The following information was previously provided to subscribers of Premium BDC Reports along with:

- TPVG target prices/buying points

- TPVG risk profile, potential credit issues, and overall rankings. Please see BDC Risk Profiles for additional details.

- TPVG dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

![]()

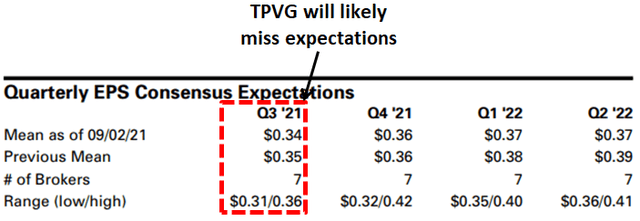

TPVG Potential Earnings Miss for Q3 2021

There is a chance that TPVG will miss upcoming earnings expectations for Q3 2021 due to the following which are taken into account with the updated projections and discussed later in this report:

- Lower prepayment-related income.

- Previous lower leverage and underinvested portfolio.

- Underutilization of its lower cost credit facility resulting in higher “unused fees” and higher blended borrowing rates.

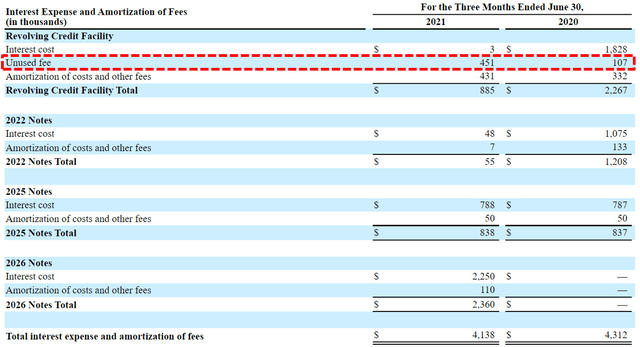

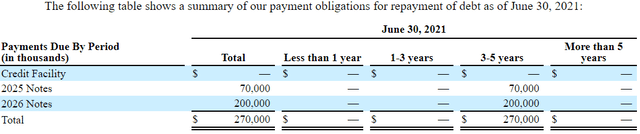

As shown below, TPVG paid $451,000 of unused credit facility fees in Q2 2021 which impacted earnings by around $0.015 per share. As the company uses higher leverage by utilizing the lower cost credit facility it will have a meaningful impact on earnings through portfolio growth and lower fees.

Given the current market with increased merger/SPAC activity, I am expecting TPVG to continue to be underleveraged, supporting the regular dividend using the previous spillover, and less likely to pay a supplemental in 2021.

“As you can see there hasn’t been a slowdown in exit activity within our portfolio, in fact, we continue to have more than it does in TPVG portfolio companies actively exploring IPOs, SPAC mergers or M&A which if consummated could unlock substantial additional value for our shareholders from our equity and warrant portfolio.”

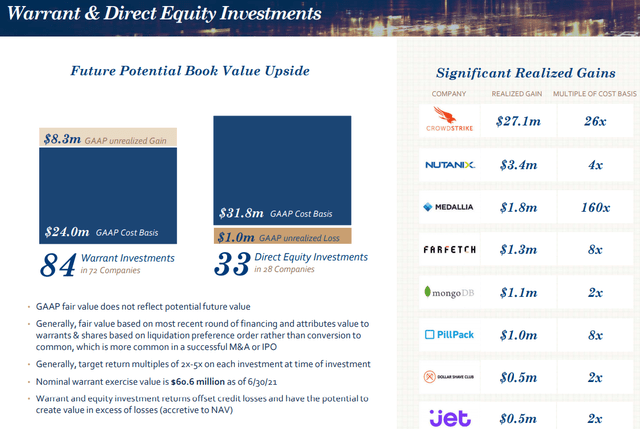

Of course, there is always a good chance that there will be some significant realized gains from many of its equity positions but these would likely be used to pay additional supplemental dividends in 2022. On the recent earnings call management mentioned continued gains from its equity/warrant positions including Revolut Ltd as discussed later that will likely drive an increase in NAV per share for Q3 2021:

“Although we have not completed our fair value process for Q3 we estimate TPVG’s equity and warrant investments to be valued between $10 million and $20 million, up from $1.8 million as of Q2 or an increase between $0.25 and $0.60 per share to net asset value. While still unrealized realized gains, this is another great development in the TPVG portfolio, but more importantly, not the only one that we believe will deliver meaningful gains as we have many portfolio companies and our heads down and doing great things. Clearly, we are excited by the outlook for both unrealized and realized gains on the equity and warrant portfolio which position us to provide shareholders with capital gains and to grow net asset value but we’re also pleased with the solid credit outlook and the strong yield profile for the portfolio.”

