The following is from the CSWC Deep Dive that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

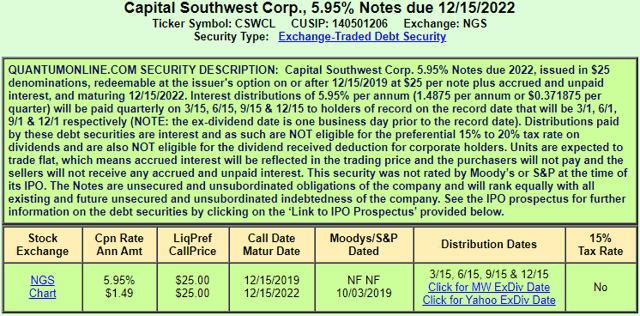

This update discusses Capital Southwest (CSWC) and its Baby Bond that trades publicly on the NASDAQ under the symbol “CSWCL”.

Capital Southwest 5.95% Notes due 12/15/2022 (CSWCL):

There is a good chance that the company will be redeeming its Baby Bond and are currently listed as a “Sell” in the BDC Google Sheets. Management discussed reducing its borrowing costs by potentially redeeming CSWCL in December 2019:

“I think that we will look to see if there is opportunistic capital raises on the debt side to take out the older version of the bonds that are at 5.95%. I don’t think there’s anything in a foreseeable future. But if the call period does end in December of this year, so if there is an opportunity to reduce cost and extend the maturity, we certainly will look like that on the fixed rate side.”

CSWC Dividend Coverage Discussion

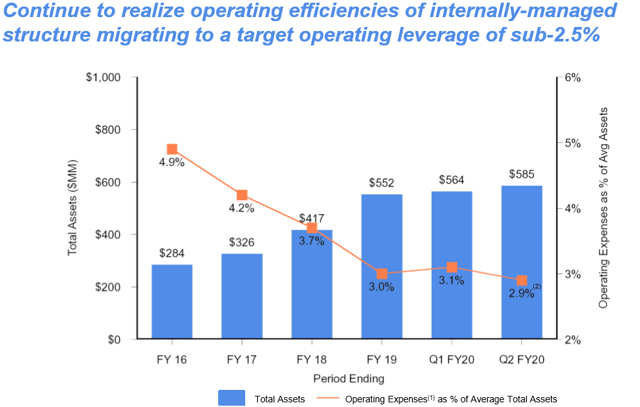

CSWC has the ability to leverage its internally managed cost structure combined with a history of stable portfolio credit quality that delivers a consistent and growing stream of recurring cash interest income with the potential for increased earnings through higher leverage and its I-45 Senior Loan Fund.

“Our operating leverage, which as of the end of the quarter was 2.9%. Excluding the aforementioned onetime deferred offering cost write off, our run rate operating leverage for the quarter would have been approximately 2.6%, which puts us near our initial target operating leverage of 2.5%. We are fully committed to actively managing our operating costs in lockstep with portfolio growth and will now set our sights on our longer term goal of achieving target operating leverage of 2% or better. With senior professionals and corporate infrastructure largely in place, operating leverage should continue to improve as the investment portfolio grows due to our internally managed structure.”

