The following information was previously provided to subscribers of Premium BDC Reports along with:

- SUNS target prices/buying points

- SUNS risk profile, potential credit issues, and overall rankings

- SUNS dividend coverage projections (base, best, worst-case scenarios)

![]()

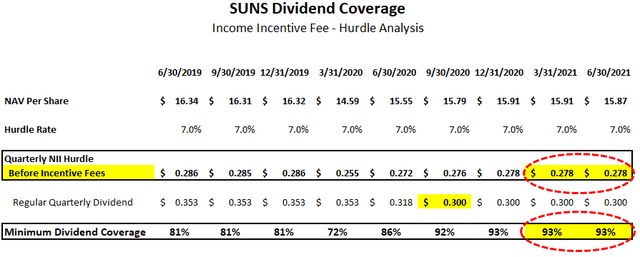

SUNS Dividend Coverage Update

On September 9, 2021, SUNS reaffirmed its monthly distribution of $0.10 per share for the month of September 2021 payable on October 1, 2021, to stockholders of record as of September 23, 2021.

The following table shows the “pre-incentive fee net investment income” per share before management earns income incentive fees based on “net assets”. SUNS will likely earn around $0.278 per share each quarter before paying management incentive fees covering around 93% which is ‘math’ driven by an annual hurdle rate of 7% on equity. As shown in the previous tables, there were no incentive fees paid for the quarter ending June 30, 2021. It is important to note that the calculation is based on the net asset values from the previous quarter.

- Please note that SUNS will likely have lower earnings per share over the coming quarters due to being underleveraged but management will not earn an incentive fee.

I am expecting improved earnings over the coming quarters mostly through increased leverage and portfolio growth as well as the recent purchase of Fast Pay Partners, a Los Angeles-based provider of asset-backed financing to digital media companies.

“SLR Business Credit acquired Fast Pay a factoring platform that provides working capital solutions to digital media firms across the U.S. led by an experienced team with a strong track record Fast Pay operates in a high growth industry and offers us an expanded product suite in geographic coverage, which should continue to fuel our growth. In conjunction with the acquisition of Fast Pay SLR business credit, amended its credit facility, increased its size, reduced its pricing and created additional flexibility. This transaction is expected to be accretive to business credits income. At quarter end, Fast Pay had a $72 million portfolio consisting of 34 our borrowers.”

It should be noted that the recent lack of portfolio growth was partially due to government stimulus programs that enabled borrowers to significantly reduce the funded balances on their revolving credit facilities. However, as these programs continue to taper off SUNS should experience increased borrowing activity driving portfolio growth:

“We anticipate meaningful portfolio growth during the second half of 2021 as we execute on our robust pipeline. Our sponsor finance business is capitalizing on increased middle-market deal volume, supported by the rebounding U.S. economy, and our specialty finance businesses are seeing greater capital needs from their borrowers as government stimulus tapers off. Utilization rates under business credit loans have been lower during COVID due to many of the borrowers benefiting from government stimulus programs, and using that liquidity to pay down our revolvers. As economic conditions continue to normalize, we expect these borrowers to redraw on our existing credit lines. Pipeline remains strong heading into the second half of the year driven both by increased utilization rates of our facilities, as well as new investment opportunities. We believe that the improved investment opportunities that expanded through SLR business credits acquisition of Fast Pay will continue to increase as companies require financing solutions for working capital and growth initiatives.”

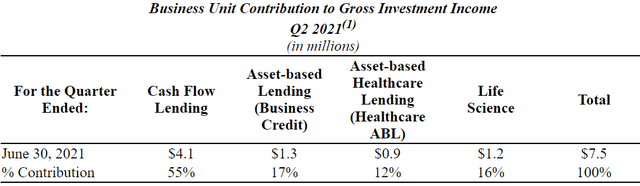

“Now let me turn to our Healthcare ABL segment. The portfolio was $73 million representing nearly 13% of our total portfolio was comprised of loans to 38 borrowers with an average investment of approximately $2 million was 100% performing and had no defaults since the start of COVID. The weighted average yield was just under 12%. In the second quarter, they funded $10 million of new investments have repayments of just over $2 million. Similar to business credit Healthcare ABL was impacted by stimulus programs that enable borrowers to significantly reduce the funded balances on their outstanding revolving credit facilities. These programs have begun to roll off which should result in our borrowers drawing more of their facilities and moving our portfolio closer to its pre-COVID size.”

