The following information was previously provided to subscribers of Premium BDC Reports along with:

- HTGC target prices/buying points

- HTGC risk profile, potential credit issues, and overall rankings

- HTGC dividend coverage projections and worst-case scenarios

HTGC Distribution Update

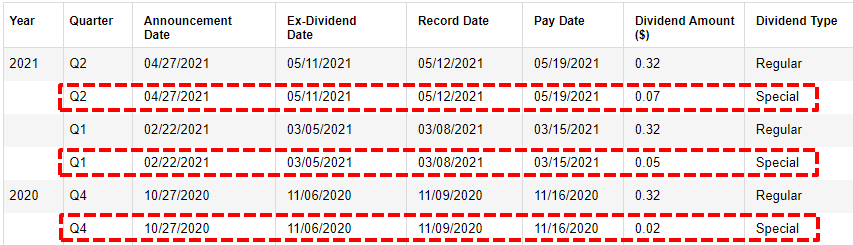

As predicted in previous updates, HTGC declared additional supplemental cash distributions during 2021 due to the “record level of spillover at $0.94” and “the trajectory of the business for the course of 2021”. HTGC will be distributing $0.28 per share (more than I was expecting) evenly over the next four quarters starting with $0.07 per share for the first quarter of 2021 paid in May 2021.

HTGC remains a higher dividend coverage BDC with the potential for supplemental dividends partially due to its internally-managed cost structure and equity investments historically providing realized gains and supporting supplemental dividends:

HTGC maintains a “variable distribution policy” with the objective of distributing four quarterly distributions in an amount that approximates 90% to 100% of the company’s taxable quarterly income or potential annual income. In addition, the company pays additional supplemental distributions to distribute approximately all its annual taxable income in the year it was earned, or it can elect to maintain the option to spill over the excess taxable income into the coming year for future distribution payments.

“We have a variable dividend policy, so it’s something that the Board evaluates on a quarterly basis, and we don’t just look short-term, we look long-term when we’re making those decisions. We’ve been very clear in terms of our public guidance on the last several calls that we see absolutely no risk to that $0.32 base distribution, and we would reiterate that guidance on this call now. If you think about what we’ve been able to do in terms of the special distributions, we’ve been able to deliver to our shareholders a supplemental or a special distribution in six of the last seven quarters on top of the $0.32 base distribution. And obviously, subject to market conditions, I think one of the things that we’re going to look at near-term here is trying to find a way to provide a little bit more consistency and continuity to those supplemental distributions. “

Hercules Adviser LLC Update

On March 25, 2021, HTGC announced that Hercules Adviser LLC, a wholly-owned subsidiary of HTGC, had successfully closed its inaugural institutional private credit fund.

Scott Bluestein, CEO and CIO of HTGC: “We are very pleased to announce that Hercules Adviser has successfully raised and closed its first institutional private credit fund. This new private credit fund will allow us to continue to expand and broaden our investment platform while at the same time serving the growing needs of the venture and growth stage companies that we seek to partner with.”

Management has mentioned that this will allow the company to “expand and broaden” its investment platform allowing HTGC to access to “a lot of deals that we’re now able to do at the BDC level”. However, as the fund ramps up it will likely be “taking some investments away” over the short-term and sharing expenses reducing HTGC’s operating costs as well as eventually paying distributions to HTGC as “100% of the benefit from the RIA activities accrues and accretes to the shareholders of the public BDC”.

“After establishing Hercules Advisor as a wholly own registered investment advisor in 2020, we are very pleased to have raised and closed our first institutional private credit fund. Having this first fund and potentially future funds gives us the opportunity to expand and diversify our investment platform while enhancing our level of service and capabilities to our current and future venture growth stage companies. While we anticipate that it will take time to ramp up our activities under our RIA, we do expect that over the short term, Hercules Capital will benefit from being able to share certain expenses with Hercules Advisor and having a more diverse platform for the funding of new investments. Longer term and subject to the ultimate performance and size of the funds managed by Hercules Advisor, we expect Hercules Capital to potentially benefit from distributions from the advisor as that business ramps up.”

