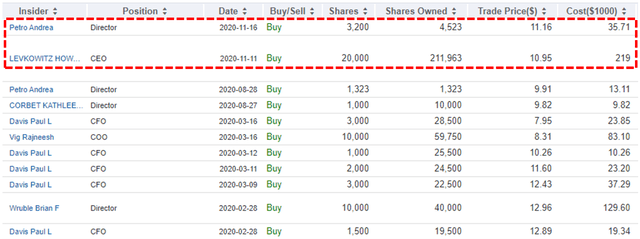

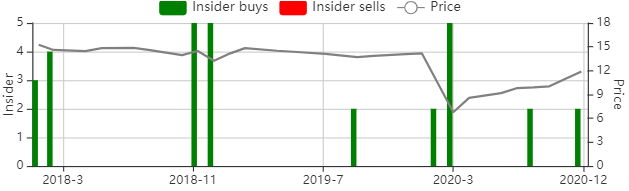

Previous TCPC Insider Purchases

- Last month, Howard Levkowitz, TCPC Chairman and CEO, purchased 20,000 shares at $10.95 per share for a total of $219,000.

TCPC Dividend Coverage Update

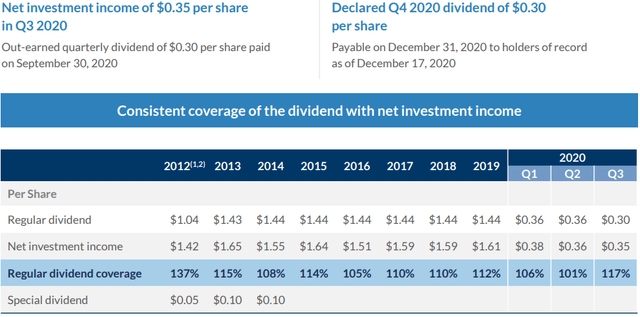

Previous reports correctly predicted the reduction of TCPC’s quarterly dividend from $0.36 to $0.30 which was at the top of my estimated range of $0.28 to $0.30. At the time, the company had spillover or undistributed taxable income (“UTI”) of almost $45 million or $0.78 per share. However, this is typically used for temporary dividend coverage issues. The previously projected lower dividend coverage was mostly due to lower LIBOR and portfolio yield combined with management keeping lower leverage to retain its investment-grade rating.

Howard Levkowitz, TCPC Chairman and CEO: “The board’s decision to adjust the dividend rate was a prudent response to substantial declines in LIBOR over the last year and a half. We are confident in the sustainability of our dividend at this level. We also strengthened our diversified and low-cost leverage program by extending and expanding our SVCP credit facility and replacing our TCPC Funding credit facility with a new facility with improved terms. We appreciate the ongoing support of our lenders.”

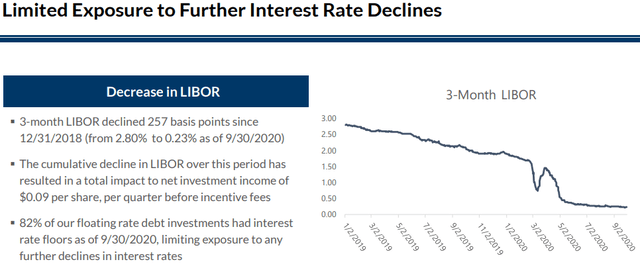

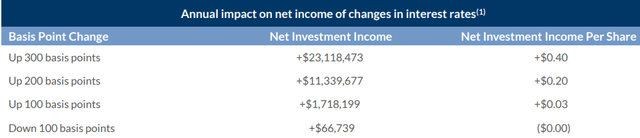

The rapid decline in interest rates (LIBOR) has mostly been responsible for the decline in portfolio yield with “limited exposure to any further declines”. During Q3 2020 there was an increase in the overall portfolio yield due to “amendments made on several loans coupled with the higher yield on originations versus exits”:

“Investments in new portfolio of companies during the quarter had a weighted average effective yield of 9.5%. Investments we exited had a weighted average effective yield of 8.8%. The overall effective yield on our debt portfolio increased to 10%, primarily reflecting amendments made on several loans coupled with the higher yield on originations versus exits. Since the end of 2018, LIBOR declined 257 basis points or by 92%, which put pressure on our portfolio yield over this period. However, our portfolio is largely protected from any further declines in interest rates as over 80% of our floating rate loans are currently operating with LIBOR floors as demonstrated on slide nine.”

