The following is a quick update that was previously provided to subscribers of Premium Reports along with target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs (including this one) please see Deep Dive Reports.

As predicted in the recently updated CGBD Deep Dive report, CGBD announced a special dividend of $0.20 per share yesterday payable on January 17, 2019 to stockholders of record as of December 28, 2018.

“We are pleased to announce a year end special dividend to our shareholders of $0.20 per share. We have also paid/declared $1.48 per share in regular dividends in 2018 year to date.” commented Michael Hart, Chairman and Chief Executive Officer.

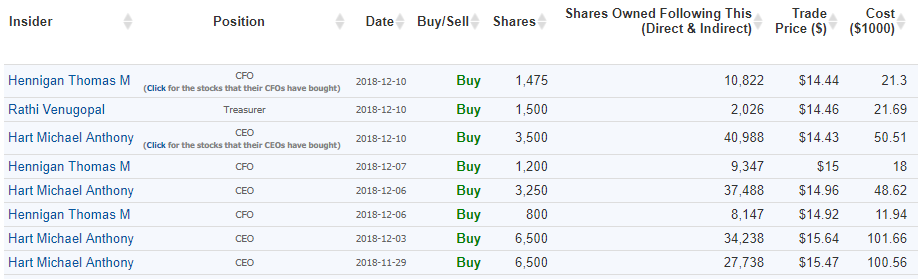

Also, the CEO, CFO & Treasurer have made additional purchases this week:

CGBD Pricing & Recommendations:

For target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs (including this one) please see Premium Reports.

CGBD Reduced Asset Coverage Ratio:

On June 6, 2018, CGBD had its 2018 Annual Shareholder Meeting and the Board was asking stockholders to approve the application of the 150% minimum asset coverage ratio. As shown below, the “required majority” of shareholders voted for Proposal 3 and the 150% minimum asset coverage ratio became effective as of June 7, 2018.

What does this mean for shareholders and upcoming dividend coverage?

Clearly more leverage implies higher risk and hopefully higher returns. It mostly comes down to how much additional leverage and the quality of assets in the portfolio. However, there are a few other considerations:

- Reduced base management fee to 1.00% on assets financed with debt-to-equity over 1.0

- Less need for frequent equity offerings as management can increase leverage during periods of lower stock prices

- Ability to take on lower yielding assets

- Larger portfolio would likely result in more diversification and/or the ability to take on larger (usually higher quality) investments

- Higher leverage will likely require BDCs to diversify funding sources using ‘matching’ and a mix of lower cost utilized credit lines (less unused fees)

On the previous call, CGDB management discussed the potential for increased leverage:

“In April, our Board of Directors unanimously approved the adoption of the new BDC leverage bill and our shareholders overwhelmingly approved its adoption through a proxy process that coincided with our year-end annual shareholder meeting, and resulted in the 150% asset coverage ratio becoming affective on June 7th this year. As we’ve mentioned previously we don’t anticipate the adoption to the reduced asset coverage requirement to influence or change of the investment thesis that we’ve applied since our company’s inception. We’ll continue to invest where we see best relative value and our portfolio construct shouldn’t change in any material way going forward.”

“Our debt-to-equity at the end of the second quarter was 0.76 up modestly from the 0.70 ratio at the end of the first quarter. We previously provided guidance the outer boundary for our owned businesses leverage would be in the area of 1.30 to 1.40. Obviously we’re comfortably inside those levels currently, but we continue to believe that those are prudent out our boundaries given the overall risk in our portfolio today. Retroactively to July 1st of this year our investment advisor and has reduced the base management fee from 1.5% to 1% on all assets financed with greater than 1:1 leverage. This reduction in management fee, which as you know has been implemented post the shareholders approval of the new leverage guidelines is another good example of Carlyle’s philosophy around shareholder alignment.”