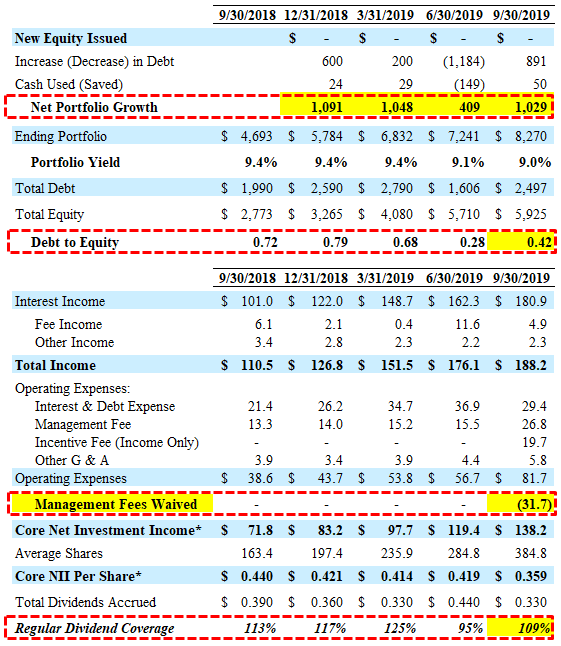

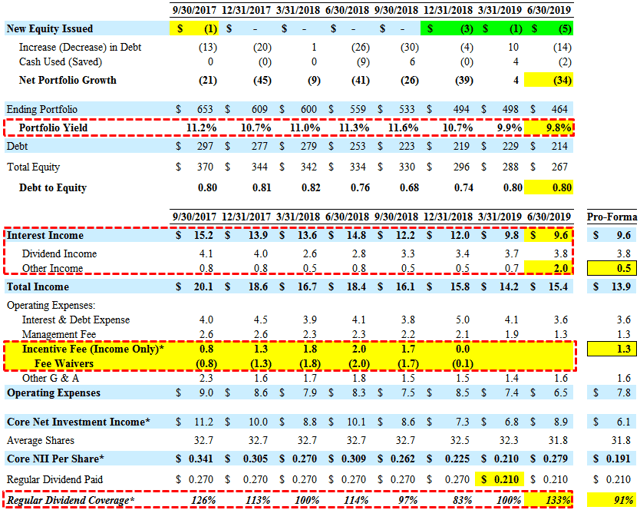

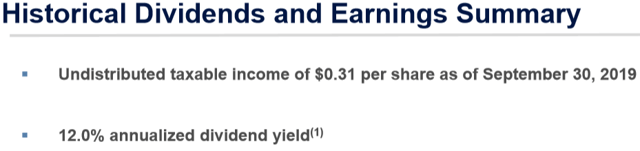

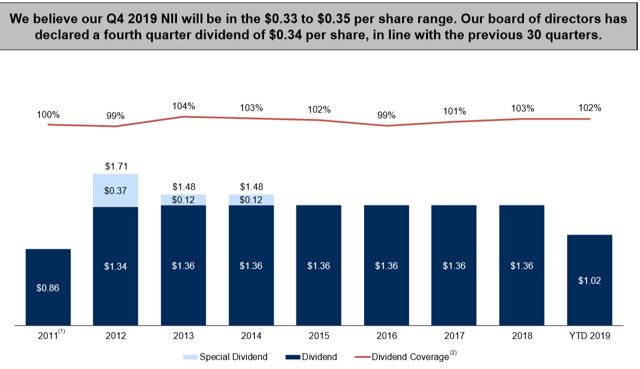

However, for the first quarter in the last four years, the company did not increase its regular quarterly dividend (discussed next) but will continue to pay its $0.10 per share supplemental dividends. CSWC had undistributed taxable income generated by excess income and capital gains accumulated through September 30, 2019, of over $18 million or $1.02 per share which is used to fund its supplemental dividends.

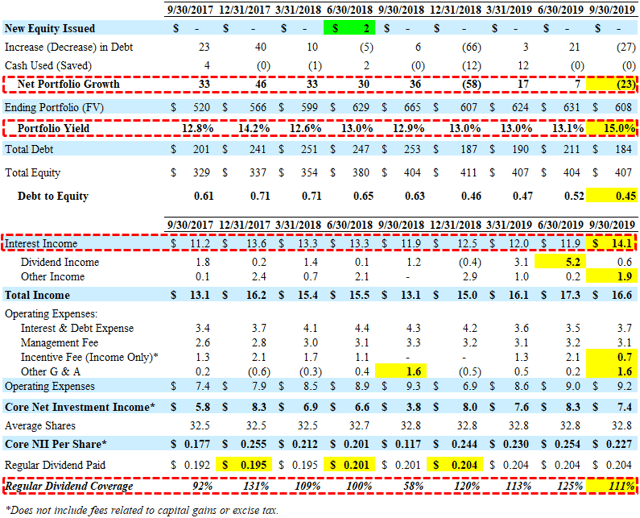

“We paid out our regular dividend during the quarter of $0.40 per share, achieving a 105% dividend coverage on pre-tax net investment income per share. Additionally we distributed $0.10 per share through our supplemental dividend program, funded by our sizable undistributed taxable income balance or UTI, which was generated by excess income and capital gains accumulated from our investment strategy to date. As of September 30 2019, we had approximately $18.3 million or $1.02 per share in UTI, providing visibility to continuing the quarterly supplemental dividend program well into the future.”

Management discussed the rate of future regular dividend increases that will likely be slower due to the timing of portfolio growth and the upcoming repayment Media Recovery, Inc. (“MRI”):

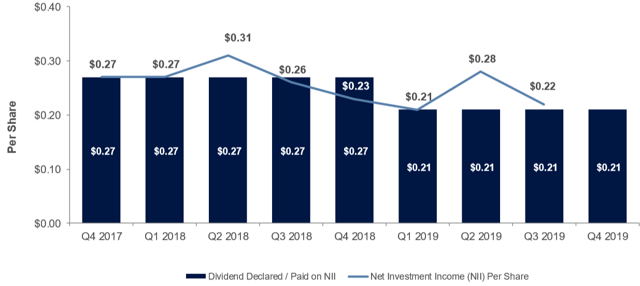

“We look at recurring income and a run rate of net investment income going forward. So this quarter, I think, we posted our number. We look at the $0.03 of expense that was incurred as a onetime, and we’d add that back to our run rates. So really our NII for the period was $0.45 So I’d tell you, going forward, we think our run rate of NII is certainly in — above the level of our dividend. We probably are going to be slowing the dividend pace as we just announced $0.40 for this current quarter. And then also has to do with our expectations potentially for MRI in the future as well.”

“So we look at all of that and we try to set a dividend at a level that is a level that frankly shareholders can rely on going forward and then will increase as our portfolio grows as it should, based on where we are in a leverage level, based on the liquidity we have available to us and our cash and credit facility availability. It’s just a matter of we need to go find the deals that are good deals. So we’ve never really been in a rush to grow portfolio or increase dividends or earnings. We want to hustle to find the deals, find the opportunities and be very diligent and careful and thoughtful and actually which ones we close. If that makes sense. It may stabilize for the moment as we absorb the capital we just received, as well as the potential for an MRI exit, but we would definitely to tell you that we expect that the dividend to grow as we redeploy capital.”

