The following information was previously provided to subscribers of Premium BDC Reports along with:

ORCC and GSBD target prices/buying points

ORCC and GSBD risk profiles, potential credit issues, and overall rankings. Please see BDC Risk Profiles for additional details.

ORCC and GSBD dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

The Big Boys Continue To Pile Into This Dividend Sector

As mentioned in “The Big Boys Continue To Pile Into This Dividend Sector: ORCC” Business Development Companies (“BDCs”), like REITs almost 20 years ago, want institutional investors and the scale that comes with them. Many of the largest asset managers have been actively building assets in the sector including BlackRock, Goldman Sachs Group, Franklin Templeton, The Blackstone Group, Barings, Apollo, The Carlyle Group, Ares Management, KKR & Co. Inc., Oaktree Capital Management, TPG Capital, Bain Capital, and Blue Owl. However, Ares and Apollo have managed Ares Capital (ARCC) and Apollo Investment (AINV) for quite a while as compared to others. This article discusses Goldman Sachs BDC (GSBD)and Owl Rock Capital (ORCC). There are now 20 publicly traded BDCs with more than $1 billion in assets and I have discussed many of them over the last few months (see list below) and will try to cover the others in upcoming articles.

These 13 asset management companies combined manage more than $16.5 trillion in assets (up from $11 trillion in early 2020), and there will likely be continued positive changes to regulations over the coming quarters driving up multiples for current investors. Please keep in mind that higher multiples mean higher prices (and lower yields) as the BDC sector continues to attract more attention and respect from the investment community especially given how they performed during the pandemic. Most BDCs seem to be in a virtuous circle of improving asset quality supporting a lower cost of capital driving improved earning, NAV, and dividend increases. Many have recently issued very low rate unsecured notes and refinanced their balance sheets including Owl Rock Capital (ORCC) and Goldman Sachs BDC (GSBD) as discussed in this article.

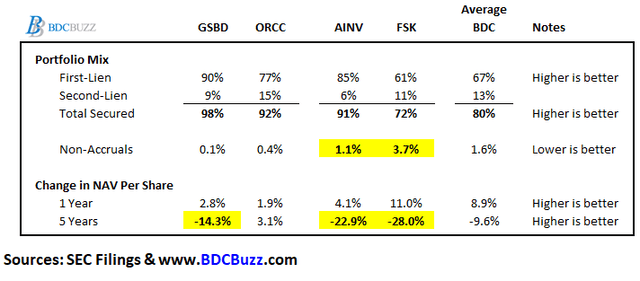

Portfolio Mix and Credit Quality

The following tables show a handful of some of the metrics used to compare BDCs but please keep in mind that this information is oversimplified and needs discussion. For example, not all “first-lien” is the same credit quality. I would feel much safer with second-lien in a higher quality BDC than first-lien in a lower quality one. Plenty of the BDCs that were the worst performers had plenty of first-lien only to have huge declines in book values or net asset values (“NAV”) the following quarters. Medley Capital (MCC) and Fifth Street Capital (FSC) were perfect examples of this.

Also, please note that BDCs such as GSBD, ORCC, and AINV have mostly secured debt positions as compared to equity participation which has been primarily responsible for most of the NAV growth for other BDCs. That is why the average BDC has experienced ANV growth of around 9% over the last four quarters but they also have lower amounts of secured positions. For some examples of BDCs that have been benefitting from equity positions please see the following articles from September 2021:

It is important to point out that BDCs that have been marking up equity positions would likely experience larger NAV declines during a serious market downturn or economic event. Please be careful.

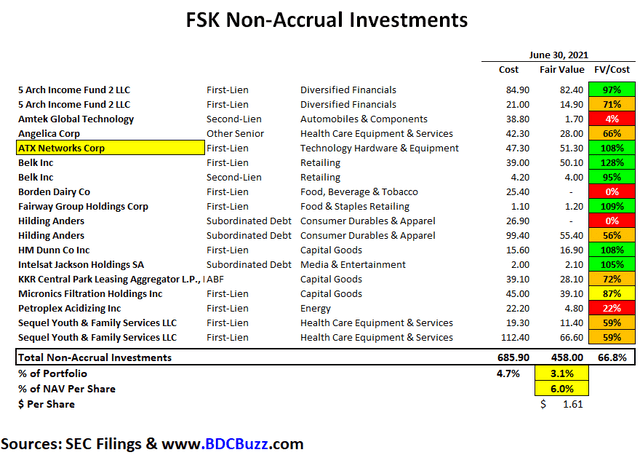

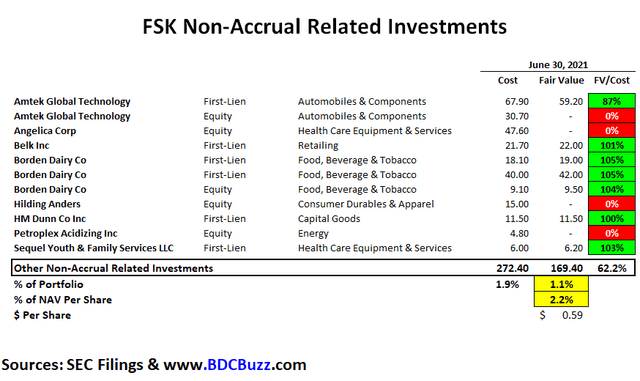

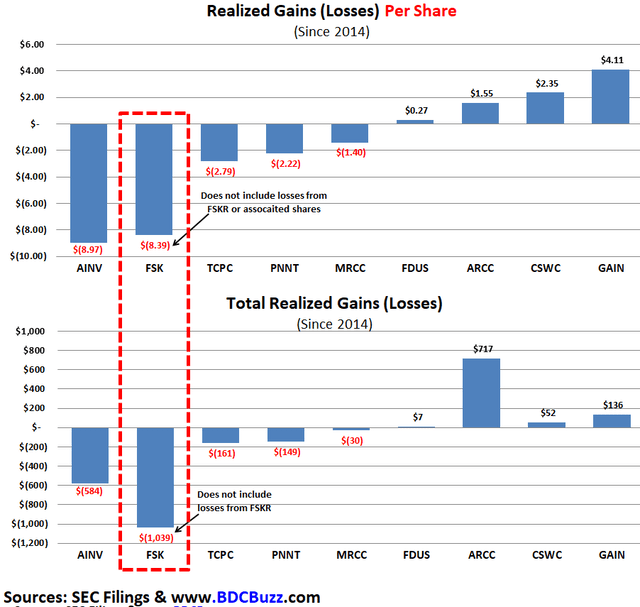

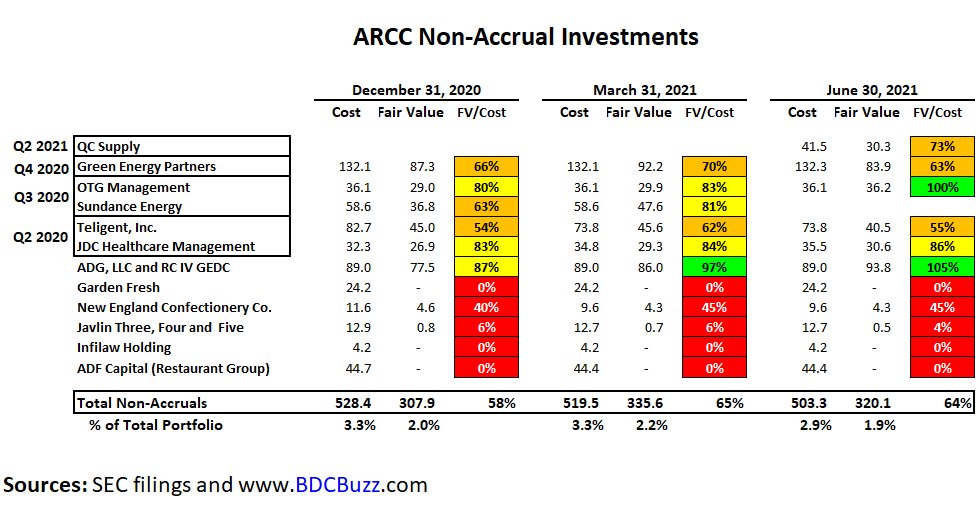

Also, non-accruals are investments that a BDC is currently not accruing income due to credit issues. Some BDCs will exit or restructure these investments just before the quarter-end taking a realized loss but avoiding being listed as a credit issue when it comes to reporting. It’s better to look at historical realized losses which clearly identify historical credit issues as discussed in some of the articles linked above including “FS KKR Capital: Dividend Decrease Coming” which discussed FSK and AINV.

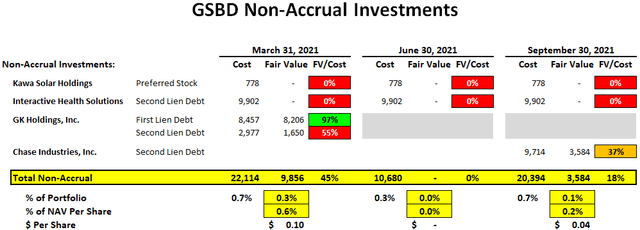

As shown in the previous table, FSK and AINV have had larger NAV declines over the last 5 years but so has GSBD mostly related to legacy investments. These investments have been discussed in previous articles and were considered idiosyncratic especially given the improved credit quality over the last two years. GSBD has 111 portfolio companies and with only 2 put on non-accrual status over the last 7 quarters.

As of September 30, 2021, GSBD’s investments on non-accrual status accounted for 0.1% and 0.7% of the total investment portfolio at fair value and cost, respectively. If its non-accrual were completely written off the impact to NAV would be around $0.04 per share or 0.2%:

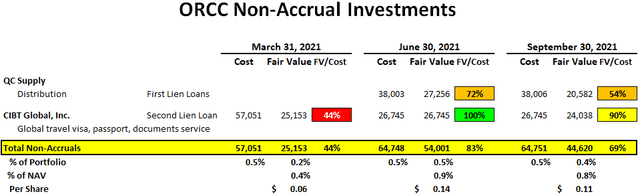

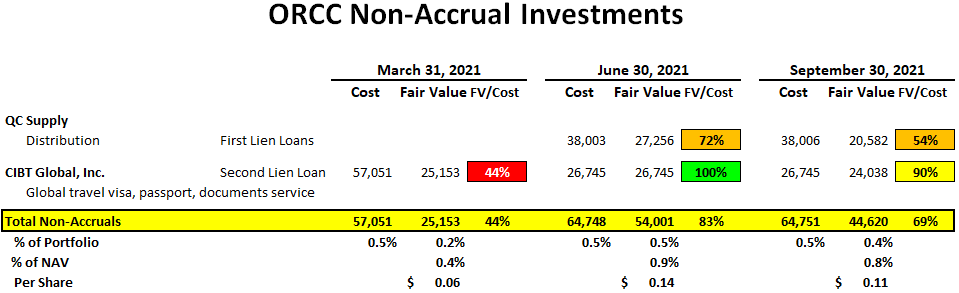

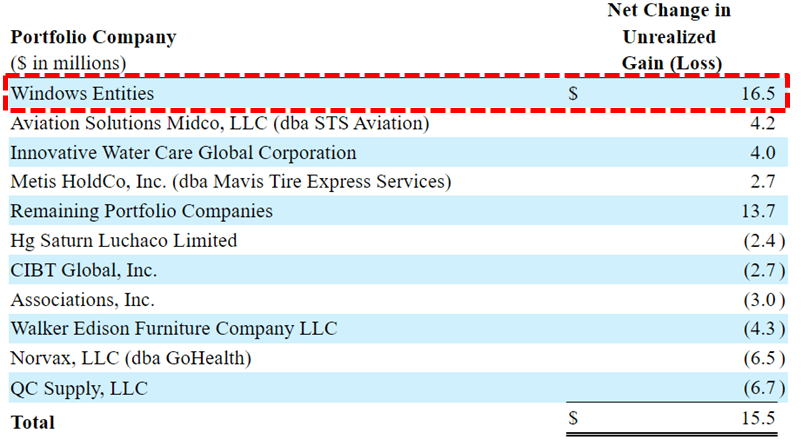

Two of ORCC’s smaller first-lien loans to QC Supply were added to non-accrual status during Q2 2021 and marked down again during Q3 2021. Also, CIBT Global, Inc. remains non-accrual and was also marked down as shown in the following table. Please keep in mind that ORCC has 130 portfolio companies so there will always be a certain amount on non-accrual which currently account for 0.4% of the total portfolio fair.

We are carefully monitoring the current headwinds caused by the labor shortages and supply chain disruptions. To date, we have not seen a material impact as many of our companies are services businesses, which have modest exposure to the manufacturing economy. For example, some of our largest sectors are software, insurance, and health care, which are not as exposed to the current economic headwinds. In line with last quarter, our nonaccruals remained low with only two investments on non-accrual status, representing 0.4% of the portfolio based on fair value. One of the lowest levels in the BDC sector and our annualized loss ratio is 14 basis points.”

Expense Ratio & Fee Agreements

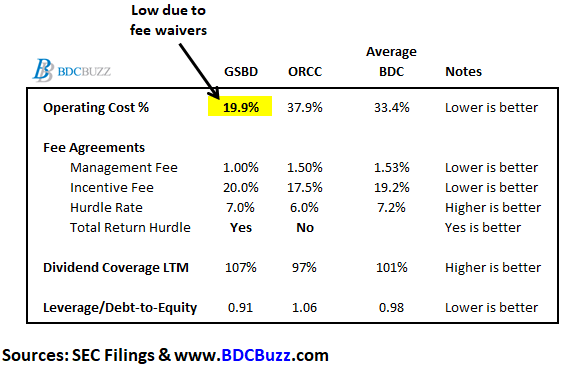

As a part of assessing BDCs, it’s important to take into account expense ratios. BDCs with lower operating expenses can pay higher amounts to shareholders without investing in riskier assets.

“Operating Cost as a Percentage of Available Income” is one of the many measures that I use which takes into account operating, management, and incentive fees compared to available income. “Available Income” is total income less interest expense from borrowings and is the amount of income that is available to pay operating expenses and shareholder distributions.

As discussed in “Conservative Portfolio Safely Paying Investors 7.3%“, many BDCs have been temporarily waiving fees or have fee agreements that take into account previous capital losses that are ending this year. GSAM is waiving a portion of its incentive fee for the four quarters of 2021 (Q1 2021 through and including Q4 2021) in an amount sufficient to ensure that GSBD’s net investment income per share is at least $0.48 per share per quarter.

