The following information was previously provided to subscribers of Premium BDC Reports along with:

- TCPC target prices/buying points

- TCPC risk profile, potential credit issues, and overall rankings

- TCPC dividend coverage projections (base, best, worst-case scenarios)

![]()

TCPC Dividend Coverage Update

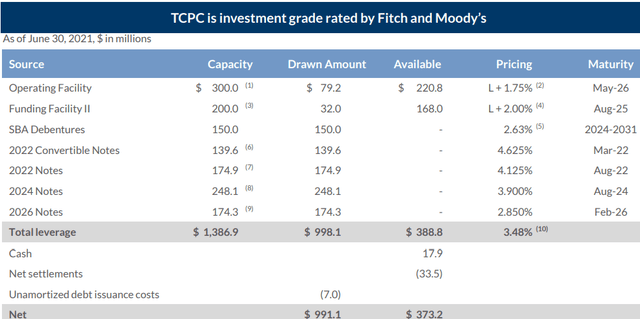

Similar to most BDCs, management continues to improve or at least maintain its net interest margin through reducing its borrowing rates including its SVCP Credit Facility reduced to L+1.75% announced on June 24, 2021, and an additional $150 million of 2.850% notes due 2026 issued on August 27, 2021, used to redeem $175 million of 4.125% notes due 2022. Both Fitch and Moody’s reaffirmed the Company’s investment-grade rating with a stable outlook.

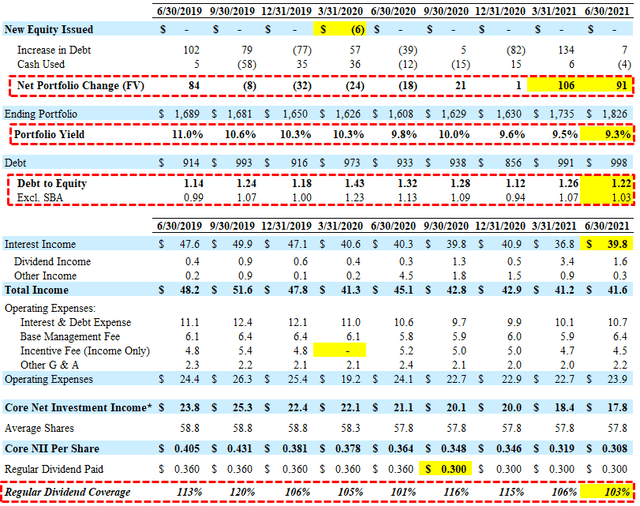

As of June 30, 2021, available liquidity was approximately $373 million, including $388 million in available capacity under its leverage program, $18 million in cash and cash equivalents, and $34 million in net outstanding settlements of investments purchased.

During Q2 2021, leverage decreased during the previous quarter and remains below its targeted debt-to-equity ratio currently at 1.03 excluding SBA debentures giving the company some cushion for upcoming portfolio growth and improved earnings.

I am expecting dividend coverage to improve over the coming quarters through continued lower borrowing rates (discussed earlier), rotation out of equity positions into income-producing debt positions (discussed next), and reduced incentive fees. As mentioned in previous reports, management was not paid an incentive fee for Q1 2020 and deferred the cost evenly over the following six quarters which added around $643,000 of additional expense each quarter. The good news is that Q3 2021 is the last quarter for these deferred expenses which is taken into account with the previous projections:

“Incentive fees related to our income from the first quarter of 2020 were deferred when our performance temporarily fell below the total return hurdle. We voluntarily deferred the amount over 6 quarters through September of this year, subject to our cumulative performance remaining above the hurdle. We believe this deferral further aligns our interest with our shareholders and demonstrates our confidence in the strength of our portfolio and its earnings capacity over time.”