I am expecting strong portfolio growth in calendar Q4 2019 as guided by management and taken into account with the updated projections:

“Subsequent to quarter-end, we have originated $33 million in new commitments to two new portfolio companies. This included $30 million in first lien senior secured debt, $2.5 million in an unfunded revolving credit facility and $1 million in an equity co-investment. We are pleased with the pipeline as it stands today and expect that two or three additional deals currently in diligence should close by calendar year-end.”

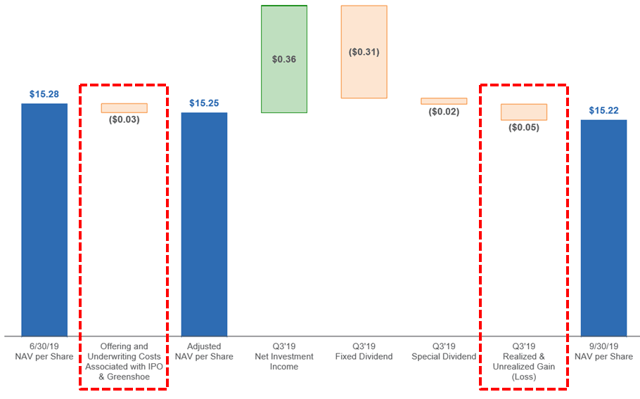

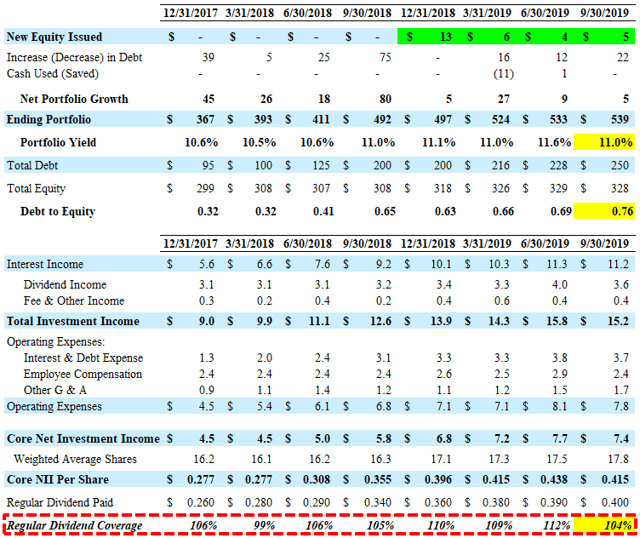

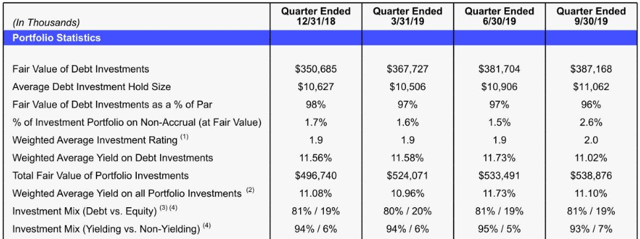

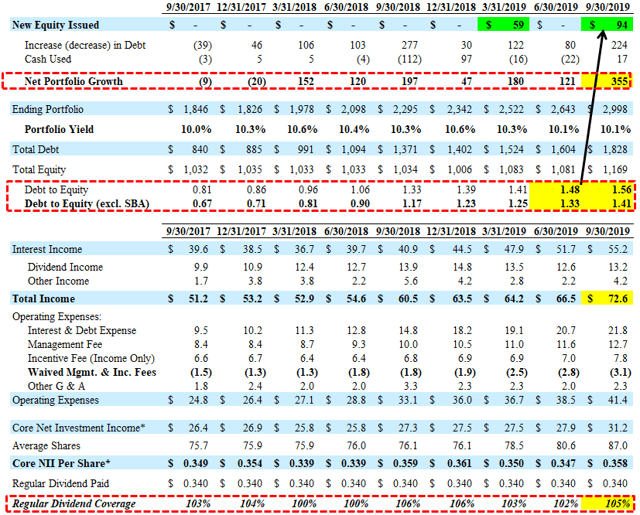

For calendar Q3 2019, Capital Southwest (CSWC) beat its base-case projections with a decline in portfolio yield closer to previous levels and covered its increased dividend by 104% even after taking into account $0.03 per share of one-time expenses.

“We are pleased with our results this quarter, having posted a solid $0.42 per share in Net Investment Income despite incurring a $472,000, or $0.03 per share, one-time expense to retire our previous registration statement.”

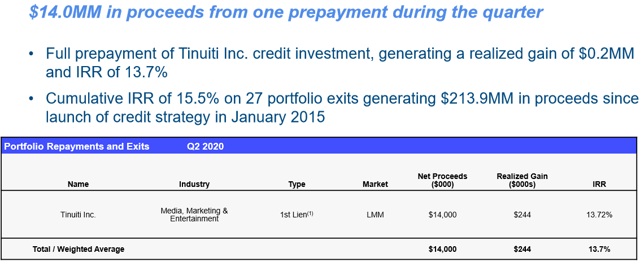

Similar to MAIN, the supplemental dividends are typically covered by realized capital gains and over-earning the regular dividend. CSWC had net realized gains of $0.3 million during calendar Q3 2019 mostly related to the $14 million prepayment of Tinuiti Inc.

“As shown on slide 12, we also had a full prepayment of one credit investment during the quarter for $14 million in total proceeds, generating a realized gain of $244,000 and an IRR of 13.7% on total invested capital.”

