Monroe Capital (MRCC) Update

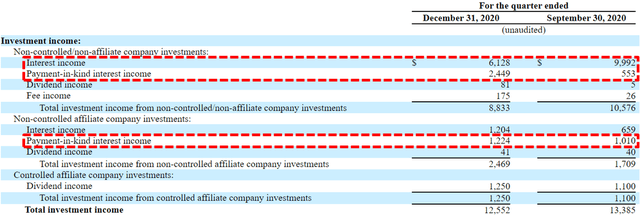

- During Q4 2020, there was a meaningful increase in the amount of PIK income from 12.8% to 33.4% of interest income.

- This is typically a sign that portfolio companies are not able to pay interest expense in cash and could imply potential credit issues over the coming quarters.

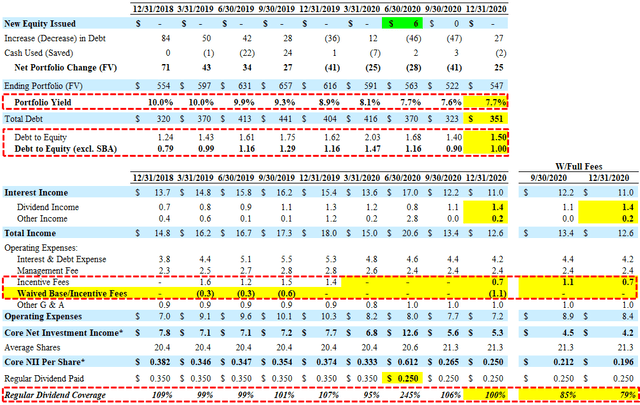

- Q4 2020 earnings would have been around $0.196 per share without the benefit of fee waivers covering 79% of the quarterly dividend which is down from 85% in Q3 2020.

- Dividend coverage should improve as the company benefits from a full quarter of interest income from new investments and reduced borrowing costs due to the redemption of its Baby Bond (MRCCL).

- MRCC is trading below NAV yielding 10.4% for a reason.

There are many factors to take into account when assessing dividend coverage for BDCs including portfolio credit quality, potential portfolio growth using leverage, fee structures including ‘total return hurdles’ taking into account capital losses, changes to portfolio yields, borrowing rates, the amount of non-recurring and non-cash income including payment-in-kind (“PIK”). During Q4 2020, there was a meaningful increase in the amount of PIK income from 12.8% to 33.4% of interest income. It should be noted that most BDCs have between 2% to 8% PIK income and I start to pay close attention once it is over ~5% of interest income.

This is typically a sign that portfolio companies are not able to pay interest expense in cash and could imply potential credit issues over the coming quarters. New investments during Q4 2020 were mostly near the end of the quarter so the company did not benefit from a full quarter of interest income for those investments. However, the total amount of PIK interest income increased 135% from $1.6 million in Q3 2020 to $3.7 million in Q4 2020 and could result in an eventual downgrade to ‘Level 3’ or ‘Level 4’ dividend coverage especially if there is another round of credit issues.

Management discussed this on the recent call and mentioned that $1 million was related to onetime activity which doesn’t account for the entire increase and there will still be a very large portion of PIK income:

“some of this is — I would consider about $1 million of this to be what I would consider non-reoccurring, sort of onetime PIK interest that we got in connection with some restructuring activities. So, we did like, for example, we did a restructuring that was very favorable on Familia, where we refinanced out a significant portion of our debt and got some PIK interest as a result and then took back considerable amount of upside equity as it applied to that deal. And so, that income is not likely to reoccur. And then, on HFZ and HFZ Member RB, we did a restructuring there as well. It was also favorable. The valuations are still very strong, and we took in some PIK interest that was kind of onetime, associated with it. There is some of that interest that will recur but some will not.”

It should be noted that we heard the same conversations with the management team at Medley Capital (MCC) just before the serious credit issues hit.

For Q4 2020, earnings would have been around $0.196 per share without the benefit of fee waivers covering 79% of the quarterly dividend which is down from 85% the previous quarter. Dividend coverage should improve in Q1 2021 as the company benefits from a full quarter of interest income from new investments. Also, on March 1, 2021, MRCC repaid $28.1 million in SBA debentures, and on January 25, 2021, the company issued $130 million of 4.75% notes due 2026 using the proceeds to redeem its 5.75% Baby Bond (MRCCL) on February 18, 2021.

