The following information was previously provided to subscribers of Premium BDC Reports along with:

- CGBD target prices/buying points

- CGBD risk profile, potential credit issues, and overall rankings

- CGBD dividend coverage projections (base, best, worst-case scenarios)

![]()

CGBD Summary

- I have increased the target prices for CGBD to take into account continued improvement in credit quality and earnings potential likely driving quarterly supplementals of $0.05/share.

- CGBD accounts for almost 3% of my portfolio providing investors with 70% total returns over the last 12 months.

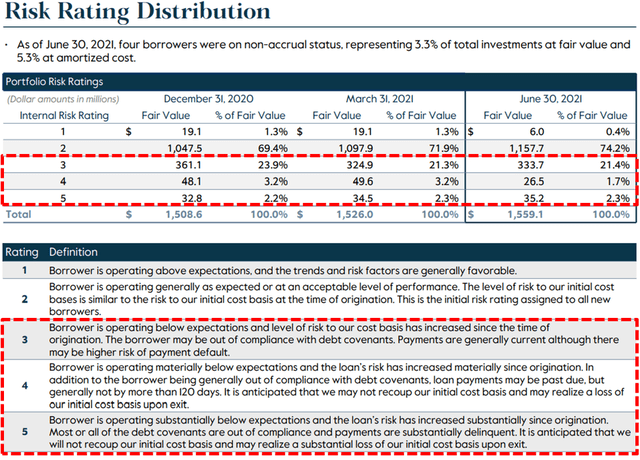

- Some of the reasons that CGBD remains a ‘Tier 3’ are discussed in this report including portfolio investments with a risk rating between 3 and 5 (implies downgraded) remains around 25.4% of the portfolio and non-accruals are still around 5.3% of the portfolio cost (3.3% of FV). I would like to see the company consistently earn $0.37 or more per share per quarter to cover the $0.32 regular quarterly dividend plus the $0.05 of quarterly supplemental dividends.

CGBD Dividend Coverage Update

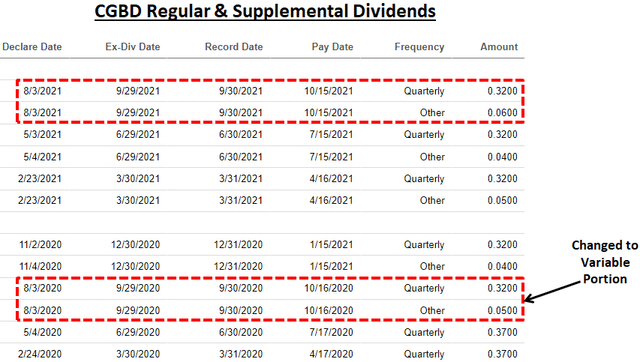

Previous reports predicted a reduction in the regular quarterly dividend (from $0.37 to $0.32) due to lower income from its Credit Fund I, declines in portfolio yield and interest income primarily due to the decrease in LIBOR and additional loans placed on non-accrual as well as the need to reduce leverage. Similar to other BDCs, CGBD converted to a “variable distribution policy” with the objective of “paying out a majority of the excess above the $0.32 and we would anticipate doing the same going forward”.

From previous call: “Similar to last quarter, as we look forward to the rest of 2021, we remain very confident in our ability to comfortably deliver the $0.32 regular dividend, but continue the sizable supplemental dividends. In line with the $0.04 to $0.05 we have been paying the last few quarters.”

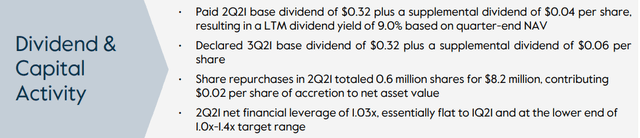

On August 3, 2021, the company announced a regular quarterly common dividend of $0.32 plus a supplemental dividend of $0.06, which are payable on October 15, 2021 to common stockholders of record on August 30, 2021. It should be noted that this was slightly above my base projected supplemental of $0.05.

“We generated net investment income of $0.38 per common share, and declared a total dividend of $0.38. This includes a base dividend of $0.32 and a $0.06 supplemental dividend in line with our policy of regularly distributing substantially all of the excess income earned over our base dividend. We see earnings continuing in the context of $0.36 to $0.37, as we’ve reported over the last several quarters, which remains comfortably in excess of our $0.32 base dividend.”