Historically, the company has consistently over-earned its dividend with undistributed taxable income. Management previously indicated that the company will likely retain the spillover income and use it for reinvestment and growing NAV per share and quarterly NII rather than special dividends.

“Today, we declared a fourth quarter dividend of $0.30 per share payable on December 31, 2020 to shareholders of record as of December 17 and in line with the third quarter dividend of $0.30 per share paid on September 30th. We are committed to paying sustainable dividends and continuing our track record of having covered our dividend every quarter as a public company. In the third quarter, our dividend coverage ratio was 117%.”

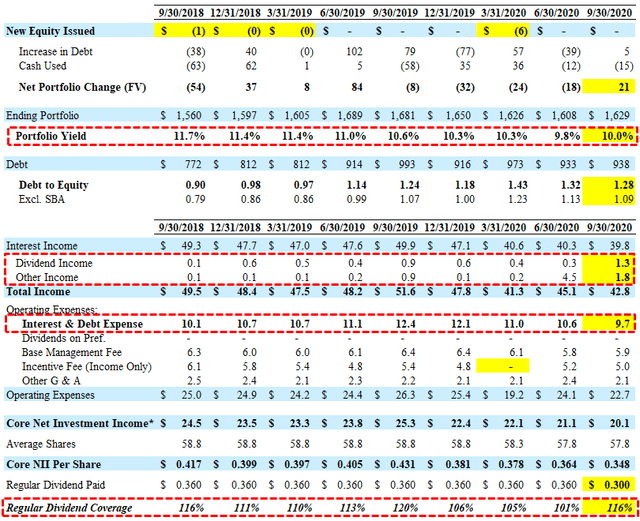

For Q3 2020, TCPC beat its best-case projections mostly due to much higher-than-expected dividend and other income as well as improved portfolio yield and $0.03 per share of income related to prepayment premiums and accelerated original issue discount amortization. Its net interest margin improved due to the higher yield combined with lower borrowing rates.

“Investment income for the third quarter was $0.74 per share. This included recurring cash interest of $0.54, recurring discount and fee amortization of $0.06 and PIK income of $0.06. We had modest prepayments in the quarter that contributed $0.03 per share including both prepayment fees and unamortized OID. Investment income also included $0.03 of other income and $0.02 of dividend income. Our income recognition follows our conservative policy of generally amortizing upfront economics over the life of an investment rather than recognizing all of it at the time the investment is made. Combined, our outstanding liabilities had a weighted average interest rate of 3.3%, down from 3.8% or 51 basis points since the end of 2019.”

On October 29, 2020, the Board re-approved its stock repurchase plan to acquire up to $50 million of common stock “at prices at certain thresholds below our net asset value per share”. There were no additional shares repurchased during Q3 2020. From October 1, 2020 through October 30, 2020, TCPC has invested approximately $18 million primarily in three senior secured loan with a combined effective yield of approximately 10.9%.

Howard Levkowitz, TCPC Chairman and CEO: “We are pleased with the continuing strength of our highly diversified portfolio even in this challenging environment, which led to a 4.1% increase in NAV. We also further strengthened our leverage structure by increasing our unsecured debt, adding an accordion commitment to our operating facility, and replacing our funding facility on even better terms. While we remain highly selective in this lending environment, our pipeline of investment opportunities is growing, and we are prudently deploying capital to achieve strong risk-adjusted returns for our shareholders.”

