The following information was previously provided to subscribers of Premium BDC Reports along with:

- GSBD target prices/buying points

- GSBD risk profile, potential credit issues, and overall rankings

- GSBD dividend coverage projections (base, best, worst-case scenarios)

![]()

GSBD Dividend Coverage Update

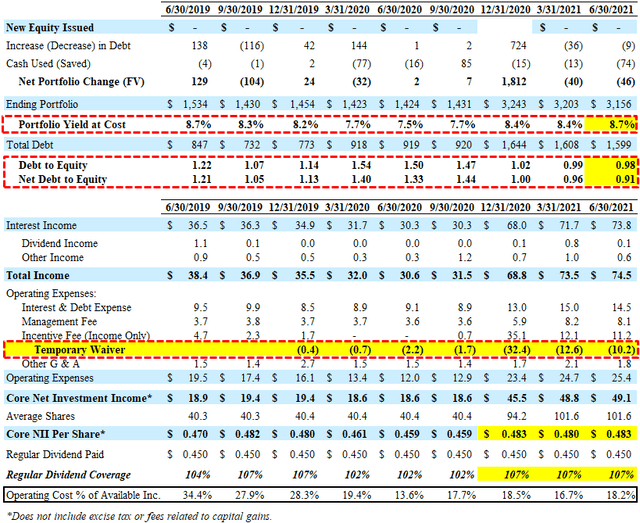

GSBD has covered its dividend by an average of 105% over the last 8 quarters growing spillover/undistributed income to around $0.46 per share for temporary dividend coverage shortfalls but the company will likely retain rather than use to pay special dividends.

From previous call: “The company had $46.6 million in taxable accumulated undistributed net investment income at quarter end, resulting from net investment income that has exceeded our dividend historically. Pro forma for the completion of the merger at the end of Q3, this equates to $0.46 per share.”

GSAM is waiving a portion of its incentive fee for the four quarters of 2021 (Q1 2021 through and including Q4 2021) in an amount sufficient to ensure that GSBD’s net investment income per weighted average share outstanding for such quarter is at least $0.48 per share per quarter. However, as shown in the previous financial projections, there is a good chance that the company will be able to cover the dividend without the need for fee waivers.

On August 5, 2021, the Board reaffirmed its regular dividend of $0.45 per share payable to shareholders of record as of September 30, 2021. Previously, the company paid a special dividend of $0.05 per share in May 2021 which is the second of its three quarterly installments of special dividends aggregating to $0.15 per share in connection with the merger.

For Q2 2021, GSBD reported slightly above its best-case projections due to much higher-than-expected portfolio yield driven by an increase in accelerated accretion related to repayments partially offset by lower portfolio growth (decline) and lower fee and dividend income. Leverage (debt-to-equity) again declined to a new near-term low of 0.91 (net of cash) giving the company adequate growth capital for increased earnings potential.

“For the third consecutive quarter, GSBD experienced a new high watermark for repayment activity, which amounted to $277 million of market value across 12 different portfolio companies this quarter. Fortunately, our powerful origination engine has largely kept pace during this active repayment environment. We expect to resume balance sheet growth in the back half of the year moving closer to more normalized net debt to equity ratios from this quarter and level of 0.91 times.”

However, management is not expecting the same level of repayments over the coming quarters:

“I do think that we will start to see a bit of a moderation at least in the short-term of some of that repayment activity relative to our pipeline of investment activity. And that should give rise to some portfolio growth.”

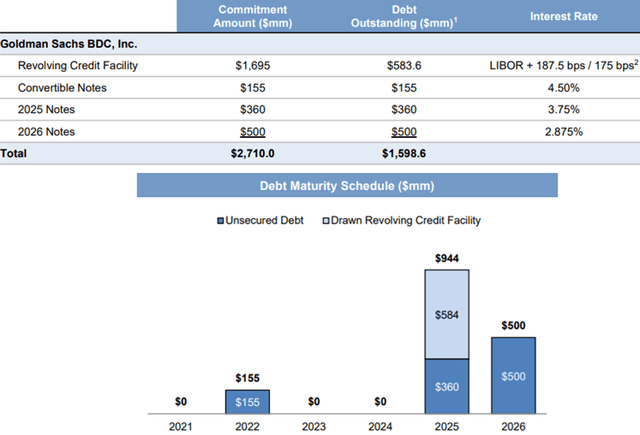

Similar to other BDCs, GSBD has been lowering its borrowing rates as well as constructing a flexible balance sheet including the public offering of $500 million of 2.875%unsecured notes due 2026. On August 13, 2021, amended its Truist Revolving Credit Facility to reduce the asset coverage required to reduce the stated interest rate from LIBOR plus 2.00% to LIBOR plus 1.875%. Previously, the company issued $360 million of unsecured notes due 2025 at 3.750%. As of June 30, 2021, 63% of its borrowings were unsecured with $1.1 billion of availability under its credit facility and $120 million in cash. Fitch’s reaffirmed GSBD’s investment grade rating of BBB- and revised the outlook to stable.

