The following information was previously provided to subscribers of Premium BDC Reports along with:

- TSLX target prices/buying points

- TSLX risk profile, potential credit issues, and overall rankings

- TSLX dividend coverage projections and worst-case scenarios

Summary

- I have updated the TSLX projections (slightly higher supplemental dividends) and pricing (no change) to take into account recent guidance from management.

- “I feel pretty confident that we’re going to grow the book in the near term. I feel more bullish today than I have historically”.

- Q1 2021 was another strong quarter for TSLX between its base and best case projections covering its regular dividend by 130% and paying another supplemental of $0.05 per share.

- There was an additional $14.6 million or almost $0.21 per share of net realized gains during Q1 2021 to support additional supplemental dividends.

- As expected NAV per share declined due to previous supplementals/specials. However, using adjusted NAV there was an increase of 3.5% due to accretive offering, overearning the dividend, and portfolio markups.

- Total non-accruals declined to 0.02% of the portfolio fair value (previously 0.90%) due to its first-lien position in American Achievement added back to accrual status.

- TSLX has higher quality management maintaining margins, reducing leverage, and 89% of the portfolio is considered ‘Performance Rating 1’

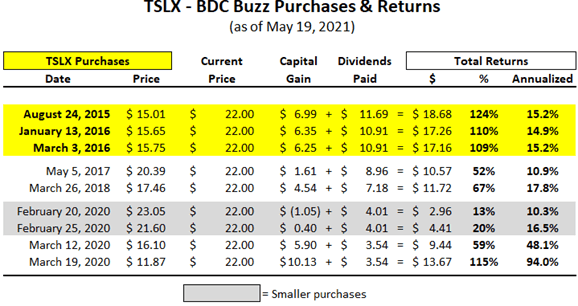

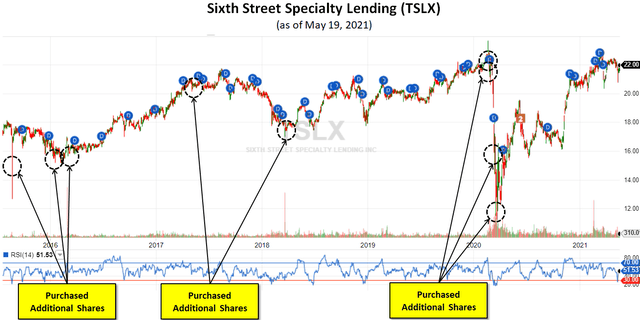

- Over the last 5 to 6 years, TSLX has provided me with annualized returns of 15% and likely headed higher as the company continues to pay special/supplemental dividends.

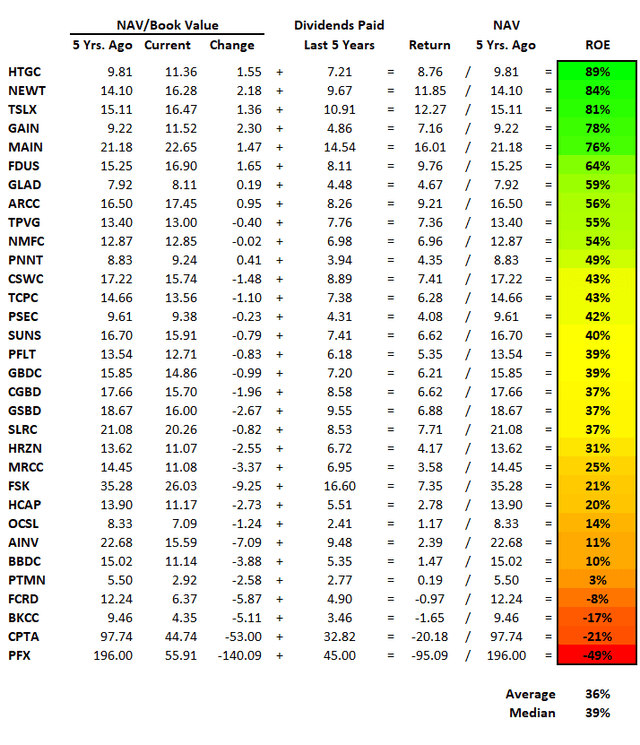

- Also included is a comparison table showing returns for each BDC over the last five years taking into account changes in book value/NAV and dividends paid.

- One of the many reasons that I consider TSLX to have higher quality management is the focus on ROE with each decision including equity offering, debt issuances, the amount of distributions paid, excise tax.

Over the last 5 to 6 years, TSLX has provided me with annualized returns of 15% and likely headed higher as the company continues to pay special/supplemental dividends. The “Annualized” return shown does not use a simple average but shows the actual compounding of annual returns. This is the true return each year. Please disregard the annualized total returns for 2020 purchases as the time frame is not long enough to accurately reflect.

