The following is a quick update that was previously provided to subscribers of Premium Reports along with business development companies (“BDC”) target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs.

Summary

- A typical advisor charges 1% or more of the portfolio value per year for what most people can do themselves.

- Interest rates will likely remain low, and investors will continue to have equity investments to generate an adequate yield from their portfolios.

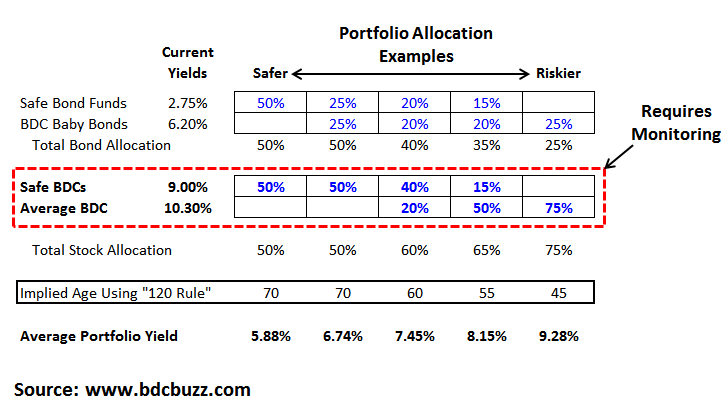

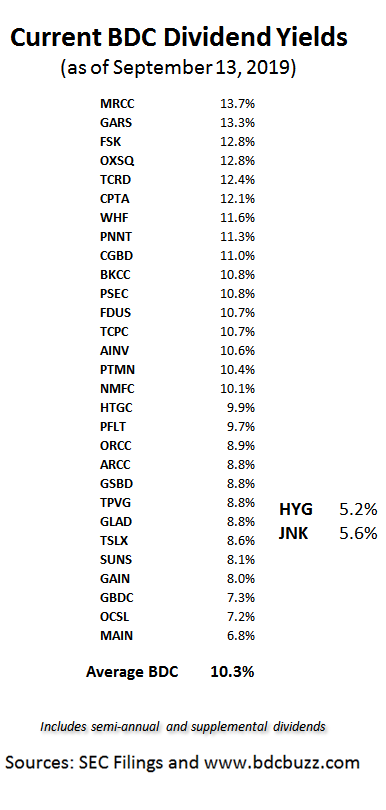

- BDC stocks are averaging 10.6% annual yields and their safer Baby Bonds are averaging 6.2% and this update discusses allocations of each for a balanced portfolio.

Typical Steps to Creating a Retirement Portfolio

- Set a realistic budget.

- Calculate the amount of pre-tax income needed from your investment portfolio.

- Assess risk tolerance including asset allocations.

A typical advisor charges 1% or more of the portfolio value per year for what most people can do themselves. To keep it simple, this article uses corporate/government bond funds and Baby Bonds that pay a set amount of interest and return the principal at the end of the period. These securities are less volatile and less risky than stocks.

- Please see below for discussions of yield and allocations.

How much of your portfolio should be in stocks and bonds?

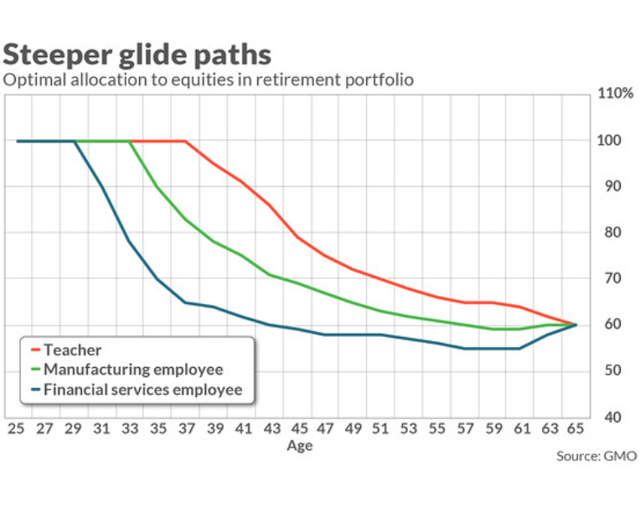

Your portfolio allocations depend on a few factors, including your age. Historically, investment advisors used the “100 minus your age” axiom to estimate the stock portion of your portfolio.