—————–

Its regular quarterly dividends are covered mostly through recurring cash sources:

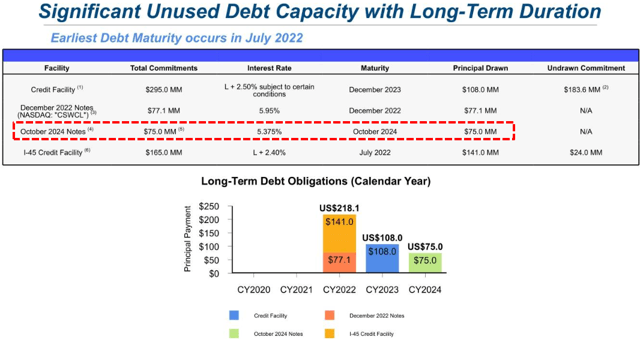

In September 2019, the company issued $65 million in 5.375% Notes due 2024 and on October 8, 2019, the Company issued an additional $10 million of the October 2024 Notes. As of September 30, 2019, CSWC had $30 million in unrestricted cash and almost $184 million in available borrowings under its credit facility for upcoming portfolio growth.

“From a capitalization standpoint, we further solidified our balance sheet by raising $75 million in an all institutionally-placed bond offering at an attractive yield of 5.375% with a 5-year maturity. The bond transaction was a unique one in the BDC space, as we believe that we are the only BDC in recent history with sub $1 billion in market cap to be able to access this market.”

“In addition, we raised $5 million in gross proceeds through our equity ATM program during the quarter, selling over 231,000 shares at a weighted average price of $21.62 per share, representing a 16% premium to book value. I am pleased to report that since the initiation of our equity ATM program, Capital Southwest has sold almost 700,000 shares at similar premiums to book value, raising approximately $15 million in gross proceeds. Our equity ATM program continues to provide a steady flow of equity capital raised on a just-in-time basis and lockstep with our ability to thoughtfully put the capital to work.”

On March 4, 2019, CSWC established its equity “At-The-Market” (“ATM”) program of slowly issuing small amounts of shares at a premium to book value/NAV and accretive to shareholders. During calendar Q3 2019, the company sold 231,272 shares of its common stock under the ATM program at a weighted-average price of $21.62 per share (~16% premium to previous NAV), raising $5 million of net proceeds after commissions to the sales agents on shares sold. Management will likely continue to use the ATM program for raising equity capital, rather than larger equity offerings. This approach is beneficial for many reasons including being more efficient, delivering higher net proceeds to the company and less disruptive to market pricing.

“We believe our equity ATM program is a prudent and cost-effective way to issue equity over time at tight spreads to the latest trade, while selling equity on a just-in-time basis so it can be thoughtfully invested in income generating assets. We certainly intend to do that by growing the portfolio, but we want to be, and we use the word prudent, we want to be prudent and diligent of raising kind of on a just-in-time basis and certain amount of equity, again, allowing us to get to target leverage in a reasonable timeframe, but being diligent about being in on a just-in-time basis. ”

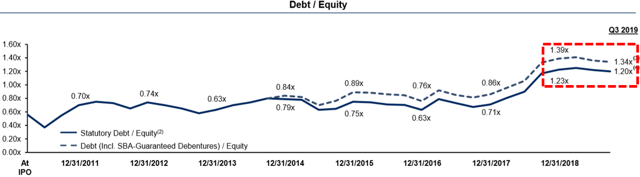

On May 23, 2019, the company announced the expansion of total commitments under its revolving credit facility from $270 million to $295 million. The increase was executed under the accordion feature which allows for an increase up to $350 million in total commitments. On April 25, 2018, the Board of Directors unanimously approved the application of the modified asset coverage requirements and the minimum asset coverage ratio applicable to the company was decreased from 200% to 150%, which became effective April 25, 2019. Management is targeting a debt-to-equity ratio between 1.00 and 1.20.