Chief Executive Officer Theodore L. Koenig: “We had a very active late fourth quarter, redeploying a portion of the proceeds we received from recent repayment activity into current yielding assets which should positively contribute to earnings in future quarters. We are also very pleased with the January 25, 2021 issuance of $130.0 million in senior unsecured notes at an interest rate of 4.75% per annum with a maturity date of February 15, 2026 (the “2026 Notes”). The proceeds from the 2026 Notes were used to redeem all of the outstanding 5.75% 2023 Notes and repay a portion of the outstanding revolving credit facility. This refinancing lowered our debt financing costs which should positively impact our Adjusted Net Investment Income and earnings in future quarters.”

Non-accrual investments currently account for 4.1% of the total portfolio fair value and if completely written off would impact result in a NAV per share decrease of around 10%.

“As of December 31, 2020, we had 12 borrowers with loans or preferred equity securities on non-accrual status (BLST Operating Company, LLC, California Pizza Kitchen, Inc., Curion Holdings, LLC (“Curion”), Education Corporation of America (“ECA”), Incipio, LLC (“Incipio”) last out term loan and third lien tranches, Luxury Optical Holdings Co. (“LOH”), NECB Collections, LLC, Parterre Flooring & Surface Systems, LLC, SHI Holdings, Inc., The Worth Collection, Ltd. (“Worth”), Toojay’s Management, LLC and Valudor Products, LLC preferred equity), and these investments totaled $22.3 million in fair value, or 4.1% of our total investments at fair value.”

“We are pleased to report another quarter of strong financial results. During the fourth quarter, we reported another increase in our Net Asset Value and we again fully covered our dividend with Net Investment Income. We continue to believe the vast majority of our portfolio companies have strong long-term outlooks and we have seen recovery and stabilization in many of our portfolio companies that have been impacted by the COVID-19 pandemic. As market volatility resulting from the uncertainty related to the impacts of COVID-19 continued to decline during the fourth quarter, we saw spreads continue to tighten and valuations for portfolio companies without significant long-term COVID-19 impact continue to rebound, consistent with our experience in the prior two quarters.”

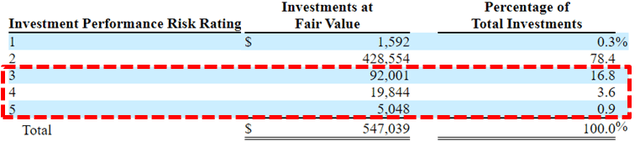

Grade 3 – Includes investments performing below expectations and indicates that the investment’s risk has increased somewhat since origination. The issuer may be out of compliance with debt covenants; however, scheduled loan payments are generally not past due.

Grade 4 – Includes an issuer performing materially below expectations and indicates that the issuer’s risk has increased materially since origination. In addition to the issuer being generally out of compliance with debt covenants, scheduled loan payments may be past due (but generally not more than six months past due).

Grade 5 – Indicates that the issuer is performing substantially below expectations and the investment risk has substantially increased since origination. Most or all of the debt covenants are out of compliance or payments are substantially delinquent. Investments graded 5 are not anticipated to be repaid in full.

Full BDC Reports

This information was previously made available to subscribers of Premium BDC Reports, along with:

- MRCC target prices and buying points

- MRCC risk profile, potential credit issues, and overall rankings

- MRCC dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

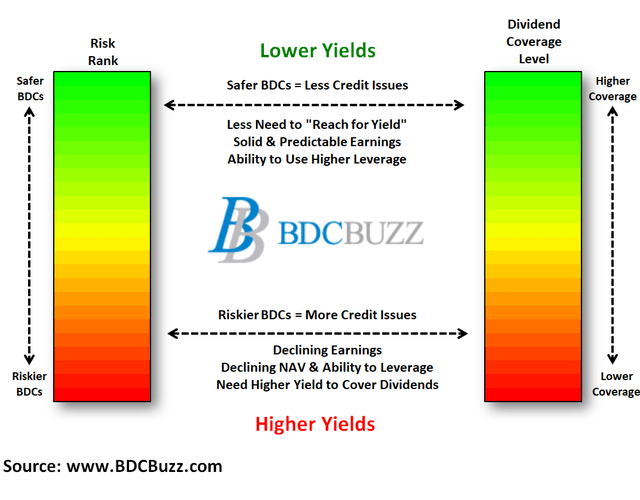

BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.

To be a successful BDC investor:

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Diversify your BDC portfolio with at least five companies. There are around 45 publicly traded BDCs; please be selective.