However, GSBD has what I consider to be a more shareholder-friendly fee agreement with a lower-than-average base management fee of 1.00% and a total return hurdle to protect shareholders from additional credit issues. ORCC has a lower yielding portfolio which is why its hurdle rate is only 6.0% (not ideal) and lower-than-average incentive fee rate.

The ‘dividend coverage LTM’ is showing the average dividend coverage over the last 12 months (4 quarters) and is higher for GSBD due to fee waivers and lower for ORCC as the company was previously underleveraged. ORCC continues to increase leverage covering its dividend by 109% in Q3 2021 as discussed later.

GSBD Dividend Coverage Update

Author’s Note: The following information was provided to subscribers along with three quarters of financial projections using base, best, and worst-case assumptions to test the sustainability of the current dividends for GSBD.

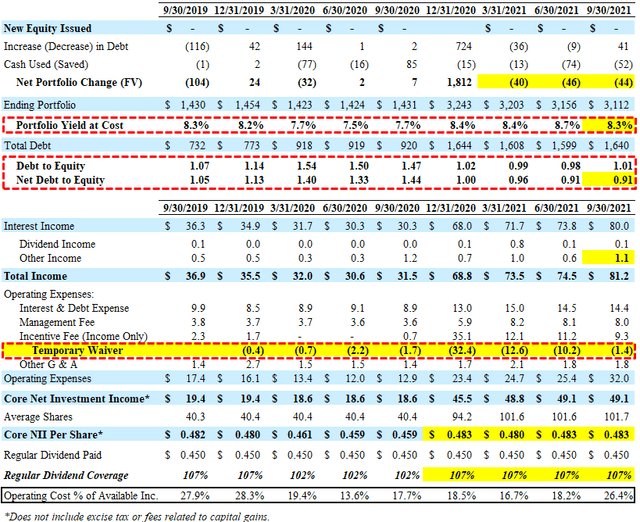

For Q3 2021, GSBD reported slightly below its best-case projections mostly due to an increase in accelerated accretion related to repayments and higher fee income partially offset by lower portfolio yield and lower portfolio growth (decline). Leverage (debt-to-equity) remains at its near-term low of 0.91 (net of cash) giving the company adequate growth capital for increased earnings potential. It should be noted that fee waivers continued to decline and were only $1.4 million.

I am expecting improved dividend coverage for GSBD over the coming quarters mostly due to:

Portfolio growth due to lower prepayments

Reinvesting the proceeds from Hunter Defense Technologies

Continued lower cost of borrowings

Higher portfolio yield from rotating into higher yield assets

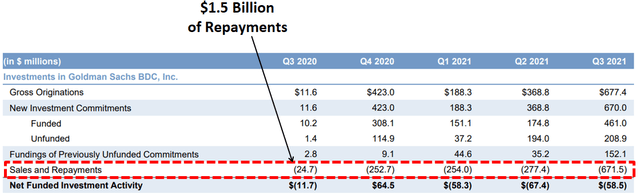

It is important to point out the GSBD remains below its targeted leverage due to $1.5 billion of repayments over the last 4 to 5 quarters which is meaningful given that its total portfolio is only $3.1 billion. However, management is not expecting the same level of repayments:

Elevated repayments continued unabated this quarter. At $672 million repayments equaled 21% of the fair value of investments at the beginning of the quarter and were 2.4 times greater than last quarter which itself was the previous high water mark repayments in the company’s nearly 10-year history. Repayments were diversified across the book with the single large repayment only amounted to less than 10% of the total. This is a somewhat remarkable level of portfolio turnover in a single quarter, there are a few takeaways I would offer for this unusual activity. First, I believe this repayment activity is a reflection of our focus on sectors and companies that continue to grow, perform well, and are therefore increasingly in investor favor. In an environment where M&A activity is high and equity evaluations are rising, it’s not surprising that high quality companies are either being sold or graduating to a lower cost of capital.”

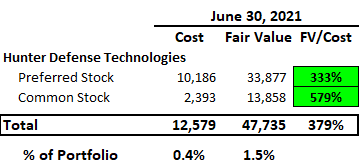

One of the repayments from Q3 2021 was Hunter Defense Technologies which accounted for almost $48 million or 1.5% of the portfolio driving a realized gain of almost $36 million or $0.35 per share. This was a non-income producing equity investment that will be reinvested into debt investments yielding at least 8% which is an additional ~$3.8 million of annual income.

During the quarter, we exited our equity position in Hunter Defense Technologies. Hunter Defense is a provider of shelters and ancillary products used primarily by the U.S. military in mobile troop deployments. The sale of the position generated a realized gain of $36 million. Hunter Defense was a previously non-income producing asset that’s been able to be monetized, recycled back into income producing assets.”

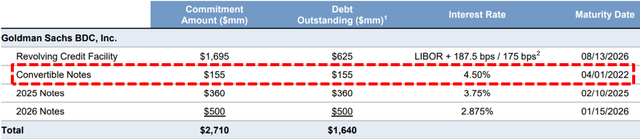

Similar to most BDCs, GSBD has been lowering its borrowing rates as well as constructing a flexible balance sheet including a public offering of $500 million of 2.875%unsecured notes due 2026. In August 2021, the company reduced the interest rate on its credit facility from LIBOR plus 2.00% to LIBOR plus 1.875%/1.75% which will be used to refinance its $155 million of 4.50% convertible notes on April 1, 2022. This will have a meaningful impact on earnings starting in Q2 2022:

There’s also tremendous tailwinds on the liability side of the balance sheet for the company here as well. I’m sure many of the investors in this space are following what’s going on in the financial markets for these assets. There’s typically generally a high correlation between if there’s pressure on asset yields, there’s also an opportunity on the liability side. For example, we’ve got our convertible bond which has a 4.5% coupon coming due early next year, that will be recycled. Our current plan would be to refinance that with our existing capacity under our revolving credit facility, which of course comes with a much lower cost of capital. I think there’ll be ongoing opportunities over the course of next year to do that, as well. So I think those are just a few things that I point to that that give us some optimism that there’s still really good opportunities to perform here.”

ORCC Dividend Coverage Update

Author’s Note: The following information was provided to subscribers along with three quarters of financial projections using base, best, and worst-case assumptions to test the sustainability of the current dividends for ORCC.

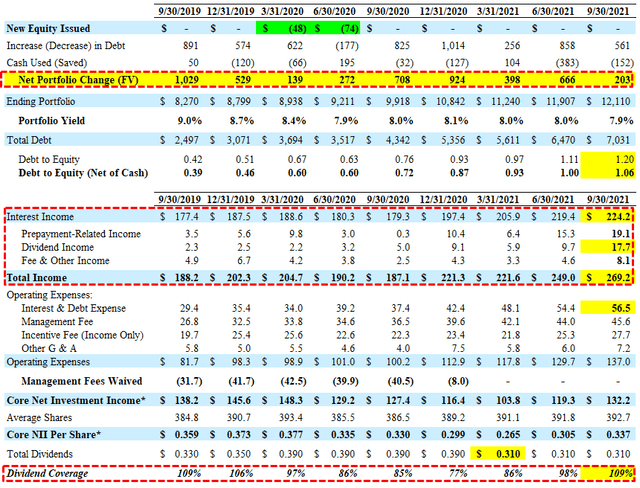

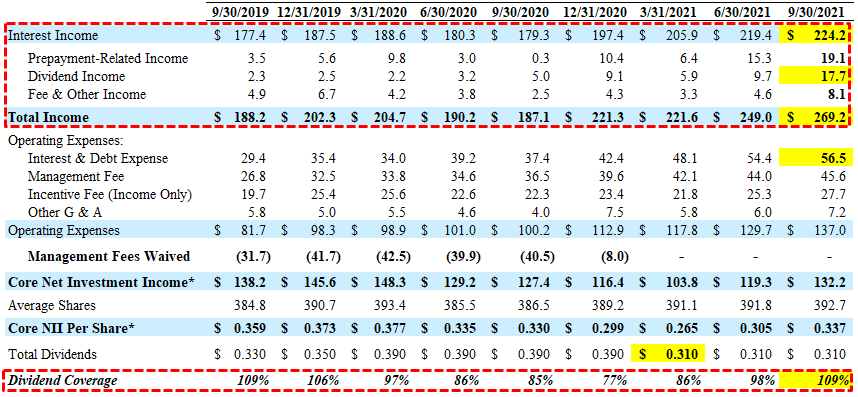

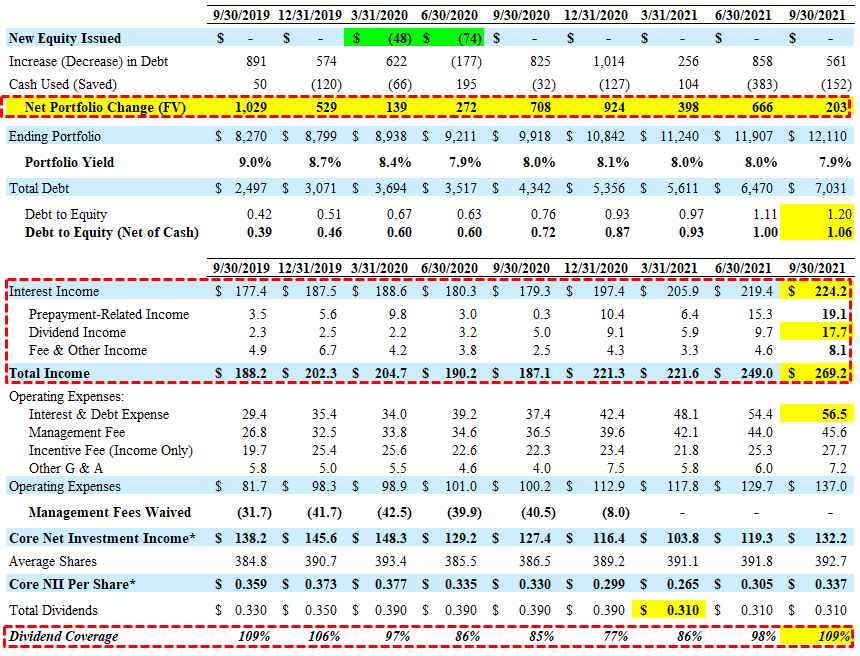

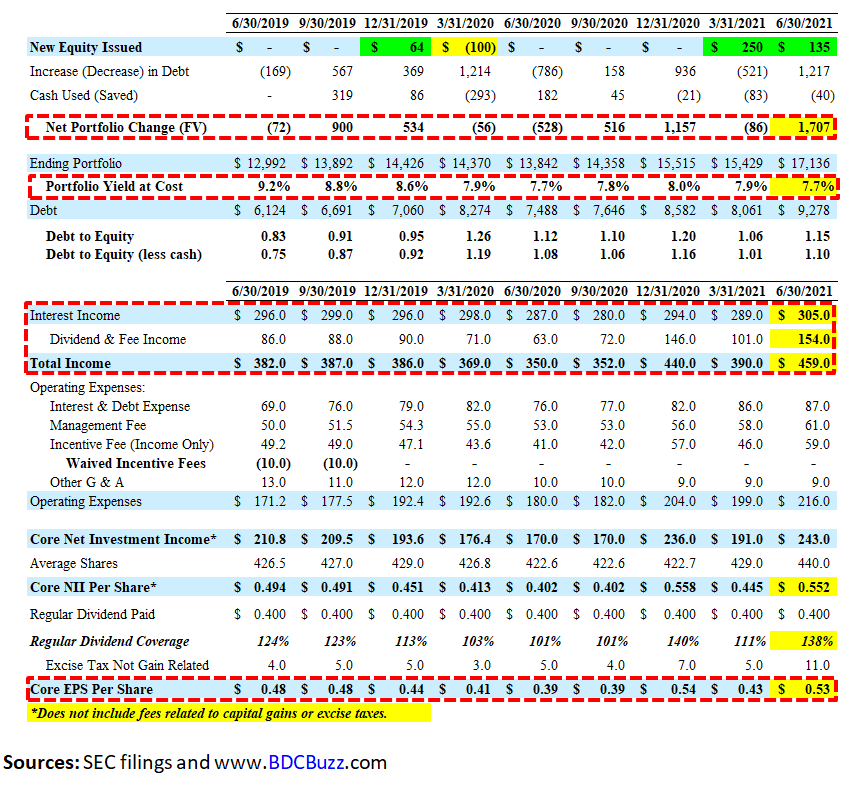

For Q3 2021, ORCC beat its best-case projected earnings due to higher-than-expected prepayment-related, dividend, and fee income as well as higher portfolio growth growing total income to the highest level of $269 million.

ORCC was not expected to cover its quarterly dividend but Core NII of $0.337 (excluding excise tax) covered 109% of its dividend of $0.310.

