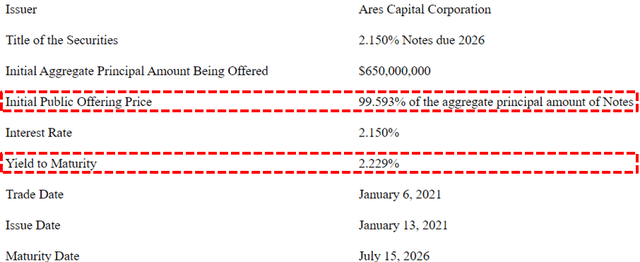

ARCC Issues An Additional $650 Million 2.150% Unsecured Notes Due 2026

-

The following information was previously covered in a public on Seeking Alpha “Ares Capital: 9.4% Yield, Provides Preliminary Results“.

On January 13, 2021, ARCC closed an offering of $650 million of its 2.150% unsecured notes due 2026 at a slight discount of 99.593% of their principal amount, resulting in estimated net proceeds, after estimated offering expenses, of approximately $641.2 million. It should be noted that issuing notes at a discount drives a slightly higher yield-to-maturity of 2.229%.

This is an extremely low fixed rate for an unsecured note due 2026. Many BDCs have been issuing unsecured notes which adds tremendous flexibility to their balance sheets not to mention maintaining net interest margins with the potential to invest at higher rates later this year. This means that we will likely see maintained or even improved earnings over the coming quarters resulting in sustainable dividends.

Source: SEC Filing

Included in the SEC filings related to the offering were the following preliminary results through December 28, 2020:

- Sold 0.2 million shares for ~$4 million.

- Funded $2.5 billion of new investments at a weighted average yield of 7.7%.

- Exited $2.8 billion of investments at a weighted average yield of 7.2%.

- Net realized losses of $177 million or around $0.42 per share.

- These realized losses were offset by $199 million of reversed unrealized losses.

ARCC’s portfolio is/was over $14 billion so there will only be a slightly positive impact on the overall portfolio yield. The realized losses were due to exiting or restructuring quite a few of its non-accrual investments but there should be a slightly positive impact to NAV per share as they were completely offset by the reversal of previous unrealized losses. This would imply that the company exited/sold these investments at a higher price (on average) than the fair value as of September 30, 2020.

From October 1, 2020 through December 28, 2020, we sold an aggregate of approximately 0.2 million shares of common stock for total net proceeds of approximately $4 million under our equity distribution agreements with Truist Securities Inc. and Regions Securities LLC.”

“From October 1, 2020 through December 28, 2020, we made new investment commitments of approximately $3.2 billion, of which $2.5 billion were funded. Of these new commitments, 78% were in first lien senior secured loans, 16% were in second lien senior secured loans, 4% were in preferred equity securities and 2% were in other equity securities. Of the approximately $3.2 billion of new investment commitments, 94% were floating rate, 4% were fixed rate and 2% were non-interest bearing. The weighted average yield of debt and other income producing securities funded during the period at amortized cost was 7.7%.”

“From October 1, 2020 through December 28, 2020, we exited approximately $2.8 billion of investment commitments. Of the total investment commitments, 79% were first lien senior secured loans, 15% were second lien senior secured loans, 2% were subordinated certificates of the SDLP, 2% were senior subordinated loans, 1% were other equity securities and 1% were collateralized loan obligations. Of the approximately $2.8 billion of exited investment commitments, 89% were floating rate, 8% were on non-accrual status, 2% were non-income producing and 1% were fixed rate. The weighted average yield of debt and other income producing securities exited or repaid during the period at amortized cost was 8.0% and the weighted average yield on total investments exited or repaid during the period at amortized cost was 7.2%. On the approximately $2.8 billion of investment commitments exited from October 1, 2020 through December 28, 2020, we recognized total net realized losses of approximately $177 million. As a result of the investment commitments exited, we reversed previously recorded net unrealized depreciation related to such net realized losses of approximately $199 million.”

“In addition, as of December 28, 2020, we had an investment backlog and pipeline of approximately $1.1 billion and $15 million, respectively.”