“During the second quarter, we also received warrants valued at $2.2 million in seven portfolio companies in conjunction with our debt commitments as compared to receiving warrants valued at $1.6 million in 13 companies last quarter. This increase demonstrates that we are capturing more equity upside potential from our portfolio companies, while still raising the bar on yield. During the quarter, Talkspace completed their SPAC merger and as at the end of the quarter, we have a total unrealized gain of 600,000 based on our warrant and equity positions in the company even though the company never drew on their deadline and there unfunded commitment expired, unused. This brings TPVG’s totaled to three successfully completed SPAC mergers, we also have five portfolio companies with the announced SPAC mergers and process. Bird, Enjoy, Inspur auto, and Sonder all announced their SPAC in Q2, and live learning technologies announced its back during the first quarter. Our cost basis in equity and warrants in these five companies totals $1.7 million with a fair value of $3 million as of Q2. Generally, we do not mark up our investments in these type of situations until merger exchange ratios are announced. And then we further discount the fair values given the uncertainty associated with their completion.”

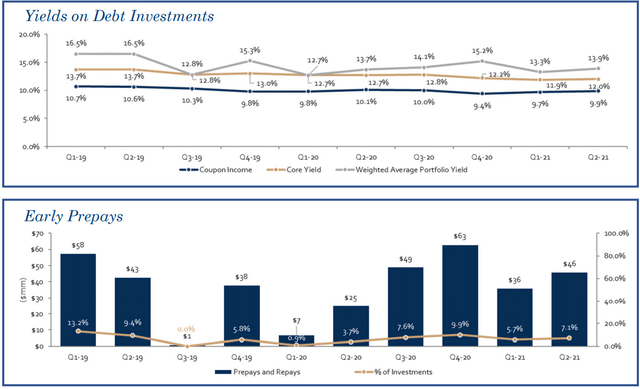

As discussed in previous reports, TPVG’s dividend coverage needs to be assessed on an annual basis due to the lumpy nature of earnings from successful portfolio companies prepaying loans. This results in certain periods of higher prepayment fees driving higher earnings often followed by lower earnings due to being underleveraged and not having a fully invested portfolio.

Previous call: “I would like to remind everyone that while prepayments are a natural part of our venture lending model, it does come with a great deal of uncertainty. One of the other aspects of prepayment activity is that the origination vintage of alone that prepays really does matter. Given the nature of income acceleration when a loan prepays, the characteristics of income changes, the longer the loan remains outstanding, for example, should alone repay or prepay in its first year, we would generally recognize a comparatively higher level of income.”

This is what happened in Q1/Q2 2021 driving interest income well below previous levels as the company continues to experience higher repayments (mostly due to investing in successful portfolio companies) but not as much prepayment-related income resulting in reduced dividend coverage mostly due to “lower weighted average principal outstanding on our income-bearing debt investment portfolio”.

“Our earnings were impacted by the significant prepay activity we’ve experienced over the past several quarters on our overall portfolio size, despite strong new commitments, growing investment funding and stable core portfolio yield is in the past. We believe any shortfall is temporary and will be more than made up during the rest of the year as the fundamentals of our industry.”

As of June 30, 2021, the company’s unfunded commitments totaled $163.5 million and through August 4, 2021, had closed $15.7 million of additional debt commitments, funded $18.2 million in new investments offset by $18.2 million of prepayments driving $0.4 million of accelerated income. However, management is expecting lower prepayments combined with a strong pipeline of new investments and signed term sheets that should drive portfolio growth in Q3/Q4 2021 taken into account with the updated projections.

“As we look to the second half of this year in terms of prepayment activity from our core equity raises we’re seeing a little more balance from portfolio companies that are fundraising or that are closing fund-raises, they’re either waiting to pay off the debt, they’re either not paying off the debt or we’re talking with them about creative ways to keep the debt outstanding which we think will then translate into meaningful portfolio growth. Our large pipeline strong levels of signed term sheets increasing commitment growth, higher utilization rates, and meaningful levels of unfunded commitments are great indicators for near-term portfolio growth, which we believe will enable us to cover the distribution on a quarterly basis this year, but we’re not going to force portfolio growth unnaturally.”

