The following information was previously provided to subscribers of Premium BDC Reports along with:

- ORCC target prices/buying points

- ORCC risk profile, potential credit issues, and overall rankings

- ORCC dividend coverage projections and worst-case scenarios

Summary

- ORCC is slowly increasing leverage to fully cover the dividend later this year. Management provided guidance for a much stronger Q2 2021 taken into account with the updated projections.

- There will likely be a meaningful increase in income related to prepayment fees, accelerated OID, a full quarter of benefit from Q1 investments, increased leverage, and portfolio growth.

- These repayments will likely be mostly offset by new investments including the recently announced $2.3 billion loan to finance Thoma Bravo’s acquisition of online trading services provider Calypso Technology.

- ORCC is for risk-averse investors as the portfolio is mostly larger middle market companies that would likely outperform an extended recession environment. Credit quality remains solid with no new non-accruals that remain at 0.2% of fair value.

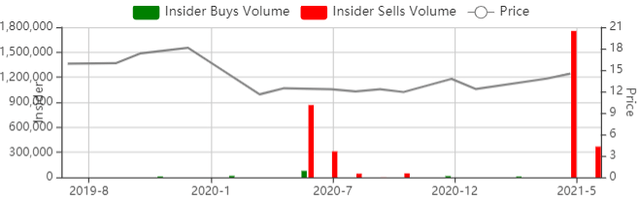

- As discussed in previous reports/updates there has been some technical selling pressure related to Regents that continued through April/May 2021.

This update discusses Owl Rock Capital Corporation (ORCC) which remains one of the best-priced BDCs especially for lower-risk investors that do not mind lower yields.

ORCC is for risk-averse investors as the portfolio is mostly larger middle market companies that would likely outperform in an extended recession environment. Also, the company has relatively low leverage with ample growth capital available for increased earnings over the coming quarters.

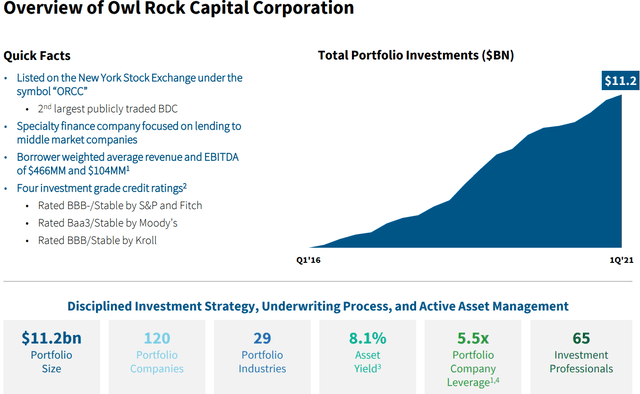

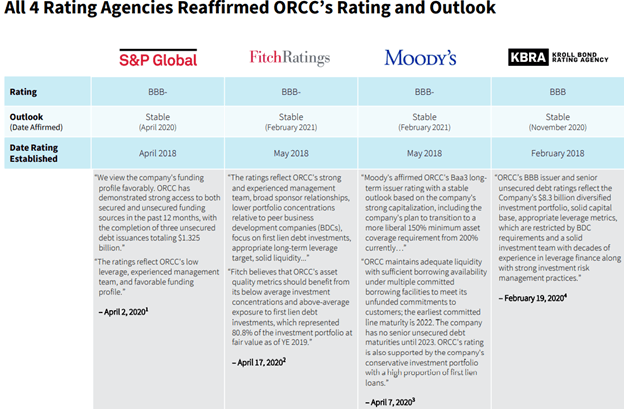

ORCC is the third-largest publicly traded BDC (much larger than MAIN, PSEC, GBDC, GSBD, NMFC, and AINV) with investments in 120 portfolio companies valued at over $11 billion that are mostly first-lien secured debt positions. ORCC is one of the few BDCs rated by all of the major credit agencies.

ORCC 10% Owner Sales

As discussed in previous reports/updates and the public article “Technical Pressure Driving 12% Yield For Owl Rock” (from July 2020), the Regents of the University of California (ORCC’s largest shareholder) was previously selling its pre-IPO shares each time the stock was above ~$12.50 but had not sold shares since September 2020. However, there have been additional sales and could be the start of another round of selling. I would suggest holding off on purchases for now. There is a chance that the stock could dip below $14.00 (again) and I will update subscribers on additional sales and provide updates as needed.

