The following information was previously provided to subscribers of Premium BDC Reports along with:

- PNNT target prices/buying points

- PNNT risk profile, potential credit issues, and overall rankings

- PNNT dividend coverage projections (base, best, worst-case scenarios)

![]()

PNNT Dividend, NAV Per Share & Management Fees Update

PNNT’s dividend coverage continues to improve partially due to its previous and upcoming increases in its net asset value (“NAV”) per share combined with its 7% hurdle, the eventual selling and reinvesting of many of its equity positions, and its PennantPark Senior Loan Fund (“PSLF”) joint-venture with Pantheon Ventures.

“With regard to growing net investment income, we have a three-pronged strategy, which includes; number one, growing assets on balance sheet at PNNT as we move towards our target leverage ratio of 1.25x, debt-to-equity from 0.8x; number two, growing our PSLF JV with Pantheon to about $550 million of assets from approximately $400 million of assets through balance sheet optimization, including a potential securitization; and three, the opportunity to rotate out of our equity investments over time into yield instruments. Equity investments held for the past 12 months have appreciated by approximately 45%, driven by many of the companies previously mentioned. Our long-term goal continues to target that percentage down to about 10% of the portfolio. As we monetize the equity portfolio, we are looking forward to investing the cash and to yielding debt instruments to increase net investment income.”

As predicted in the previous report, there was $41.7 million or $0.62 per share of realized gains during Q2 2021. Please keep in mind that the company is only paying $0.12 per share of quarterly dividends so this is a significant amount and was predicted in previous reports.

“We are making substantial progress on the exit of those equity investments. Additionally, we have been actively investing in new loans since the most recent quarter end and the outlook in our view for continued growth is excellent. During the quarter, we generated $51 million of cash proceeds from the equity portfolio, including proceeds from Wheel Pros, Walker Edison, DecoPac, WVB, Cano, and others.”

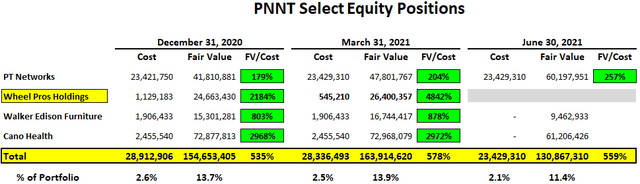

There is a good chance that PNNT will be selling its equity positions in Cano Health, Inc. (CANO), PT Networks, and Walker Edison Furniture over the next 12 to 18 months. These investments account for over $130 million or 11.4% of the portfolio with the proceeds to be reinvested into income-producing assets.

As shown in the table below, these investments are marked well above cost and will likely result in a total of $107 million or $1.60 per share of realized gains.

Management discussed these investments on the recent call mentioning additional NAV upside as well as increased earning potential through reinvestment:

“We are pleased that we have significant equity investments in several of these companies, which can substantially move the needle of our NAV. I would like to highlight some of those companies; the companies are Cano, Walker Edison, PT Network, and JF Petroleum. These companies are gaining financial momentum in this environment and our NAV should be solidified and bolstered from these substantial equity investments as their momentum continues.”

“PT Network is the leading physical and occupational therapy provider in the Mid-Atlantic States. Our equity position has a cost of $23 million and a fair market value of $60 million as of June 30. MidOcean JF Holdings or JF Petroleum, is a leader in the distribution, installation and servicing of vehicle fueling, and related equipment to retail fueling locations in the U.S.”

“Walker Edison is a leading e-commerce platform focused on selling furniture exclusively online through top e-commerce companies. Our equity position has a cost of zero and a fair market value of $9.5 million as of June 30. Due to two capital transactions, one in dividend recap and another in equity financing by Blackstone, we have received cash equal to 4x our capital on our equity position.”

“Cano Health is a national leader in primary healthcare, who is leading the way in transforming healthcare to provide high-quality care at a reasonable cost to a large population. Our equity position has a cost and fair market value on June 30 of zero and $61 million, respectively.”

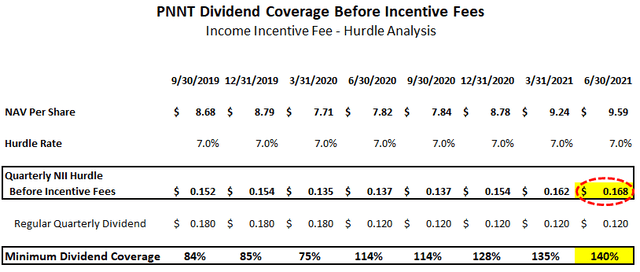

PNNT’s incentive fee “hurdle rate” of 7.0% is applied to “net assets” to determine “pre-incentive fee net investment income” per share before management earns its income incentive fees. As shown in the following table, over the coming quarters the company will likely earn around $0.16 to $0.17 per share each quarter before paying management incentive fees covering around 140% which is ‘math’ driven by an annual hurdle rate of 7% on equity. It is important to note that PNNT could earn less but management would not be paid an incentive fee.

Management is expecting lower amounts of repayments coupled with higher amounts of originations for calendar Q3 2021 which has been taken into account with the updated projections driving higher leverage:

“Since June 30, PNNT has had new originations of $69 million. Although in the June quarter, repayments on loans roughly equaled new loan originations and the September quarter so far repayment activity has abated and new originations have accelerated.”

There is a chance that the company could start repurchasing shares using some of the proceeds from selling equity positions especially given that the stock is trading 32% below its NAV per share and was discussed on the recent call;

Q. “Is there any consideration towards even a modest share repurchase program to take advantage of the discount? I mean, it’s the highest in the peer group and yet your returns seem to be improving and NAV is clearly improved and perhaps that would be a useful way to take advantage of it for shareholders?”

A. “Yes. It’s a great question, and we’re always considering and I think as we generate a $51 million of proceeds on from equity investments this past quarter. I’m hopeful that as – those continue and get even greater. So hopefully it will be a lot greater than the $51 million and dedicate a portion of that over time to buying back the stock. So we got to play it out. We got to start generating these proceeds over the coming quarters. And I would certainly, if the stock price continues to be where it is certainly consider – we would certainly consider dedicating a portion of hopefully bigger proceeds to very worthwhile investment of the stock.”

My primary concerns for PNNT are mostly related to the recent increase in payment-in-kind (“PIK”) interest income from 13% to 20% of total income over the last three quarters and the commodity-related exposure combined lack of a “total return hurdle” incentive fee structure to protect shareholders from capital losses. However, management consistently “does the right thing” including continued fee waivers and previously reducing its base management (from 2.00% to 1.75%) and incentive fees (from 20.0% to 17.5%).

PNNT June 30, 2021 & Risk Profile Update

PennantPark Investment (PNNT) reported between its base and best case projections with ‘core NII’ of $0.141 per share and 118% coverage of the quarterly dividend adjusting for $1.1 million of expenses related to the early repayment of SBA debentures and $0.2 million provisions for taxes. There was a slight increase in interest and dividend income from its recently formed joint-venture PennantPark Senior Loan Fund (“PSLF”) which is expected to grow over the coming quarters. Also the company has started exiting some of its non-income-producing assets which will likely be reinvested into “yield generating debt instruments”:

Art Penn, Chairman/CEO: “We are pleased with the substantial increase in net asset value this past quarter due to material appreciation in the value of several equity investments. We believe that we can generate increased income over time as we grow the PNNT and PSLF balance sheets and by rotating equity positions into debt instruments. We are making substantial progress on the exit of those equity investments. Additionally, we have been actively investing in new loans since the most recent quarter end and the outlook in our view for continued growth is excellent.”

PNNT has plenty of borrowing capacity especially after taking into account its SBA leverage at 10-year fixed rates (current average of 3.2%) that are excluded from typical BDC leverage ratios. Previously, PNNT received a “green light” letter for its third SBIC license for an additional $175 million of SBA financing but withdrew the application and will be paying down a portion of its second license:

“We have withdrawn our application for a new SBIC at this time. We intend to gradually pay down SBIC 2, while also providing — proving out our portfolio through COVID, before reassessing.”

On April 14, 2021, PNNT announced the pricing of a public offering of $150 million in its 4.50% unsecured notes due May 1, 2026. These notes were priced just below par driving a yield-to-maturity of 4.625% and will slightly increase the overall borrowing rates but also a more flexible balance sheet for future portfolio growth.

As mentioned in previous reports PRA Events, Inc. and MailSouth, Inc. were added back to accrual status resulting in no non-accrual investments as of December 31, 2020. However, the interest payments from these investments are payment-in-kind (“PIK”) which now accounts for 20% of total income (compared to 13.0% previously) and needs to be watched

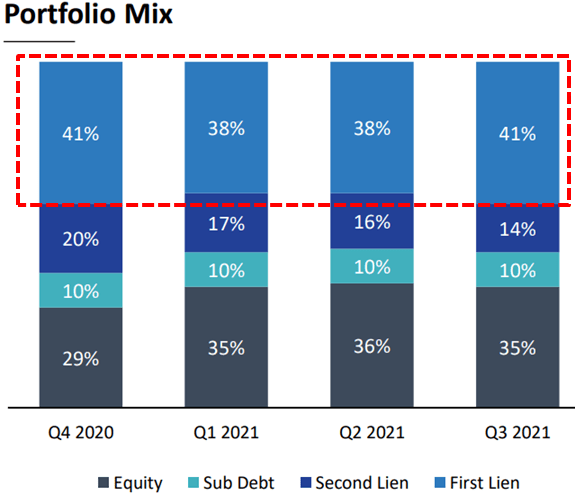

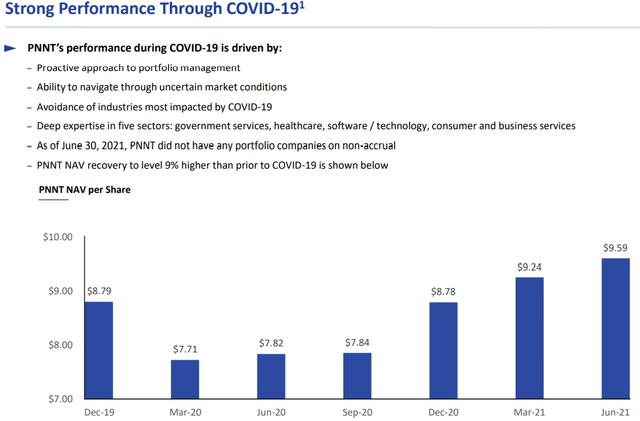

As expected its NAV per share grew by another 3.8% mostly due to equity investments driving PNNT’s leverage (debt-to-equity) well below historical levels (0.70 net of SBA debentures) giving the company plenty of growth capital for increased earnings potential.

“Our portfolio performance remains strong. As of June 30, average debt-to-EBITDA on the portfolio was 4.6x and the average interest coverage ratio, the amount by which cash income exceeds cash interest expense was 3.4x. We have no non-accruals on our books in PNNT and PSLF.”

Equity investments now account for 35% of the portfolio and over the coming quarters, I am expecting the company to sell a good portion of these investments (including energy/oil-related) and reinvested into first-lien income-producing assets that should support a higher dividend payment to shareholders.

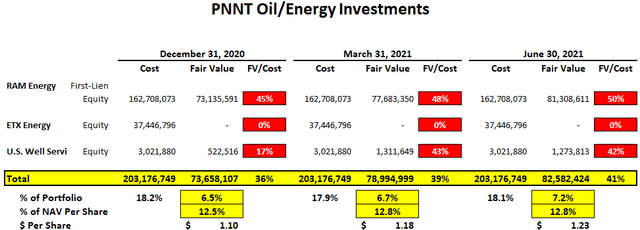

The fair value of energy, oil & gas portfolio exposure is currently around $82.6 million and now only accounts for 7.2% of the portfolio. If PNNT completely marked down its oil/energy-related investments the impact to NAV per share would be around $1.23 or 12.8%. This is more than priced into the stock that is currently trading at a ~32% discount to its NAV/book value of $9.59 per share.

Previously, PNNT recapitalized RAM Energy and converted all of its remaining debt obligations to equity. As mentioned in previous reports, both RAM and ETXhave reduced all nonessential capital expenditures, expenses and personnel. As shown below, the total expenses for RAM continue to decline and the company is now profitable:

Management discussed RAM on the recent call mentioning “we look forward to that day and we will try to optimize value and as expeditious a timeframe as possible”:

“PNNT has among its lowest percentage of energy investments since 2013. Energy investments represent only 7% of the overall portfolio. RAM is now on stable operational and financial footing and has benefited from higher prices and production. The company is free cash flow positive after debt service and plans to use any cash flow to repay debt. As of June 30, equity represented approximately 35% of the portfolio. RAM has a very well delineated acreage and 12 holes in the ground that had been very productive that’s a really good use of shareholder investor cash to buy RAM. So now everyday you’re reading the newspapers, the big companies are being very judicious and careful, they’re not drilling and they’ve got the discipline and all this other stuff. We are waiting for them to feel a little bit more expansive about doing things, whether that be drilling, whether that be M&A and we look forward to that day and we will try to optimize value and as expeditious a timeframe as possible.”

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy to digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning we provide quick updates for the sector including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on at least two BDCs each week prioritized by focusing on ‘buying opportunities’ as well as potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Friday Comparison or Baby Bond Reports – A series of updates comparing expense/return ratios, leverage, Baby Bonds, portfolio mix, with discussions of impacts to dividend coverage and risk.

![]()

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.