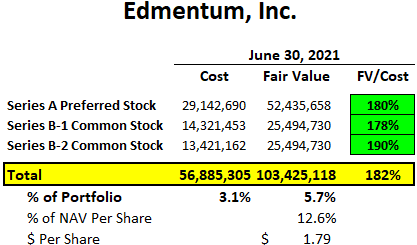

I am expecting continued dividend income including from Edmentum, Inc. (not as much as Q1 2021) which was discussed by management on the recent call:

“Dividend income in the Second Quarter included $1.1 million or $0.02 per share of recurring dividend income on our equity investment in Edmentum.”

Subsequent to June 30, 2021, TCPC sold around one-third of its equity position in Edmentum which is a good thing for shareholders as management can reinvest the proceeds into other assets with higher income. As shown in the following table, TCPC’s investment is currently valued at over $103 million and accounts for 5.7% of the portfolio. Management did not mention which shares they sold but using an average would imply proceeds of around $34 million and realized gain of around $15.5 million or $0.27 per share. It should be noted that TCPC has historical net realized losses and will not need to pay out the gains to shareholders.

Management discussed Edmentum on the recent call:

Q. “Following up on the question regarding Edmentum, can you repeat your comments there? I believe you said you had a $1.1 million of recurring income in the second quarter from that investment. Should we expect future income from Edmentum? And then how does that look regarding post-sale of a portion of your position, as well as on top of that, when you sold down a 1/3 of your position, how did that amount come about? Why was it not a full exit or why did you guys not choose to hold all? Why did you guys just right size it down to just selling off 1/3?”

A. “It is a recurring dividend income. We’re invested both in a preferred equity tranche and then the common equity as well. And as you recall, last quarter we had somewhat elevated level of dividend income, but this was more normalized recurring. But as you mentioned, we did sell down a portion of that equity position. This comes as a result of a nice run-up in the valuation, and also realized exit in part at those elevated valuations. The benefit here is we can take those proceeds and obviously redeploy it into our more normative investment profile for interest income. We do believe, obviously, as part of a sell-down, that it was important to manage the position size. Being an equity owner of a business is not the normative strategy. Doing so as a way to really fully realize the work effort and the benefits of that work and the position was part of the sell-down philosophy. We are still excited about the business. It’s well-positioned. There’s been a lot of work to get it to where it is today. I do think there are ongoing positive winds in the sails, so to speak, for the business. You have new institutional investors who have come in, as well as part of this transaction. So we want to be a part of that success on an ongoing basis, but we want to balance it with what the core part of the strategy is, as well as managing a diverse and well-diversified book with the growth in net position. And that is a combination of things that led us to partially exit, take some chips off the table, but also be a part of the future success of the business.”

Management was asked about selling some of the other equity investments on the recent call:

Q. “Just looking at the overall asset mix of the portfolio, you’ve clearly benefited from the strong performance on the equity side, and I believe equity is now 11% of assets after the event on sales. Be great if you could get a little color around how you’re thinking about, the asset mix moving forward. Do you think that we should expect to see more monetization of the equities position?”

A. “We are focused on credit instruments. It is the primary strategy where we have equity. It’s a function of either some ability to have warrants or things that convert into that or it’s a function of something like inventing somewhere. The path to defending our capital is defined by converting to a different instrument, which is really the exception, not the rule. Fortunately, those — a number of those have worked out, in some cases very well. But I would say, in terms of normal course activity, you should expect this to be a debt — primarily a senior secured debt portfolio, occasionally, things need a little bit of different type of work or activity that may result in equity, but if that is really not the primary focus, that is a function of protecting the portfolio versus deploying it in an original investment.”

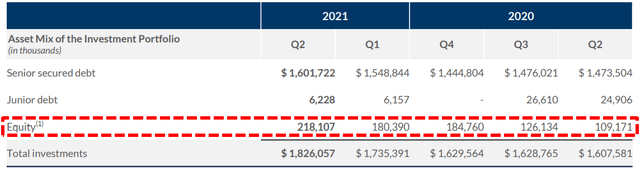

As shown below, equity investments have grown from $109 million to $218 million partially due to marking up Edmentum and accounted for around 11.9% of the portfolio as of June 30, 2021. There is a good chance that management will be monetizing some of these investments which will drive additional recurring interest income and is taken into account with the ‘best case’ financial projections shown earlier.

