The following information was previously provided to subscribers of Premium BDC Reports along with:

- CGBD target prices/buying points

- CGBD risk profile, potential credit issues, and overall rankings

- CGBD dividend coverage projections and worst-case scenarios

This update discusses TCG BDC (CGBD) and was previously posted on our new platform with updated target prices, dividend projections, rankings, and recommendations:

- Full CGBD Report: CGBD Recent Pullback, Updated Projections & Pricing

Summary

- We have recently updated the dividend coverage projections and target pricing to take into account March 31, 2021, reported results as well as guidance provided by management on the recent earnings call.

- Included in the projections are the expected upcoming supplemental dividends.

- CGBD is currently one of the highest-yielding BDCs even compared to higher-risk companies such as PSEC, AINV, MRCC, and FSK.

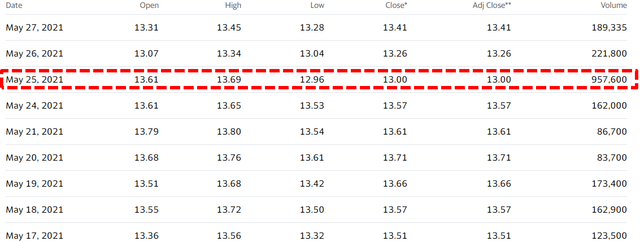

- As shown below there was a recent pullback in the stock price on May 25, 2021, with increased trading volumes (around five times the average daily volume).

- Non-accruals remain around 3.3% of the portfolio but I am expecting improvements for Direct Travel and Derm Growth which account for a majority.

- PIK increased during Q1 2021 (now 5.2% of total income) and needs to be watched.

Recent CGBD Pullback

As discussed last week, there was a recent pullback in CGBD’s stock price on May 25, 2021, with increased trading volumes (around five times the average daily volume). The pullback was likely just a selling shareholder followed by profit-taking maybe fear-driven due to the spike in volume.

The recent drop is responsible for CGBD currently having one of the lowest RSIs and highest yields in the sector.

CGBD Distributions Quick Update

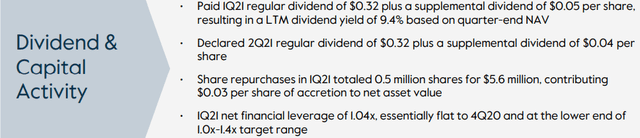

On May 4, 2021, the company announced a regular quarterly common dividend of $0.32 plus a supplemental dividend of $0.04, which are payable on July 15, 2021, to common stockholders of record on June 30, 2021. It should be noted that this was slightly below my base projected supplemental of $0.05.

On previous calls, management has mentioned “paying out a majority of the excess income above the $0.32 and we would anticipate doing the same going forward”:

“We generated net investment income of $0.36 per common share and declared a total dividend of $0.36. This includes the base dividend of $0.32 and a $0.04 supplemental dividend. As we have noted before, we expect earnings to continue to be well in excess of our $0.32 base dividend.”

“Similar to last quarter, as we look forward to the rest of 2021, we remain very confident in our ability to comfortably deliver the $0.32 regular dividend, but continue the sizable supplemental dividends. In line with the $0.04 to $0.05 we have been paying the last few quarters.”

Previous reports predicted a reduction in the regular quarterly dividend (from $0.37 to $0.32 per share) due to lower income from its Credit Fund I, declines in portfolio yield and interest income primarily due to the decrease in LIBOR and additional loans placed on non-accrual as well as the need to reduce leverage.

Upcoming CGBD Share Repurchases

On November 2, 2020, the Board authorized an extension as well as the expansion of its $150 million stock repurchase program at prices below NAV per share through November 5, 2021. The company previously repurchased around $86 million worth of shares but “paused” in Q2 2020. CGBD has reduced its debt-to-equity ratio increasing liquidity and management “intends to pursue the appropriate balance of both share repurchases and attractive new investment opportunities”. During Q1 2021, the company repurchased 0.5 million common shares at an average price of $12.03 per share, or $5.6 million, resulting in accretion to net assets per share of $0.03. As of March 31, 2021, there was $47.6 million remaining under the stock repurchase program. Management discussed on the recent call including less share repurchases as the stock price continues higher and I have taken into account with the updated projections:

“Additionally, we repurchased almost $6 million of our common stock at an average discount of 22% of our net asset value. This resulted in $0.03 of accretion to net asset value. We continue to be consistent active repurchasers of our shares. We continue to be consistent re-purchasers of it, but we will obviously scale those who purchases based on how accretive they are overall, and that will fluctuate as our as our stock price fluctuates. So, it shouldn’t be a surprise that we purchased a bit less this quarter. Repurchasing our shares was a bit less accretive this quarter than it had been in prior quarters. But nevertheless, again we continue to see great value in our shares. So, you should continue to see repurchases at least in the near future. And we have just as a side note, we have plenty of room and plenty of time left on our repurchase authorization that the Board gives us each year.”

Full BDC Reports

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.