- For example, if you’re 50, 50% of your portfolio should be in stocks.

That has been revised to 110/120 due to the change in life expectancy and lower interest rates for risk-free and safer investments. Today, 10-year treasury-bill yields just over 2% annually compared to 10% in the early 1980s. Please see Bloomberg article “U.S. Is Heading to a Future of Zero Interest Rates Forever” from earlier this week.

For the table above, I have used 120 as I believe interest rates will remain low given the various policies from central banks and investors will continue to have equity investments for an adequate yield from their portfolios.

- For example, if you’re 50, 70% of your assets should be in stocks.

- For further reading on allocations, try stock allocation rules from Investopedia and Determining Asset Allocation By Age

The following chart uses a different approach that seems more aggressive and is discussed in “Is your retirement portfolio too heavily invested in equities?” from MarketWatch earlier this month.

Bond Funds & Baby Bonds

There are plenty of choices when it comes to bonds, including government bonds such as treasuries, municipal bonds, or corporate bonds. Within each of those categories, there is a wide variety of maturities to select from, ranging from a matter of days to 30 years or more. And, there is a full range of credit ratings, depending on the strength of the bond’s issuer.

To make it easy, many investors use a bond-based mutual fund or ETF that fits their needs. The primary reasons for allocating a portion of your portfolio to bonds are to offset the stock volatility and a reliable income stream as compared to capital gains or beating the market.

For my portfolio, I have various bonds some of which are related to my personal tax situation and likely not applicable to most.

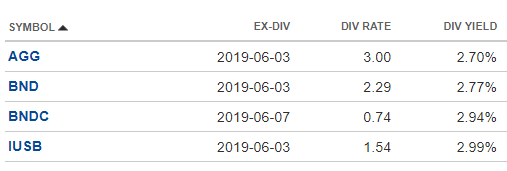

Below is a list of typical safer investment-grade bond funds currently with annual yields around 2.7% to 3.0%. I will discuss further in upcoming posts if subscribers are interested, let me know in the comments.