On a previous earnings call, management was asked about resetting the dividend higher (closer to the previous level) and mentioned the lumpy nature of fee, dividend and prepayment-related income, “investors take comfort from dividend stability” and “great pride and comfort from knowing that we’ve got good dividend coverage”. I agree but there is a chance that the amount of recurring/stable earnings could increase enough to support a higher dividend due to continued lower borrowing rates, reduced incentive fees, and rotation out of equity positions into income-producing debt positions. Again, these are taken into account with the ‘best case’ projections.

Q. “Knowing that you folks never like to do anything in a herky jerky way and having just trimmed your dividend from 36 to 30 last year for reasons that are understandable kind of in the middle of the lockdowns. And so I’m just kind of wondering, again, not for the next quarter, two or three. But just philosophically, what would you be looking forward to or is it a goal to get back to the prior distribution?”

A “So yes, we did this during the lockdown. But we were also reacting to the very significant change in LIBOR, and the math is set out. And so when we made that decision, it was really primarily looking at LIBOR as opposed to events in the portfolio. We’re very proud of having earned our dividend every quarter. We think investors take comfort from dividend stability, knowing that it’s well-earned and appropriately covered. And that’s really been our focus. I think the other thing is, as you look at our earnings, we benefited from prepayment fees. And as we discussed earlier on the call, those are lumpy. We take great pride and comfort from knowing that we’ve got good dividend coverage. But we also know that there’s a certain lumpiness to the extra earnings from additional fees, dividends and prepayments.”

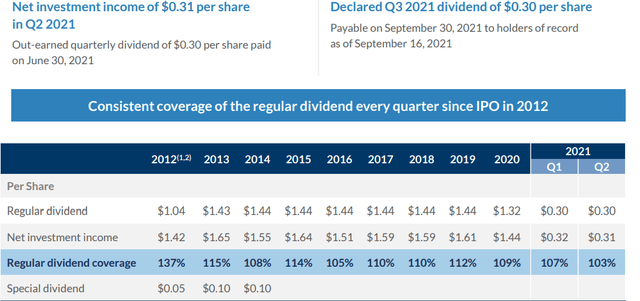

Historically, the company has consistently over-earned its dividend with undistributed taxable income. Management will likely retain the spillover income and use for reinvestment and growing NAV per share and quarterly NII rather than special dividends. On August 2, 2021, the Board declared a third quarter dividend of $0.30 per share payable on September 30, 2021, to stockholders of record as of the close of business on September 16, 2021.

For Q2 2021, TCPC reported slightly below its base-case projections due to lower-than-expected dividend and other income as well as lower portfolio yield covering its dividend by 103%. The amount of payment-in-kind (“PIK”) income continues to decline from 7.6% in Q2 2020 to 2.4% in Q2 2021 the lowest level of PIK income in three years.

“Investment income for the Second Quarter was $0.72 per share. This included recurring cash interest of $0.61, recurring discount and fee amortization of $0.03, and PIK income of $0.02. Notably, PIK income is at a lowest level in more than 3 years. As a reminder, our income recognition follows our conservative policy of generally amortizing upfront economics over the life of an investment, rather than recognizing all of it at the time the investment is made.”

On July 29, 2021, the Board re-approved its stock repurchase plan to acquire up to $50 million of common stock “at prices at certain thresholds below our net asset value per share”. There were no additional shares repurchased during Q2 2021.

Previous reports correctly predicted the reduction of TCPC’s quarterly dividend from $0.36 to $0.30 which was at the top of my estimated range of $0.28 to $0.30. At the time, the company had spillover or undistributed taxable income (“UTI”) of around $0.78 per share. However, this is typically used for temporary dividend coverage issues. Please do not rely on UTI as an indicator of a ‘safe’ dividend. The previously projected lower dividend coverage was mostly due to lower LIBOR and portfolio yield combined with management keeping lower leverage to retain its investment-grade rating. Again, the previous declines in LIBOR were mostly responsible for the decline in portfolio yield with “limited exposure to any further declines”.