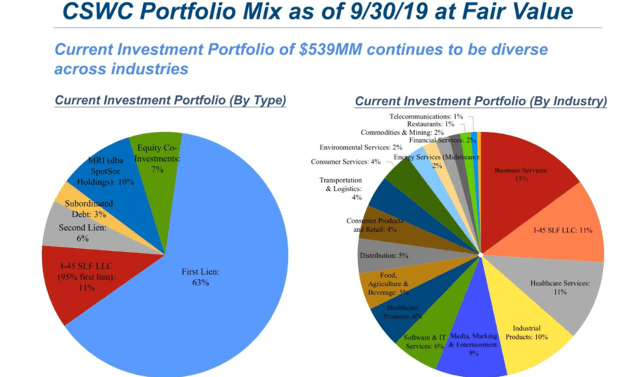

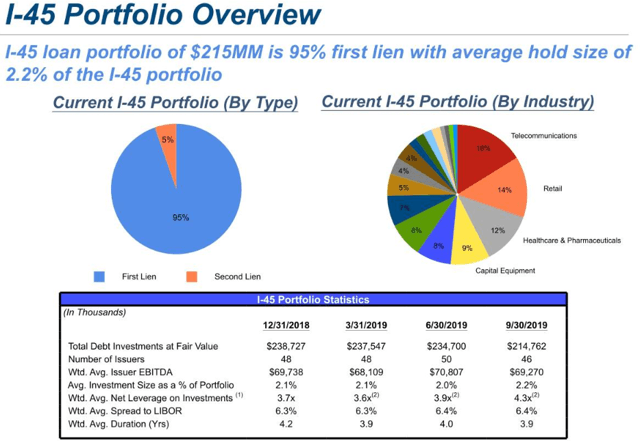

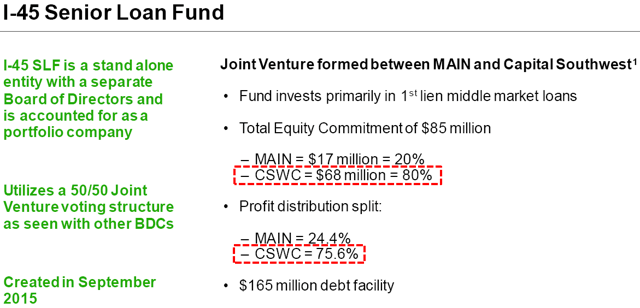

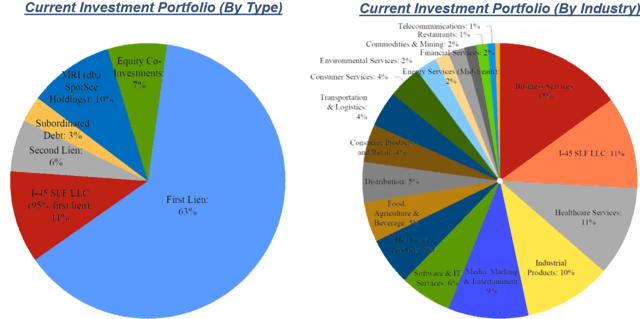

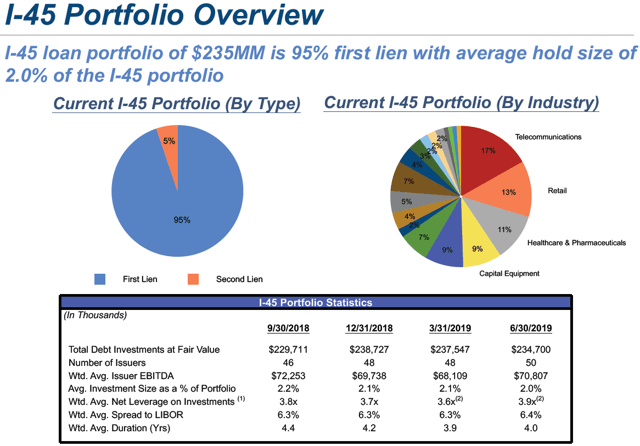

Its I-45 Senior Loan Fund accounts for 11% of the portfolio (previously 12%) and is a joint venture with MAIN created in September 2015. The portfolio is 95% invested in first-lien assets with CSWC receiving over 75% of the profits providing 16% annualized yield:

“Our I-45 senior loan fund provided dividends to Capital Southwest, representing a 16% annualized yield at fair value on our capital in the fund for the quarter.”

From previous call: “Overall, we have been pleased with the solid performance of I-45 over the past 3.5 years. We and our partner in I-45, Main Street Capital, have invested approximately $500 million through the fund and have harvested 50 exits generating $196 million in proceeds at a weighted average IRR our on the exit for the 11.4%. Our senior loan fund, I-45 also continued its solid performance producing a 15% annualized yield on our capital in the fund for the quarter.”