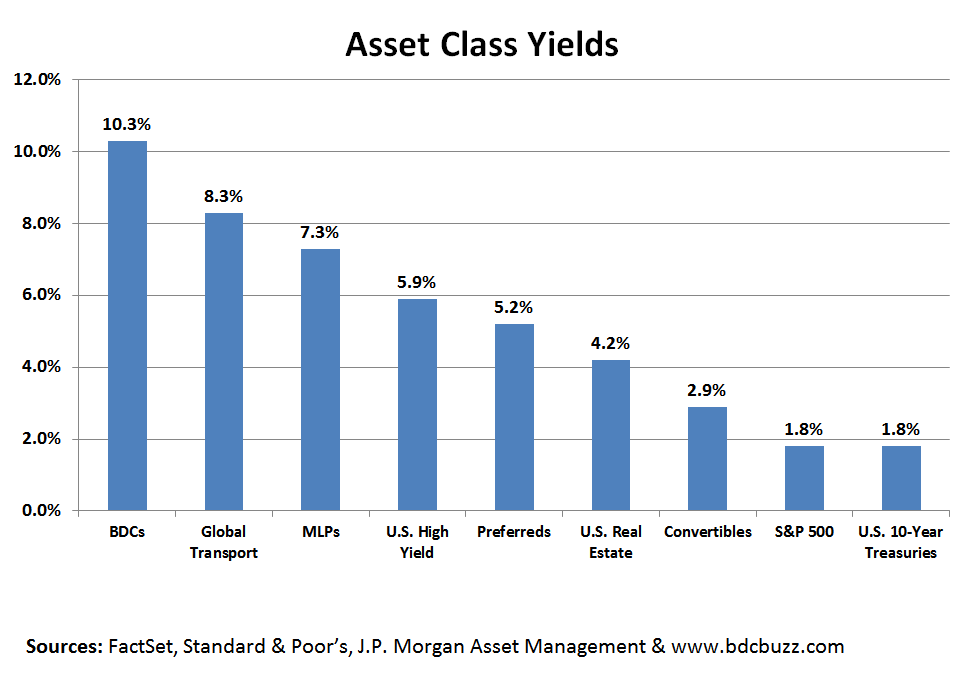

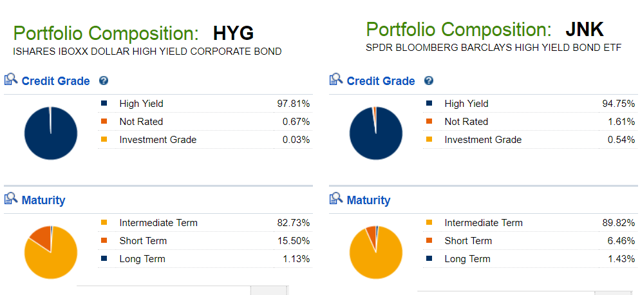

There are plenty of higher yield bond funds that typically invest in non-investment grade assets such as HYG and JNK that were discussed in my article from last week “Search For Yield: Bond Funds Vs. BDCs Paying 10%+“. Currently, HYG and JNK are yielding 5.2% and 5.6%, respectively.

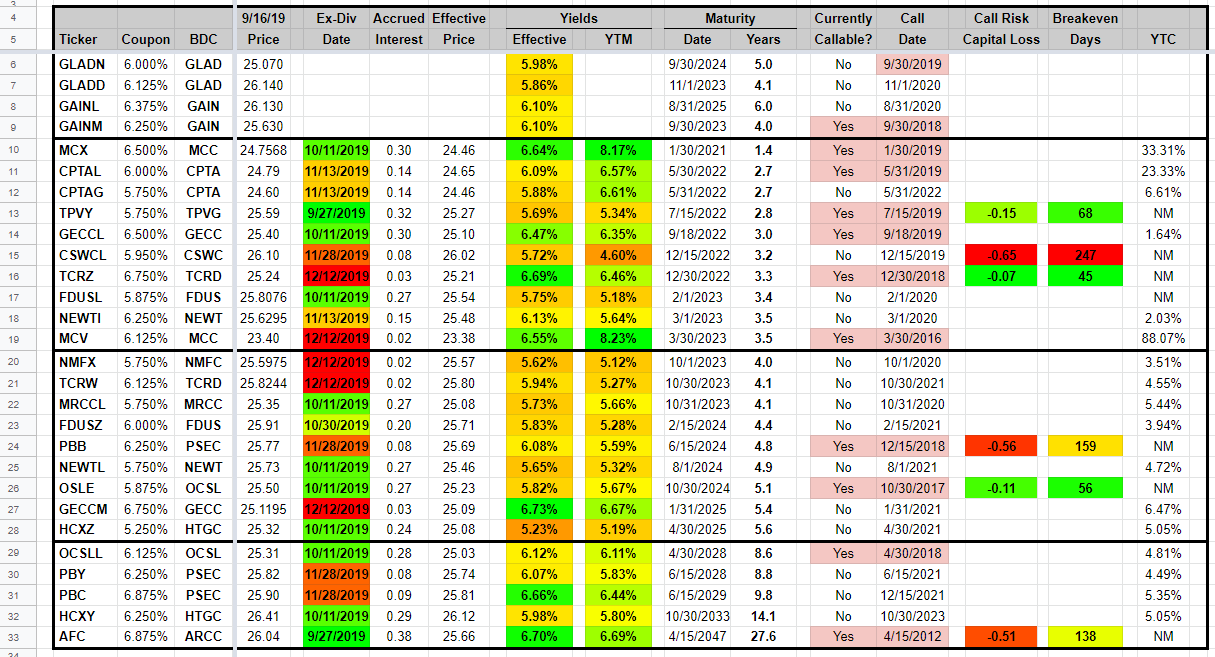

I invest in BDC Baby Bonds (currently averaging 6.24% yield as shown below) and Preferred Stocks for higher yields including some that are considered investment grade. Please read “Baby Bonds For BDCs: Price Stability” for previous discussions and information about these investments. The following is from the BDC Google Sheets and is what I use to make purchases when increasing my allocations:

What is a BDC?