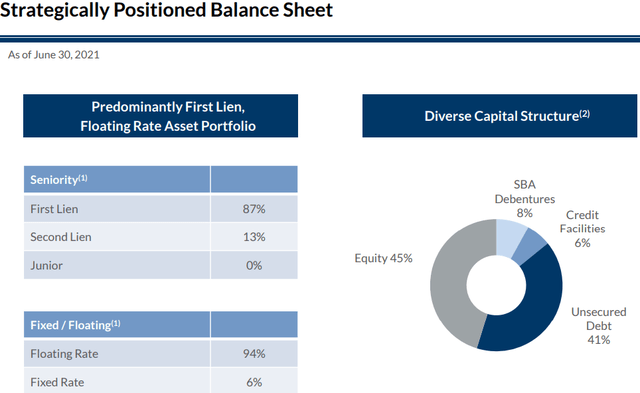

“Since 12/31/2018, LIBOR has declined 265 basis points or by 95%, which has put pressure on our overall portfolio yield. However, 87% of our floating rate loans are currently operating with LIBOR floors. And given that 94% of our loans are floating rate, we are well-positioned to benefit when rates eventually rise.”

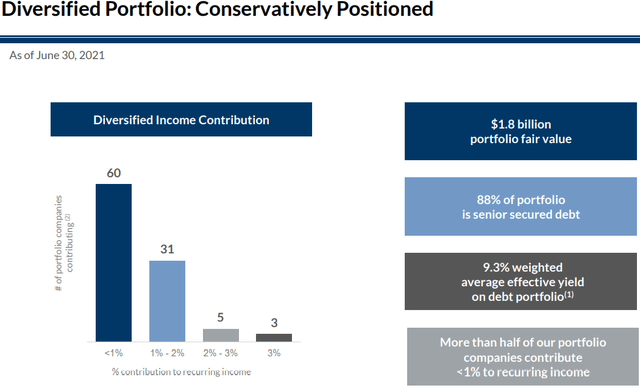

As shown below, TCPC’s portfolio is highly diversified by borrower and sector with only three portfolio companies that contribute 3% or more to dividend coverage:

“Our recurring income is spread broadly across our portfolio and is not reliant on income from any one company. In fact, over half of our portfolio companies each contribute less than 1% to our recurring income.”

TCPC Risk Profile Quick Update

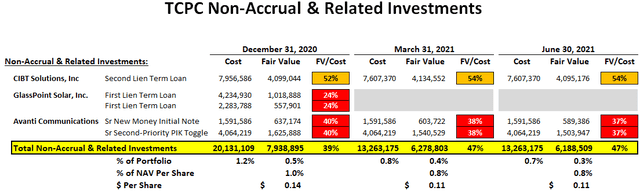

There were no additional loans added to non-accrual status that remain low representing 0.3% of the portfolio at fair value and 0.7% at cost. CIBT Solutions, Inc. remains on non-accrual status (was added during Q3 2020) and is a provider of expedited travel document processing services serving multinational corporations, global travel management companies, tour and cruise operators, government agencies, and Do-It-Yourself travelers. GlassPoint Solar, Inc. was exited during Q1 2021 and Avanti Communications remains on non-accrual. If these investments were completely written off the impact to NAV per share would be around $0.11 or 0.8%.

As discussed in the previous report, Edmentum is a provider of online learning programs that was acquired by Vistria Group resulting in a full recovery. Similar to NMFC, TCPC chose to re-invest a meaningful portion of the proceeds ($54.4 million) and “remain a significant shareholder of Edmentum, due to strong conviction in the continued growth”. As mentioned earlier, TCPC sold a third of its equity position in Edmentum and will record a realized gain in Q3 2021.

