The following information was previously provided to subscribers of Premium BDC Reports along with:

- PNNT target prices/buying points

- PNNT risk profile, potential credit issues, and overall rankings

- PNNT dividend coverage projections and worst-case scenarios

Summary

- PNNT is currently considered a ‘Hold’ but has started to pull back and we thought that this might be a good time to provide a quick update.

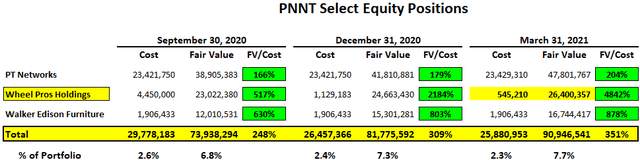

- I am expecting $26 million or $0.39 per share of realized gains during calendar Q2 2021 related to the exit of its equity position in Wheel Pros.

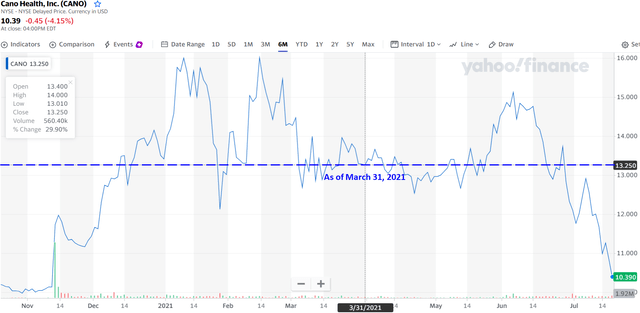

- On June 3, 2021, its portfolio company Cano Health (CANO) closed its combination with JWS with PNNT’s shares publicly tradable in December 2021.

- However, CANO has declined by around 9% through June 30, 2021, and down another 14% through July 19, 2021, which will drive unrealized losses likely offset by other investments.

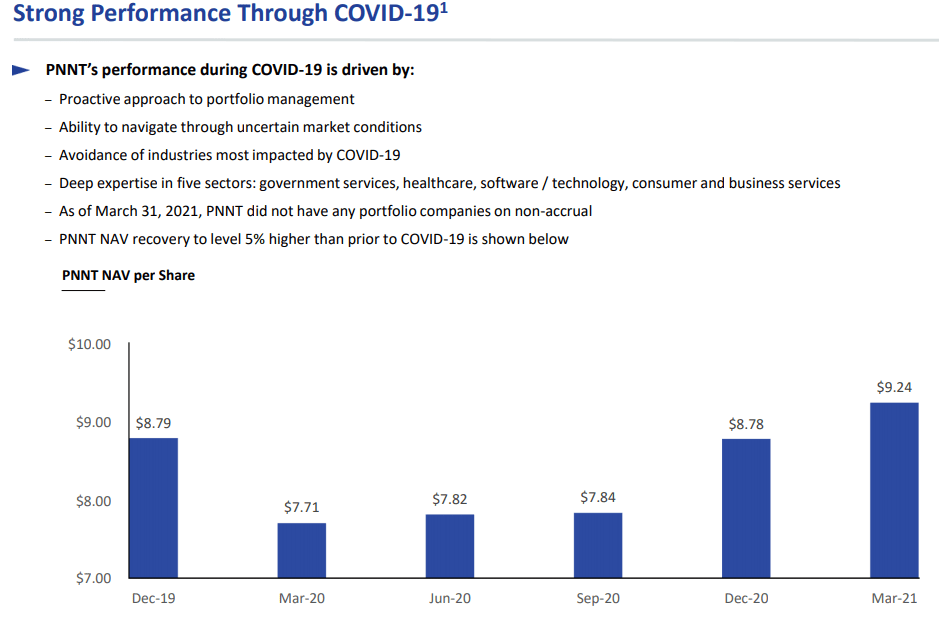

- PNNT previously reported results last month between its base and best case projections with ‘core NII’ of $0.133 per share and 111% coverage of the quarterly dividend.

- As expected its NAV per share grew by another 5.2% mostly due to equity investments driving PNNT’s leverage (debt-to-equity) well below historical levels (0.75 net of SBA debentures).

- The company has started exiting some of its non-income-producing assets which will likely be reinvested into “yield generating debt instruments”.

- There was a slight decline in income from its recently formed joint-venture PSLF but is expected to grow over the coming quarters.