I am expecting improved dividend coverage for ORCC over the coming quarters mostly due to:

Increased dividend income from its Senior Loan Fund and Wingspire

Maintaining target leverage with new investments offsetting repayments

Additional prepayment fees and accelerated OID

Higher portfolio yield from rotating into higher yield assets

Continued lower cost of borrowings

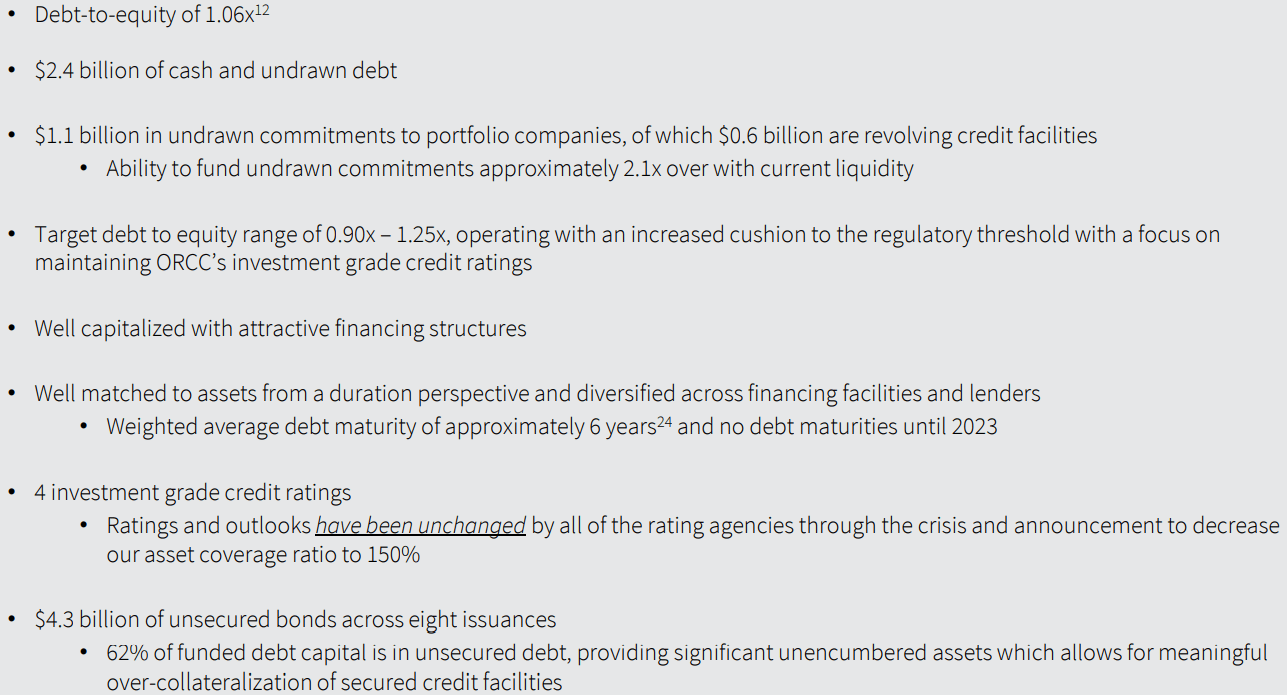

ORCC continues to increase leverage and is now near the midpoint of its target debt-to-ratio between 0.90 and 1.25 (currently 1.06 excluding $780 million of available cash) giving the company plenty of growth capital.

We experienced a record level of originations this quarter which resulted in a fully ramped $12 billion-plus portfolio. We also had a record level of repayments. Prior to this quarter we had not yet seen the pace of repayments expected for a portfolio of our size but this trend finally materialized in the third quarter. We had more than $2 billion of repayments, which generated healthy fee and amortization income. At the same time, we’re able to seamlessly replace those repaid investments with equally attractive new investments of a similar credit quality and comparable economics, which has allowed us to finish the quarter in an equally strong position and with leverage comfortably in our target range. While this quarter may prove to be on the higher end, we do expect repayments to continue to exceed the levels we have seen in the last couple of years.”

Management is expecting another strong quarter partially due to higher prepayment-related income which has been taken into account with the updated financial projections and was discussed on the recent earnings call:

We had a significant amount of repayments this quarter, which drove a material increase in earnings from accelerated accretion and prepayment fees. While this is not a contractual earnings stream, we do expect repayment-related income to broadly stay around these levels in future quarters, as we expect that our repayments will remain at a more normalized pace, recognizing that the timing of repayments is idiosyncratic in any specific quarter.”

“We expect to see a healthy level, likely lower than this quarter’s record, but higher than previous quarters. Now that the portfolio is fully ramped, we will generally be targeting originations in line with repayments in order to maintain a fully levered, fully invested portfolio, and we have a strong backlog of attractive deals expected to close this quarter.”

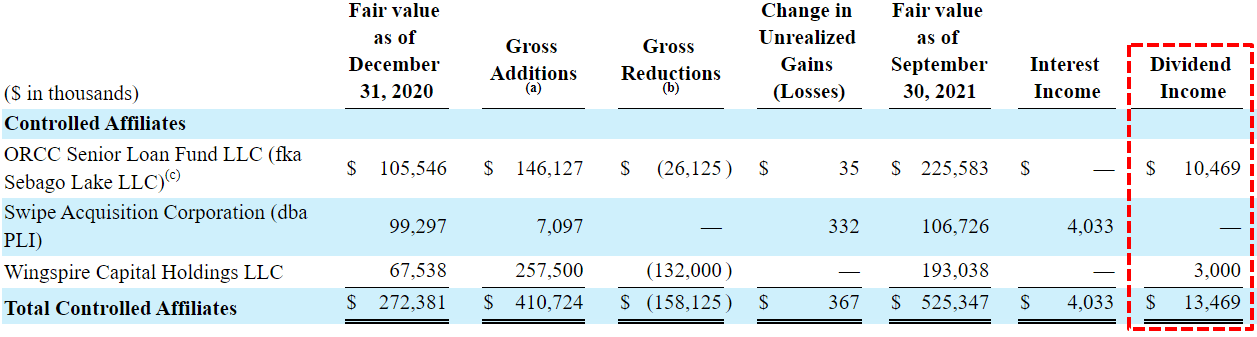

The increased dividend income was mostly related to equity investments in Windows Entities and Wingspire Capital Holdings that will likely continue over the coming quarters:

Our total investment income for the quarter, increased to $269 million, up $20 million from the prior quarter. This increase was primarily driven by dividend income, which increased by $8 million. We received our first dividend from Wingspire this quarter, as well as continued dividend income from Windows Entities and our senior loan fund. We expect dividend income from Wingspire and our senior loan fund to continue to increase as our committed capital is deployed.”

“Our investment in Wingspire, an asset-based lender to US-based middle market companies, with roughly $350 million of assets and very strong credit performance. We currently have approximately $195 million invested in Wingspire and see opportunities to invest more capital going forward. We expect Wingspire will be run rating at a high single-digit ROE by the end of this year and can generate a 10-plus percent ROE.”

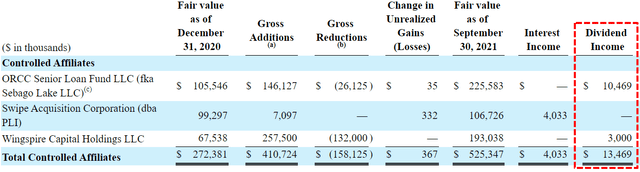

Also taken into account with the updated projections is additional dividend income from its ORCC Senior Loan Fund (previously Sebago Lake LLC) which now accounts for 1.9% of the total portfolio. Management is expecting this joint venture with Nationwide Life Insurance to eventually provide quarterly dividend income of $7 million:

“The other investment is in our Senior Loan Fund. As you recall, last quarter, we increased our equity commitment in the fund to $325 million and our economic ownership to 87.5%. The fund has already generated an attractive average quarterly ROE over the past three years of approximately 10%, and we will look to increase our capital invested over time.”

From previous call: “And so we’ll just be able to increase over time the amount of money ORCC has working and grow that number, when we get all that working it’s going to take some time should be we $7 million a quarter, which is I think terrific.”

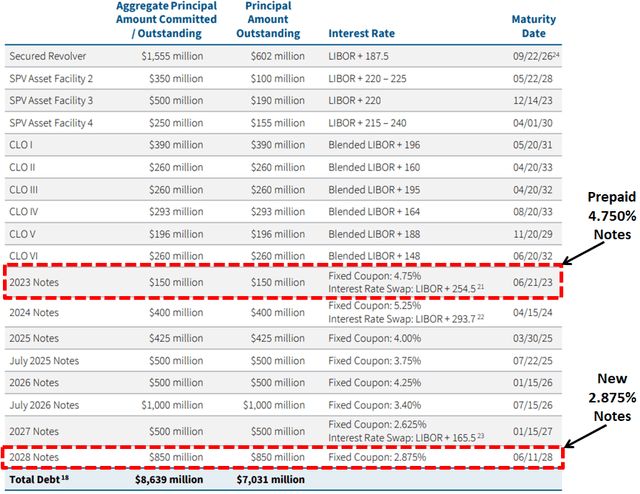

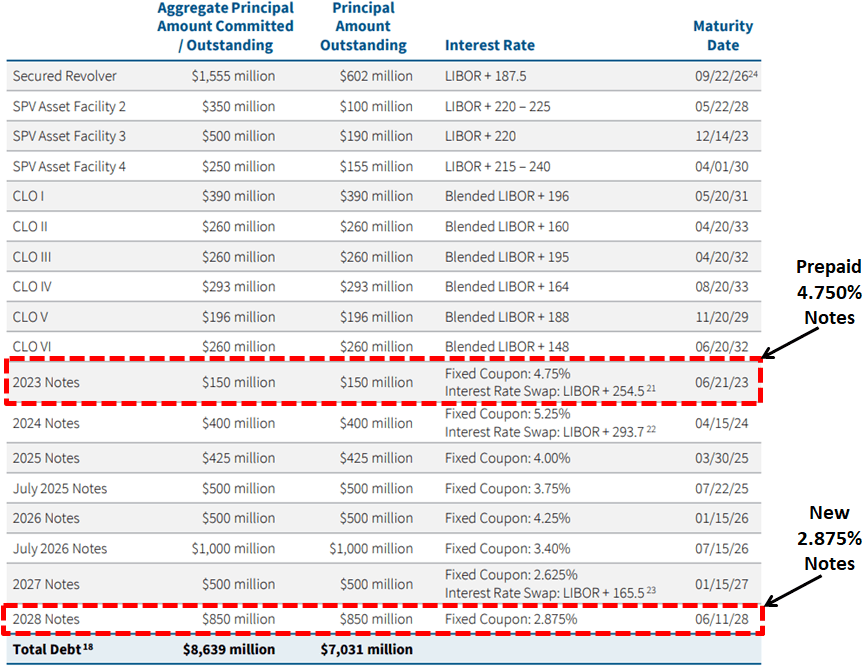

On November 23, 2021, ORCC announced the prepayment of its higher rate of 4.75% notes due 2023. In August 2021, the company issued another $400 million of its 2.875% notes due 2028. As of September 30, 2021, ORCC had around $2.4 billion of liquidity consisting of $780 million of cash and almost $1.6 billion of undrawn debt capacity (including upsizes).

Setting Target Prices

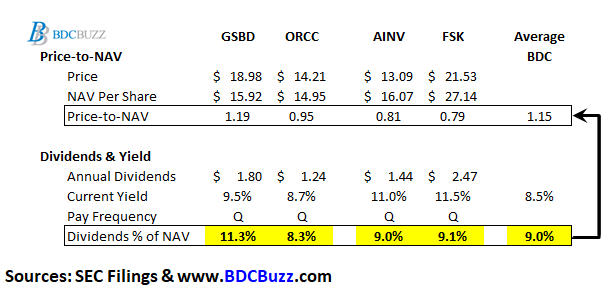

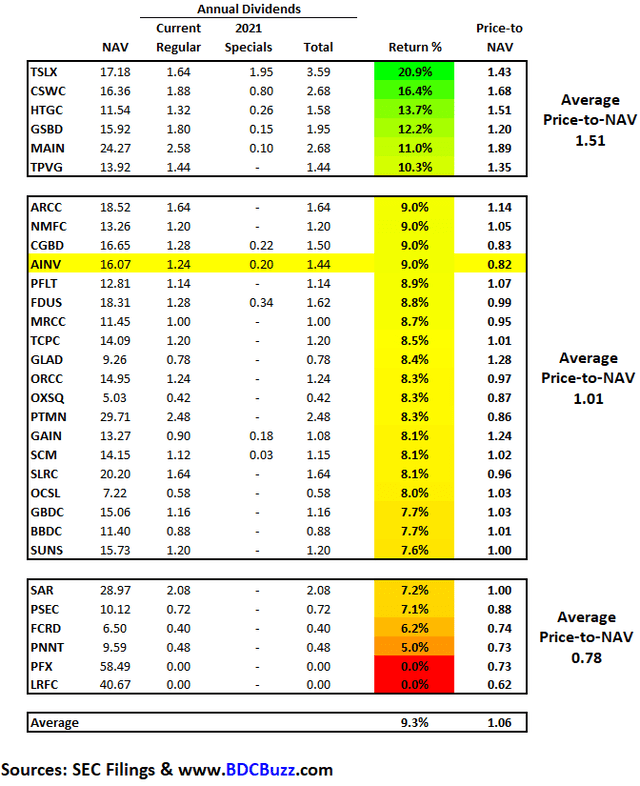

There are very specific reasons for the prices that BDCs trade driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). Also, and this is very important, the price-to-book/NAV is highly dependent on the amount of dividends that a BDC is paying as a percentage of NAV (but also taking into account risk profile and projected dividends).

For example, GSBD is currently paying a regular quarterly dividend of $0.45 per share which is $1.80 annually and 11.3% of its current NAV per share ($1.80/$15.92). This is much higher than most BDCs which are currently averaging around 9.0% of NAV.

ORCC pays a regular quarterly dividend of $0.31 per share which is $1.24 annually and 8.3% of its current NAV per share ($1.24/$14.95).

The last table from “Dividend Increase Coming For PennantPark” shows each BDC roughly categorized into groups of paying below 7.5%, 7.5% to 9.0% (including ORCC), and over 10.0% (including GSBD). If GSBD is able to maintain its regular dividend then the current pricing should be higher driving a yield closer to the average of 9.0% and its price-to-NAV closer to the other BDCs in the top group (paying over 10.0% of NAV).

Again, BDCs with higher quality credit platforms and management typically have higher quality portfolios and investors pay higher prices. This drives higher multiples to NAV and lower yields.

BDCs with lower expenses and higher potential dividend coverage typically have stable to growing dividends and investors pay higher prices. This drives higher multiples to NAV and lower yields.

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy to digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

Monday Morning Update – Before the markets open each Monday morning we provide quick updates for the sector including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

Deep Dive Projection Reports – Detailed reports on at least two BDCs each week prioritized by focusing on ‘buying opportunities’ as well as potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

Friday Comparison or Baby Bond Reports – A series of updates comparing expense/return ratios, leverage, Baby Bonds, portfolio mix, with discussions of impacts to dividend coverage and risk. This week we are providing a general market update with “suggested limit orders” for each BDC due to the expected volatility.

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying including setting target prices using the portfolio detail shown in this article (at a minimum) as well as financial dividend coverage projections over the next three quarters as discussed earlier.

The following information was previously provided to subscribers of Premium BDC Reports along with:

ORCC target prices/buying points

ORCC risk profile, potential credit issues, and overall rankings. Please see BDC Risk Profiles for additional details.

