The following information was previously provided to subscribers of Premium BDC Reports along with:

- PSEC target prices/buying points

- PSEC risk profile, potential credit issues, and overall rankings

- PSEC dividend coverage projections and worst-case scenarios

Summary

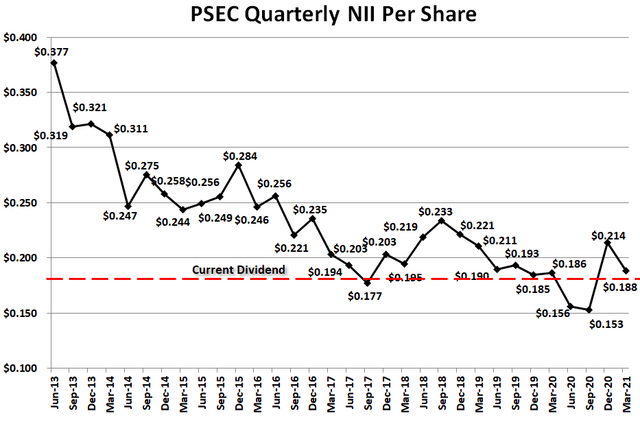

- Same as the previous quarter, four investments are responsible for PSEC’s NAV growth and ‘other income’ needed for covering the dividend.

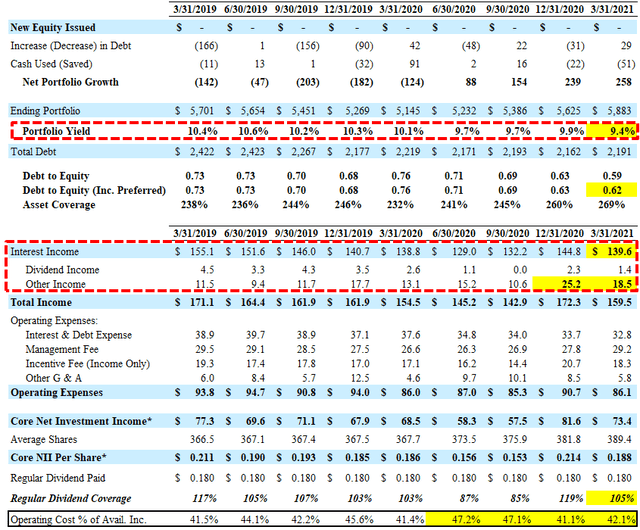

- PSEC reported just below its base-case projections mostly due to much lower-than-expected recurring interest income partially offset by other income from NPRC and First Tower.

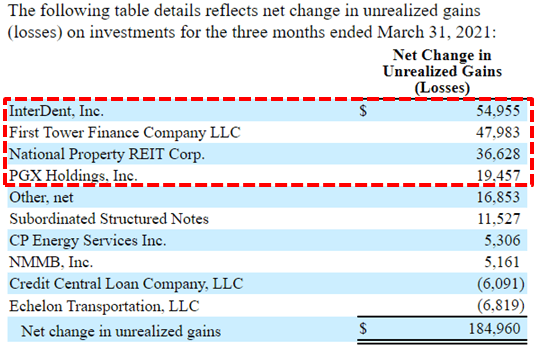

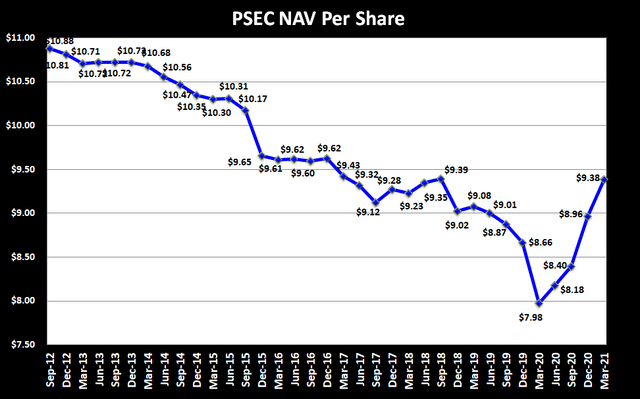

- NAV per share increased by 4.7% due to unrealized appreciation primarily related to the same control/affiliate investments as previous quarters (InterDent, First Tower, PGX Holdings, and NPRC).