PNNT Dividend, NAV Per Share & Management Fees Update

PNNT continues to improve dividend coverage partially due to its previous and upcoming increases in its net asset value (“NAV”) per share combined with its 7% hurdle, the eventual selling and reinvesting of many of its equity positions, and its new joint-venture PennantPark Senior Loan Fund (“PSLF”) with Pantheon Ventures that will likely improve its portfolio yield and risk-adjusted returns.

“With regard to income generation, we have the opportunity to rotate out of our out of our equity investments over time and into yield instruments. In addition, we have the ability to grow the P&L balance sheet, and that of our PSLF JV with Pantheon, which should also generate additional income for the company. Our goal is to fully extend the existing JV and we have a little bit of room to go there. And then you know, subject to pantheons approval of course, in partnership, we be totally open to expanding that JV optimizing it if you look at what’s going on over PFLT our sister company with Kemper. We’ve grown that JV, we’re growing more, we’ve optimized the financing by doing a CLO transaction to get a higher ROI.”

“We have several portfolio companies in which our equity investments have materially appreciated in value as they’re benefiting from the recovery. This is solidifying and bolstering our NAV. As part of our business model, alongside the debt investments we make we selectively choose to co invest in the equity side by side with a financial sponsor. Our returns on these equity investments have been excellent over time. From inception through March, 31, our $226 million of equity investments have generated an IRR of 28% and a multiple on invested capital of 2.9 times. We are pleased that we have significant equity investments in five of these companies, which can substantially move the needle of our NAV. I would like to highlight those five companies, they are Cano, Wheel Pros, Walker Edison, PT Network, and JF Petroleum. As of March 31, PNNT owned equity securities, with a cost and fair market value of $40 million and $43 million, respectively. These companies are gaining financial moment in this environment, and our NAV should be solidified to bolster from these substantial equity investments as their momentum continues. Additionally, we are pleased with a liquidity event that Wheel Pros and Walker Edison, which are a solid start to our equity rotation program.”

I am expecting almost $26 million or $0.39 per share of realized gains during calendar Q2 2021 related to the exit of its equity position in Wheel Pros as discussed on the recent call:

“Wheel Pros is the largest national distributor of aftermarket custom wheels. Our equity position has a cost of $500,000 and a fair market value of $26.4 million as of March 31. At the end of March, the company announced a strategic transaction with the new sponsor investment vehicle, which will result in the full exit of our investment in Wheel Pros. The transaction is expected to close in the next couple of weeks. This will resolve in our equity investment in Wheel Pros, generating an IRR of 104% and a multiple on invested capital of seven times.”

On June 3, 2021, its portfolio company Cano Health, Inc. (CANO) closed its business combination with Jaws Acquisition Corp (“JWS”). As shown in the following table, this investment is marked well above cost and could result in $70.4 million or $1.05 per share of realized gains if sold at the previous fair value.

However, the stock price for CANO has declined by around 9% from March 31, 2021, through June 30, 2021, and down another 14% through July 19, 2021, which will drive unrealized losses likely offset by appreciation from other portfolio equity positions.

Also, there is a six-month lock-up on its shares with 20% of the exit proceeds paid to the financial sponsor and a 6% illiquidity discount applied to the valuation for the March 31, 2021, results. Management discussed Cano Health on the recent call:

“Cano health is a national leader in primary health care who is leading the way in transforming healthcare to provide high quality care at a reasonable cost to a large population. Our equity position as a cost and fair market value on March 31, of $2.5 million and $73 million respectively. We believe that there’s a massive market opportunity for Canada to grow in the years ahead with a Medicare Advantage program and merger with Jaws acquisition is scheduled to close in June. At that time, we will receive another $6.7 million in cash and 6,629,953 shares of Cano health and limited partnership controlled by a financial sponsor where the sponsor will earn 20% of the exit proceeds, the shares will be locked up for six months. From a valuation perspective due to the lockup, the independent valuation firm valued the position with a 6% illiquidity discount to traded value on March 31.”

There is a good chance that PNNT will be selling its equity positions in PT Networks, and Walker Edison Furniture over the next 12 to 18 months. These investments along with the previously discussed Wheels Pros were marked up again and now account for almost $91 million or 7.7% of the portfolio with the proceeds to be reinvested into income-producing assets. As shown in the table below, these investments are marked well above cost and will likely result in a total of $65 million or $0.97 per share of realized gains.

Management discussed these investments on the recent call mentioning additional NAV upside as well as increased earning potential through reinvestment:

“As of March 31, equity represented approximately 36% of the portfolio. Over 60% of this 36% has come from appreciation over the last 12 months driven by many of the companies previously mentioned. Our long term goal continues to target that percentage down to about 10% of the portfolio. As we monetize the equity portfolio, we’re looking forward to investing the cash into yielding debt in investments to increase Net investment income.”

Q. “The long term goal, to get equity, obviously, non equity down to 10%. What’s a realistic timeframe to achieve that goal? I mean, there’s that three years out, is it going to take longer than and it’s certainly not going to happen in 12 months?”

A. “Certainly not a year and, and hopefully not three years. You know, you’re right. I mean, I don’t know if that’s a tight enough band for you. Some of these we control some of these we don’t control we control RAM, to some extent, but we don’t control where the oil and guess M&Amarket is, when the oil and gas M&Amarket starts to heat up. We will meet in a hopefully more action RAM, we do control PT, pivot. And that that, you know, is more in our control in that market strong. So that may be you know, sooner rather than later, does that mean 12 months or 18 months, it’s kind of something in that zone. We don’t control Cano. We don’t control Walker Edison, etcetera. So, you know Cano going through the dispatch process, hopefully in the next month or six weeks. We said well control it after it does the [indiscernible] back but at least it’s more and more on its way to a liquidity event. That’ll be a big milestone. So yes, a year to three years just as a general you know, if you really want to say let’s run the table, get it down to 10%. I think that’s probably right.”

“Walker Edison is a leading e-commerce platform focused on selling furniture exclusively online through top ecommerce companies, our equity position as a cost of 1.9 million and a fair market value of $16.7 million as of March 31. Shortly after quarter and the company executed a refinancing and dividend recap, which resulted in shareholders receiving two times their costs while maintaining the same ownership in the company. This resulted in PNNT receiving a $3.8 million cash payment on his equity position.”

Q. “On Walker Edison you mentioned that $3.8 million cash payment, what should we expect, say half of that to be recognized as dividends and maybe the other half to be returned to capital and take your cost basis down to zero or with the whole thing, the dividend?”

A. “It’ll be based on what we could tell it’ll be the first obviously the first part of its return on capital. And the second part of it looks like it’s can be counted as a capital gain.”

“PT Network is the leading physical and occupational therapy provider in the Mid-Atlantic states. Our equity investment in PT came through a restructuring which came about after the company made several operational mistakes. We’ve always had a positive view of the industry and the outlook to the industry tailwinds and demographics, which results in comparable companies trading at EBITDA multiples of 12 to 15 times. Under our ownership, we brought in an excellent management team who corrected those operational mistakes and has shepherded the company well through COVID. Our equity position as a cost of $23 million, and the fair value of $48 million as of March 31.”

My primary concerns for PNNT are mostly related to the recent increase in payment-in-kind (“PIK”) interest income from 13.0% to 20.3% of total income over the last two quarters and the commodity-related exposure combined lack of a “total return hurdle” incentive fee structure to protect shareholders from capital losses. However, management consistently “does the right thing” including continued fee waivers and previously reducing its base management (from 2.00% to 1.75%) and incentive fees (from 20.0% to 17.5%).

PNNT March 31, 2021, Quick Update

PennantPark Investment (PNNT) reported between its base and best case projections with ‘core NII’ of $0.133 per share and 111% coverage of the quarterly dividend adjusting for $0.2 million provisions for taxes. There was a slight decline in interest and dividend income from its recently formed joint-venture PennantPark Senior Loan Fund (“PSLF”) but is expected to grow over the coming quarters. Also the company has started exiting some of its non-income-producing assets which will likely be reinvested into “yield generating debt instruments”:

Art Penn, Chairman/CEO: “We are pleased with the substantial increase in NAV this past quarter due to material appreciation in the value of several equity investments. We believe that we can generate increased income over time by rotating those equity positions into yield generating debt instruments. We are starting to see some progress on the exit of those equity investments. Additionally, we have the ability to grow the PNNT balance sheet and our PSLF JV which should also generate additional income for the Company.”

As expected its NAV per share grew by another 5.2% mostly due to equity investments driving PNNT’s leverage (debt-to-equity) well below historical levels (0.75 net of SBA debentures) giving the company plenty of growth capital for increased earnings potential.

For additional detail about PNNT including dividend coverage potential and risk profile, please read “PNNT Updated Projections/Pricing: Dividend Increases Coming“. We will update this report next month.

Full BDC Reports

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.