“At quarter end, 63% of the company’s outstanding borrowings were unsecured debt and $1.1 billion of capacity was available under GSBD’s secured revolving credit facility. Given the current debt position and available capacity, we continue to feel we have ample capacity to fund new investment opportunities with borrowings under our credit facility.”

On October 12, 2020, GSBD completed its merger with Goldman Sachs Middle Market Lending (“MMLC”) which doubled the size of the company including significant deleveraging. This created more capacity to deploy capital while adding a greater margin of safety to maintain GSBD’s investment-grade credit rating. Previously, shareholders approved the reduced asset coverage ratio of at least 150% (potentially allowing a debt-to-equity of 2.00) and management reduced the base management fee from 1.50% to 1.00%.

GSBD Risk Profile Quick Update

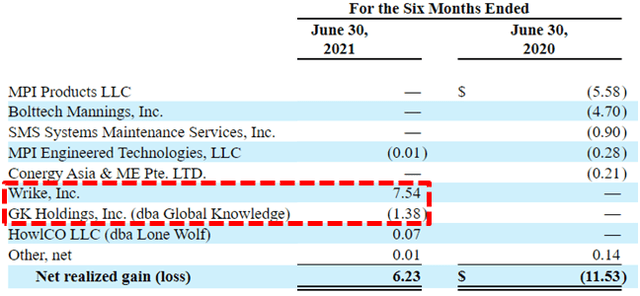

On June 11, 2021, its non-accrual investment in GK Holdings, Inc. (Global Knowledge) was partially repaid due to a SPAC-related merger with a competitor resulting in a small realized loss of $0.01 per share but reduced non-accruals. As of June 30, 2021, investments on non-accrual status accounted for 0.0% and 0.3% of the total investment portfolio at fair value and cost, respectively. It should be noted that GSBD has placed only one portfolio company on non-accrual status over the last six quarters.

“This decline in non-accrual is primarily a result of the repayment of our investment in GK Holdings. On June 11, GK Holdings consummated a merger with competitor in conjunction with incremental capital from a SPAC. As a result, GSBD received partial repayments on both first lien and second lien positions and received past due interest on the first lien position. GSBD rolled a portion of the existing loan into a new loan to the combined company, which is called Skillsoft in a deleveraged structure. Subsequent to quarter end, Skillsoft refinance its capital structure and repaid that remaining loan. So as a result of these transactions, we have fully exited our investment. And while we’re never placed an investment on non-accrual, we do think that this transaction is a demonstration of the care and effort that we put into our underperforming positions

During Q1 2021, there was around $7.5 million or $0.07 per share in realized gains related to the sale of its equity investment in Wrike, Inc in March 2021.

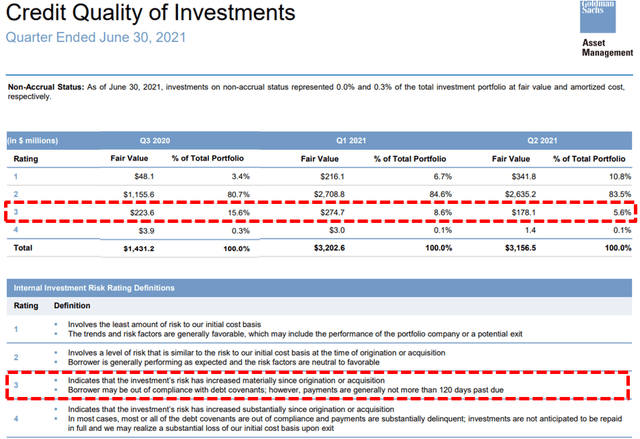

There has been continued improvement in the amount of investments considered ‘Rating 3’ to have “risk has increased materially” and/or “out of compliance with debt covenants” from 15.6% to 5.6% of the portfolio over the last three quarters.