Business Development Companies (“BDCs”) were created by Congress in 1980 to give investors an opportunity to invest in private small and mid-sized U.S. companies typically overlooked by banks. Most BDCs are publicly traded with a highly transparent structure subject to oversight by the SEC, states and other regulators, providing investors with higher than average dividend yields (most between 7% and 13% annually, see details below) by avoiding taxation at the corporate level. This allows them to pass along ordinary income and capital gains directly to the shareholder.

Their non-bank structure gives them the flexibility to invest in multiple levels of a company’s capital structure and most are Regulated Investment Companies (“RICs”) where capital gains, dividends and interest are passed onto shareholders avoiding taxation at the corporate level. However, they are required to distribute at least 90% of interest, dividends, and gains earned on investments. RICs are also required to distribute 98% of net investment income to avoid paying a 4% excise tax.

BDCs are limited in the amount of financial leverage they can use which is typically much lower than banks and REITs. They are required to diversify their holdings and to have at least 70% of total assets considered as “qualifying assets,” and offer managerial assistance to the businesses that they invest in.

Safer BDCs are currently averaging 9.2% yield compared to the average which is closer to 10.5% but patient investors can get higher yields by taking advantage of volatility.

Why do I like BDCs?

I like the idea of investing in companies that provide capital to smaller private businesses often unable to get growth capital from typical banks. Also, BDC stock pricing can be volatile which can be a good thing for investors that watch closely and take advantage of ‘oversold’ conditions.

BDC fundamentals remain strong/stable including a healthy U.S. economy, low market defaults and most BDCs focused on protecting shareholder capital with first-lien assets and protective covenants.

Also, most BDCs have excellent diversification by sector and have built their portfolios and balance sheets in anticipation of a recession with investments supported by high cash flow multiples and protected by protective covenants and first-lien on assets for worst-case scenarios.

The following is from a previous call with ARCC management:

As we look at the portfolio and evaluate the economy, we continue to approach the market with the belief that we are late in a credit cycle, and that economic growth is slowing. As a lender, these are perfectly healthy conditions for underwriting and strong portfolio performance. However, we do believe that slowing economic growth can challenge weaker companies. And if this thesis proves itself out it should benefit Ares Capital as more differentiation among credit managers is a good thing for established companies like ours which has resources and access to capital that surpasses our peers. A more fundamental credit downturn can be a significant market opportunity for us. We have been able to consolidate market share during times of distress, and outperform other credit managers. And we’re positioning ourselves to take advantage of this if an opportunity arises.

To be a successful BDC investor:

For investors that are looking to build a portfolio that includes BDCs, please consider the following suggestions:

- Identify BDCs that fit your risk profile by reading the BDC Risk Profiles report along with the individual Deep Dive Reports for each BDC.

- Use the BDC Google Sheets to purchase BDCs below or close to the ‘Short-Term Target Price’.

- Dipping your toe in: it is important for new investors to be patient and start with a small amount of shares using limit orders. Initiating a position will likely help with gaining interest and following the stock (and management team) to develop a comfort level for future purchases.

- Opportunity cost: Keep in mind that while you are waiting for lower prices, BDCs are paying dividends.

- Dollar averaging purchases: Eventually, there will be a general market and/or sector volatility driving lower prices providing opportunities to lower your average purchase prices.

The information in this article was previously made available to subscribers of Premium Reports, along with:

- Real-time changes to my personal BDC positions

- Target prices and buying points

- Real-time announcement of changes to dividend coverage and worst-case scenarios

- Updated rankings and risk profile