“On an initial basis as it ramps up potentially taking some investments away with the two caveats that we mentioned before. Number one, there are a lot of deals that we’re now able to do at the BDC level that we probably could not otherwise have done. If we didn’t have the private vehicle to be investing alongside us. And then no two, this is not an externally managed private fund. This is a private fund that’s managed by a wholly owned RIA. So 100% of the benefit from the RIA activities accrues and accretes to the shareholders of the public BDC. During Q1 we successfully closed our first private fund, and as a result, we allocated a portion of certain commitments and fundings to the initial private fund. This also allowed us to allocate certain expenses to Hercules Advisor, our RIA managing the private fund during the quarter.”

HTGC March 31, 2021, Results

Hercules Capital (HTGC) reported just above its base case projections for Q1 2021 not fully covering its dividend (as expected). However, the company had around $0.94 of undistributed income for temporary shortfalls and has covered its dividend by an average of 110% over the last 8 quarters supporting the previously announced supplemental dividends. Also, as mentioned in the previous report, there were higher expenses related to payroll tax in Q1:

“SG&A expenses increased to $17.6 million from $16 million in the prior quarter. The increase was driven by higher compensation expenses related to the increase in fundings and first quarter payroll taxes which normally run higher in the first quarter. Net of truck costs recharged to the RIA, the SG&A expenses were $16.7 million. For the second quarter, we expect SG&A expenses of $16 million to $17 million slightly below the prior quarter, as Q1 always has higher employer payroll taxes. We expect our second quarter borrowing costs to decrease modestly.”

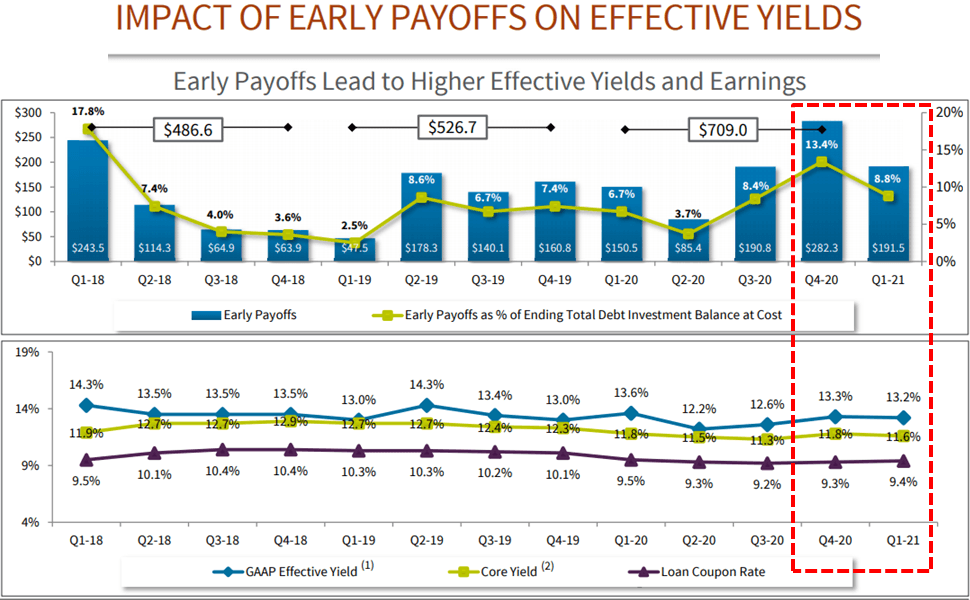

The effective yield was 13.2% during Q1 2021, down slightly compared to 13.3% for Q4 2020 due to lower early loan repayments (discussed next). Effective yields generally include the effects of fees and income accelerations attributed to early loan repayments and other one-time events. HTGC’s ‘Core Yield’ decreased from 11.8% to 11.6% and over 98% of its debt portfolio is now at its contractual interest rate floor.