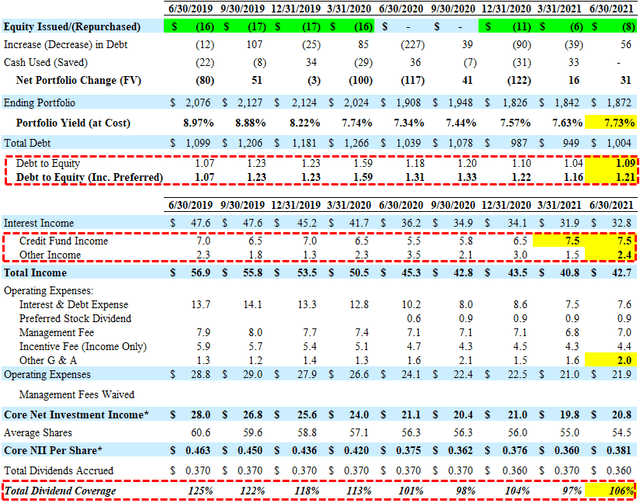

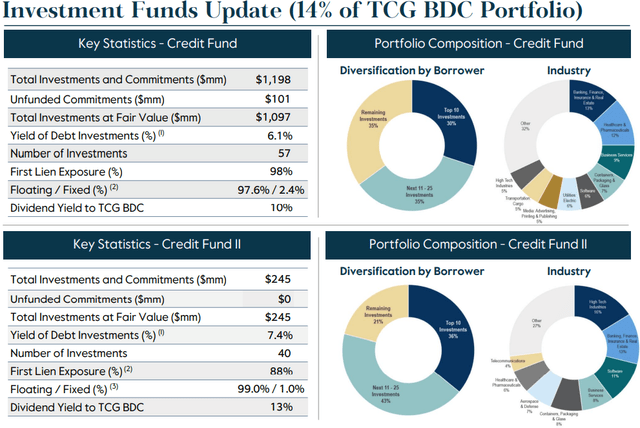

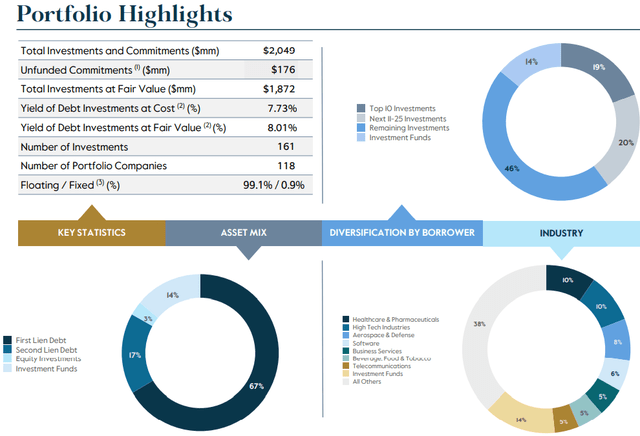

For Q2 2021, CGBD reported between its base and best-case projections covering its regular and supplemental dividends by 106% mostly due to higher-than-expected amendment and underwriting fees during the quarter. Also, there was another increase in its portfolio yield from 7.63% to 7.73%. Dividend income from its Credit Funds remained stable that currently represent around 13.9% of the total portfolio.

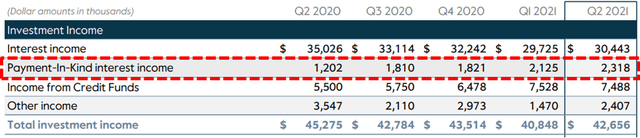

As mentioned in previous reports, the amount of payment-in-kind (“PIK”) interest income has been increasing and needs to be watched as it now accounts for 7.1% of interest income as compared to only 1.5% in Q1 2020.

Upcoming Share Repurchases:

On November 2, 2020, the Board authorized an extension as well as the expansion of its $150 million stock repurchase program at prices below NAV per share through November 5, 2021. The company previously repurchased around $86 million worth of shares but “paused” in Q2 2020. CGBD has reduced its debt-to-equity ratio increasing liquidity and management “intends to pursue the appropriate balance of both share repurchases and attractive new investment opportunities”.