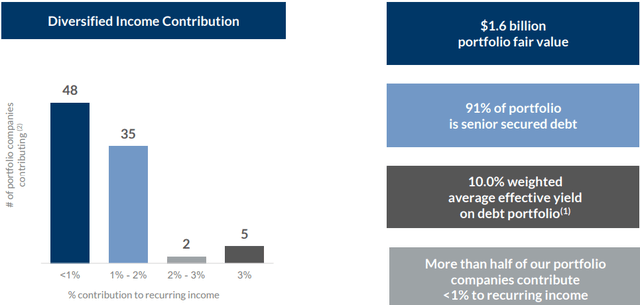

Payment-in-kind (“PIK”) income declined from 7.6% in Q2 2020 to 7.4% in Q3 2020 and needs to be watched. As shown below, TCPC’s portfolio is highly diversified by borrower and sector with only 5 portfolio companies that contribute 3% or more to dividend coverage:

TCPC Risk Profile Update

During Q3 2020, TCPC’s net asset value (“NAV”) per share increased by another $0.50 or 4.1% (from $12.21 to $12.51) “primarily driven by continued spread tightening”:

“Our net asset value increased 4.1% from the prior quarter, reflecting a 1.8% net market value gain on our investments, driven by spread narrowing on middle market private credit transactions as well as improved financial results for several portfolio companies. Importantly, the overall credit quality of our portfolio remains strong.”

Some of the largest markups during the quarter were Edmentum and One Sky Flight:

“Unrealized gains included $6.9 million of appreciation in the value of our investment in Edmentum and $4.4 million of appreciation on our investment in OneSky. The strong performance at One Sky as charter flight activity has outpaced expectations and Edmentum continues to benefit from a shift toward online learning that has accelerated in the current environment.”

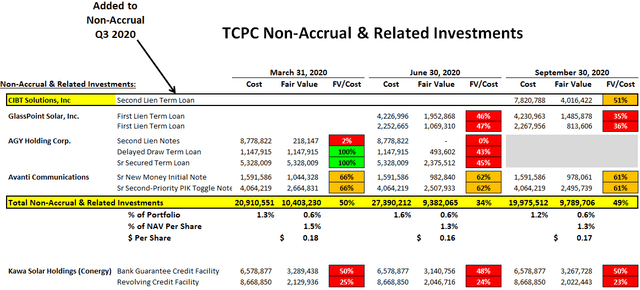

However, there were net realized losses of $18 million or $0.31 per share mostly due to the restructuring of its non-accrual investment in AGY Holding Corp that was discussed on the call:

“Net realized losses during the quarter were comprised primarily of the restructuring of our investment in AGY. AGY is fundamentally good business, but it has struggled with the cost of one of its major inputs rhodium. And we reached the conclusion that it was more appropriate to let a third party come into the business and pay down our position and sell down significant part of our economics and retain small preferred upside.”

CIBT Solutions, Inc. was added to non-accrual status during Q3 2020 and is a provider of expedited travel document processing services serving multinational corporations, global travel management companies, tour and cruise operators, government agencies and Do-It-Yourself travelers. GlassPoint Solar, Inc. and Avanti Communications remain on non-accrual. As of June 30, 2020, loans on non-accrual status represented 0.6% of the portfolio at fair value and 1.2% at cost. If these investments were completely written off the impact to NAV per share would be around $0.17 or 1.3%.

“As of September 30, total non-accruals were only 0.6% of the portfolio at fair value. This is a testament to our disciplined approach to underwriting, our more than 20 years of experience lending to middle market companies and the strength and breadth of the BlackRock platform.”

“We have loans to just three portfolio companies on non-accrual, GlassPoint, CIBT, and Avanti, which together represented only 0.6% of the portfolio at fair value and 1.2% of costs. CIBT, which is new this quarter is a leading global provider of immigration and visa services for corporations and individuals and the company has been challenged, given the current slowdown in international travel.”

TCPC will likely finally exit its investment in Kawa Solar Holdings “in the near future”:

“Kawa Solar Holdings is part of a larger series of securities and some of the loans in certain regions were paid off via loans [ph]. The Kawa loans, I believe, were also paid off and then what’s remaining is, some of the equity that was converted in the APAC region, which is the outstanding position. So the loans that were paid off are no longer on the balance sheet and there were a number that were successfully completed. What remains is simply the equity position as part of a conversion in Asia. That’s in a run-off mode that we’ve talked about a few times in the past. The primary asset is also an operating facility that we expect to exit at some point in the near future as we’re going through a process there.”