“The decline in both total investment income and net investment income was consistent with our guidance, and due to the lower debt portfolio balance attributable to the record Q4 payoffs, and lower fee income as a result of a lower level of prepayments during the first quarter. Core yield, a non-GAAP measure, was 11.6% during Q1 2021, within the Company’s expected range of 11.0% to 12.0%, and decreased slightly compared to 11.8% in Q4 2020. Hercules defines core yield as yields that generally exclude any benefit from income related to early repayments attributed to the acceleration of unamortized income and prepayment fees and includes income from expired commitments. During Q1, we continue to see strength in terms of portfolio company exits, and portfolio company liquidity events. This combined with continued very strong performance across our portfolio, again drove high levels of early pay-offs. Early loan repayments were at the high end of our guidance of $150 million to $200 million at over $191 million, but decreased from $282 million in Q4.”

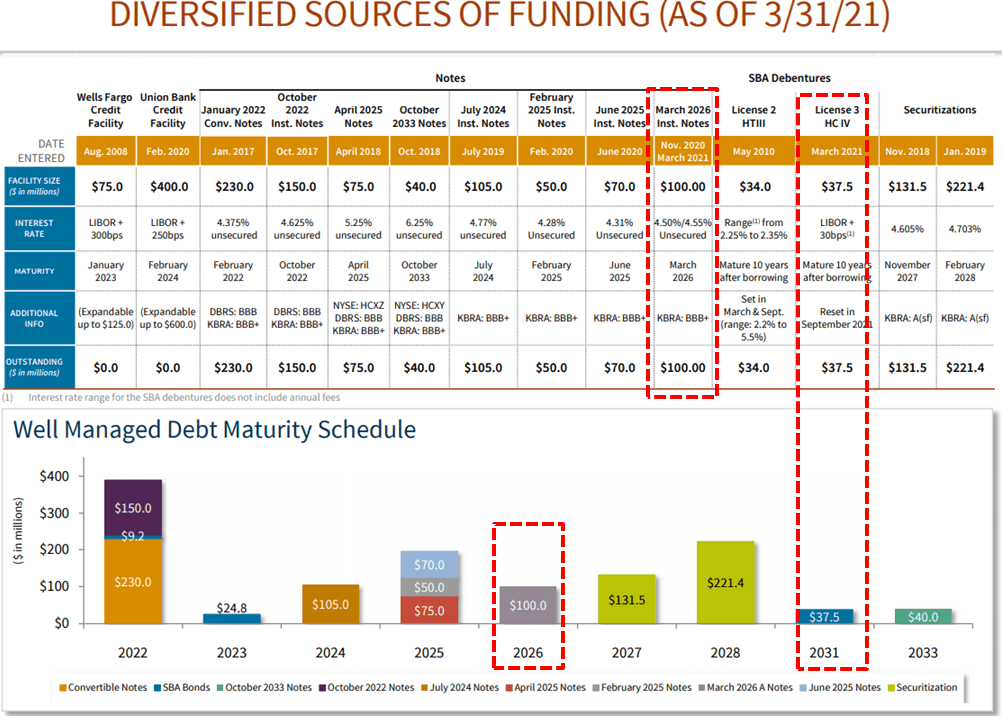

HTGC ended Q1 2021 with $550 million of available liquidity, including $75 million in unrestricted cash and cash equivalents, and $475 million in available credit facilities. HTGC had pending commitments of $153 million as of April 27, 2021, and since the close of Q1 2021, the company has closed new debt and equity commitments of $135 million and funded $25 million.

“For Q2, we again expect prepayments to be between $150 million and $200 million, although this could change materially as we progress in the quarter.”