Rating 3 investments indicate that the risk to our ability to recoup the initial cost basis of such investment has increased materially since origination or acquisition, including as a result of factors such as declining performance and non-compliance with debt covenants; however, payments are generally not more than 120 days past due;

“The underlying performance of our portfolio companies overall was stable quarter-over-quarter. The weighted average net debt to EBITDA of the companies in the portfolio was 5.9 times at quarter end, which is a slight improvement from 6 times at the end of the last quarter. The weighted average interest coverage of the companies in our investment portfolio was 2.6 times, again, a slight improvement from the 2.5 times at the end of the prior quarter. Consistent with our history, none of our investment activity this quarter was in so-called covenant-lite structures. Furthermore, in certain positions where we were the incumbent lender, we opted not to roll into new deals that did not meet our standards for risk reward characteristics sometimes based on rate and other times based on structure and document integrity.

“The focus of the platform continues to be that heart of the middle markets that business that does maybe up to $50 million of EBITDA focusing on sectors where could be bigger capital structures in parts of, for example, the technology and software space but the nature of the underwrite, the nature of the growth trajectory of those businesses requires a little bit of a more structured credit investment and we’ve been doing that for quite a long period of time. Even in those bigger cap opportunities, our history, our position of that market allows us to continue to be quite successful there.”

During Q2 2021, GSBD’s net asset value (“NAV”) per share increased slightly by 0.3% due to over-earning the dividends.

“Net asset value per share increased to $16.05 per share as of June 30, an improvement of approximately 30 basis points from the end of the first quarter. Against the accommodative overall market backdrop, the NAV increase resulted from ongoing stable to improving performance our portfolio companies offset slightly by the impact of $0.50 per share specialty event paid during the quarter.”

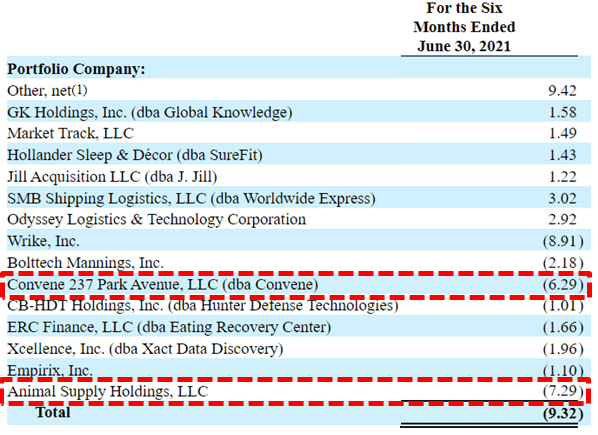

As discussed in the previous report, Animal Supply Holdings and Convene 237 Park Avenue have been recently marked down and need to be watched. During Q3 2020, its first-lien debt investment, preferred and common equity in Animal Supplywere exchanged for second lien debt, common equity and a right to purchase additional first-lien debt, second lien debt, and common equity, which resulted in a realized loss $0.89 per share. Convene focuses on shared meeting spaces directly impacted by the pandemic but has recently received additional capital from its equity shareholders and junior capital (below GSBD’s first-lien position).

“So Convene is focused on providing shared meeting space services and leading — it’s a first lien investment in top of the capital structure, very well structured, leading into the pandemic, really performing quite, quite well, broadly benefiting from a trend around people wanting to optimize their real estate footprints. One of the least efficient uses of your real estate is a big shared meeting space that gets used on a less frequent basis, so big secular tailwinds driving their business. But of course, in the lockdown environments, a lot of challenges within that business, really, a remarkable, I would say, management effort to get the business’s cost structure down significantly to reduce the rent payments quite significantly as well. In addition, we’ve had significant support from the equity shareholder base that has infused additional liquidity into the company. So we, like you, are looking forward to a bit more of a normalization of behavior more broadly. And I think in the current environment, appropriate to mark that investment down. But like I noted, we do take comfort in junior capital beneath us coming into the business and more broadly, the vaccine rollouts that are really starting to take hold here, resulting in a very different return to office, for example. And I think just more significant social interaction.”

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy to digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning we provide quick updates for the sector including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on at least two BDCs each week prioritized by focusing on ‘buying opportunities’ as well as potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Friday Comparison or Baby Bond Reports – A series of updates comparing expense/return ratios, leverage, Baby Bonds, portfolio mix, with discussions of impacts to dividend coverage and risk.

![]()

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.