ORCC dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

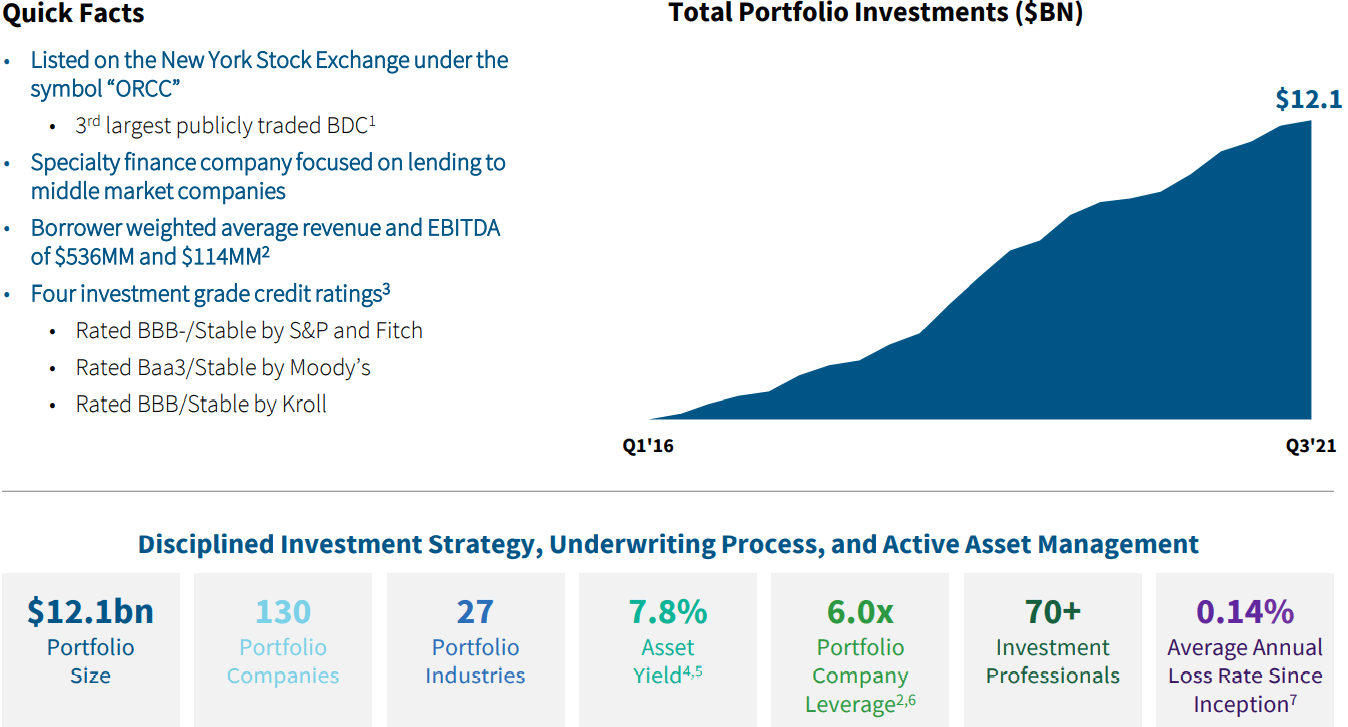

This update discusses Owl Rock Capital Corporation (ORCC) remains one of the best-priced BDCs especially for lower-risk investors that do not mind lower yields. ORCC is for risk-averse investors as the portfolio is mostly larger middle market companies that would likely outperform in an extended recession environment.

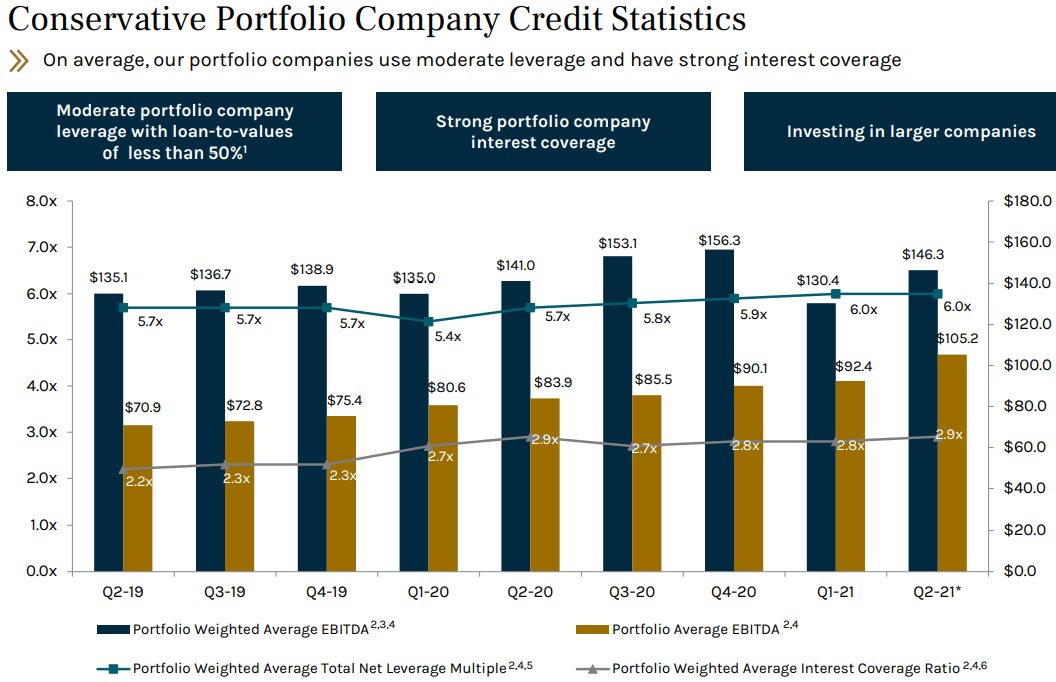

“We also continue to grow the size of the companies in our portfolio. The weighted average EBITDA of our borrowers is now $114 million, which is up from $95 million a year ago. In addition to allowing us to invest more efficiently, we believe larger companies are safer to lend to, and that has been borne out by our results over the last five years. This year, we have already evaluated more than 20 opportunities over $1 billion in size, and invested in or committed to eight of these, and continue to evaluate others. This trend continues to accelerate and is creating exciting opportunities for large direct lenders like Owl Rock.”

As predicted in previous reports, ORCC’s dividend coverage continues to improve mostly due to:

Increased dividend income from its ORCCSenior Loan Fund and Wingspire

Maintaining target leverage with new investments offsetting repayments

Additional prepayment fees and accelerated OID

Continued lower cost of borrowings

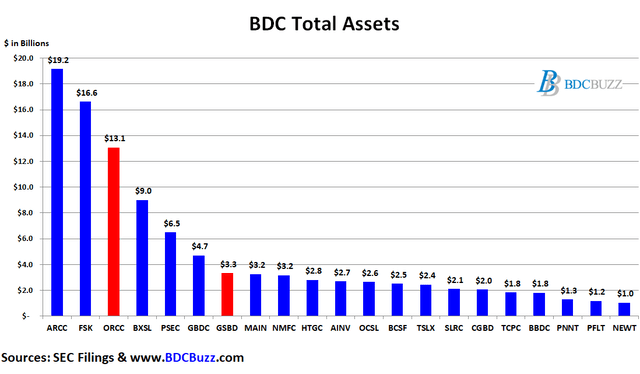

ORCC is the third-largest publicly traded BDC (much larger than MAIN, PSEC, GBDC, GSBD, NMFC, BXSL, HTGC, and AINV) with investments in 130 portfolio companies valued at around $12 billion that are mostly first-lien secured debt positions. ORCC is one of the few BDCs rated by all of the major credit agencies.

ORCC Dividend Coverage Update

ORCC’s longer-term (“LT”) target price takes into account improved dividend coverage over the coming quarters mostly due to:

Increased dividend income from its Senior Loan Fund and Wingspire

Maintaining target leverage with new investments offsetting repayments

Additional prepayment fees and accelerated OID

Higher portfolio yield from rotating into higher yield assets

Continued lower cost of borrowings

ORCC continues to increase leverage and is now near the midpoint of its target debt-to-ratio between 0.90 and 1.25 (currently 1.06 excluding $780 million of available cash) giving the company plenty of growth capital.

“We experienced a record level of originations this quarter which resulted in a fully ramped $12 billion-plus portfolio. We also had a record level of repayments. Prior to this quarter we had not yet seen the pace of repayments expected for a portfolio of our size but this trend finally materialized in the third quarter. We had more than $2 billion of repayments, which generated healthy fee and amortization income. At the same time, we’re able to seamlessly replace those repaid investments with equally attractive new investments of a similar credit quality and comparable economics, which has allowed us to finish the quarter in an equally strong position and with leverage comfortably in our target range. While this quarter may prove to be on the higher end, we do expect repayments to continue to exceed the levels we have seen in the last couple of years.”

“As a result of this activity our net leverage increased to 1.06 times roughly the midpoint of our target ranges of 0.90 to 1.25 times. I would expect that we would operate somewhere between there and 1.10 in sort of center of gravity.”

For Q3 2021, ORCC beat its best-case projected earnings due to higher-than-expected prepayment-related, dividend, and fee income as well as higher portfolio growth growing total income to the highest level of $269 million.

“We had been expecting to achieve full coverage of our $0.31 per share dividend sometime in the second half of 2021. With these strong results we have now achieved this milestone and are well-positioned to continue to fully earn our dividend going forward.”

Management is expecting another strong quarter partially due to higher prepayment-related income which has been taken into account with the updated financial projections and was discussed on the recent earnings call:

“We had a significant amount of repayments this quarter, which drove a material increase in earnings from accelerated accretion and prepayment fees. While this is not a contractual earnings stream, we do expect repayment-related income to broadly stay around these levels in future quarters, as we expect that our repayments will remain at a more normalized pace, recognizing that the timing of repayments is idiosyncratic in any specific quarter.”

“We expect to see a healthy level, likely lower than this quarter’s record, but higher than previous quarters. Now that the portfolio is fully ramped, we will generally be targeting originations in line with repayments in order to maintain a fully levered, fully invested portfolio, and we have a strong backlog of attractive deals expected to close this quarter.”

The increased dividend income was mostly related to equity investments in Windows Entities and Wingspire Capital Holdings that will likely continue over the coming quarters:

“Our total investment income for the quarter, increased to $269 million, up $20 million from the prior quarter. This increase was primarily driven by dividend income, which increased by $8 million. We received our first dividend from Wingspire this quarter, as well as continued dividend income from Windows Entities and our senior loan fund. We expect dividend income from Wingspire and our senior loan fund to continue to increase as our committed capital is deployed.”

“Our investment in Wingspire, an asset-based lender to US-based middle market companies, with roughly $350 million of assets and very strong credit performance. We currently have approximately $195 million invested in Wingspire and see opportunities to invest more capital going forward. We expect Wingspire will be run rating at a high single-digit ROE by the end of this year and can generate a 10-plus percent ROE.”

Also taken into account with the updated projections is additional dividend income from its ORCC Senior Loan Fund (previously Sebago Lake LLC) which now accounts for 1.9% of the total portfolio. Management is expecting this joint venture with Nationwide Life Insurance to eventually provide quarterly dividend income of $7 million:

“The other investment is in our Senior Loan Fund. As you recall, last quarter, we increased our equity commitment in the fund to $325 million and our economic ownership to 87.5%. The fund has already generated an attractive average quarterly ROE over the past three years of approximately 10%, and we will look to increase our capital invested over time.”

From previous call: “And so we’ll just be able to increase over time the amount of money ORCC has working and grow that number, when we get all that working it’s going to take some time should be we $7 million a quarter, which is I think terrific.”

On November 23, 2021, ORCC announced the prepayment of its higher rate of 4.75% notes due 2023. In August 2021, the company issued another $400 million of its 2.875% notes due 2028. As of September 30, 2021, ORCC had around $2.4 billion of liquidity consisting of $780 million of cash and almost $1.6 billion of undrawn debt capacity (including upsizes).

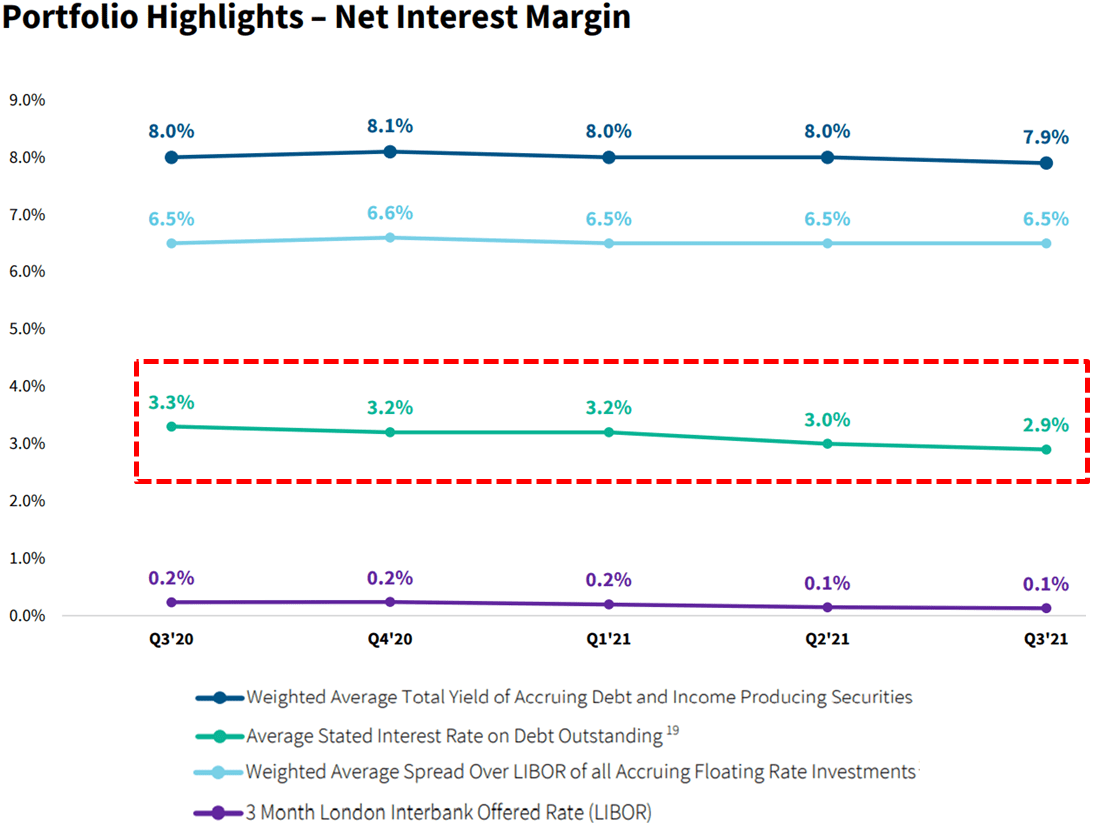

Similar to other BDCs, ORCC has been improving or at least maintaining its net interest margin which is the difference between the yield on investments in the portfolio and the rate of borrowings. During the most recently reported quarter, ORCC’s portfolio yield declined slightly but will likely trend higher over the coming quarters as the company rotates into higher yield assets “without sacrificing credit quality”:

“We continue to see an opportunity to improve our portfolio mix. We still have just over $1 billion of debt investments in the portfolio with a spread lower than 550 basis points. Our portfolio spread will benefit as these investments are repaid and we seek to redeploy this capital into higher spread investments, typically unitranches, which is an area where we have been able to achieve attractive pricing. There’s a portion of that $1 billion that I think there’s a reasonable chance we’ll get repaid in the next one to two quarters. And then there’s a portion that I think will take longer than that. There’s a portion in there that we might choose to sell over time and then there’s others that probably aren’t easily sold because there’s not other lenders in the credit with us, not from a credit reason.”