In March 2021, the company issued an additional $50 million 4.50% Notes due March 2026 and $50 million 4.55% Notes due March 2026.

“Our leverage includes the March issuance of $50 million five-year notes in a private placement with a fixed coupon of 4.55%. This was the second tranche of the arrangement announced in November 2020, totaling up $100 million in private placement financing.

In October 2020, the company announced that it had received approval for its third SBA license. It should be noted that this was quicker than expected and will provide an additional $175 million of fixed-rate borrowings at very attractive 10-year rates.

“In addition, we have started to utilize our third SBA license drawing down $37.5 million of debentures and has attractive annual interest rate of 0.77%.”

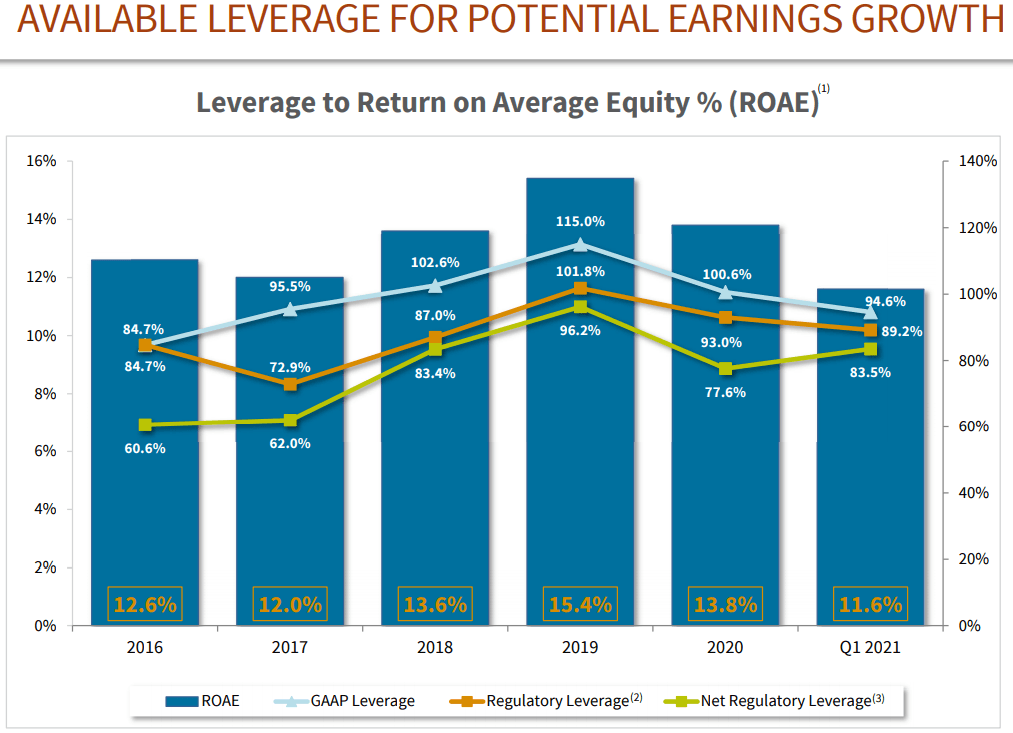

During Q1 2021, the company did not issue additional shares through its At-the-Market (“ATM”) Equity Distribution Agreement. HTGC continues to target a regulatory debt-to-equity ratio between 0.95 to 1.25 and will likely use the ATM program to maintain leverage while growing the portfolio. As of March 31, 2021, approximately 16.2 million shares remain available for issuance and sale

“Moving on to discuss leverage. Our GAAP and regulatory leverage was 94.6% and 89.2%, respectively, which decreased compared to the prior quarter due to the partial repayment of the two securitizations, which are now in runoff. Netting out leverage with the cash on the balance sheet, our GAAP and regulatory leverage was 88.9% and 83.5% respectively, putting us in a very strong position heading into the next quarter.”

Full BDC Reports

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.