During Q2 2021, the company repurchased 0.6 million shares at an average cost of $13.62 per share for $8.2 million resulting in accretion to NAV per share of $0.02. As of June 30, 2021, there was $39.4 million remaining under the stock repurchase program.

“We repurchased $8 million of our common stock, resulting in $0.02 of accretion to net asset value. We care deeply about our shareholders total return and at our stock’s current valuation, we’ll continue to be consistent active repurchasers of our shares.”

Management discussed on the previous call including less share repurchases if the stock price continues higher and I have taken into account with the updated projections:

“We will obviously scale those who purchases based on how accretive they are overall, and that will fluctuate as our as our stock price fluctuates. So, it shouldn’t be a surprise that we purchased a bit less this quarter. Repurchasing our shares was a bit less accretive this quarter than it had been in prior quarters. But nevertheless, again we continue to see great value in our shares. So, you should continue to see repurchases at least in the near future. And we have just as a side note, we have plenty of room and plenty of time left on our repurchase authorization that the Board gives us each year.”

Middle Market Credit Funds:

Previously, the company announced a new joint venture (“JV”) with Cliffwater to “create Middle Market Credit Fund II (“Credit Fund II”), a move that’s intended to better capitalize on senior-loan opportunities that have emerged from recent market volatility”. CGBD sold senior secured debt investments with a principal balance of $250 million to Credit Fund II in exchange for 84.13% of Credit Fund II’s membership interests and gross cash proceeds of $170 million. The new venture gives TCG BDC enhanced balance sheet flexibility, including increased capital to deploy into an attractive origination environment and additional capacity to repurchase shares.

Previously, there was a decline in income recognized from its Credit Fund I from $7.0 million in Q4 2019 to $5.5 million in Q2 2020 due to lower yields, OID, and lower leverage. During Q2 2021 ORCC recognized almost $7.5 million in income (same as previous quarter) related to the funds compared to $6.5 million in Q4 2020. Management expects the amount of dividend income to remain around $7.5 million and is taken into account with the ‘base case’ projections.

“Moving on to the performance of our 2 JVs. Total dividend income was $7.5 million in line with last quarter. On a combined basis, our dividend yield from the JVs inched up from 10% closer to a 11%. Given we’re able to make return of capital at MMCF 1 following a recent favorable amendment under our primary credit facility. Total assets at the JVs increased from $1.2 billion to $1.3 billion reversing the recent trend of declines that have been driven by repayment headwinds. This was particularly evident in the MMCF 1 portfolio with fair value increasing by over 10% in the second quarter. Going forward, we continue to expect stable dividend generation from the 2 JVs similar to this quarter’s results.”

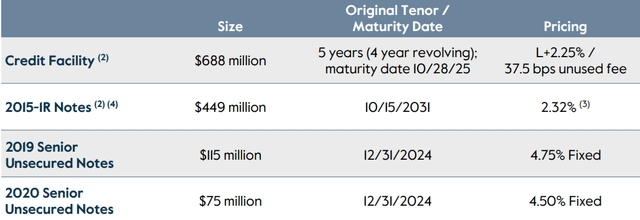

As of June 30, 2021, CGBD had cash and cash equivalents of around $59 million and almost $323 million available for additional borrowings under its revolving credit facilities. Management is targeting a debt-to-equity ratio between 1.00 and 1.40 including the recently issued preferred equity and is taken into account with the projections.

“We continue to be very well positioned with the right side of our balance sheet. Statutory leverage was again stable at about 1.2x, while net financial leverage, which as soon as the preferred is converted in a risk metric we used to manage the business was again right around one turn of leverage. So we’re sitting close to the lower end of our target range of 1.00x to 1.40x giving us flexibility to invest prudently in the current robust field environment.”

In May 2020, the company issued $50 million in Series A Convertible Preferred Stock, purchased by an affiliate of The Carlyle Group, Inc. with the proceeds used to pay down outstanding debt. The Series A Convertible Preferred Stock pays dividends, at the Company’s option, at a rate of either 7% (to the extent paid in cash) or 9% (to the extent paid in kind) and is convertible into common shares at an implied conversion price of $9.50, or 57% above the current 30-day VWAP. This transaction improved the overall capitalization/liquidity but with a dilutive impact to current shareholders. Management continues to mention that “there is no intention to convert” into common shares:

Recent call: “And regarding the preferred equity issuance for May 2020. I’ll reiterate again, this instrument was a strong sign of support by Carlyle during the darkest days of the global pandemic. And it continues to be a long-term investment by Carlyle in our BDC. So currently, there is no intention to convert.”

