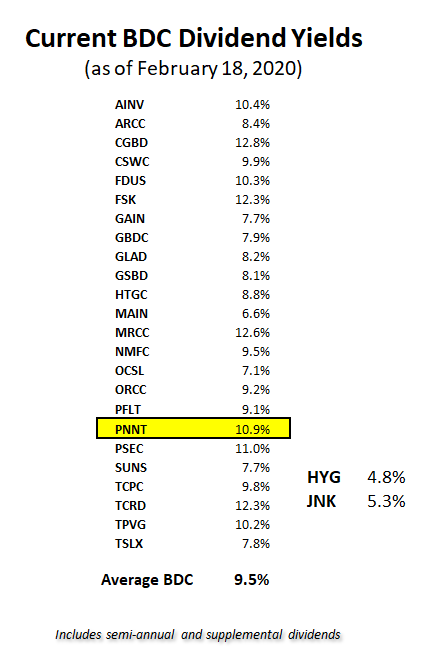

The following is from the PNNT Update that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

PNNT Update Summary:

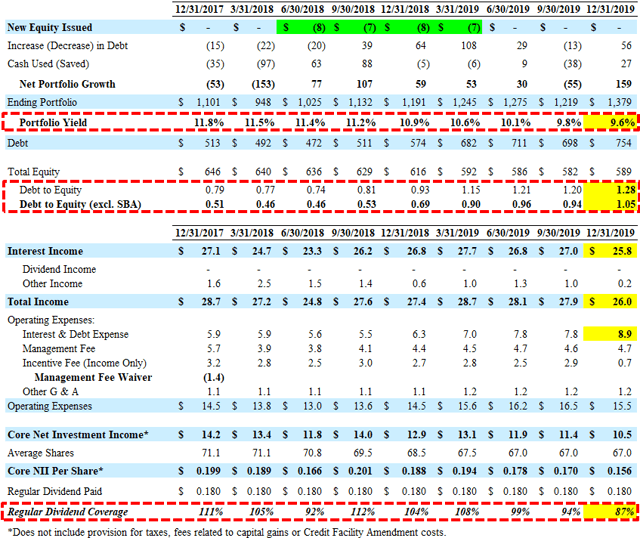

- PNNT reported just below its worst-case projections mostly due to lower-than-expected portfolio yield and “the timing of purchases and sales” only covering 87% of the dividend but should improve next quarter.

- Portfolio growth was much higher-than-expected with almost $174 million of new investments during the quarter but likely weighted toward the end of the quarter.

- Its debt-to-equity is around 1.40 after taking into account almost $63 million “payable for investments purchased” and around 1.16 excluding SBA debentures.

- There was another decline in the overall portfolio yield but management is improving earnings through portfolio growth, rotation out of non-income producing assets and increased leverage available with its “green light” letter for its third SBIC license.

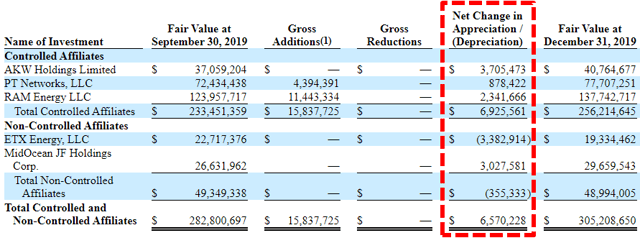

- NAV per share increased by $0.11 or 1.3% (from $8.68 to $8.79) mostly due to marking up some of its equity positions including AKW Holdings and RAM Energy. Also, there was a meaningful markup of its first-lien position in AKW.

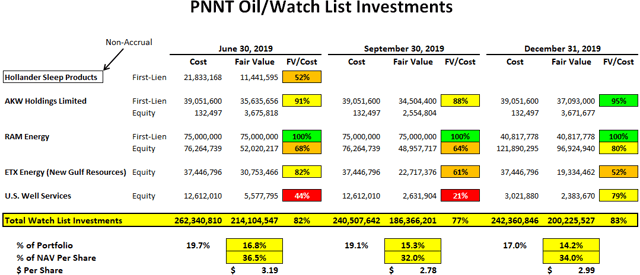

- There are still no investments on non-accrual status and energy, oil & gas exposure decreased from 12.2% to 11.3% of the portfolio due to the increase in the overall size of the portfolio and marking down its investment in ETX Energy by almost $3.4 million partially offset by the markups in RAM Energy.

- Also, PNNT finally exited its publicly traded shares U.S. Well Services (USWS) driving most of the $12 million of realized losses for the quarter.

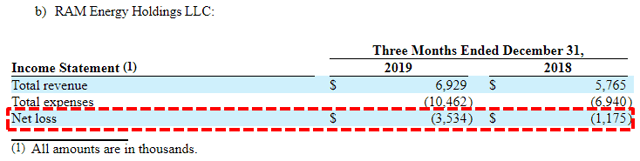

- One of my concerns is the recent markup of PNNT’s equity position in RAM Energy that continues to operate at a loss according to the SEC filings

PennantPark Investment (PNNT) reported just below its worst-case projections mostly due to lower-than-expected portfolio yield and “the timing of purchases and sales”. Portfolio growth was much higher-than-expected with almost $174 million of new investments during the quarter but likely weighted toward the end of the quarter. This means that the company did not receive the full benefit from interest income during the quarter. Also, it should be noted that there was almost $63 million “payable for investments purchased” which is not included in the borrowings and leverage amounts for quarter-end. The debt-to-equity ratio increased from 1.20 to 1.28 or almost 1.40 after taking into account the amounts payable.

Art Penn, Chairman and CEO: “We are pleased with the progress we are making in several areas. Our activity and selectivity have resulted in a more senior secured portfolio, which should result in even more steady and stable earnings. Additionally, our earnings stream should improve over time based on a gradual increase in our debt to equity ratio and the potential for a joint venture, a new SBIC, and the exit of successful equity investments.”

“Non-recurring net debt-related costs” and provision for taxes of $0.3 million are not included when calculating ‘Core NII’ resulting in net investment income (“NII”) per share of $0.156 which only covered 87% of the dividend but should improve next quarter.

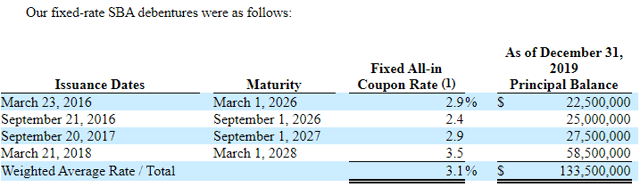

There was another decline in its portfolio yield from 9.8% to 9.6% but management will be offsetting the impact from lower yields through the rotation out of non-income producing assets as well as increasing leverage. The company has significant borrowing capacity due to its SBA leverage at 10-year fixed rates (current average of 3.1%) that are excluded from typical BDC leverage ratios. As mentioned in the previous report, PNNT received “green light” letter for its third SBIC license for an additional $175 million of SBA financing.

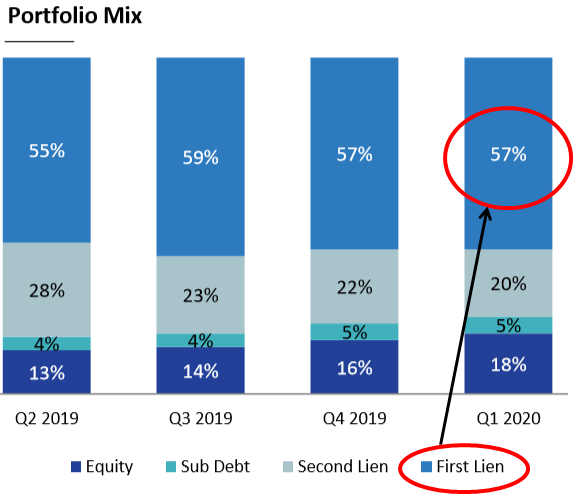

Previously, PNNT was keeping a conservative leverage policy of GAAP debt-to-equity (includes SBA debentures) near 0.80 until it can rotate the portfolio into safer assets.” However, the company has already increased the amount of first-lien debt from 40% to 57% of the portfolio over the last two years and is slowly increasing its regulatory debt-to-equity (excludes SBA debentures) to 1.50:

“Over time we are targeting a regulatory debt-to-equity ratio of 1.1 to 1.5 times. We will not reach this target overnight, we will continue to carefully invest and it may take several quarters to reach the new target. A careful and prudent increase in leverage against primarily first lien assets should lead to higher earnings.”

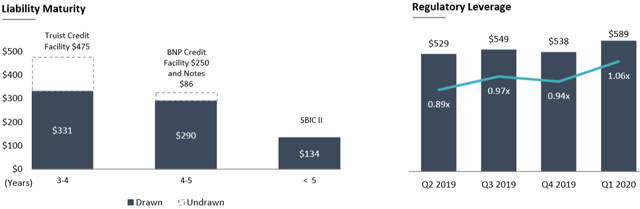

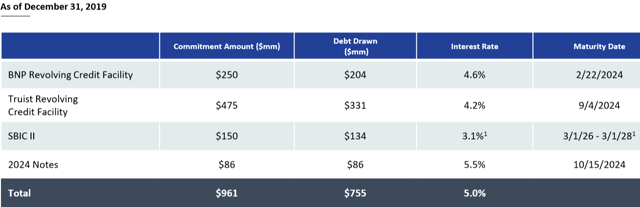

As mentioned earlier, the company had higher-than-expected portfolio growth during the previous quarter driving its debt-to-equity to almost 1.40 after taking into account the amounts payable and around 1.16 excluding SBA debentures. On September 4, 2019, PNNT amended its SunTrust Credit Facility increasing the amount of commitments from $445 million to $475 million and amended the covenants “to enable us to utilize the flexibility and incremental leverage provided by the SBCAA.

“We are pleased that in early September we amended the credit facility enabling us to use the incremental flexibility provided by the new guidelines. Additionally, at the end of September and in early October we completed an $86 million offering of 5.5% unsecured notes. In early October, we also received the green light for our SBIC number three. We are extremely gratified that our long-term track record and excellent relationship with the SBA will result in attractively priced long-term financing for the company.”

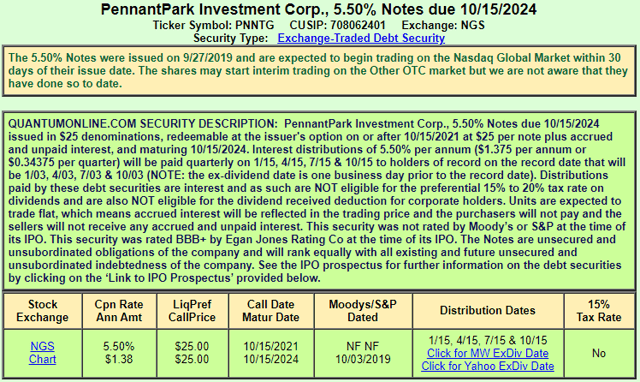

On September 25, 2019, PNNT priced its public offering of $75 million of 5.50% unsecured notes due October 15, 2024, trading under the symbol “PNNTG” and are included in the BDC Google Sheets and currently considered a ‘Hold’.

As shown below, equity investments are now around 18% of the portfolio due to the recent markups discussed next. PNNT will likely continue to use higher leverage as it increases the amount of first-lien positions that account for 57% of the portfolio (up from 40% two years ago).

PNNT’s net asset value (“NAV”) per share increased by $0.11 or 1.3% (from $8.68 to $8.79) mostly due to marking up some of its equity positions including AKW Holdings and RAM Energy.

Also, there was a meaningful markup of its first-lien position in AKW as shown below:

There are still no investments on non-accrual status and energy, oil & gas exposure decreased from 12.2% to 11.3% of the portfolio due to the increase in the overall size of the portfolio and marking down its investment in ETX Energy by almost $3.4 million partially offset by the markups in RAM Energy. Also, PNNT finally exited its publicly traded shares U.S. Well Services (USWS) driving most of the $12 million of realized losses for the quarter.

One of my concerns is the recent markup of PNNT’s equity position in RAM Energy that continues to operate at a loss according to the SEC filings:

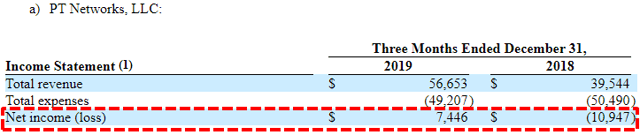

PT Networks was also marked up likely due to improved financials:

Again, there were no additional share repurchases due to only around $0.5 million of availability. Previously, PNNT purchased 1 million shares during the three months ended March 31, 2019, at a weighted average price of around $7.10 per share or a 22% discount to its previously reported NAV per share.

Previous call: “We purchased $7 million of a common stock this quarter as part of our stock repurchase program, which was authorized by our board. We’ve completed our program and have purchased $29.5 million of stock. The stock buyback program is accretive to both NAV and income per share. The accretive effect of our share buyback was $0.03 per share.”

This information was previously made available to subscribers of Premium BDC Reports, along with:

- PNNT target prices and buying points

- PNNT risk profile, potential credit issues, and overall rankings

- PNNT dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.