ORCC’s average borrowing rate has declined from 4.6% to 2.9% over the last 7 quarters due to continued issuances of notes and CLOs at lower rates.

For Q3 2021, ORCC beat its best-case projected earnings due to higher-than-expected prepayment-related, dividend, and fee income as well as higher portfolio growth growing total income to the highest level of $269 million.

“primarily due to an increase in our investment portfolio. Included in interest income is dividend income, which increased period over period, and other fees such as prepayment fees and accelerated amortization of upfront fees from unscheduled paydowns.”

ORCC was not expected to cover its quarterly dividend but Core NII of $0.337 (excluding excise tax) covered 109% of its dividend of $0.310.

The Board declared a Q4 2021 dividend of $0.31 per share for stockholders of record as of December 31, 2021, payable on or before January 31, 2022.

“We are very pleased to report strong results this quarter. We experienced a record level of both originations and repayments and were able to seamlessly redeploy capital from those repaid investments into equally attractive new investments. We are very proud of where our portfolio stands today and to achieve the important milestone of earning our dividend from net investment income this quarter with continued strong credit.”

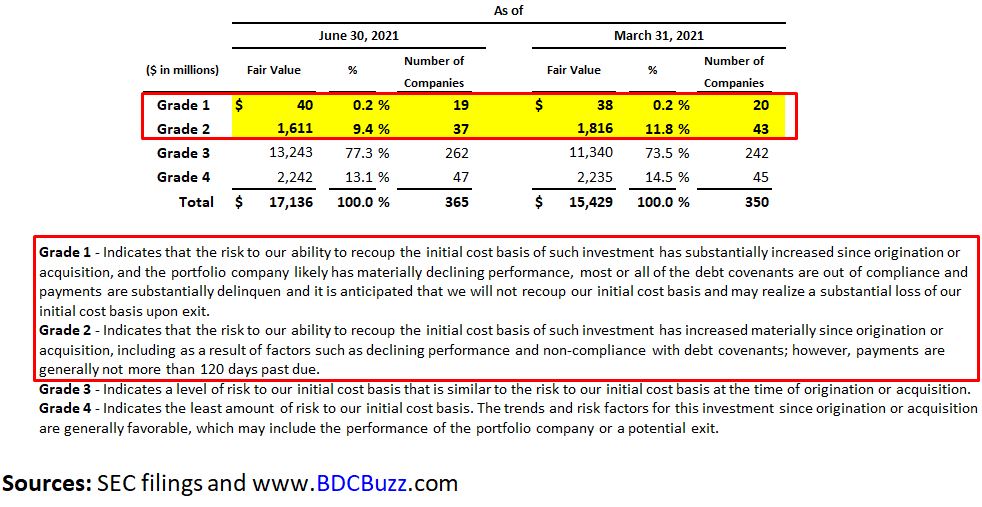

ORCC Quick Risk Profile Update

Two of its smaller first-lien loans to QC Supply were added to non-accrual status during Q2 2021 and marked down again during Q3 2021. Also, CIBT Global, Inc. remains on non-accrual and was also marked down as shown in the following table. Please keep in mind that ORCC has 130 portfolio companies so there will always be a certain amount on non-accrual which currently account for 0.4% of the total portfolio fair.

“We are carefully monitoring the current headwinds caused by the labor shortages and supply chain disruptions. To date, we have not seen a material impact as many of our companies are services businesses, which have modest exposure to the manufacturing economy. For example, some of our largest sectors are software, insurance, and health care, which are not as exposed to the current economic headwinds. In line with last quarter, our nonaccruals remained low with only two investments on non-accrual status, representing 0.4% of the portfolio based on fair value. One of the lowest levels in the BDC sector and our annualized loss ratio is 14 basis points.”

ORCC’s portfolio is mostly larger middle market companies that would likely outperform in an extended recessionary environment.

“We also continue to grow the size of the companies in our portfolio. The weighted average EBITDA of our borrowers is now $114 million, which is up from $95 million a year ago. In addition to allowing us to invest more efficiently, we believe larger companies are safer to lend to, and that has been borne out by our results over the last five years.”

“We generally favor bigger companies for our portfolio. This year, we have already evaluated more than 20 opportunities over $1 billion in size, and invested in or committed to eight of these and continue to evaluate others. This trend continues to accelerate and is creating exciting opportunities for large direct lenders like Owl Rock. We believe we are especially well-positioned for this due to our scale platform with a full suite of financing solutions, large, deeply experienced team with strong relationships in the financial sponsor community.”

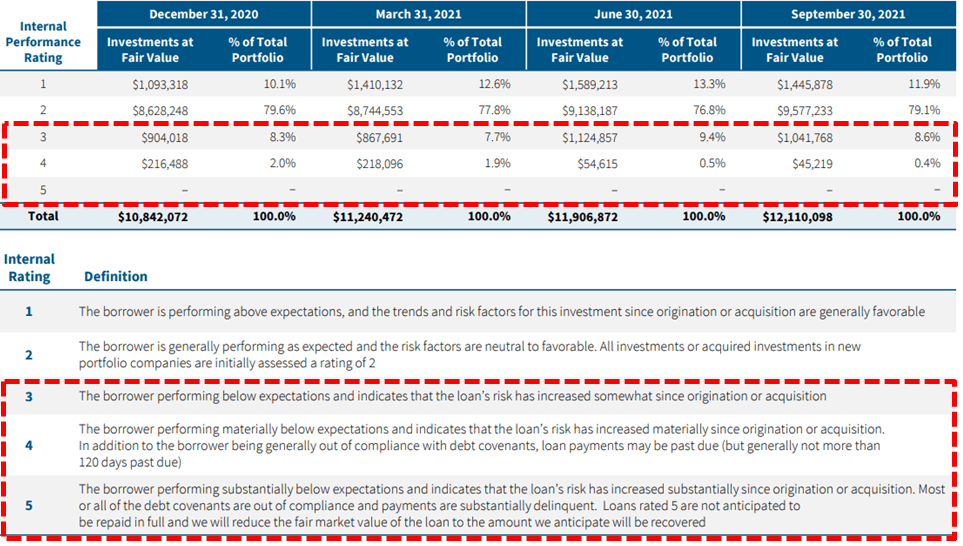

Investments Rating 3 or 4 which are borrowers performing “below” or “materially below” expectations indicating that the loan’s risk had increased “somewhat” or “materially” continue to decline and are now only 9.0% of the portfolio.

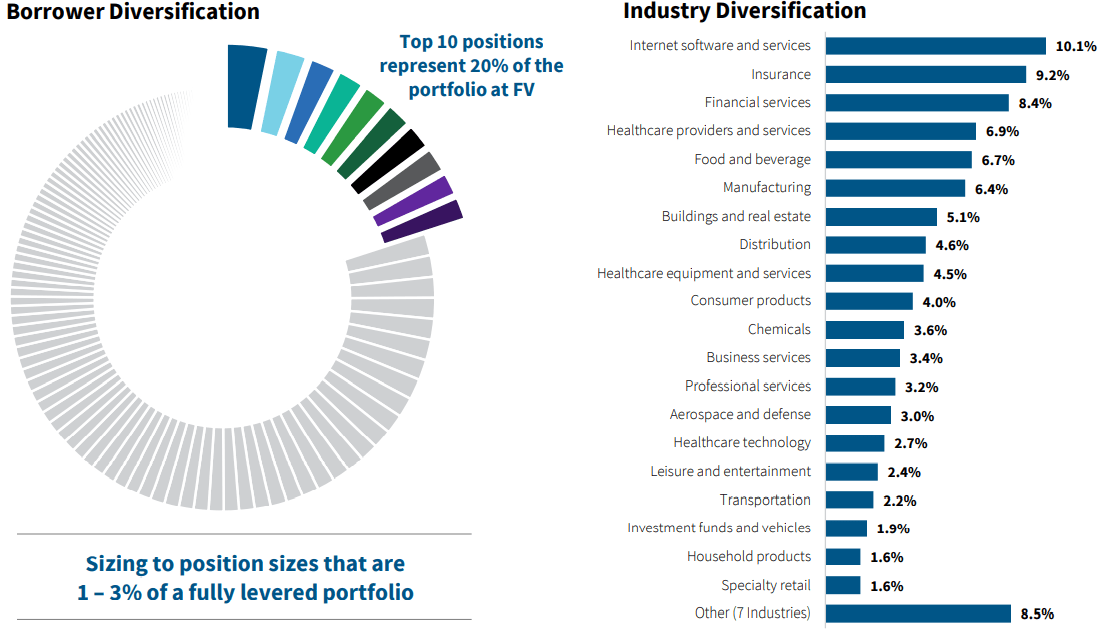

The portfolio is highly diversified with the top 10 positions accounting for around 20% of the portfolio with low cyclical exposure including retail, oil, energy, and gas.

During Q3 2021, its net asset value (“NAV”) per share increased by 0.4% due to overearning the dividend and unrealized portfolio appreciation including its equity position in Windows Entities. Please note that ORCC is for lower-risk investors with less equity participation in portfolio companies which typically drives NAV per share volatility for certain BDCs.

“Net asset value per share increased to $14.95, up $0.05 from last quarter. This increase was primarily driven by the growth in our net investment income, which exceeded our dividend by $10 million, as well as from $12 million of unrealized gains.”

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy to digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

Monday Morning Update – Before the markets open each Monday morning we provide quick updates for the sector including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

Deep Dive Projection Reports – Detailed reports on at least two BDCs each week prioritized by focusing on ‘buying opportunities’ as well as potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

Friday Comparison or Baby Bond Reports – A series of updates comparing expense/return ratios, leverage, Baby Bonds, portfolio mix, with discussions of impacts to dividend coverage and risk.

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying including setting target prices using the portfolio detail shown in this article (at a minimum) as well as financial dividend coverage projections over the next three quarters as discussed earlier.

The following information was previously provided to subscribers of Premium BDC Reports along with:

AINV target prices/buying points

AINV risk profile, potential credit issues, and overall rankings. Please see BDC Risk Profiles for additional details.

AINV dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

This update discusses Apollo Investment (AINV) which is one of the larger or at least more established BDCs that I do not write much about only due to being higher risk and typically not a good fit for longer-term investors. Management previously took on too much risk including concentration risk in the wrong sectors and there will likely be continued realized losses over the coming quarters including investments discussed in this article.

Setting Target Prices

Author’s Note: Many readers are constantly focused on BDCs trading at a “discount” or “premium” to net asset value (“NAV”) but not necessarily understanding the reasons. Trading at a premium is a good thing for longer-term investors. Buy more during market volatility to dollar average your purchases.

There are very specific reasons for the multiples that BDCs trade driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). Also, and this is very important, the price-to-book/NAV is highly dependant on the amount of dividends that a BDC is paying as a percentage of NAV (but also taking into account risk profile and projected dividends).

The following table shows each BDC roughly categorized into groups of paying below 7.5%, 7.5% to 9.0%, and over 10.0%. Again, there are ranges within these groups based on risk profile and projected dividends which is why most of my articles (including this one) discuss these categories providing the details so that readers can set appropriate target prices. AINV trades at a lower multiple (should be around 1.00 times NAV for the dividends paid) likely due to upcoming dividend coverage issues and realized losses discussed below. Also, using only the regular quarterly dividend of $0.31 per share would be $1.24 per annually which is only 7.7% of NAV and likely more appropriate given the direction of the portfolio toward lower yield assets (that is a good thing).

AINV Advisory Fee Agreement

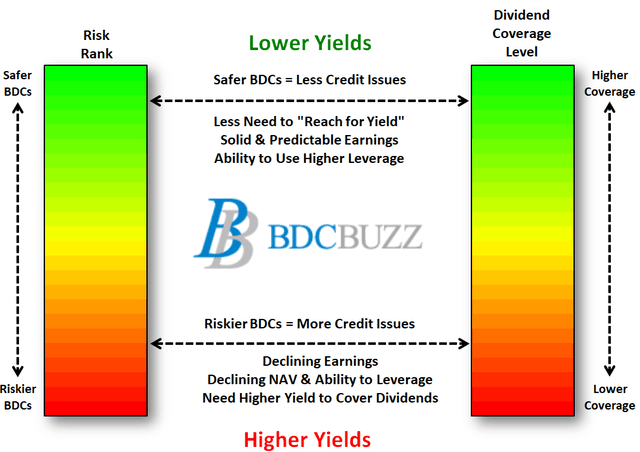

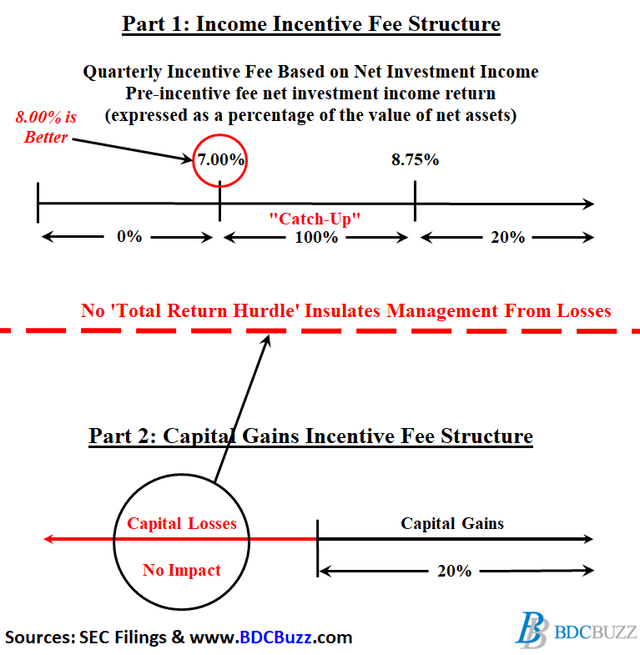

The older incentive fee structures can incentivize management to take on increased risk with investors’ capital. Management benefits from higher yields (through higher income incentive fees) with less risk related to future credit issues because capital losses are not included when calculating income incentive fees. This could encourage management to take higher risks (for increased yields) due to being insulated from potential capital losses when calculating the income portion of the incentive fees as shown in the diagram below. Ultimately, management could receive higher fees during periods of declining NAV per share, resulting in lower total returns to shareholders.