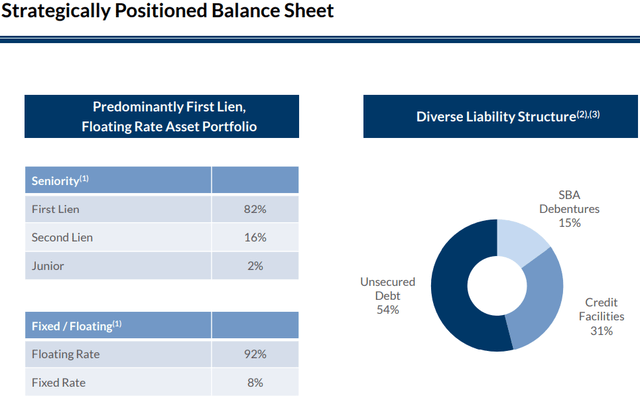

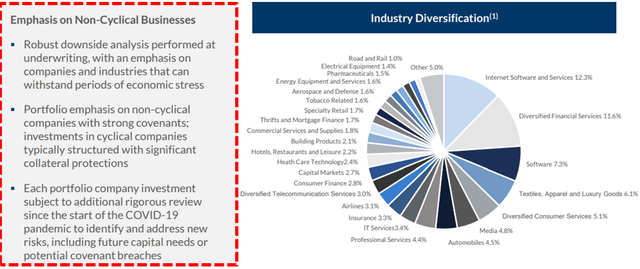

“91% of our investments are senior secured debt and are spread across a wide variety of industries. We have a diverse portfolio of companies with an emphasis on less cyclical businesses with limited direct exposure to sectors that have been more severely affected by the pandemic. Furthermore, our loans to companies in more impacted industries including retail and airlines are generally supported by strong collateral protections and most of our investments in these industries continue to perform well. As an example, the value of our investment in OneSky, the second largest provider of private jet aviation services in the country appreciated during the quarter based on strong performance, resulting from increased charter flight activity. At the end of the third quarter, our diverse portfolio included 101 companies. Our largest position, which represented only 4.5% of the portfolio is an equipment leasing company that itself has a highly diversified underlying portfolio of lease assets. As the chart on the left side of slide seven illustrates, our recurring income is not reliant on income from any one portfolio company. In fact, over half of our individual portfolio companies contribute less than 1% to our recurring income.”

“Our investment activity in the fourth quarter to-date has been selective and focused on companies that are minimally impacted by the pandemic or beneficiaries of the COVID impacted operating environment. Dispositions in the third quarter included payoffs of our $29 million loan to InMobi, our $16 million loan to American Broadband and the refinancing of our $11 million loan to Pulse Secure.”

Volatility is your friend!

BDC pricing can be volatile and timing is everything for investors that want to get the “biggest bang for their buck” but still have a higher-quality portfolio that will deliver higher-than-average returns over the long term. One of my goals is to help subscribers take advantage of “oversold” conditions.

Full BDC Reports

This information was previously made available to subscribers of Premium BDC Reports, along with:

- TCPC target prices and buying points

- TCPC risk profile, potential credit issues, and overall rankings

- TCPC dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

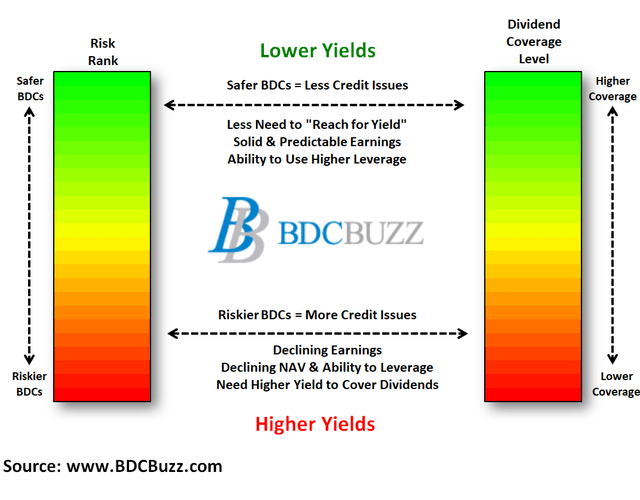

BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.

To be a successful BDC investor:

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Diversify your BDC portfolio with at least five companies. There are around 45 publicly traded BDCs; please be selective.