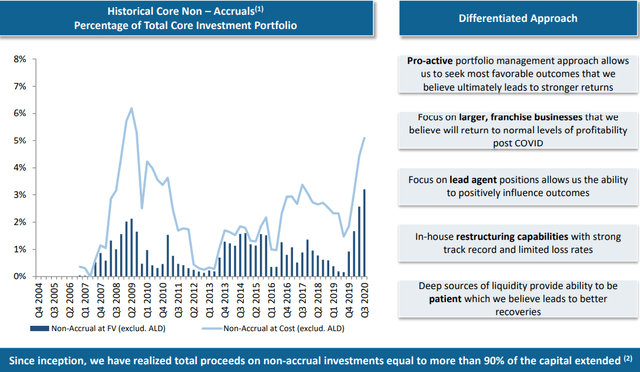

ARCC Portfolio Credit/Non-Accruals Update

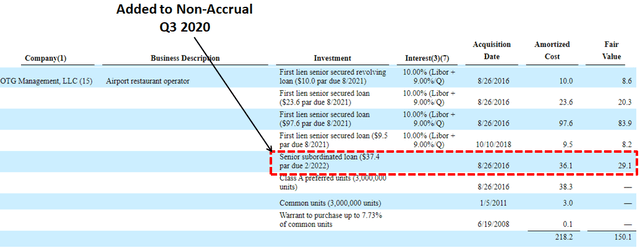

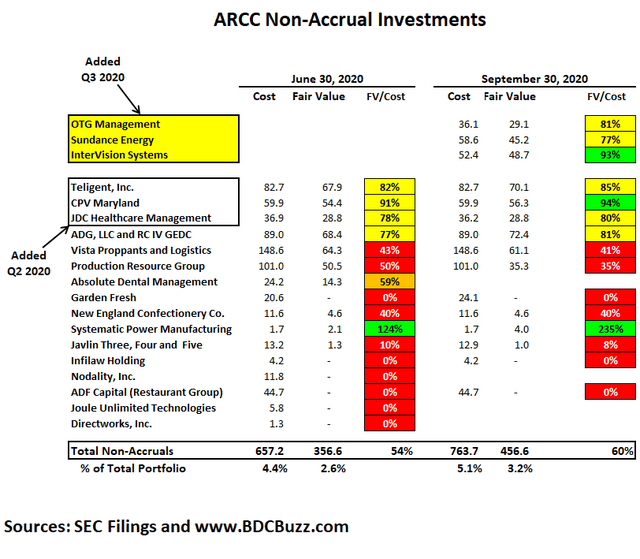

During Q3 2020, non-accrual investments increased from 2.6% to 3.2% of fair value (from 4.4% to 5.1% of cost) of the total portfolio due to adding OTG Management, Sundance Energy, and InterVision Systems with the weighted average grade of the investments in the portfolio at fair value remains around 2.9. As mentioned in the previous report, OTG Management is an airport restaurant operator that was partially added to non-accrual status during Q3 2020 and continues to be marked down currently at 69% of cost and accounts for around 1.0% of the portfolio and $0.36 per share or 2.2% of NAV.

Source: SEC Filing

As mentioned earlier, the company will likely have around $177 million or around $0.42 per share of realized losses in Q4 2020 mostly related to the exiting or restructuring of its non-accrual investments. But there should be a slightly positive impact to NAV per share as they were completely offset by the reversal of previous unrealized losses. This would imply that the company exited/sold these investments at a higher price (on average) than the fair value as of September 30, 2020. Also, it’s important to note that there will likely be a meaningful reduction in the amount of investments on non-accrual as well as additional income related to investments that were restructured during the quarter.