Previous call: “And regarding the preferred equity issuance for May of 2020, our stock is now trading well above the conversion price. But as we’ve noted previously, this instrument remains a long-term investment by Carlyle in our BDC. So there currently is no intention to convert.”

Also discussed on the recent call was potentially refinancing the preferred stock especially given the current market for unsecured debt with many of the larger BDCs borrowing between 2% to 3% compared to the 7% currently being paid. I fully agree but management perceives this as “permanent equity” capital and provides the company with increased financial flexibility”:

Q. “You guys have been able to issue liability, unsecured notes recently at 4.5%. I wouldn’t be surprised if you could do something less than that in today’s market. So why is paying 7% cash on a convertible preferred, an attractive source of financing when you’re able to tap unsecured notes at 4.5% and then depending on your answer that we can get into converting that, what does that look like? How does that look like from a manager converting at a sizable discount, the external manager converting and having and making a sizable profit from supporting the BDC, I don’t know if that’s a great look either, but I just don’t understand that comment why paying 7% is attractive source when you guys are issuing debt for significantly below that.”

A. “So just to kind of reiterate if you recall, when we put the convert in place, life was pretty dire, right our stock price was half of what it is today, we’re in the middle of the pandemic, we’re looking at really how to make sure our balance sheet was strong and defensible during a time that was – just an enormous amount of uncertainty. And Carlyle coming in and doing the preferred was a really great testament not only to their support of our business, but also to just really help us achieve the goals that we wanted to achieve at that point in time. So, I’d like really people to kind of just put all of this in context. For Carlyle, it’s a great show support, but let’s not forget it, it is $50 million for Carlyle, and it’s $50 million for our balance sheets. So it’s relatively small, and Carlyle, this is strategic right they’re not looking to convert this anytime soon, it’s here to support the business, and we really look at this as equity. So, compared to our dividend yield on our common stock, this is paying 7%, which is we think, actually a pretty attractive piece of equity for our balance sheet. And converting it is just not really in the cards. So I would just encourage people to think of this really as permanent equity, which you may view as expensive, but we actually view as pretty, pretty cheap. And know that this is not something that is going to dilute our current shareholders really in the foreseeable future that that we can tell. So and we’re pretty conscious of that, when back when we issued this, we didn’t want to dilute shareholders especially back in the Spring of 2020 and that’s still our view now, there’s no reason to dilute current shareholders, not when Carlyle is standing behind the business like it is. We have the financial flexibility, effectively equity, we manage the business as if it’s equity, we get credit under our leverage facilities as if it’s equity. So certainly from the financial flexibility perspective, we think it’s well priced equity. So managing the business would mean we have to have this in the capital structure, we would have better capital structure.”

CGBD has an average fee structure of 1.50% base management fee (compared to 1.00% to 2.00%) and an incentive fee of 17.5% (compared to the standard 20.0%) but is not best-of-breed as it does not include a ‘total return hurdle’ to take into account capital losses when calculating the income incentive fees. This was discussed on the recent call:

Q. “I agree that life was pretty dire when the parents stepped up in during COVID. But it was also rather bright and sunny in 2018 when the BDC lost a lot of money and was paying the parent a full incentive fee. So I guess the question is, against your opening remarks about caring deeply about the shareholders total return. Do you perhaps care more deeply about the advisor or should something give – like, should there be sort of pick one between the convert and not having a credit look back?”

A. “We do believe that Carlyle, Carlyle has a very fair and balanced management fee structure. We think that in the shareholders are getting a lot of value for that. Keep in mind that, we do manage the JVs and don’t take a fee for that. So sometimes, I think that gets a little bit lost when people look at our overall fee structure. So we’re kind of getting the management the JVs at a very nice discount on the management fee. So our management fee and not having a look back, I’m not really sure that that is what is going to be driving our stock price higher, it’s really, we’ve got to continue on this straightforward consistent performance get our non-accruals down, which is looking better and better. And really keep our shareholders satisfied by knowing that we can generate our dividends, perform well on credits. And ultimately, we think that will get our stock price up. I’m not sure our management fee is really the issue.”