ORCC Dividend Coverage Update

ORCC remains a ‘Level 2’ dividend coverage BDC implying that the regular quarterly dividend is stable. The company was not expected to fully cover its Q1 2021 dividend and was discussed on the previous call:

“We continue to make good progress toward earning our dividend and are on track to achieve our target leverage by the second half of 2021. We expect to continue to pay our regular dividend of $0.31 per share and would anticipate returning a modest amount of capital in the interim. ”

ORCC’s longer-term (“LT”) target price takes into account improved dividend over the coming quarters mostly due to:

- Increased use of leverage to grow the overall portfolio

- Prepayments fees and accelerate OID

- Higher portfolio yield from rotating into higher yield assets

- Continued lower cost of borrowings

ORCC remains underleveraged and is targeting a debt-to-equity ratio up to 1.25 (currently 0.93 net of cash) giving the company plenty of growth capital.

“Thinking ahead to the rest of this year, we expect interest income to continue to increase each quarter over the coming quarters, as we modestly increase our leverage within our target range. We’ve made steady progress to get to the low end of our targeted range of 0.90 to 1.00 in a quarter and expect to modestly increase our leverage within that range in the coming quarters.”

“As we expected first quarter NII was temporarily down. Our originations were largely first lien investments, which once again were weighted toward the end of the quarter and as a result, the net one penny per share of growth in NII is not reflective of the full benefit of Q1 originations. In addition, dividend income was lower this quarter, which also impacted NII by approximately one penny per share. However, we expect that we will make meaningful progress in the second quarter towards earning our dividends. We believe we are still on track to fully cover our dividend from NII in the second half of the year. We don’t typically provide forward guidance, but I can say that sitting here today as we are expecting a very active second quarter and originations in excess of the first quarter and more in line with the fourth quarter.”

Management is expecting a much stronger Q2 2021 partially due to higher prepayment-related income which has been taken into account with the updated financial projections and was discussed on the recent earnings call:

“So we only had about $250 million of actual repayments. And we expect that number to go up materially in the second quarter. That obviously is very impactful for earnings. Because as we get through repayments, we are able to recognize the OID that remains on those investments and oftentimes, pre-payment penalties. So we’re calling attention to that because it generates earnings. For the second quarter, we also have visibility on increased pre-payments, which will generate additional fees from accelerated OID and call protection. Based on the net effect of the pipeline borrowing something unexpected, we believe we will continue to modestly increase our leverage level as well as improve earnings in second quarter. As a result, we expect Q2 earnings to grow and then make solid progress towards covering our $0.31 per share dividend, which we ultimately expect to occur in the second half of this year. We do expect repayments to pick up later this year based on the continued seasoning of our portfolio. I would also note that we had some higher yielding repayments early on in the quarter.”

These repayments will likely be mostly offset by new investments including the recently announced $2.3 billion loan to finance Thoma Bravo’s acquisition of online trading services provider Calypso Technology:

“We are pleased that we continue to be successful in winning the deals that we want to win. In names in situations where we have high conviction around the asset and the sponsor are able to demonstrate the value of our platform and often take a sole or lead position in these deals. As a great example of this, it was recently announced that Owl Rock is leading the $2.3 billion unitranche loan to finance Thoma Bravo’s acquisition of Calypso, which is expected to close later this year. We believe this will be the largest unitranche facility ever we done in the U.S. and is a reflection of our ability to provide attractive sizeable financing commitments for top tier investment opportunities. It also highlights our expertise in the software space. Calypso reflects the continued growth of the private credit space as increasingly larger borrowers are choosing direct lending solutions over the syndicated market. Given our large capital base, Owl Rock is very well positioned for this trend. We’re very excited about the continued growth of the platform and the sourcing opportunities that we expect to generate as a result of the Blue Owl transaction closing. We look forward to discussing the Blue Owl platform in more detail in the quarters to come.”

Similar to other BDCs, ORCC has been improving or at least maintaining its net interest margin which is the difference between the yield on investments in the portfolio and the rate of borrowings. During the most recently reported quarter, ORCC maintained its portfolio yield but is expecting “modestly higher” in Q2 2021:

“The visibility we have on second quarter, I would expect spreads to be a bit wider than we’d gotten the first quarter. But I think we’re continuing to find investments that have a spread consistent with today’s weighted average spread in our portfolio, in some cases, higher, some cases slightly lower. But our visibility in the second quarter I would say it’s modestly higher.”