CSWC Risk Profile Update

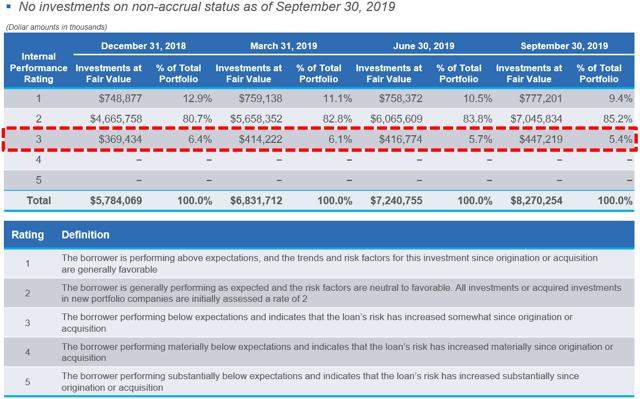

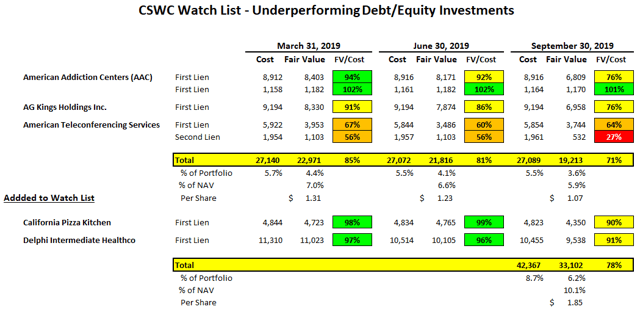

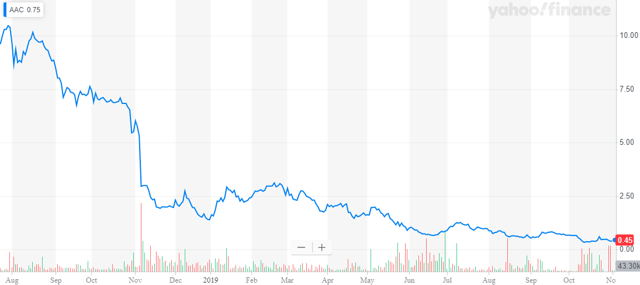

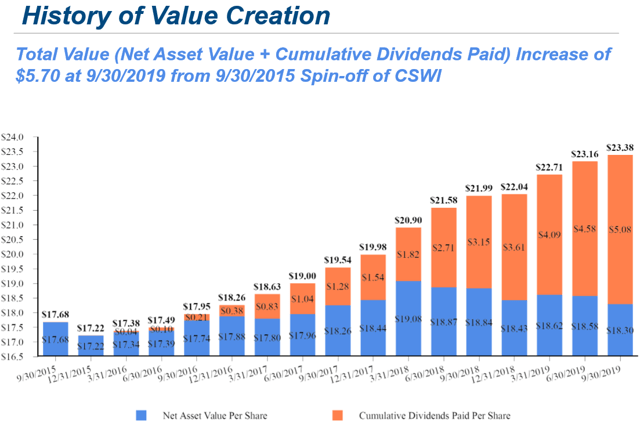

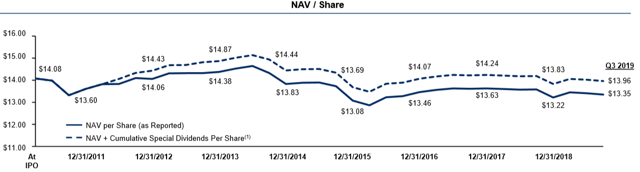

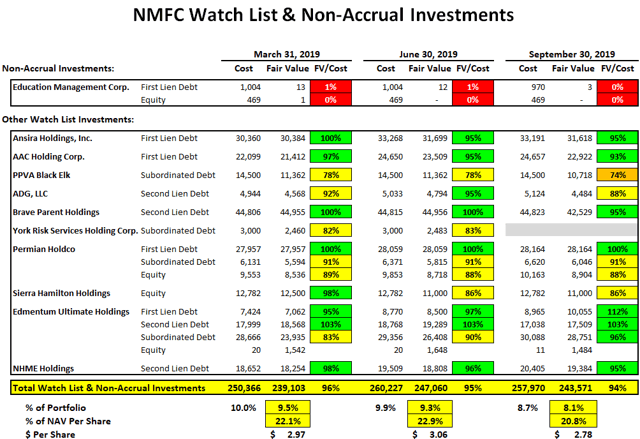

As mentioned in the previous report, my primary credit concerns for CSWC’s portfolio include its positions in AG Kings Holdings Inc., American Addiction Centers (AAC), and American Teleconferencing Services. During calendar Q3 2019, its net asset value (“NAV”) per share declined by $0.28 or 1.5% partially due to markdowns in these investments.

Also, there were markdowns in California Pizza Kitchen and Delphi Intermediate Healthco that have been added to the watch list that now accounts for around 6.2% of the portfolio fair value and 10.1% of NAV per share. Management discussed Delphi on the recent call:

“We’ve got another company Delphi that we made a three this quarter. It’s also in the behavioral health space in the upper middle market. But if you look at that — I think I attribute it mainly more of the structures and the quote dynamic in the upper middle market would be how I would see — how I’d react to that divergency you referenced.”

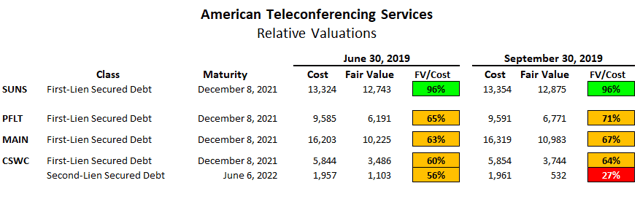

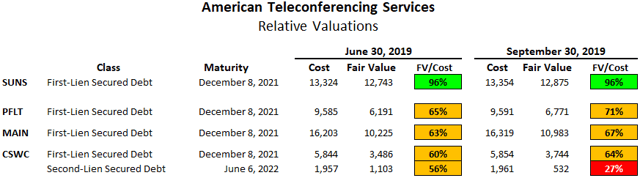

American Teleconferencing Services, Ltd. (“ATS”) is an investment also held by MAIN, PFLT and SUNS that operates as a subsidiary of Premiere Global Services (“PGi”), offering conference call and group communication services. As shown in the previous and following tables, the second-lien portion of ATS was marked down again during calendar Q3 2019. On January 28, 2019, Moody’s downgraded PGi’s debt to Caa2.

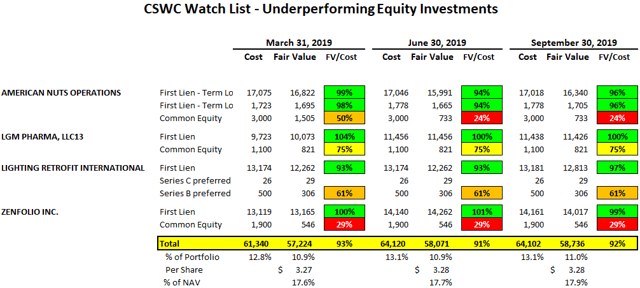

Another concern is additional unrealized losses from companies with equity positions that have been previously marked down including American Nuts which is an importer, mixer, roaster, and packager of bulk nuts, LGM Pharma, Lighting Retrofit International, and Zenfolio, Inc. These investments account for 11% of the portfolio and almost 18% of NAV per share and need to be watched.