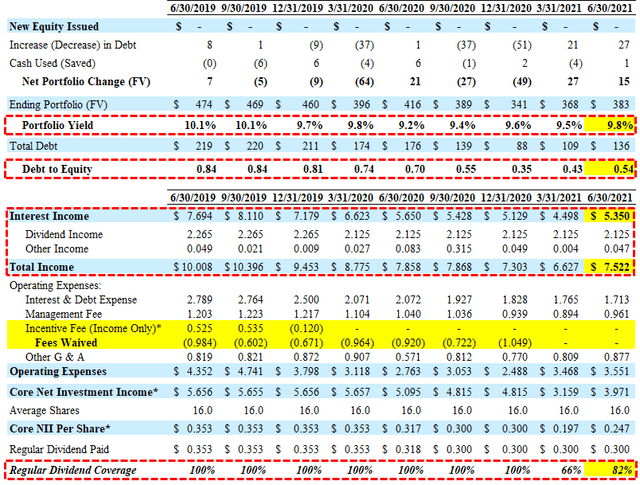

For Q2 2021, SUNS did not fully cover its dividends due to no fee waivers (same as the previous quarter) combined with being under-leveraged. However, leverage continues to increase and there was a meaningful increase in the portfolio yield.

“We are pleased with the 15% growth in SUNS’ comprehensive portfolio during the second quarter, predominantly driven by an increase in our asset-based lending verticals. Additionally, net investment income increased 25%, and we are optimistic about further earnings growth in the coming quarters.”

As mentioned in previous reports, shareholders approved the reduced asset coverage ratio allowing for higher leverage and management is targeting a range of 1.25 to 1.50 debt-to-equity.

“As a reminder SLR’s in senior’s and target leverage ratio is 1.25 times to 1.50 times net debt to equity under the reduced asset coverage requirement.” “SLR Senior Investment Corp.’s second quarter results benefited from both portfolio expansion and strong overall fundamentals. At June 30, our net debt to equity was 0.51 time, up from 0.4 times at March 31, an approximately 62% as SLR’s senior funded debt was comprised of unsecured term notes. We have over $325 million of available capital to support future earnings growth, and importantly, the economic climate has improved considerably in our pipeline across all four business verticals is very attractive. We expect portfolio growth to continue in the coming quarters from first lien cash flow, as well as asset based investment opportunities.”

SUNS remains a component in the ‘Risk Averse’ portfolio due to “true first-lien” positions diversified across cash flow, asset-based lending, and life science verticals, historically stable net asset value (“NAV”) per share, and low non-accruals. Management has a history of doing the right thing including waiving fees to cover the dividend without the need to “reach for yield” and deploying capital in a prudent manner.

Michael Gross, Co-CEO: “I’m pleased to report that SLR Senior Investment Corp’s, or SUNS, portfolio continues to be 100% performing, which continues to support our investment thesis at a diversified portfolio across asset-based loans in niche markets, in first lien cash flow loans to upper middle-market companies provides meaningful downside protection during challenging economic periods. Credit quality portfolio continues to be strong, and our watch list remains at historic lows. Approximately 57% of our portfolio was invested in asset-based and life science lending strategies and the remaining 43% was in senior secured cash flow loans. Our largest industry exposures were digital media, healthcare services, and insurance. The average investment per issue was $2.5 million or less than one half of 1%. At June 30, approximately 100% of our portfolio consisted of first lien loans with no second lien loan exposure and a de minimis amount of equity.”

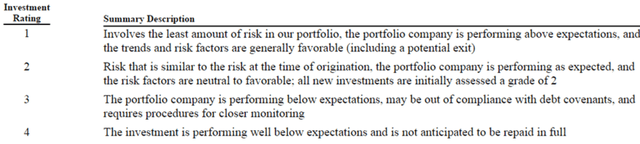

There was an increase in the amount of investments with “Internal Investment Rating 3” which are investments “performing below expectations, may be out of compliance with debt covenants” to 5.2% of investments (previously 2.2%):

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy to digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning we provide quick updates for the sector including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on at least two BDCs each week prioritized by focusing on ‘buying opportunities’ as well as potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Friday Comparison or Baby Bond Reports – A series of updates comparing expense/return ratios, leverage, Baby Bonds, portfolio mix, with discussions of impacts to dividend coverage and risk.

![]()

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.