“The most notable progress is a continued rise we are seeing in signed term sheets, which was one of the highest quarterly totals in TPVG’s history. Additionally, our pipeline increased 50% over last quarter and is more than doubled since a year ago. We have substantial liquidity to meet this increased demand and we’re on course to achieve the growth targets we outlined for the second half of the year and drive consistent long-term growth of investment income in net asset value. So far we have funded over $18 million of new loans here in the third quarter. Consistent with prior guidance, we expect gross fundings for Q3 and Q4 to come in between $100 million and $150 million per quarter, which is supported by our pipeline, our backlog of signed term sheets, high utilization rates of new commitments at close, sizable unfunded commitments as well as the pattern of our portfolio companies drawing on existing unfunded commitments towards the second half of the year.”

Q. “In your comments, did you say that you expect the quarterly EPS to cover the dividend in the second half?”

A. “I didn’t say that. What I was what our trend will be is to originate to get to a level where it’s sustainable. So, we clearly need to get to the $100 million, $150 million in the third and fourth quarter. And then we’re on track for doing that.”

Last month, the Board reaffirmed its quarterly distribution of $0.36 per share for Q3 2021, and dividend coverage will continue to improve partially due to the recent/previous reductions in borrowing rates as well as growing the portfolio using leverage from its credit facility.

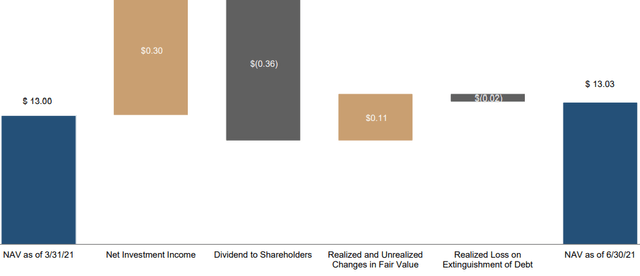

“During the second quarter, the company recorded a one-time $681,000 or $0.02 per share net realized loss on extinguishment of debt. This was the result of the full redemption on April 5th of our baby bonds. With this redemption complete, we expect a positive effect to earnings as we continue to lower our cost of capital going forward.”

“The most notable progress is a continued rise we are seeing in signed term sheets, which was one of the highest quarterly totals in TPVG’s history. Additionally, our pipeline increased 50% over last quarter and is more than doubled since a year ago. We have substantial liquidity to meet this increased demand and we’re on course to achieve the growth targets we outlined for the second half of the year and drive consistent long-term growth of investment income in net asset value.”

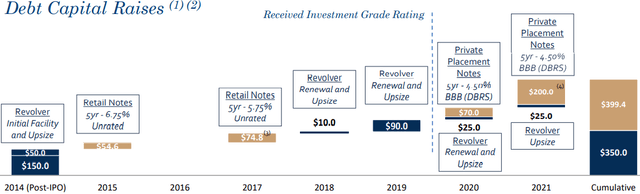

On March 1, 2021, TPVG closed a private offering of $200 million 4.50% institutional unsecured notes due 2026, and used a portion of the proceeds to redeem its 5.75% Baby Bond (TPVY) lowering its overall borrowing rates. Leverage remains low due to previous early repayments driving a debt-to-equity ratio of 0.59 net of cash giving the company plenty of growth liquidity. It should be noted that TPVG is one of the only BDCs currently with 100% unsecured borrowings giving the company much more flexibility over the coming quarters:

TPVG Risk Profile Quick Update

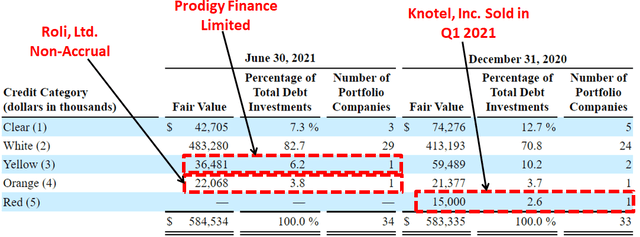

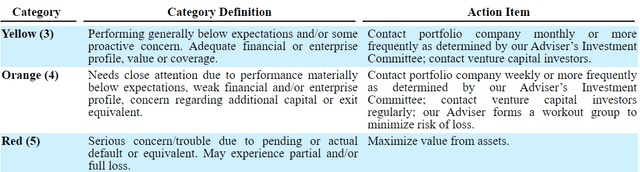

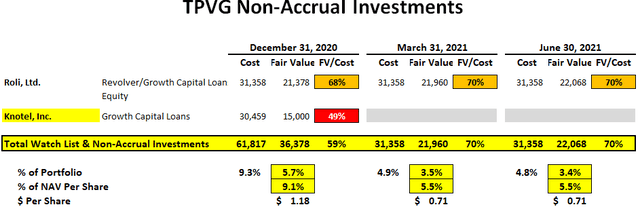

TPVG maintains a credit watch list with portfolio companies placed into one of five categories, with Clear, or 1, being the highest rating and Red, or 5, being the lowest. Generally, all new loans receive an initial grade of White, or 2. Knotel was its only Red (5) and was sold during Q1 2021, Roli, Ltd. is its only Orange (4) and remains on non-accrual status, and Prodigy Finance Limited is its only Yellow (3) and needs to be watched. Please see the description of categories and discussion of Prodigy and Roli below.