The largest markdown during calendar Q3 2019 was American Addiction Centers which was added to non-accrual status and is a subsidiary of AAC Holdings, Inc. (AAC) to which CSWC has invested $8.9 million marked down to $8.2 million. On June 14, 2019, Michael Nanko, President and Chief Operating Officer of AAC resigned from his positions according to an AAC filing with the SEC. Mr. Nanko leaves AAC one month after CEO Michael Cartwright and CFO Andrew McWilliams conducted a call with investors to map out a 10-year strategy for the company to reverse a slide that began in 2015. On July 1, 2019, AAC submitted a plan to the NYSE regarding the company’s efforts to improve its total market capitalization, following notice on May 17, 2019 from the NYSE that its stock was at risk of being delisted as its average market capitalization was less than the required $50 million over a 30-day trading period.

AAC received waiver defaults to remain operating but needs to improve its positive cash flows/EBITDA to avoid a bankruptcy/restructuring. CSWC management discussed its investment in AAC on the recent call:

“With respect to American Addiction, the company continues to have challenges. As in prior quarters, due to being a public company, we want to be careful not to effectively announce developments prior to the American Addiction management team appropriately communicating to their shareholders. What we will say is that the lender group continues to work with the company on solutions to the capital structure. The company’s lending — leading market position in the substance abuse industry, the company’s cost savings and business development initiatives and its large owned real estate portfolio, all provide reasons to remain optimistic on the prospects of a favorable resolution. American Addiction was placed on non-accrual this quarter and remains rated 3 on our internal rating system.”

However, there is a good chance that AAC will be selling its real estate assets to avoid bankruptcy and is likely why CSWC has only slightly marked down its first-lien loan. AAC still accounts for around 1.5% of CSWC’s portfolio and 2.5% of NAV per share.

“Despite its underperformance, we continue to feel reasonably confident about our 1st Lien position in the company, due to the value of its national substance abuse treatment franchise, managements operational efficiency initiatives, the tremendous demand for drug addiction treatment in the U.S., and the company’s large real estate portfolio associated with its street facilities.”

On March 15, 2019, S&P Global Ratings downgraded AAC Holdings Inc.’s issuer credit rating to CCC from B- after the company took out a $30 million term loan.

“The outlook is negative for AAC, which provides substance use treatment services for people with drug and alcohol addiction, and co-occurring mental and behavioral issues in the U.S. S&P Global Ratings said the downgrade reflects an increased risk of default and risk that AAC’s liquidity will not be sufficient over the next 12 months as the loan matures in about one year. The rating agency expects AAC to monetize its real estate assets to repay the new term loan March 31, 2020, and fund its operations in 2019. It believes there are risks that proceeds from a potential sale-leaseback may not be sufficient to cover operating needs and repay the term loan. S&P Global Ratings noted that AAC’s solvency heavily depended on executing its cost-saving initiatives.”

AG Kings was previously on non-accrual but marked down again now at 76% of cost and was discussed on the recent call:

Q. “AG Kings, we don’t have the 10-Q in front of us. Was that credit marked up or down at all this quarter and is — or materially and is there any update to pass along?”

A. “Yes, company is kind of still on the same — it’s just — it’s kind of bumping along. It hasn’t gotten worse. It really hasn’t gotten a whole lot better. We did market down by 10 points this quarter. So down from the mid 80s to the mid 70s.”

“We have had some of our portfolio, it’s a small handful, but it’s a couple of, like you referenced American Addiction and AG Kings. So we have had some softening in certain names, no question about it. Most of it’s really more idiosyncratic on a small handful of names. Across the portfolio, I would say, EBITDA performance is softened slightly from what it was the last couple of quarters, maybe by now a little bit on the economy. But generally from a first lien senior secured lender perspective not — yes, disappointing in some of the company’s performance. But from an investor perspective sitting in the first lien loan, less worrisome. But I mean, everything worries us. We’re managing the portfolio. Obviously, it’s our job to worry. But generally speaking, I think the structures are working as designed.”

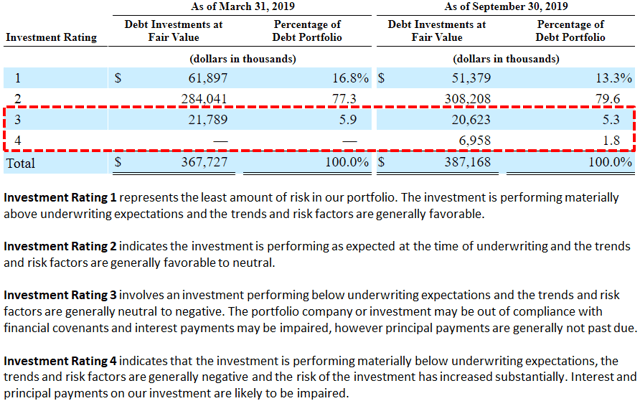

“As of the end of the quarter, of the 40 loans in the portfolio at fair value, we had three with the highest rating of one, representing 13% of the credit portfolio; we had 32 loans rated at two, representing 80% of the credit portfolio; we had four loans rated at three, representing 5% of the credit portfolio, and we had one loan rated at four, representing 2% of the credit portfolio.”