CGBD Quick Risk Profile

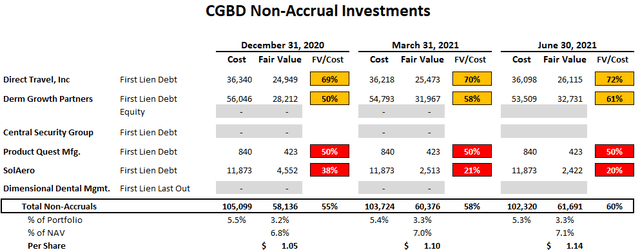

Non-accrual investments remain around 3.3% of the portfolio fair value as there have been no investments added over the last four quarters. If these investments were completely written off it would have an impact of around $1.14 to its net asset value (“NAV”) per share or around 7.1%.

“We have seen no new non-accruals in the last year and we’re confident in the trajectory and progress we’re making in each of our four non-accrual names. We’re proud of the performance of the portfolio through COVID. And most importantly, we see the current trajectory of improving performance and solid credit continuing on its current upward path. Total non-accruals were flat at 3.3% based on fair value, and this was the fourth consecutive quarter with no new additional non-accruals. Similar to last quarter, we don’t see any additional loans at risk of non-accrual.”

It should be noted that Direct Travel and Product Quest currently have a risk ranking of 4 compared to Derm Growth Partners and SolAero with a lower risk ranking of 5 and have been discussed in previous reports.

Risk Rating 4 – Borrower is operating materially below expectations and the loan’s risk has increased materially since origination. In addition to the borrower being generally out of compliance with debt covenants, loan payments may be past due, but generally not by more than 120 days. It is anticipated that we may not recoup our initial cost basis and may realize a loss of our initial cost basis upon exit.

Risk Rating 5 – Borrower is operating substantially below expectations and the loan’s risk has increased substantially since origination. Most or all of the debt covenants are out of compliance and payments are substantially delinquent. It is anticipated that we will not recoup our initial cost basis and may realize a substantial loss of our initial cost basis upon exit.

CGBD previously had 6 categories of risk ratings and basically combined the previous rating 3 and 4 that accounted for 16.7% of the portfolio as of Q1 2020 into the new rating 3 which is now 21.4% and needs to be watched. However, the total amount of investments with risk rating between 3 and 5 (which implies that these investments have been downgraded) declined from 26.8% (as of Q1 2021) to 25.4% (as of Q2 2021) of the portfolio but is still considered high and is one of the reasons that CGBD remains a ‘Tier 3’ BDC as discussed earlier.

“The total fair value of transactions risk rated 3 to 5, indicating some level of downgrade since we made the investment improved again this quarter by $14 million in the aggregate. While over $15 million in transactions experienced some level of upgrade. While there remain some unfinished work, we’re very pleased with the continued positive momentum and the performance of the overall portfolio.”

SolAero was marked slightly lower again in Q2 2021 (now valued at 20% of cost) and was discussed on the previous call:

From previous call: “So on SolAero that’s a deal we actually restructured about a year and a half ago, that had just fundamental issues based on the industry solid industry. It’s highly typical, and you’re exactly right, that this is had some issues based on its ties to one web that’s one that we are in the equity see in that transaction and it’s one that we see a positive resolution going forward or at least we’re in negotiations and hoping to have positive resolution in terms of that company, turning the corner and working with their top customer one web as one way emergence from their bankruptcy. Direct Travel probably one of, if not the most severely COVID impacted name on our book and that was the other transaction I noted, we had two deals that restructured that deal also restructured in early October timeframe and the lenders again supporting that business and are the majority owners going forward it providing the capital for that, for that business. I will say is each all four of those situations what I’d highlight is we are the original debt and existing debt is in the first lien position in each case. In three cases the lenders are there now all in the equity or we anticipate will own the equity. So we think we’re in a good position based on our seniority and based on our equity position to drive strong outcomes in recoveries in those situations.”