Historical BDC Returns

The following table shows the returns for each BDC over the last five years taking into account changes in book value or net asset value (“NAV”) and dividends paid. It is important to note that when BDCs pay out large special/supplemental dividends it directly impacts NAV which is why both are taken into account. Also, some BDCs use conservative or aggressive valuations and their current NAV could be understated or overstated. One of the many reasons that I consider TSLX to have higher quality management is the focus on return on equity (“ROE”) with each decision including equity offering, debt issuances, the amount of distributions paid, excise tax:

“As we look ahead to the year, we continue to target a return on equity of 11.5% to 12%, corresponding to a range of $1.82 to $1.90 for full year 2021 adjusted net investment income per share. We did a small equity issuance sized at less than 6% of our pro forma market cap with net proceeds approximating the size of our special dividend payment. What we did essentially was swap out capital that had excise tax associated with it and replaced it with new capital without the burden of excise tax. This allowed us to create NAV and ROE accretion for our shareholders while remaining leverage neutral.

Return on equity (“ROE”) for Q1 2021 was 13.3% and 22.1% on a net investment income and a net income basis, respectively.

TSLX Upcoming Supplemental Dividends

On May 4, 2021, the company reaffirmed its regular quarterly dividend of $0.41 plus another supplemental dividend of $0.06 per share which was between the previous base and best-case projections of $0.03 and $0.08, respectively. Previously the company paid a special cash dividend of $1.25per share and a supplemental dividend of $0.05 per share.

Over the last five years, TSLX has increased the amount of supplemental dividends paid:

When calculating supplemental dividends, management takes into account a “NAV constraint test” to preserve NAV per share. This is one of the reasons that management prefers not to pay large supplemental dividend payments even though the amount of undistributed/spillover income continues to grow. However, management also likes to avoid paying excessive amounts of excise tax by “cleaning out” the spillover as it “creates a drag on earnings” which is why the company paid a total of $1.30 per share in supplementals during Q1 2021.

During Q1 2021, there was an additional $14.6 million or almost $0.21 per share of net realized gains (mostly due to the sale of its equity position in Capsule Technologies to Philips) to support additional supplemental dividends.

“The realization of our small equity investment in Capsule Technologies upon a sale to Philips drove the bulk of our realized gains this quarter.”

TSLX still has around $1.02 per share of undistributed/spillover income as well as its Series A preferred shares of Validity, Inc. valued at $8.5 million over cost and will likely result in upcoming realized gains of $0.12 per share to support additional supplemental dividends.

Full BDC Reports

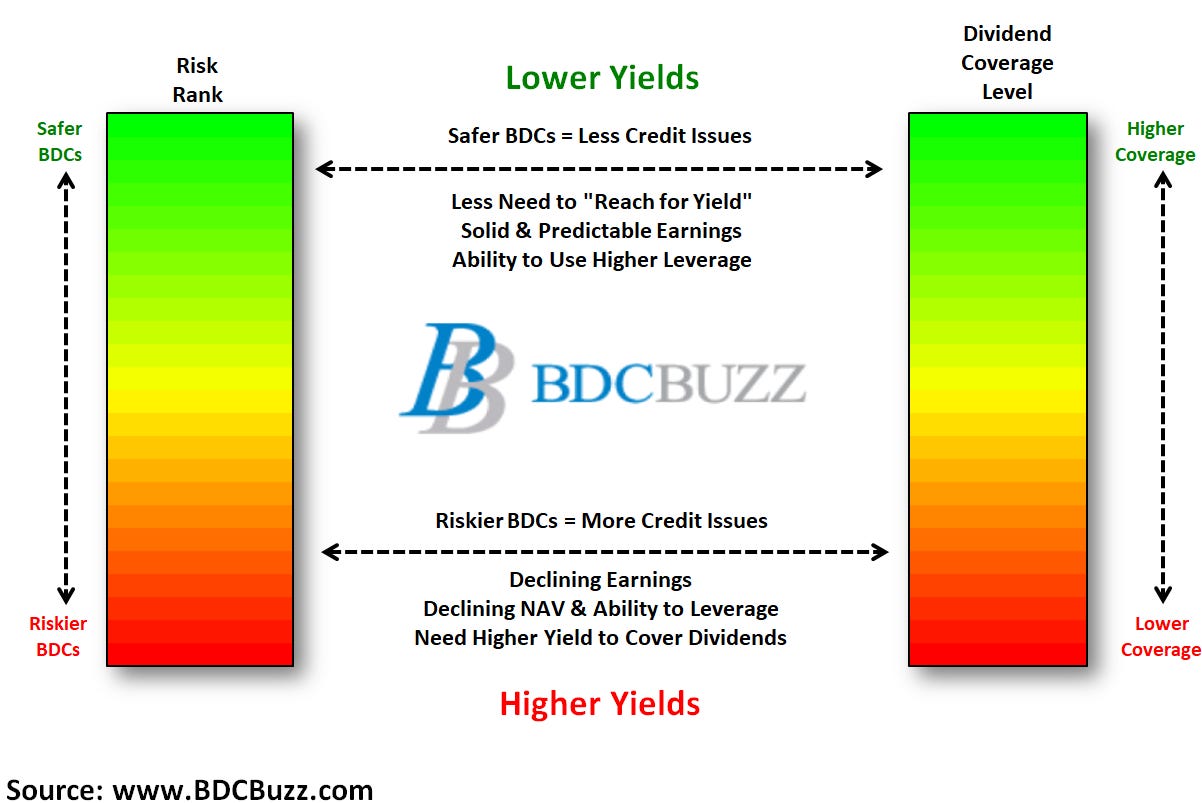

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.