Many of the newer fee structures have a ‘total return’ hurdle taking into account realized/unrealized losses when calculating income incentive fees for management, with a look-back feature to keep management on the hook for the performance of investments over the long term.

Unfortunately, many of the higher risk BDCs do not have total return hurdles including Prospect Capital (PSEC) and more recently FS KKR Capital (FSK) which removed this feature as discussed earlier this month in “FS KKR Capital: Dividend Decrease Coming“.

However, AINV has higher quality management that previously added this feature to their fee agreement and as mentioned on the recent call:

The total return requirement closely aligns the incentives of our manager with the interest of our shareholders.”

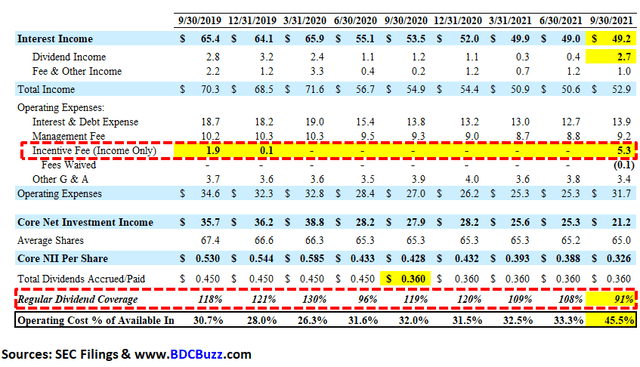

Since 2018, AINV has covered its dividend only due to no incentive fees paid driven by the total return hurdle and previous realized/unrealized losses. However, the company is now paying full incentive fees with a meaningful impact on dividend coverage as discussed later.

Net investment income for the quarter reflects a full incentive fee. Prior to the September quarter, AINV had not paid any incentive fee since the quarter ended December 2019. As a reminder, AINV’s incentive fee on income includes a total return hurdle with a rolling 12 quarter look back. Given the reversal of unrealized losses during the look back period, the manager earned a full 20% incentive during the quarter.”

Source: AINV Earnings Call

AINV Risk Profile Update

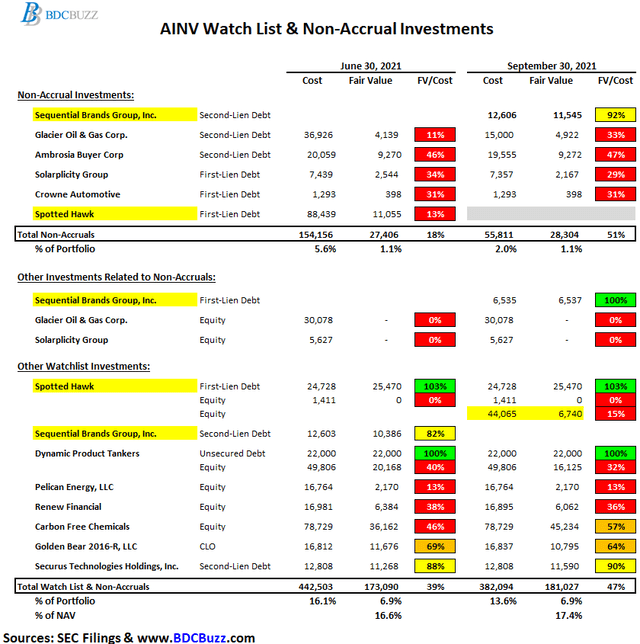

During calendar Q3 2021, its second-lien position in Sequential Brands Group, Inc. was added to non-accrual status but marked up during the quarter due to likely being resolved during Q4 2021:

Our second lien position in Sequential Brands was placed on non-accrual status during the quarter. Sequential Brands owns managers and licenses, a portfolio of consumer brands in the active and lifestyle categories. The company filed for Chapter 11 bankruptcy in August and is seeking an orderly liquidation of the brands in this portfolio. Our second lien position was marked at 92 at the end of September compared to 82 at the end of June. The mark at the end of September reflects the liquidation process and the resolution of our current position, which is expected to occur in the December quarter. At the end of September investments on non-accrual status totaled $28 million, or 1.1% of the total portfolio at fair value.”

Source: AINV Earnings Call

Sequential Brands is also held by FS KKR Capital (FSK) which is another higher-risk BDC and discussed this investment on its recent earnings call:

On November 3, the judge approved the sales without objections. We expect closing for the various sales to occur before November 14, proceeds leave to pay back a 100% of the DIP loans, we, and another lender provided fund a wind down reserve and provide a recovery on our loan. Pursuant to the contemplated transactions, we expect to receive a combination of cash, as well as newly structured debt and equity in the buyer of the active division.”

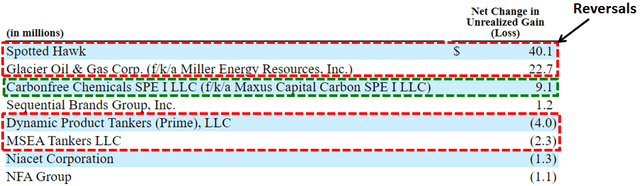

As predicted in the previous report there were additional realized losses of $65 million or $1.00 per share due to its non-accrual investments in Spotted Hawk and Glacier Oil & Gas. AINV has been working to restructure its first-lien position in Spotted Hawk which was converted to equity with no additional impact to its NAV per share and no longer on non-accrual status.

During the quarter Spotted Hawk completed restructuring of its balance sheet our second lien position tranche A was converted to equity in our third lien position tranche B was cancelled. Both of these positions were previously on non-accrual status. The valuation of our investment in Spotted Hawk was not impacted by this restructuring.”

Source: AINV Earnings Call

Source: AINV SEC Filing

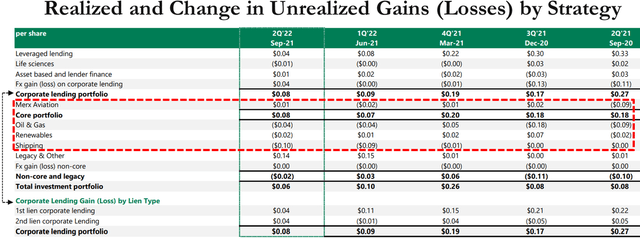

Non-accruals remain around 1.1% of the portfolio fair value due to adding Sequential Brands offset by restructuring Spotted Hawk and Glacier Oil & Gas as mentioned earlier. Again, there will likely be continued realized losses over the coming quarters including previously discussed investments some of which are included in the following table. These investments alone account for $201 million or $3.11 per share of previous unrealized losses but still account for almost 7% of the total portfolio fair value and 17.4% of NAV per share.

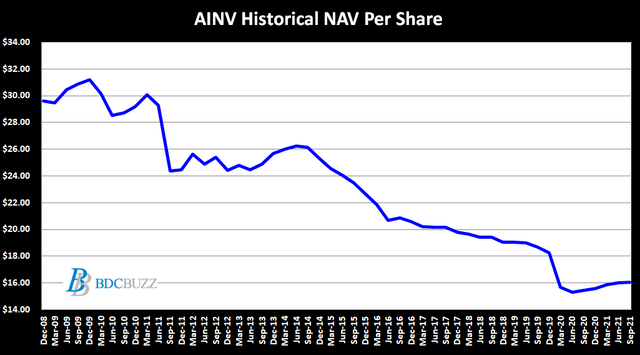

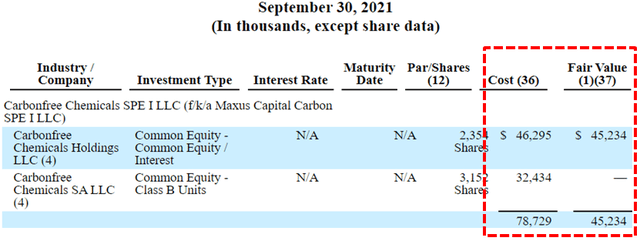

Net asset value (“NAV”) per share increased by $0.05 or 0.3% (from $16.02 to $16.07) mostly due to Carbonfree Chemicals (same as previous quarter) as well as accretive share issuances partially offset by shipping investments (same as previous quarter) Dynamic Product Tankers and MSEA Tankers and not adequately covering the dividends (missing by $0.034 per share).

We ended the quarter with net asset value per share of $16.07, up $0.05 or 0.3%, driven by our corporate lending portfolio, which continues to perform well as well as the accretive impact of stock buybacks. We’re in the September quarter or corporate lending, portfolio had a gain of $5 million or $0.08 per share partially offset by $1.3 million or $0.02 per share on non core and legacy assets. The net loss on non core and legacy assets reflects net losses on oil and gas renewables and shipping investments, partially offset by a gain on carbon-free legacy investments.”

Source: AINV Earnings Call

Source: AINV SEC Filing

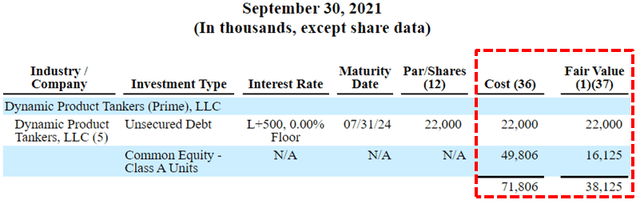

Same as the previous quarter, the largest markdown was its equity position in Dynamic Product Tankers which is a shipping business 85% owned by AINV (since 2015) discussed in previous reports. As shown below, AINV currently has a $22 million subordinated loan due July 2024 at a very low rate of LIBOR +500 basis points and continues to mark down its equity position currently 32% of cost accounting for almost $34 million or $0.52 per share of unrealized losses.

Source: AINV SEC Filing

Also discussed in previous reports, AINV restructured its first-lien loans to Carbonfree Chemicals and now owns 27% of the company. The equity portion has been marked up during the recent quarters and is now valued at 57% of cost but needs to be watched as it could result in higher (or lower) NAV over the coming quarters. Carbonfree produces proprietary technologies that capture and reduce carbon emissions by producing chemicals such as limestone and baking soda for sale or for long term storage and could benefit from the current administration.

Management discussed on the recent call:

Regarding carbon-free, as a reminder, our investment in carbon-free consists of an investment in the company’s proprietary carbon capture technologies and an investment in the company’s chemical plant. Carbon-free is benefiting from strong interest in carbon capture, utilization and storage as part of broader ESG trends. We believe carbon-free is a leader in this space, as evidenced by partnerships announced during the quarter, which demonstrate market acceptance for its technology.”

Source: AINV Earnings Call

Source: AINV SEC Filing

Source: AINV Earnings Presentation

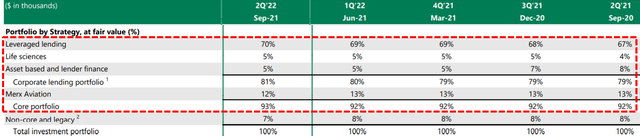

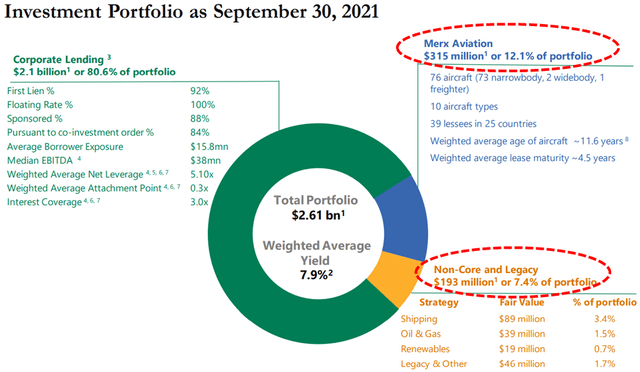

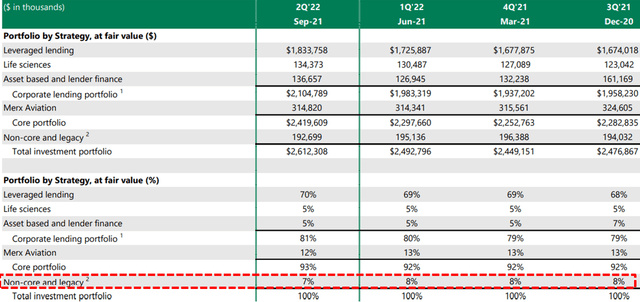

Since 2016, the company has been repositioning the portfolio into safer assets including reducing its exposure to oil & gas, unsecured debt, and CLOs. The “core strategies” portion of the portfolio remains around 92.6% of all investments and includes Merx:

We continue to make good progress increasing our exposure to first lien floating rate corporate loans, while reducing our exposure to junior capital and non-core positions. Repayments during the quarter included the exit to second lien investments, as well as a small partial pay down from one of our shipping investments. We remain focused on reducing our exposure to the remaining non-core assets, while ensuring an optimal outcome for our shareholders.”