As discussed in previous reports, U.S. Dermatology Partners defaulted on a $377 million financing provided by a group of investment firms. The Washington Post previously reported that the company may have received financing from the Paycheck Protection Program. The dermatology practice owner was reviewing its options, including a recapitalization or debt-for-equity swap with its current lenders, Golub Capital, The Carlyle Group Inc. and Ares Management. CGBD’s investment in Derm Growth Partners (Dermatology Associates) was added to non-accrual status during Q4 2019. This investment will likely be restructured over “the next couple of quarters”.

From previous call: “Dermatology Associates is one we have been engaged and we remain engaged and we anticipate a similar resolution on that transaction or that current capital structure within, let’s call it the next couple of quarters.”

Also mentioned in previous reports, Direct Travel completed a restructuring whereby the lenders received the majority of the equity in Direct Travel but maintained the principal balance in the existing debt. As part of the transaction, the lenders also provided a delayed draw term loan facility to support ongoing liquidity of the business, CGBD received an approximate 9% ownership stake in Direct Travel and the debt remains on non-accrual.

From previous call: “You’ll see in the cases of Direct Travel and Central Security that we closed successful restructurings and now hold both debt and equity instruments. In both cases, we think with lenders now holding majority of the equity, we’re better positioned to achieve superior recoveries.”

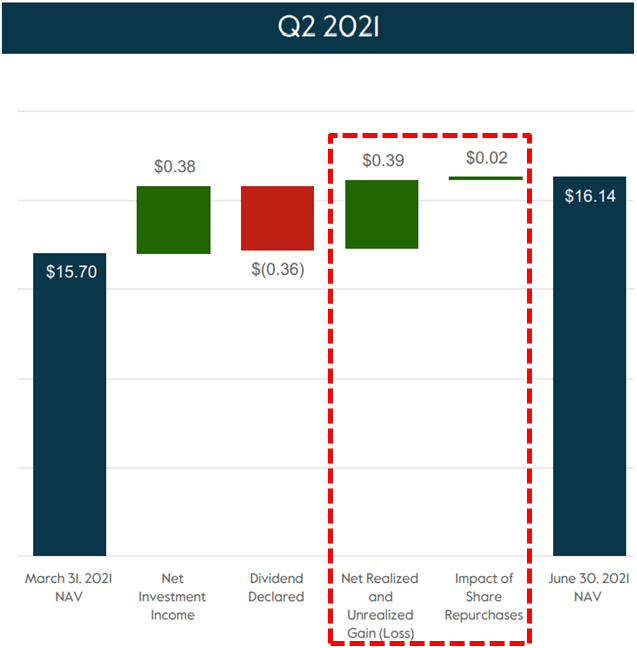

During Q2 2021, CGBD’s net asset value (“NAV”) increased by another $0.44 or 2.8% mostly due to net unrealized appreciation of $0.39 per share driven by “stronger overall credit performance, particularly in those names impacted by COVID” including Derm Growth Partners and Direct Travel as well as accretive share repurchases adding $0.02 per share.

“Net asset value per share increased 2.8% or $0.44 from $15.70 to $16.14 while improving market yields drove some of this increase, NAV was substantially bolstered by stronger overall credit performance, particularly in those names impacted by COVID. We’ve taken an appropriately conservative approach to valuation through this cycle and we expect continued underlying fundamental improvement to drive positive NAV migration in the coming quarters. Additionally, we repurchased $8 million of our common stock, resulting in $0.02 of accretion to net asset value.”

“On evaluations our total aggregate realized and unrealized net gain was $21 million for the quarter. The fifth consecutive quarter of positive performance following the drop in March 2020. Using the same buckets I’ve outlined in prior quarters, we again saw improvement across the board. First, performing lower COVID-impacted names plus our equity investments in the JVs, which accounts for combined 70% of the portfolio increased in value about $8 million compared to 3/31. Second, the assets that have been underperforming pre-pandemic, so which have COVID exposure were up $4 million, marking the fifth consecutive quarter of stability or improvement. This included in exit at par of our investment in Plano Molding. The final category is the moderate to heavier COVID-impacted gains. We continue to see improvement in fundamentals and recovery prospects for these investments. Collectively they experienced a net $9 million increase in value.”

Full BDC Reports

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.