“Moving on to credit quality, the credit outlook for our portfolio remains strong with 90% of our debt investments in our top two categories, consistent with Q1, no obligor’s were added to categories, three, four and five, and no obligor’s were placed on non-accrual during the second quarter. In fact, the weighted average investment ranking of our debt investment portfolio improved to 2.06 compared to 2.11 as at the end of Q1. During the quarter, one company was upgraded from category 3 to category 2 as a result of completing a financing, leaving only one company in category 3 which is Prodigy finance in international graduate student lending company. During Q2 Prodigy paid down $5 million on outstanding loans to us and we’re pleased to report that here in Q3, Prodigy completed its first securitization issuing $228 million of investment-grade asset-backed securities and are remaining loans will now switch from PIK interest to cash pay interest. Based on these and other developments that Prodigy, we expect to upgrade them to category 2 here in Q3. Our one category 4 portfolio company really continues to be our only loan on non-accrual and our mark was flat with last quarter prior to currency fluctuations.”

Roli, Ltd. was discussed on a previous call:

“If you look at the value accreted quarter-over-quarter for ROLI, so it’s not out of the woods, but if you’ve seen some very favorable product reviews, and some awards that they won for their product in Q4. So we continue to be balanced, but we feel again, conditions continued to improve at ROLI.”

Revolut Ltd announced the closing of an $800 million private equity raise at a $33 billion valuation driving an estimated fair value range of TPVG’s equity and warrant investments of approximately $10 million to $20 million, up from a combined fair value of $1.8 million at June 30, 2021. As mentioned earlier this will likely drive an increase in NAV per share for Q3 2021:

“Revolut, as an example, recently announced the closing of an $800 million equity round at a $33 billion valuation. Positive trends and our excitement in these technology sectors, if you can’t tell, continues. We foresee substantial equity fundraising activity in the venture capital industry as a whole and within our portfolio in particular. It’s a testament to our portfolio’s quality. We believe future venture lending opportunities are large and plentiful given today’s environment. This robust industry-wide equity financing activity continues to create demand for debt to compliment or top off an equity raise in some cases. “Although we have not completed our fair value process for Q3 we estimate TPVG’s equity and warrant investments to be valued between $10 million and $20 million, up from $1.8 million as of Q2 or an increase between $0.25 and $0.60 per share to net asset value.”

During Q2 2021, Bird Rides, Inc., Enjoy, Inc., Inspirato LLC and Sonder, Inc. announced plans to go public through SPAC mergers and Groop Internet Platform, Inc. (Talkspace) closed its SPAC merger.

During Q1 2021, Hims & Hers, Inc. and View, Inc. closed their SPAC mergers and GROOP Internet Platform, and Live Learning Technologies announced plans to go public through SPAC mergers.

For Q2 2021, TPVG’s net asset value (“NAV”) per share increased slightly by 0.2% mostly due to portfolio unrealized gains partially offset by losses related to redeeming its Baby Bond as discussed earlier as well as under-earning the dividend.

“Net unrealized gains on investments for the second quarter were $3.2 million or $0.10 per share, resulting primarily from favorable fair value adjustments on debt investments of $1.9 million on warrant and equity investments of $800,000 and favorable changes in foreign exchange rates of $500,000. During the second quarter, the company recorded a one-time $681,000 or $0.02 per share net realized loss on extinguishment of debt. This was the result of the full redemption on April 5th of our baby bonds.”

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy to digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning we provide quick updates for the sector including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on at least two BDCs each week prioritized by focusing on ‘buying opportunities’ as well as potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Friday Comparison or Baby Bond Reports – A series of updates comparing expense/return ratios, leverage, Baby Bonds, portfolio mix, with discussions of impacts to dividend coverage and risk.

![]()

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying including setting target prices using the portfolio detail shown in this article (at a minimum) as well as financial dividend coverage projections over the next three quarters as discussed earlier.