Source: AINV Earnings Call

Source: AINV Earnings Presentation

Source: AINV Earnings Presentation

Its aircraft leasing through Merx Aviation remains the largest investment and is around 12% of the portfolio and was discussed on the call including “the level of lease revenue generated from our fleet has stabilized” and “continues to benefit from a growing servicing business which has increased in value over time”:

Moving to Merx. The overall air traffic environment appears to be improving, particularly in the US. We’re optimistic that demand for air traffic will continue to grow with the ongoing rollout of the vaccine and the lifting of travel restrictions. Furthermore, the aircraft leasing market will continue to be an important and growing percentage of the world fleet, as airlines will increasingly look at third-party balance sheets to finance their operating assets. Specific to our investment, as Howard mentioned, we believe Merx has successfully navigated the significant disruption caused by the COVID-19 pandemic. The level of lease revenue generated from our fleet has stabilized. We have worked through our exposure to airlines that have undergone restructurings. We have been able to remarket aircraft during the period with long term leases or sales. And Merx continues to benefit from a growing servicing business which has increased in value over time. Given the stabilization of Merx, during the quarter we recast at $4.5 million of Merx equity into debt, and as Howard mentioned, AINV received $6.9 million of interest income from Merx during the September quarter, $2.1 million more than last quarter. Merx remains focused on remarketing aircraft that are due to come off lease via extensions, with existing lessees releasing to other airlines on long term leases or sales. During the September quarter, Merx sold two aircraft and signed lease extensions for six aircraft. Our lease maturity schedule is well staggered. We believe Merx’s portfolio compares favorably with other major lessors in terms of asset, geography, age, maturity and lessee diversification. Merx’s portfolio is skewed towards the most widely used types of aircraft, which means demand for Merx’s fleet is anticipated to be resilient. Merx’s fleet primarily consists of narrow body aircraft serving both US and foreign markets. The Apollo aviation platform will continue to seek to opportunistically deploy capital. To be clear, Merx has focused on its existing portfolio, and is not seeking to materially grow its balance sheet portfolio.”

Source: AINV Earnings Call

Management was also asked about the impacts of inflationary pressure on its portfolio companies:

Q. “There’s some inflationary pressures and wage pressures, what’s the biggest risk economically as you’re thinking about as you’re deploying capital?”

A. “We’ve talked about over an extended period of time, the best defense to that is sort of granularity and diversity. So, that — like any of these risks don’t expose you across the portfolio. It’s why we’ve always said like one of the key aspects is to have a very wide funnel, have a diversity of products, and be able to be as selective as you can be in a market like this. It’s a very benign environment this minute. But you can see all sorts of things that could potentially come your way. So, we take a very — we take portfolio construction very seriously. And then on individual credits, try to look out at the specific risks we see coming to see how they can absorb.”

Source: AINV Earnings Call

AINV Dividend Coverage Update

Author’s Note: The following information was provided to subscribers along with 3 quarters of financial projections using base, best, and worst-case assumptions to test the sustainability of the current dividends.

On November 4, 2021, the Board declared a distribution of $0.31 per share plus a supplemental distribution of $0.05 per share payable on January 6, 2022, to shareholders of record as of December 20, 2021. Investors should expect dividend coverage to “fluctuate” over the coming quarters but management is committed to paying the regular quarterly distribution of $0.31 plus the supplemental distribution of $0.05 through March 31, 2022, as discussed on the recent call:

The board has declared a base distribution of $0.31 per share, and a supplemental distribution of $0.05 per share, both distributions are payable on January 6 2022, to shareholders as a record on December 20 2021. I’d like to remind everyone that as we’ve indicated previously, we intend to declare a quarterly based distribution of $0.31 per share, and a quarterly supplemental distribution of $0.05 per share for at least one more quarter.”

Source: AINV Earnings Call

As mentioned earlier, the distributions have been covered only through fee waivers and not paying the full incentive fees. However, the company is now paying full incentive fees with a meaningful impact on dividend coverage as predicted in previous reports.

Net investment income for the quarter reflects a full incentive fee. Prior to the September quarter, AINV had not paid any incentive fee since the quarter ended December 2019. As a reminder, AINV’s incentive fee on income includes a total return hurdle with a rolling 12 quarter look back. Given the reversal of unrealized losses during the look back period, the manager earned a full 20% incentive during the quarter. The total return requirement closely aligns the incentives of our manager with the interest of our shareholders.”

Source: AINV Earnings Call

AINV’s recurring interest income has recently declined to its lowest level over the last 15 years and is now below $50 million.

The quarter-over-quarter decline in interest income was attributable to the pace of the investment activity and a relatively higher yield on repayments versus fundings.”

Source: AINV Earnings Call

There was an additional $65 million of realized losses in calendar Q3 2021 due to its non-accrual investments in Spotted Hawk and Glacier Oil & Gas as discussed later. It is important to note that AINV has experienced over $760 million ofrealized losses over the last ~9 years which is around $11.75 per share using the current number of shares. A good portion of AINV’s previous and recent losses was due to higher amounts of exposure to cyclical sectors including extended stay hotels and oil/energy. However, other BDCs also had larger amounts of oil/energy exposure with much stronger NAV performance during the same period.

During calendar Q3 2021, AINV repurchased 450,953 shares at a weighted average price per share of $13.09, inclusive of commissions, for a total cost of $5.9 million. From October 1, 2021, through November 3, 2021, the company repurchased another 308,005 shares at a weighted average price per share of $13.30 for a total cost of $4.1 million. Since the inception of the share repurchase program, the company has repurchased 14,559,137 shares at a weighted average price per share of $16.15 for a total cost of $235.1 million, leaving a maximum of almost $15 million available for future purchases.

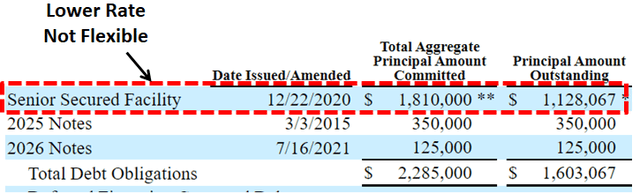

In July 2021, the company issued $125 million of 4.50% Notes due July 16, 2026, which increased the overall cost of borrowings but strengthened the balance sheet and is taken into account with the updated projections:

The increase in interest expense reflects both the growth in the portfolio, as well as an increase in our funding costs. As a reminder, in July, we issued $125 million of five year 4.5% unsecured notes, which drove the increase in our weighted average cost of funding from 3.08% to 3.2% quarter over quarter. Importantly, unsecured debt increase to 30% of our outstanding debt at the end of September, up from 24% last quarter.”

Source: AINV Earnings Call

However, it should be pointed out that having 70% of your borrowings consisting of secured credit facilities is not flexible relative to most higher quality BDCs. This is important if there is another market meltdown and BDCs have to temporarily mark down assets driving many issues including coverage ratios and borrowing covenants. Especially given that AINV currently has the highest leverage ratio (during good times). Also, as AINV refinances its balance sheet into more unsecured notes it will drive up its overall borrowing rates putting additional pressure on dividend coverage. Not ideal and needs to be watched.

Also taken into account is additional guidance from management on the recent call including:

Fee and prepayment income totaled $1.7 million dollars for the quarter. Although these sources of income can fluctuate from quarter-to-quarter, we expect to generate approximately $3.5 million of fee and prepayment income per quarter on average. As an illustration, in a March 2021 and June 2021 quarters, fee and prepayment income totaled $3.9 million and $5.9 million respectively.”

“We continue to focus on monetizing underlying assets, specifically Spotted Hawk, dynamic, MC and Chiron. Taken together these assets and a few others account for approximately $230 million of fair value and generate only $16 million of annual income, redeploying those assets that are approximate on euro yield to generate an incremental $2 to $3 million of annual net investment income.”

“We continue to generate incremental cash proceeds from the portion of our non-core assets that are non-generating income. For every $10 million of cash we generate from these non-income producing assets, we can generate approximately $650,000 of annual net investment income, or approximately $0.01 per share. In this regard, we have generated incremental cash each quarter and are very focused on executing some more significant process in the coming — progress in the coming quarters.”

Source: AINV Earnings Call

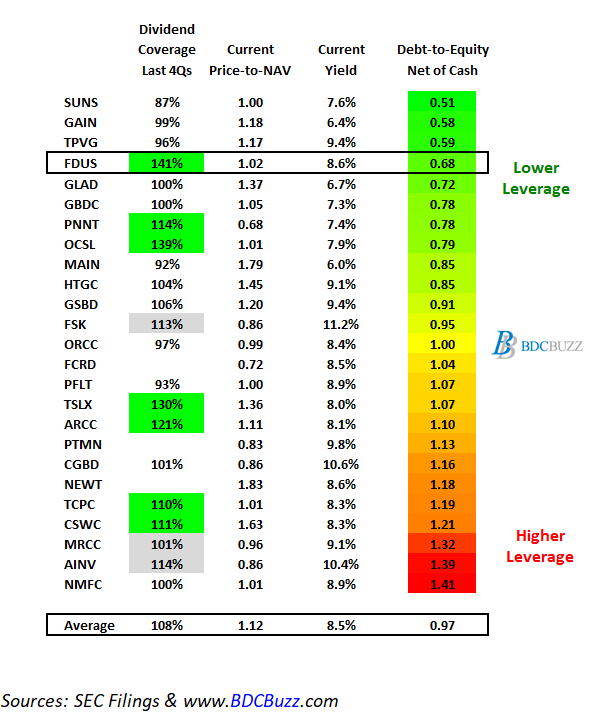

Management has guided for portfolio growth using increased leverage which is already the highest in the sector at 1.52 debt-to-equity (net of cash) compared to the average BDC currently around 0.96.

Given this solid level of activity, our investment portfolio grew and our net leverage ratio increased to 1.52 times at the end of September, right in the middle of our target leveraged range of 1.40 times to 1.60 times. As we look ahead, we are confident in our ability to grow our portfolio and operate within our target leverage range, given the tremendous need for creative and flexible private capital.”

Source: AINV Earnings Call

Previously, AINV was considered a ‘Level 4’ dividend coverage BDC implying that a dividend reduction was imminent mostly related to needing higher leverage as well as the reliance on fee waivers to cover the quarterly dividend. On August 6, 2020, the company announced a decrease in the regular quarterly dividend per share from $0.45 to $0.31.

From previous call: “Turning to our distribution, in light of the challenges and uncertainty created by the COVID-19 pandemic and our plans to further reduce the funds leverage, we have reassessed the long-term earning power of the portfolio and included that as a prudent to adjust the distribution at this time. We believe that distribution level should reflect the prevailing market environment and be aligned with the long-term earnings power of the portfolio. Going forward in addition to a quarterly based distribution, the company’s Board expects to also declare supplemental distribution and an amount to be determined each quarter.”

Over the coming quarters, AINV could be downgraded depending on the progress of rotating out of “non-earning and lower-yielding assets” and improved results/income from its investment in Merx Aviation.

Management mentioned that the $2.1 million dividend income received in calendar Q3 2021 will likely fall back to previous levels and is taken into account with the updated projections:

We believe Merx has successfully navigated this challenging period. As a result, AINV earned more income from Merx during the September quarter compared to recent quarters. As a result of the stability we expect to continue to see from Merx, during the recorder, we recap the capital structure and receive $6.9 million of interest income from Merx during the September quarter, $2.1 million more than last quarter. We earned a $2 million dividend from MSEA Tankers during the September quarter, we expect to earn approximately $1 million on average going forward, a level consistent with prior periods.”

Source: AINV Earnings Call

Source: AINV Earnings Presentation

Article Summary & Recommendations

Assess investor profile

Set target prices based on expected risk and dividends paid

Purchase additional shares during market volatility

First of all, please assess whether you are a “trader” and a “buy and hold” investor. The difference is how long you plan to hold certain investments, your overall appetite for risk, and expected returns. Traders typically have a higher risk tolerance but also expect higher returns. Personally, I am a buy and hold longer-term investor but continue to buy each time the market pulls back constantly reinvesting my dividends building positions in higher quality BDCs that easily outperform due to having higher quality management. I currently have 18 BDC positions some of which have been discussed in my recent public articles. I will try to cover the remaining positions in upcoming articles.

As mentioned earlier, most BDCs have recently issued very low rate unsecured notes and refinanced their balance sheets taking some short-term hits but locking in some strong quarters coming up. Q4 is typically the busiest for portfolio turnover driving higher fees and prepayment-related income which has been discussed on many of the recent earnings calls. There is a good chance that is why BDC prices have continued higher. Also, most of my ‘Level 1’ dividend coverage BDCs have recently announced dividend increases and/or supplemental/special dividends.

As for AINV, please do your due diligence including setting target prices using the portfolio detail shown in this article (at a minimum) as well as financial dividend coverage projections over the next three quarters as discussed earlier. AINV is a higher risk BDC due to previous and upcoming realized losses as well as not ideal sector exposures (similar to FSK) but management is actively working to clean up the portfolio (seems to be taking a very long time in my opinion). The company is likely trying to maximize shareholder value and at least has an incentive fee structure that partially aligns management with the shareholders.

AINV trades at an 18% discount to NAV currently paying $0.36 per share of quarterly dividends which is an 11% annual yield compensating investors for a not-so-certain future of upcoming dividends and/or realized losses. Not my cup of tea and would much rather own a BDC trading at a premium to NAV with a lower cost of capital and a lower dividend yield (before taking into account upcoming dividend increases).

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy to digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

Monday Morning Update – Before the markets open each Monday morning we provide quick updates for the sector including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

Deep Dive Projection Reports – Detailed reports on at least two BDCs each week prioritized by focusing on ‘buying opportunities’ as well as potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

Friday Comparison or Baby Bond Reports – A series of updates comparing expense/return ratios, leverage, Baby Bonds, portfolio mix, with discussions of impacts to dividend coverage and risk.

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying including setting target prices using the portfolio detail shown in this article (at a minimum) as well as financial dividend coverage projections over the next three quarters as discussed earlier.

The following information was previously provided to subscribers of Premium BDC Reports along with:

TPVG target prices/buying points

TPVG risk profile, potential credit issues, and overall rankings. Please see BDC Risk Profiles for additional details.

TPVG dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

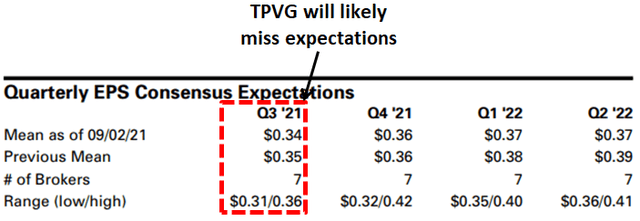

TPVG Potential Earnings Miss for Q3 2021

There is a chance that TPVG will miss upcoming earnings expectations for Q3 2021 due to the following which are taken into account with the updated projections and discussed later in this report:

Lower prepayment-related income.