“Unrealized gains primarily reflected a $40.7 million gain on our investment in Edmentum, as a result of an additional equity investment committed to the company in the second quarter. Edmentum continues to benefit from the dramatic increase in demand for online education. Additional equity investment also resulted in the sale of approximately one-third of our investment in the Company post-quarter end. Unrealized gains in the second quarter also reflected overall spread tightening and continued market recovery, as well as improved investor sentiment following the significant market dislocation in the first half of last year, as a result of the pandemic.”

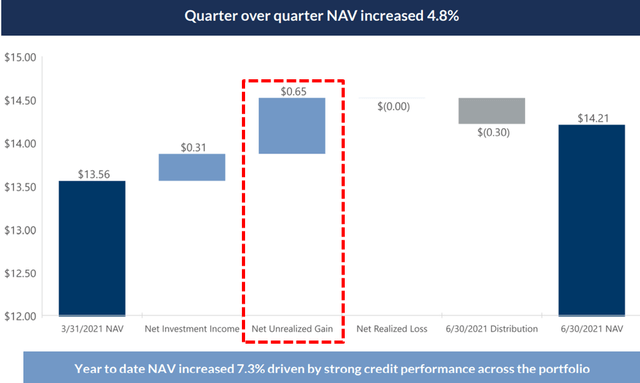

During Q2 2021, TCPC’s net asset value (“NAV”) per share increased by another $0.65 or 4.8% (from $13.56 to $14.21) primarily driven by additional gains on its investment in Edmentum (similar to previous quarters) partially offset by markdowns for Amteck and Fishbowl Inc.

“In the second quarter, our net asset value increased 4.8%, and the year-over-year, net asset value is up 16.4%. This is our fifth consecutive quarter of net asset value increases, and builds on the positive net asset value accretion we had during 2020, a result of which we are extremely proud. The increase in NAV in Q2 was primarily driven by a $41 million unrealized gain on our investment in Edmentum together with more modest increases in value across the portfolio.”

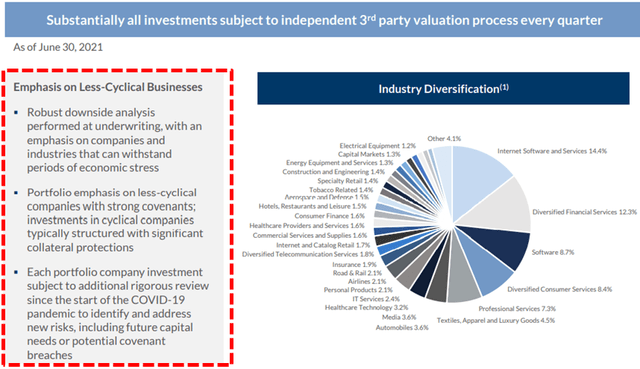

“Unrealized gains were partially offset by the reversal of $7.6 million of unrealized gains on Amtech, and $5.3 million in unrealized losses from Fishbowl. Fishbowl provides marketing software and services to restaurants, and these are only direct exposure to the restaurant industry. Given Fishbowl’s exposure to this industry, the Company has been slower to recover. Substantially, all of our investments are valued every quarter using prices provided by independent third-party sources. These include quotation services and independent valuation services, and our process is also subject to rigorous oversight, including back testing of every disposition against our valuations.”

“Our portfolio is also weighted towards companies with established business models in less cyclical industries. The portfolio remains diverse at quarter-end and was made up of investments in 108 companies. As the chart on the left side of slide 6 shows of the presentation, our recurring income is spread broadly across our portfolio and is not reliant on income from any one company. In fact, over half of our portfolio companies each contribute less than 1% to our recurring income. 87% of our debt investments are first-lien, providing significant downside protection, and 94% of our debt investments are floating rate, positioning us well for when interest rates eventually rise.”

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy to digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning we provide quick updates for the sector including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on at least two BDCs each week prioritized by focusing on ‘buying opportunities’ as well as potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Friday Comparison or Baby Bond Reports – A series of updates comparing expense/return ratios, leverage, Baby Bonds, portfolio mix, with discussions of impacts to dividend coverage and risk.

![]()

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.