—————–

The portfolio has energy/oil-related exposure of around 2% and commodities/mining exposure of 2%. The energy investments are considered “midstream” as compared to “upstream” which usually involves more commodity-related risk.

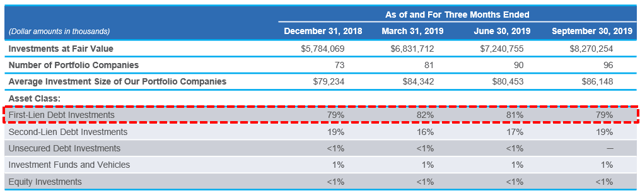

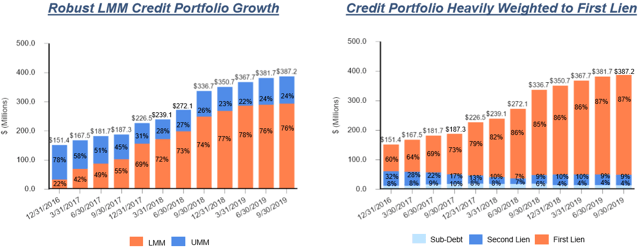

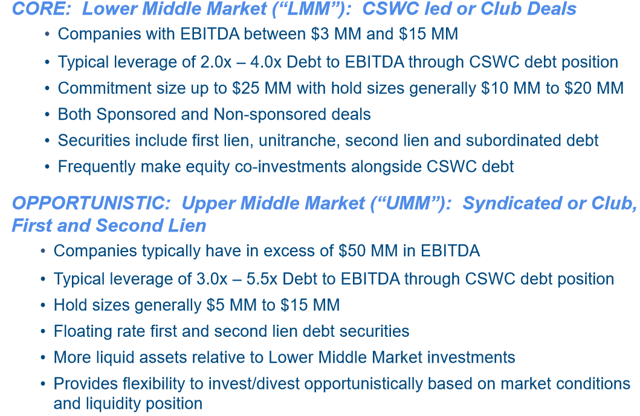

As the portfolio has grown, the percentage of its debt investments (excluding I-45 SLF) represented by the lower middle market has increased to 76% and first-lien accounts for 87%:

“While we have increased the percentage of the portfolio represented by the lower middle market, we have also continued to heavily emphasize Senior Secured 1st Lien Debt in our investment strategy. As of the end of the quarter, we had 76% of our on-balance sheet credit portfolio invested in lower middle market companies, while having 87% of the credit portfolio in first lien senior secured debt.”

—————–

Its I-45 Senior Loan Fund accounts for 12% of the portfolio and is a joint venture with MAIN created in September 2015, 95% invested first-lien.

—————–

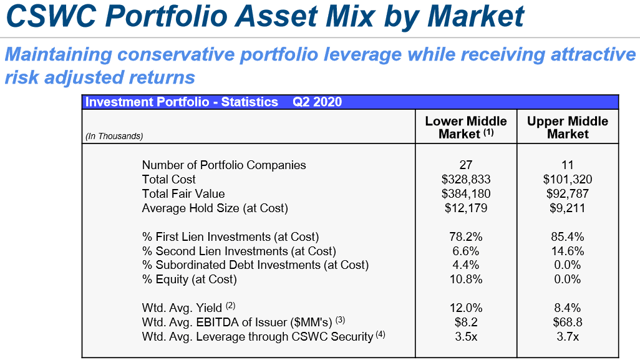

CSWC’s debt portfolio is mostly first-lien positions with the potential for realized gains from its equity investments, especially in its lower middle-market investments (similar to MAIN). Equity participation is partially responsible for growing its NAV per share as well as ‘recurring non-recurring’ income, which contributes to the growing amount of undistributed spillover income and gains used to support continued supplemental dividends.

“We had 27 lower middle market portfolio companies with an average hold size of $12.2 million, a weighted average EBITDA of $8.2 million, a weighted average yield of 12% and a leverage ratio measured as debt-to-EBITDA through our security of 3.5 times. Within our lower middle market portfolio, as of the end of the quarter, we held equity ownership in 70% of our portfolio companies. Our on-balance sheet upper middle market portfolio consisted of 11 companies with an average hold size of $9.2 million, a weighted average EBITDA of $68.8 million, a weighted average yield of 8.4% and a leverage ratio through our security of 3.7 times.”

“In our core market, the lower middle market, we directly originate opportunities consisting of debt investments and equity co-investments. Building out a highly performing and granular portfolio of equity co-investments is important to driving growth in NAV per share, while aiding in the mitigation of future credit losses. At the same time, our capability and presence in the upper middle market provides us the ability to opportunistically invest in a more liquid market when attractive risk-adjusted returns exist. Capital Southwest continues to have an equity co-investment in the company with significant unrealized appreciation. This continues our strong track record of successful exits as we have now had 27 portfolio exits since launch of our credit strategy, generating $214 million in total proceeds and a cumulative IRR of 15.5%. ”

This information was previously made available to subscribers of Premium BDC Reports, along with:

- CSWC target prices and buying points

- CSWC risk profile, potential credit issues, and overall rankings

- CSWC dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.

Gladstone Investment (GAIN) Update Summary:

Gladstone Investment (GAIN) Update Summary: