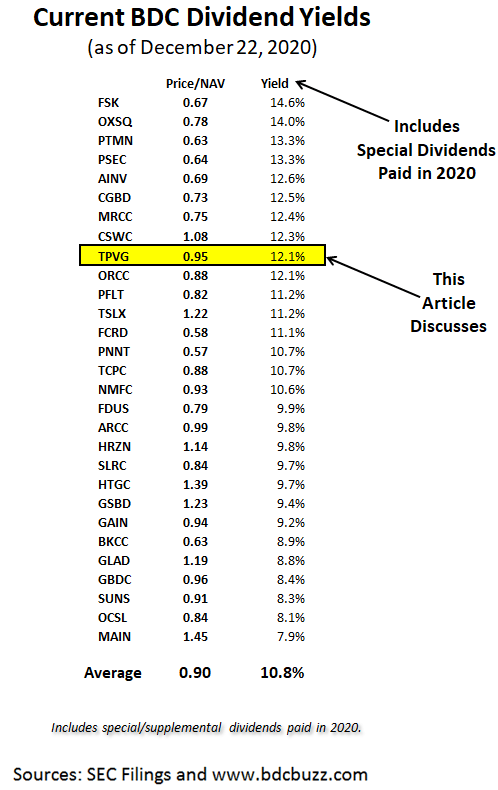

- The BDC sector continues to deliver strong returns during the pandemic, including recently improved earnings, dividend coverage, and increased book values.

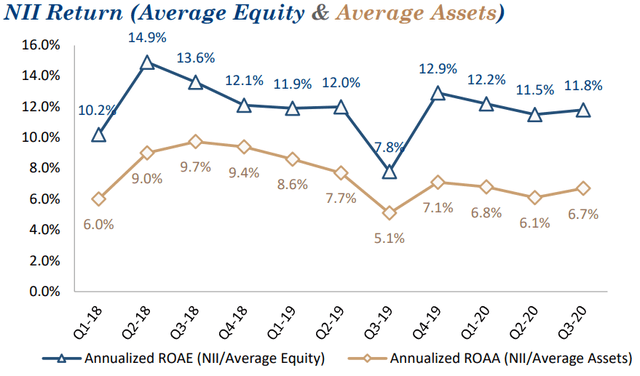

- The average BDC is currently yielding 10.8% with an average dividend coverage ratio of 110% for Q3 2020 and improving net interest margins.

- This article discusses TPVG that I recently purchased currently yielding 12% annually taking into account the special dividend announced last week.

Introduction

The following information discussing TriplePoint Venture Growth (TPVG) was previously provided in the public article “Oasis Of Dividends From This 10.8% Yielding Sector“. Please read when you get a chance as it provides additional details discussing the overall BDC sector.

BDCs reported calendar Q3 2020 results last month, most with very strong earnings and average dividend coverage of around 110%. Also, they almost all reported meaningful increases in net interest margins due to higher portfolio yields and/or reduced borrowing expenses including TriplePoint Venture Growth (TPVG), which is discussed in this article.

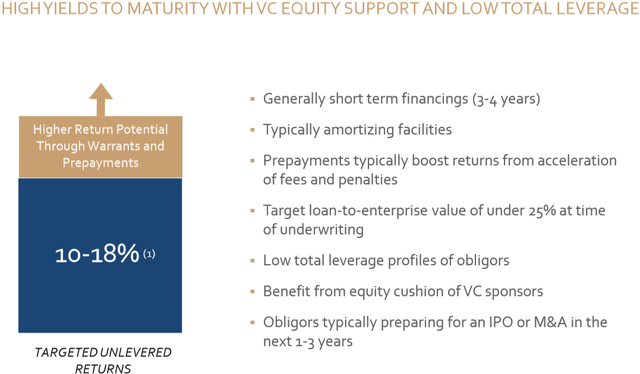

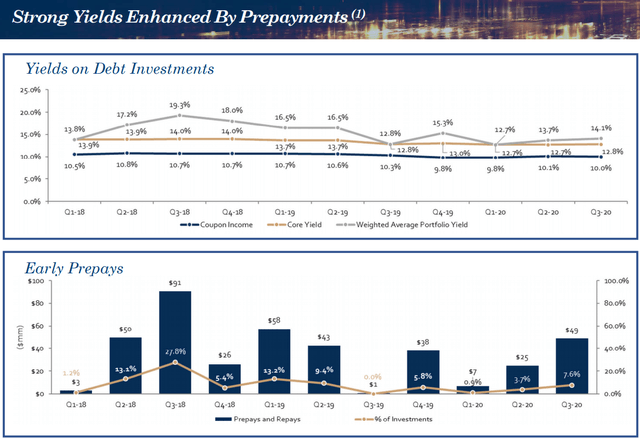

There are many factors to take into account when assessing dividend coverage for BDCs including portfolio credit quality, potential portfolio growth using leverage or equity offerings, fee structures including “total return hurdles” taking into account capital losses, changes to portfolio yields and borrowing rates, the amount of non-recurring and non-cash income including payment-in-kind (“PIK”). A portion of the reported earnings each quarter for TPVG is related to the accrual of the end of term (“EOT”) payment that ranges from 2% to 12% providing higher effective yields. EOT payments provide upside potential when loans are repaid earlier. However, this contractual payment is accrued and added to income but not paid in cash until the loan is repaid.

Source: TPVG Earnings Call Presentation

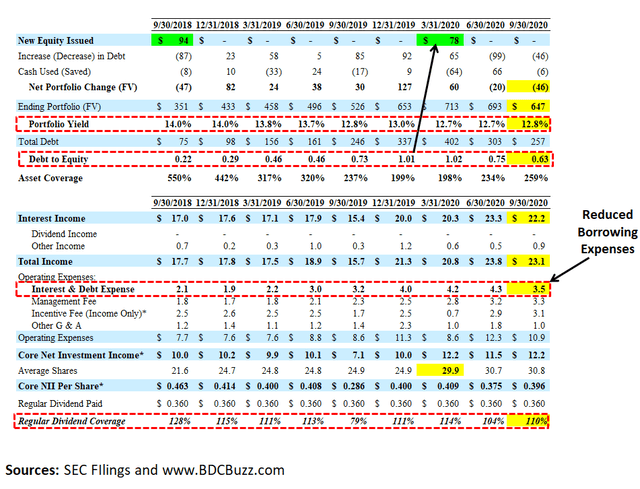

For the three months ended September 30, 2020, TPVG reported between my base and best-case projections covering its dividend by 110% with a higher-than-expected portfolio yield due to prepayment-related income. As shown below, the company reduced its debt-to-equity ratio from the upper end of its target range (1.00) to 0.63 giving the company plenty of growth capital.

Since September 30, 2020, and through November 4, 2020:

- Nestle USA announced that it acquired TPVG portfolio company, Freshly Inc.; TPVG portfolio company Hims, Inc. announced plans to go public through a merger with Oaktree Acquisition Corp.; and TPVG portfolio company Qubole was acquired by Idera;

- Received $32.0 million of principal prepayments generating approximately $2.4 million of prepayment fees and interest income;

- Entered into $30.0 million of additional non-binding signed term sheets with venture growth stage companies;

- Closed $15.0 million of additional debt commitments; and

- Funded $6.0 million in new investments.

This information has been taken into account with my updated projections.

We are pleased to see the levels of exit, liquidity and prepayment events within our portfolio. These events generate exceptional returns on our investments and give us the flexibility to efficiently redeploy our capital.”

Source: TPVG Earnings Call

Source: TPVG Earnings Call Presentation

On October 29, 2020, the company’s board of directors declared a quarterly distribution of $0.36 per share for the fourth quarter of 2020, payable on December 14, 2020, to stockholders of record as of November 27, 2020. TPVG had around $10 million or $0.33 per share of “spillover” or undistributed income that can be used for temporary coverage shortfalls. On the recent call management mentioned that this amount could be used for “additional distributions to shareholders in the future” which could imply regular and/or supplemental dividends:

“During the third quarter, we just we distributed $0.36 per share from ordinary income as part of our regular quarterly distribution. Net investment income provided 110% coverage of the quarterly distribution, despite leverage being at the lower end of our target range. And further, we have undistributed earnings spillover from net investment income of approximately $10 million or another $0.33 per share to support additional distributions to shareholders in the future.”

Source: TPVG Earnings Call

The following discussion was from a previous call:

Q. What degree of confidence do you have in your portfolio providing earnings at this run rate – at the dividend run rate beyond the second quarter?”

A. I think that the Board always has the discussion, and it’s a prudent thing to do. So I think that we were just kind of elaborating and sharing those conversations that are natural for each quarter that we’re talking about at a distribution level. I think just given the robust discussion that always happens, we thought it would be fair to say that we are comfortable where we are with the portfolio, with the additional leverage that we have and the earnings power of the portfolio.”