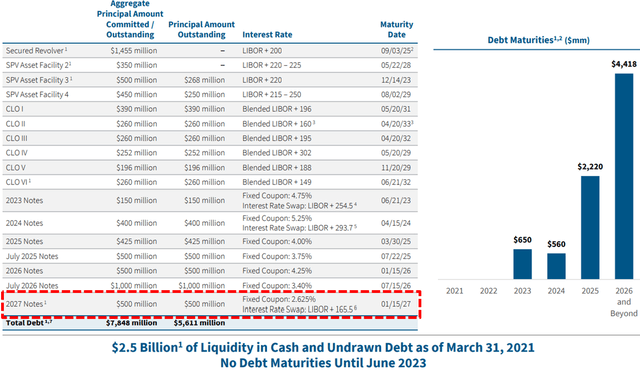

ORCC’s average borrowing rate has declined from 4.6% to 3.2% over the last five quarters due to continued issuances of notes and CLOs at lower rates including another $398 million on May 5, 2021. On April 26, 2021, the company issues $500 million of 2.625% notes due 2027.

“We continue to focus on optimizing our funding costs. In that regard, we had two notable transactions we did that helped further us in reducing costs on the right side of our balance sheet. We priced our sixth CLO this one for $260 million of incremental financing at a blended spread of 149 basis points a great print and very cost efficient for us. And we issued our seventh bonds, this one for $500 million of incremental financing at a fixed coupon of 2.158% or tightest print ever.”

As of March 31, 2021, ORCC had around $2.5 billion of liquidity consisting of $244 million of cash and almost $1.24 billion of undrawn debt capacity (including upsizes).

Full BDC Reports

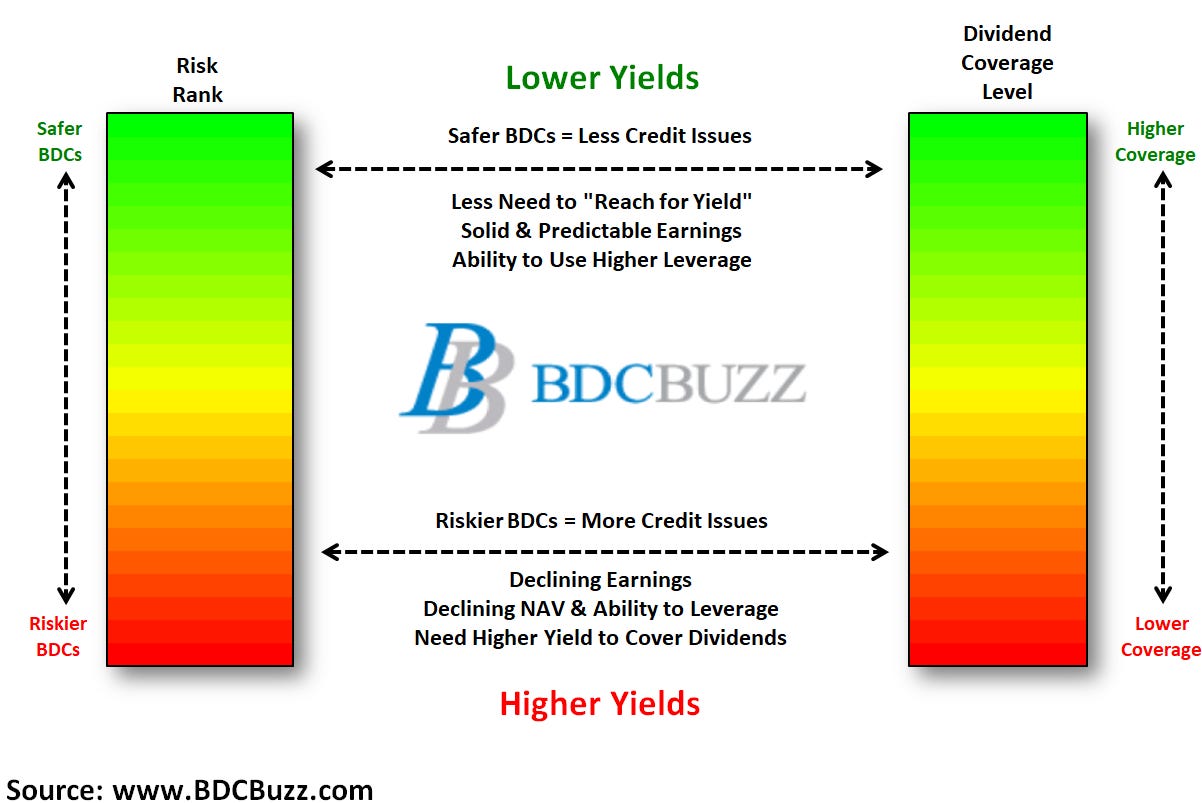

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.