The following is from the GAIN Quick Update that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

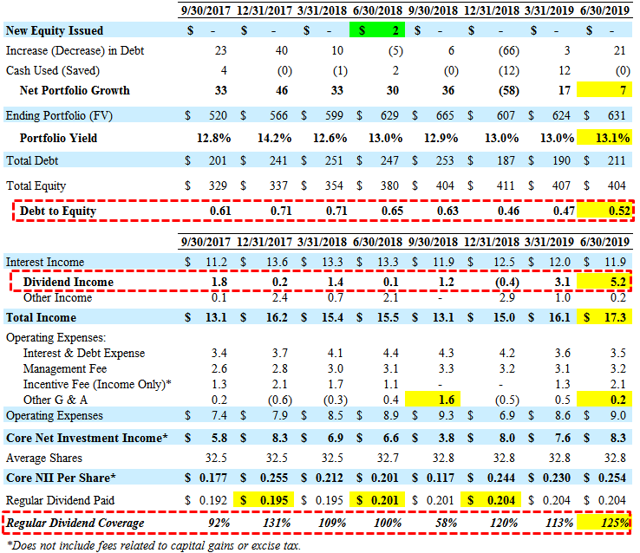

For Q2 2019, Gladstone Investment (GAIN) beat its best-case projections due to higher-than-expected dividend income covering its dividends by 125% and NAV per share declined by 0.9% (discussed later). As shown below, ‘Other G&A’ (net of credits) is inconsistent and has a meaningful impact on dividend coverage.

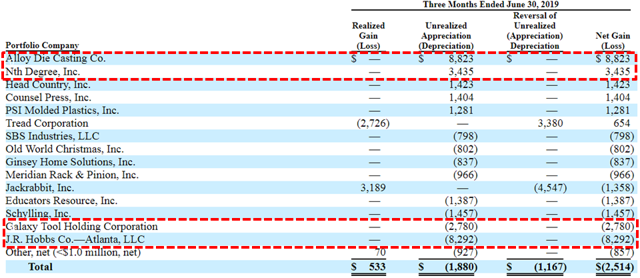

Its secured first-lien debt of B-Dry, LLC that was previously on non-accrual with a cost basis of $11.9 million and a fair value of $0, which was converted into equity during the three months ended June 30, 2019 (still with a cost basis of $11.9 million and a fair value of $0).

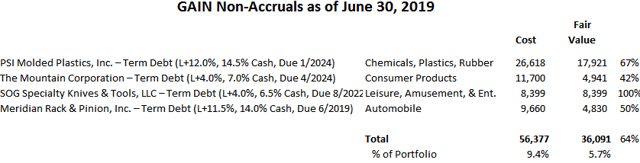

During calendar Q1 2019, Meridian Rack & Pinion was added to non-accrual status and marked down an additional $1.0 million during calendar Q2 2019 and SOG Specialty Knives & Tools (“SOG”), PSI Molded Plastics (“PSI”), and The Mountain Corporation remain on non-accrual status. Total non-accruals now have a cost basis of $56.4 million, or 9.4% of the portfolio at cost, and fair value of $36.1 million, or 5.7% of the fair value of the portfolio. It should be noted that the equity positions in most of these companies have been marked down to zero fair value. If these non-accruals were completely written off, it would impact NAV per share by around $1.10 or around 8.9%.

For calendar Q2 2019, NAV per share declined by 0.9% (from $12.40 to $12.29) due to various markdowns including its equity positions in J.R. Hobbs Co. (by $8.3 million) and Galaxy Tool Holding (by $2.8 million) partially offset by overearning the dividend and various markups including Alloy Die Casting and Nth Degree, Inc.

Due to the previous repayments, GAIN has higher portfolio concentration risk with the top five investments accounting for over 38% of the portfolio fair value and 31% of investment income:

“Our investments in Nth Degree, Inc., J.R. Hobbs, Counsel Press, Inc., Brunswick Bowling Products, Inc., and Horizon represented our five largest portfolio investments at fair value as of June 30, 2019, and collectively comprised $240.4 million, or 38.1%, of our total investment portfolio at fair value.”

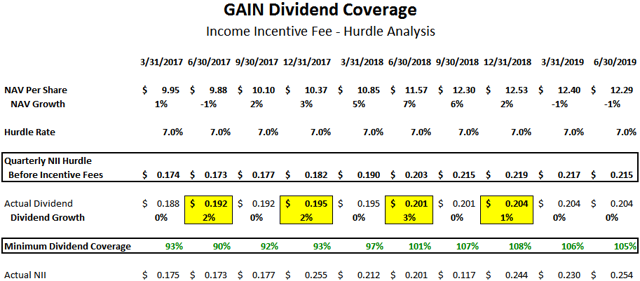

There is the potential for improved coverage through portfolio growth and rotating out of equity investments. As shown in the following table, the company will likely earn at least $0.215 per share each quarter covering 105% of the current dividend which is basically ‘math’ driven by an annual hurdle rate of 7% on equity before paying management incentive fees.

“The income-based incentive fee rewards the Adviser if our quarterly net investment income (before giving effect to any incentive fee) exceeds 1.75% [quarterly] of our net assets, adjusted appropriately for any share issuances or repurchases during the period (the “Hurdle Rate”). No incentive fee in any calendar quarter in which our pre-incentive fee net investment income does not exceed the Hurdle Rate (7.0% annualized)”

This calculation is based on “net assets” per share which have continued to grow driving a higher amount of “pre-incentive fee net investment income” per share before management earns its income incentive fees. As shown in the analysis below, the company continues to increase the dividend as NAV grows and increases the “Minimum Dividend Coverage”:

As mentioned in previous reports, the Board approved the modified asset coverage ratio from 200% to 150%, effective April 10, 2019. However, the company is subject to a minimum asset coverage requirement of 200% with respect to its Series D Term Preferred Stock. Historically, the company has maintained its leverage with a debt-to-equity ratio between 0.60 and 0.70 but is currently 0.52 giving the company plenty of growth capacity. The amount of preferred/common equity still accounts for 34% of the portfolio fair value (marked well above cost) which needs to be partially monetized and reinvested into income-producing secured debt.

This information was previously made available to subscribers of Premium BDC Reports, along with:

- GAIN target prices and buying points

- GAIN risk profile, potential credit issues, and overall rankings

- GAIN dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.