As predicted in “TPVG Projections/Pricing Update (Includes Baby Bond): Upgraded Again!” TPVG announced a special dividend of $0.10 per share payable on January 13, 2021, to shareholders of record at the close of business on December 31, 2020. More importantly, was the mention of significant capital gains in 2020 which likely implies additional gains in Q4 as well as the confidence that the Board has in paying additional amounts to shareholders.

The special dividend represents a portion of the Company’s estimated net capital gain income earned during the fiscal year. The anticipated remaining undistributed net capital gain income along with the Company’s estimated undistributed taxable earnings from net investment income, which was $10.0 million or $0.33 per share, as of September 30, 2020, will spill-over into 2021.

“We benefited from our warrant and equity portfolio in 2020, generating significant capital gains for shareholders. The declaration of our third special distribution since our IPO highlights the powerful warrant and equity investment components of our returns and underscores TPVG’s differentiated business model. We are uniquely positioned to generate additional long-term shareholder returns from our warrant and equity investments.”

Source: TPVG Press Release

TPVG Risk Profile Update

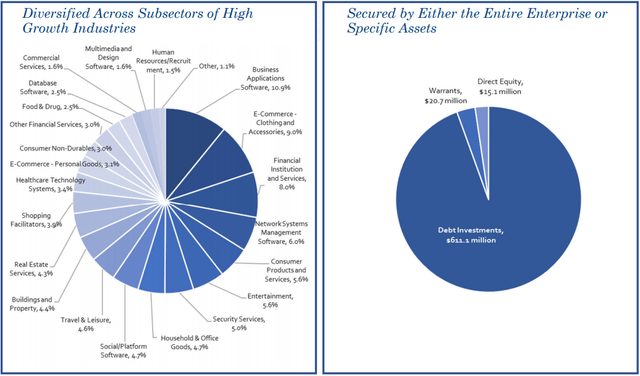

TPVG provides financing primarily to venture capital (“VC”) backed technology companies at the venture growth stage (see the end of this report), similar to Hercules (NYSE:HTGC) and Horizon (NASDAQ:HRZN). As discussed in previous reports, TPVG has historically had portfolio concentration risk and management is actively working to diversify the portfolio using the ability to co-invest across the broader platform and likely one of the reasons for the previous equity offering. The top five positions currently account for around 28% of the portfolio compared to 44% in December 2018 and 57% in early 2018.

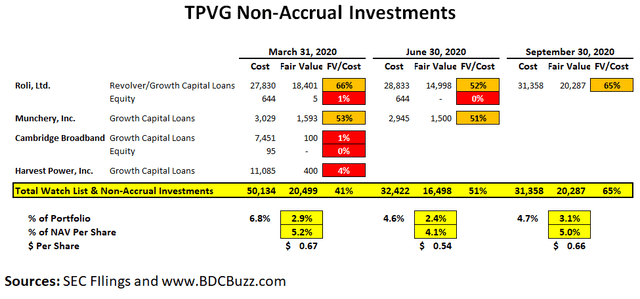

During Q3 2020, TPVG recognized net realized gains of $4.1 million including $6.0 million of realized gains from the sale of publicly traded shares held in CrowdStrike, Inc. (OTC:CRWD) and Medallia, Inc. (MDLA), offset by $1.9 million of realized losses from the finalization of asset sales of Munchery, Inc., which was rated Red (5) on the credit watch list.

There were no additional investments added to non-accrual status during Q3 2020. As mentioned earlier, TVPG finally exited its non-accrual investments in Munchery, Inc. However, TPVG invested an additional $2.5 million in Roli Ltd. as well as was marked up a portion of the investment increasing non-accruals from 2.4% to 3.1% of the portfolio fair value and from 4.6% to 4.7% at cost. This was discussed on the recent call:

We have only one company rated 4 on our watch list. ROLI, a music technology company. During the quarter we saw an increase in the value of our position in ROLI as a result of progress the company made during the quarter, which culminated in the launch of their LUMI keyboard on October 1st, favorable product reviews and strong initial demand and sales. We hope to see momentum – we hope to see this momentum translate into continued favorable trends for the company and our investment. We are in the process of working on a global restructuring of our outstanding indebtedness with them, based on that – we were waiting for the product launch and positive developments that happened during the third quarter.”