We believe that in future quarters, non-accrual levels may stabilize or could improve from these third quarter levels. Of the existing non-accruals we think, for the most part, they’re all pretty darn good businesses, that tier-point are operating in cities impacted by COVID. And through a combination of equity coming into those companies and potentially providing some concessions in the near term, they figured out how to operate. But, yes, I think there will be a path to recovery for most, if not all of them. So, I think it’s being reasonably optimistic on the existing non-accruals. But I think I’m optimistic too around the portfolio, because when you when you look at our non-accrual list, it’s pretty small list, right? And we’ve talked about the grade ones and twos being, I think in my mind, ring fenced at this point, and that we understand where the issues are. And we think that we have them under control, as I mentioned in the prepared remarks, so definitely a lot more optimistic than I was in April.”

Please note that ARCC has a very large portfolio with investments in 347 companies valued at almost $14.4 billion so there will always be a certain amount of non-accruals.

In terms of risk management, we remain focused on maintaining a highly diversified portfolio, which today includes 347 different companies with an average hold position at fair value of only 0.3%. We believe this diversity is a differentiator as it underscores the performance of any single investment and is unlikely to have a material impact on the aggregate performance of our company.”

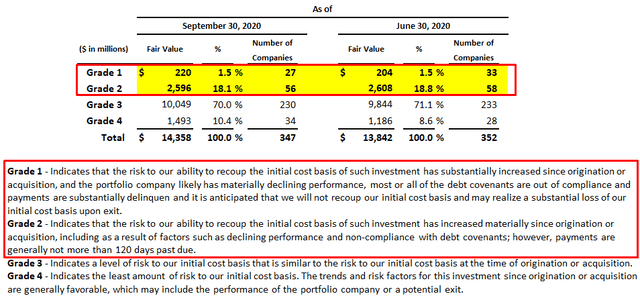

My primary concern is 18.1% (previously 18.8%) of the portfolio considered “Investment Grade 2” which indicates that the “risk to our ability to recoup the initial cost basis of such investment has increased materially since origination or acquisition, including as a result of factors such as declining performance and non-compliance with debt covenants, however, payments are generally not more than 120 days past due.” However, ARCC has higher quality management that takes a conservative approach to assess portfolio credit quality and there will likely be a material improvement during Q4 2020 for the reasons discussed earlier.

Regarding the health of our portfolio, our weighted average portfolio grade of 2.9 remain stable versus last quarter, and less than 5% of our portfolio companies changed grades. The ratio of upgrades to downgrades was greater than three to one, which we believe highlights the steady to improving cash flows of our portfolio companies that is followed with partial or complete reopening of many businesses. For the more COVID impacted names, which we largely see in our grade one and grade two names, we believe we have an informed view of their path to recovery but we do think this recovery will take time and likely be quite uneven with the ever-evolving COVID health crisis. Many of these companies are generally strong franchises with every reason to perform as they did pre-COVID and that they will recover during more certain economic times.”

Full BDC Reports

This information was previously made available to subscribers of Premium BDC Reports, along with:

- ARCC target prices and buying points

- ARCC risk profile, potential credit issues, and overall rankings

- ARCC dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

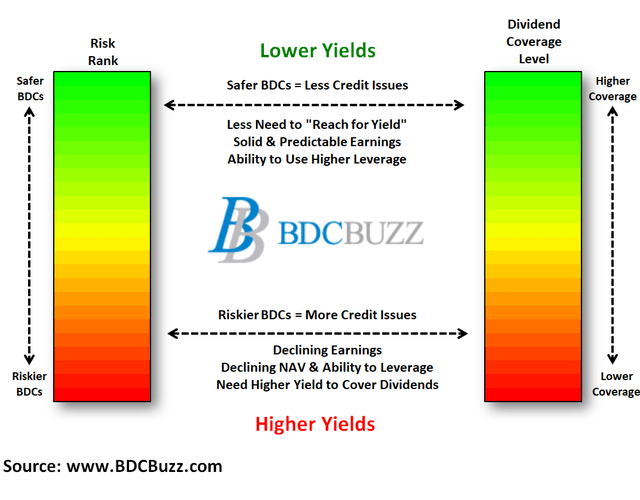

BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.

To be a successful BDC investor:

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Diversify your BDC portfolio with at least five companies. There are around 45 publicly traded BDCs; please be selective.