Previous lower leverage and underinvested portfolio.

Underutilization of its lower cost credit facility resulting in higher “unused fees” and higher blended borrowing rates.

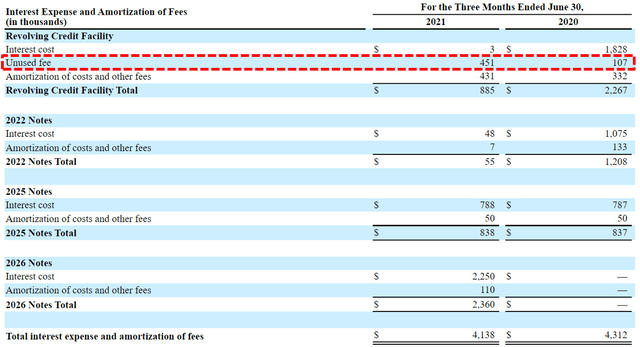

As shown below, TPVG paid $451,000 of unused credit facility fees in Q2 2021 which impacted earnings by around $0.015 per share. As the company uses higher leverage by utilizing the lower cost credit facility it will have a meaningful impact on earnings through portfolio growth and lower fees.

Given the current market with increased merger/SPAC activity, I am expecting TPVG to continue to be underleveraged, supporting the regular dividend using the previous spillover, and less likely to pay a supplemental in 2021.

“As you can see there hasn’t been a slowdown in exit activity within our portfolio, in fact, we continue to have more than it does in TPVG portfolio companies actively exploring IPOs, SPAC mergers or M&A which if consummated could unlock substantial additional value for our shareholders from our equity and warrant portfolio.”

Of course, there is always a good chance that there will be some significant realized gains from many of its equity positions but these would likely be used to pay additional supplemental dividends in 2022. On the recent earnings call management mentioned continued gains from its equity/warrant positions including Revolut Ltd as discussed later that will likely drive an increase in NAV per share for Q3 2021:

“Although we have not completed our fair value process for Q3 we estimate TPVG’s equity and warrant investments to be valued between $10 million and $20 million, up from $1.8 million as of Q2 or an increase between $0.25 and $0.60 per share to net asset value. While still unrealized realized gains, this is another great development in the TPVG portfolio, but more importantly, not the only one that we believe will deliver meaningful gains as we have many portfolio companies and our heads down and doing great things. Clearly, we are excited by the outlook for both unrealized and realized gains on the equity and warrant portfolio which position us to provide shareholders with capital gains and to grow net asset value but we’re also pleased with the solid credit outlook and the strong yield profile for the portfolio.”

“During the second quarter, we also received warrants valued at $2.2 million in seven portfolio companies in conjunction with our debt commitments as compared to receiving warrants valued at $1.6 million in 13 companies last quarter. This increase demonstrates that we are capturing more equity upside potential from our portfolio companies, while still raising the bar on yield. During the quarter, Talkspace completed their SPAC merger and as at the end of the quarter, we have a total unrealized gain of 600,000 based on our warrant and equity positions in the company even though the company never drew on their deadline and there unfunded commitment expired, unused. This brings TPVG’s totaled to three successfully completed SPAC mergers, we also have five portfolio companies with the announced SPAC mergers and process. Bird, Enjoy, Inspur auto, and Sonder all announced their SPAC in Q2, and live learning technologies announced its back during the first quarter. Our cost basis in equity and warrants in these five companies totals $1.7 million with a fair value of $3 million as of Q2. Generally, we do not mark up our investments in these type of situations until merger exchange ratios are announced. And then we further discount the fair values given the uncertainty associated with their completion.”

As discussed in previous reports, TPVG’s dividend coverage needs to be assessed on an annual basis due to the lumpy nature of earnings from successful portfolio companies prepaying loans. This results in certain periods of higher prepayment fees driving higher earnings often followed by lower earnings due to being underleveraged and not having a fully invested portfolio.

Previous call: “I would like to remind everyone that while prepayments are a natural part of our venture lending model, it does come with a great deal of uncertainty. One of the other aspects of prepayment activity is that the origination vintage of alone that prepays really does matter. Given the nature of income acceleration when a loan prepays, the characteristics of income changes, the longer the loan remains outstanding, for example, should alone repay or prepay in its first year, we would generally recognize a comparatively higher level of income.”

This is what happened in Q1/Q2 2021 driving interest income well below previous levels as the company continues to experience higher repayments (mostly due to investing in successful portfolio companies) but not as much prepayment-related income resulting in reduced dividend coverage mostly due to “lower weighted average principal outstanding on our income-bearing debt investment portfolio”.

“Our earnings were impacted by the significant prepay activity we’ve experienced over the past several quarters on our overall portfolio size, despite strong new commitments, growing investment funding and stable core portfolio yield is in the past. We believe any shortfall is temporary and will be more than made up during the rest of the year as the fundamentals of our industry.”

As of June 30, 2021, the company’s unfunded commitments totaled $163.5 million and through August 4, 2021, had closed $15.7 million of additional debt commitments, funded $18.2 million in new investments offset by $18.2 million of prepayments driving $0.4 million of accelerated income. However, management is expecting lower prepayments combined with a strong pipeline of new investments and signed term sheets that should drive portfolio growth in Q3/Q4 2021 taken into account with the updated projections.

“As we look to the second half of this year in terms of prepayment activity from our core equity raises we’re seeing a little more balance from portfolio companies that are fundraising or that are closing fund-raises, they’re either waiting to pay off the debt, they’re either not paying off the debt or we’re talking with them about creative ways to keep the debt outstanding which we think will then translate into meaningful portfolio growth. Our large pipeline strong levels of signed term sheets increasing commitment growth, higher utilization rates, and meaningful levels of unfunded commitments are great indicators for near-term portfolio growth, which we believe will enable us to cover the distribution on a quarterly basis this year, but we’re not going to force portfolio growth unnaturally.”

“The most notable progress is a continued rise we are seeing in signed term sheets, which was one of the highest quarterly totals in TPVG’s history. Additionally, our pipeline increased 50% over last quarter and is more than doubled since a year ago. We have substantial liquidity to meet this increased demand and we’re on course to achieve the growth targets we outlined for the second half of the year and drive consistent long-term growth of investment income in net asset value. So far we have funded over $18 million of new loans here in the third quarter. Consistent with prior guidance, we expect gross fundings for Q3 and Q4 to come in between $100 million and $150 million per quarter, which is supported by our pipeline, our backlog of signed term sheets, high utilization rates of new commitments at close, sizable unfunded commitments as well as the pattern of our portfolio companies drawing on existing unfunded commitments towards the second half of the year.”

Q. “In your comments, did you say that you expect the quarterly EPS to cover the dividend in the second half?”

A. “I didn’t say that. What I was what our trend will be is to originate to get to a level where it’s sustainable. So, we clearly need to get to the $100 million, $150 million in the third and fourth quarter. And then we’re on track for doing that.”

Last month, the Board reaffirmed its quarterly distribution of $0.36 per share for Q3 2021, and dividend coverage will continue to improve partially due to the recent/previous reductions in borrowing rates as well as growing the portfolio using leverage from its credit facility.

“During the second quarter, the company recorded a one-time $681,000 or $0.02 per share net realized loss on extinguishment of debt. This was the result of the full redemption on April 5th of our baby bonds. With this redemption complete, we expect a positive effect to earnings as we continue to lower our cost of capital going forward.”

“The most notable progress is a continued rise we are seeing in signed term sheets, which was one of the highest quarterly totals in TPVG’s history. Additionally, our pipeline increased 50% over last quarter and is more than doubled since a year ago. We have substantial liquidity to meet this increased demand and we’re on course to achieve the growth targets we outlined for the second half of the year and drive consistent long-term growth of investment income in net asset value.”

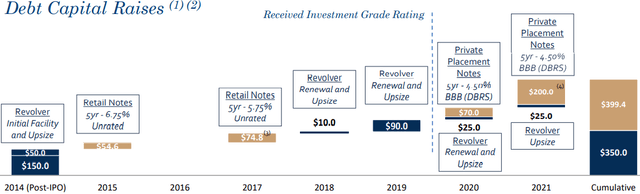

On March 1, 2021, TPVG closed a private offering of $200 million 4.50% institutional unsecured notes due 2026, and used a portion of the proceeds to redeem its 5.75% Baby Bond (TPVY) lowering its overall borrowing rates. Leverage remains low due to previous early repayments driving a debt-to-equity ratio of 0.59 net of cash giving the company plenty of growth liquidity. It should be noted that TPVG is one of the only BDCs currently with 100% unsecured borrowings giving the company much more flexibility over the coming quarters:

TPVG Risk Profile Quick Update

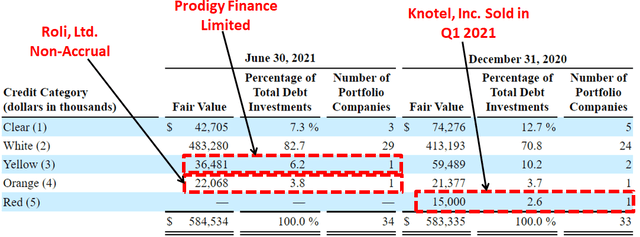

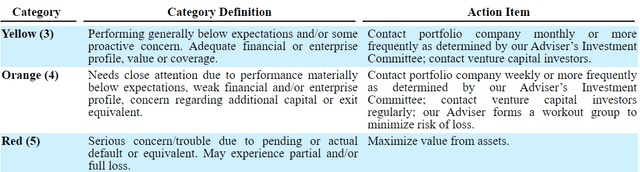

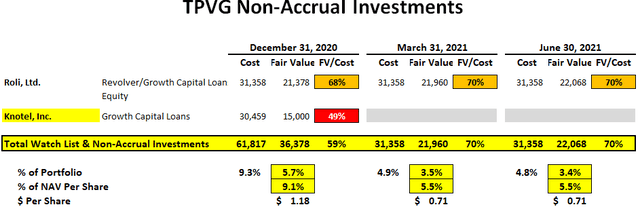

TPVG maintains a credit watch list with portfolio companies placed into one of five categories, with Clear, or 1, being the highest rating and Red, or 5, being the lowest. Generally, all new loans receive an initial grade of White, or 2. Knotel was its only Red (5) and was sold during Q1 2021, Roli, Ltd. is its only Orange (4) and remains on non-accrual status, and Prodigy Finance Limited is its only Yellow (3) and needs to be watched. Please see the description of categories and discussion of Prodigy and Roli below.

“Moving on to credit quality, the credit outlook for our portfolio remains strong with 90% of our debt investments in our top two categories, consistent with Q1, no obligor’s were added to categories, three, four and five, and no obligor’s were placed on non-accrual during the second quarter. In fact, the weighted average investment ranking of our debt investment portfolio improved to 2.06 compared to 2.11 as at the end of Q1. During the quarter, one company was upgraded from category 3 to category 2 as a result of completing a financing, leaving only one company in category 3 which is Prodigy finance in international graduate student lending company. During Q2 Prodigy paid down $5 million on outstanding loans to us and we’re pleased to report that here in Q3, Prodigy completed its first securitization issuing $228 million of investment-grade asset-backed securities and are remaining loans will now switch from PIK interest to cash pay interest. Based on these and other developments that Prodigy, we expect to upgrade them to category 2 here in Q3. Our one category 4 portfolio company really continues to be our only loan on non-accrual and our mark was flat with last quarter prior to currency fluctuations.”

Roli, Ltd. was discussed on a previous call:

“If you look at the value accreted quarter-over-quarter for ROLI, so it’s not out of the woods, but if you’ve seen some very favorable product reviews, and some awards that they won for their product in Q4. So we continue to be balanced, but we feel again, conditions continued to improve at ROLI.”

Revolut Ltd announced the closing of an $800 million private equity raise at a $33 billion valuation driving an estimated fair value range of TPVG’s equity and warrant investments of approximately $10 million to $20 million, up from a combined fair value of $1.8 million at June 30, 2021. As mentioned earlier this will likely drive an increase in NAV per share for Q3 2021:

“Revolut, as an example, recently announced the closing of an $800 million equity round at a $33 billion valuation. Positive trends and our excitement in these technology sectors, if you can’t tell, continues. We foresee substantial equity fundraising activity in the venture capital industry as a whole and within our portfolio in particular. It’s a testament to our portfolio’s quality. We believe future venture lending opportunities are large and plentiful given today’s environment. This robust industry-wide equity financing activity continues to create demand for debt to compliment or top off an equity raise in some cases. “Although we have not completed our fair value process for Q3 we estimate TPVG’s equity and warrant investments to be valued between $10 million and $20 million, up from $1.8 million as of Q2 or an increase between $0.25 and $0.60 per share to net asset value.”

During Q2 2021, Bird Rides, Inc., Enjoy, Inc., Inspirato LLC and Sonder, Inc. announced plans to go public through SPAC mergers and Groop Internet Platform, Inc. (Talkspace) closed its SPAC merger.

During Q1 2021, Hims & Hers, Inc. and View, Inc. closed their SPAC mergers and GROOP Internet Platform, and Live Learning Technologies announced plans to go public through SPAC mergers.

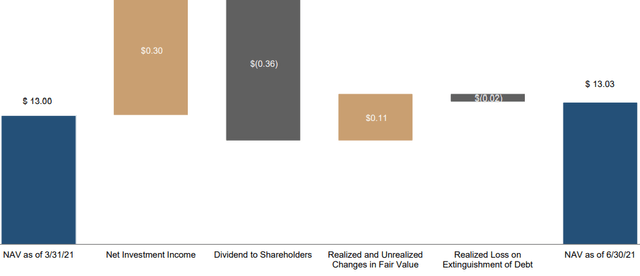

For Q2 2021, TPVG’s net asset value (“NAV”) per share increased slightly by 0.2% mostly due to portfolio unrealized gains partially offset by losses related to redeeming its Baby Bond as discussed earlier as well as under-earning the dividend.

“Net unrealized gains on investments for the second quarter were $3.2 million or $0.10 per share, resulting primarily from favorable fair value adjustments on debt investments of $1.9 million on warrant and equity investments of $800,000 and favorable changes in foreign exchange rates of $500,000. During the second quarter, the company recorded a one-time $681,000 or $0.02 per share net realized loss on extinguishment of debt. This was the result of the full redemption on April 5th of our baby bonds.”

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy to digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.