Source: TPVG Earnings Call

If these TPVG’s non-accrual investments were completely written off it would impact NAV per share by around $0.66 or 5.0%:

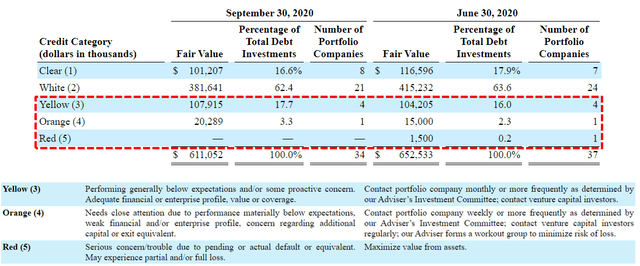

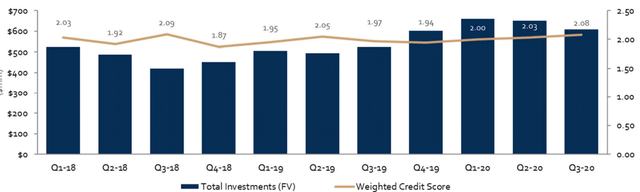

TPVG maintains a credit watch list with portfolio companies placed into one of five categories, with Clear, or 1, being the highest rating and Red, or 5, being the lowest. Generally, all new loans receive an initial grade of White, or 2. Munchery was its only Red (5) and was sold during Q3 2020. As of September 30, 2020, the weighted average investment ranking of its debt investment portfolio was 2.08, as compared to 2.03 as of the end of the prior quarter.

Source: SEC Filing

Source: TPVG Earnings Call Presentation

There will likely be additional liquidity and realized gains from exiting its equity investments including its remaining 16,747 shares of CRWD valued at $2.3 million over cost and 18,616 shares of MDLA valued at $0.5 million over cost as of September 30, 2020.

We sold a portion of our holdings in CrowdStrike, resulting in additional $4.9 million of realized gains in Q3, bringing our total to $24.3 million have realized gains on that name alone and also recorded $1.1 million of realized gains on our Medallia holdings. We continue to hold shares in both companies, representing $2.7 million of unrealized gain as of September 30th, and expect to exit our remaining positions over the next one quarter to two quarters.”

Source: TPVG Earnings Call

Source: Yahoo

TPVG has around $46 million invested in Prodigy Finance Limited which lends to international graduate students and is currently marked at full value likely due to:

Q. Looking at Prodigy Finance, that’s a decent sized maturity at the end of 2020, now 18.7 million. My understanding is that student loans for international students which I’d imagine with my limited information is pretty challenged. Is there any context or color you can provide on the status of that lender obligation?”

A. So, just to clarify that’s a lender to international graduate students. So, I’d say Prodigy lends to those graduate students attending top tier business school, engineering school and law school. So, the folks that have a higher likelihood of getting jobs regardless of crisis. So, I would say the very focused approach or thoughtful approach, they’re not lending to under grads, they’re not lending to just any graduate programs but very focused on those degrees particularly again business schools, engineering schools and then a small percentage of law schools. And then top schools only. So, I’d say the good news is very focused on higher quality company or sorry obligor based than traditional students.”

Source: TPVG Earnings Call

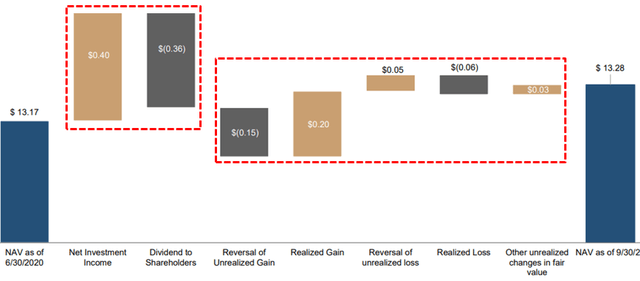

During Q3 2020, TPVG’s net asset value (“NAV”) per share increased by less than expected $0.11 or 0.8% (from $13.17 to $13.28 mostly due to over-earning the dividend by $0.04 per share and net realized/unrealized gains of $0.07 per share.

Source: TPVG Earnings Call Presentation

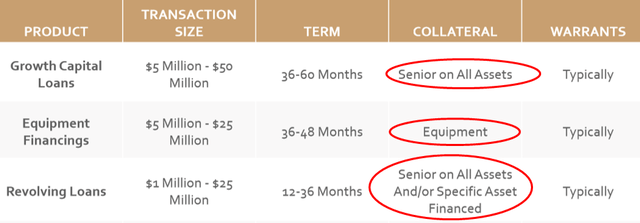

TPVG’s portfolio is typically around 90% debt investments structured as “growth capital loans” or “equipment financing” and mostly backed by a senior position on all assets (see below), typically with warrants that provide upside potential. However, around 31% of growth capital loans are with borrowers that have other facilities in a senior position to TPVG and I have classified as “second lien.”

Source: TPVG Earnings Call Presentation

I consider TPVG to have a safer-than-average risk profile due to mostly 1st lien positions with VC equity support. The following discussion is from the recent earnings call:

During the quarter, four portfolio companies raised over $430 million of capital. This brings our total to 22 portfolio companies raising over $2.8 billion of capital since the beginning of the year, approximately 70% of our portfolio companies have 12 months or more of cash runway.”

Growth activity well underway here in the fourth quarter. We believe this positive trend will continue in our business and serve as a basis for meaningful growth in 2021. This is due to several reasons. The first is our focus on technology. We are living in a different world in one of uneven consequences. The technology sector is one of the more sustainable parts of the economy today and is an area for investment for the foreseeable future. TriplePoint will continue to benefit from this trend as we provide loans and invest primarily in technology-driven companies and sectors, many of them experiencing tailwinds and stand to benefit in this environment.”

Many of our portfolio companies operate in the virtual and digital technology world today, and TPVG is well positioned to take advantage of this ecosystem as new venture capital investments remain focused in it. We’re seeing this not only within our own portfolio companies, but within the broader venture ecosystem as well, further validating the needs of these companies for venture lending. This activity continues to be robust this year and includes everything from the emergence of these facts to multi-billion dollar acquisition exits. Increase opportunities for venture lending in today’s environment also includes providing financing for many of the companies out there that are actively considering opportunistic acquisitions in the COVID era.”

Source: TPVG Earnings Call

Source: TPVG Earnings Call Presentation

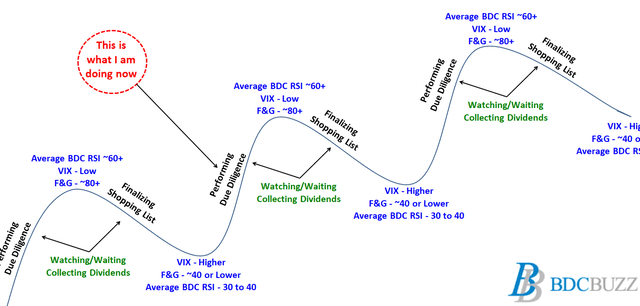

Volatility is your friend!

BDC pricing can be volatile and timing is everything for investors that want to get the “biggest bang for their buck” but still have a higher-quality portfolio that will deliver higher-than-average returns over the long term. One of my goals is to help subscribers take advantage of “oversold” conditions.

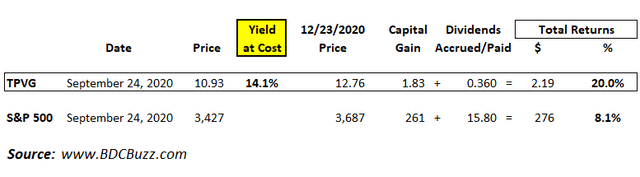

On September 24, 2020, the Fear & Greed Index (“F&G” in the chart above) hit 40 and I purchased shares in six BDCs including TPVG all of which have easily outperformed the S&P 500 during the same period. I will be discussing the other five BDCs in upcoming articles.

Full BDC Reports

This information was previously made available to subscribers of Premium BDC Reports, along with:

- TPVG target prices and buying points

- TPVG risk profile, potential credit issues, and overall rankings

- TPVG dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

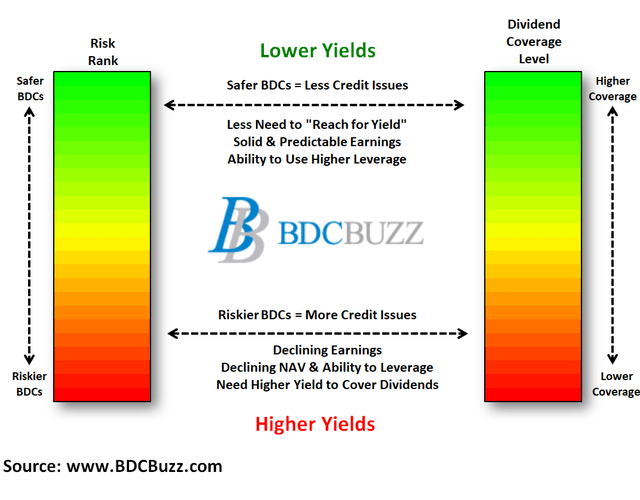

BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.

To be a successful BDC investor:

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Diversify your BDC portfolio with at least five companies. There are around 45 publicly traded BDCs; please be selective.