- These four investments have been continually marked up and now account for $2.3 billion, 39% of the total portfolio or over 62% of NAV per share.

PSEC March 31, 2021, Quick Update

Prospect Capital (PSEC) reported just below its base-case projections mostly due to much lower-than-expected recurring interest income driven by a lower portfolio yield (from 9.9% to 9.4%) partially offset by higher-than-expected ‘other income’ from its control investment (mostly National Property REIT and First Tower Finance discussed later)

PSEC’s dividend coverage potential and risk profile will be discussed in the updated PSEC Projections & Pricing report over the coming weeks.

Leverage remains low with a current debt-to-equity at 0.62 (below the lower end of its target range) after taking into account the convertible Perpetual Preferred stock that continues to increase and discussed at the end of this update.

NAV per share increased by 4.7% (from $8.96 to $9.38) due to unrealized appreciation primarily related to the same control/affiliate investments as previous quarters (InterDent, First Tower Finance, National Property REIT, and PGX Holdings).

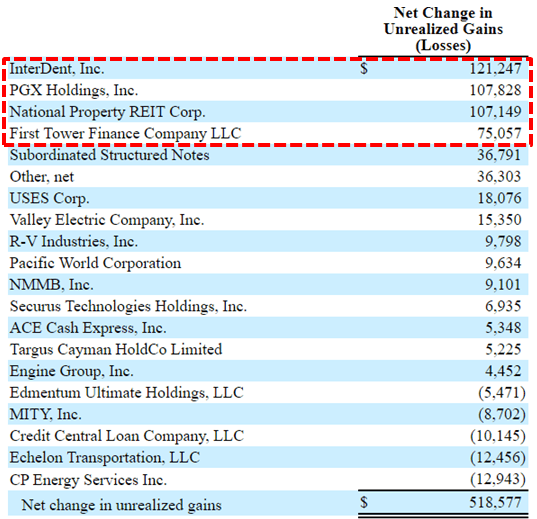

The following table details net change in unrealized gains (losses) on investments for the nine months ended March 31, 2021, showing these four same investments account for over $411 million or $1.08 per share of the recent gains:

More importantly is that four investments (National Property REIT, PGX Holdings, InterDent, and First Tower Finance) have been continually marked up and now account for $2.3 billion, 39% of the total portfolio or over 62% of NAV per share. It should be noted that these investments have a cost basis of under $1.5 billion resulting in around $793 million or $2.04 per share of unrealized appreciation compared to the current NAV per share of $9.38. This is very high concentration risk, especially if management is using aggressive valuation measures.

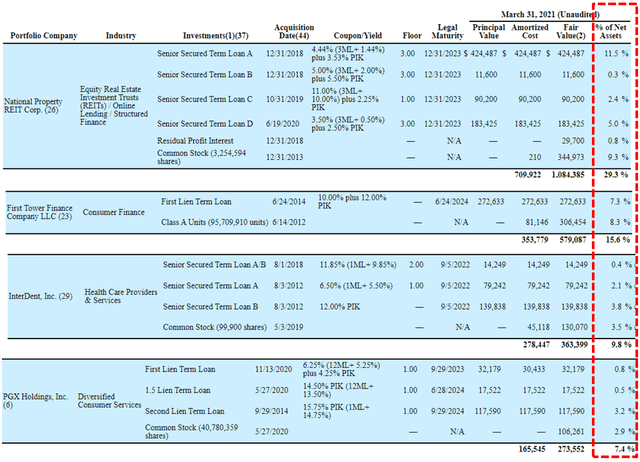

- Please see below for extensive discussions from the previous earnings call regarding National Property REIT (“NPRC”) and InterDent.

On August 3, 2020, PSEC launched a $1 billion 5.50% “Perpetual Preferred” stock offering to “enhance balance sheet liquidity, including repaying our credit facility and purchasing high-quality short-term debt instruments, and to make long-term investments in accordance with its investment objective.” For common shareholders this creates additional risks as the preferred is cumulative and has to be paid in full before common stock shareholders receive their distributions. The preferred stockholders have the option to convert into common at any time and there is a chance that PSEC could redeem these shares at “any time” converting into common stock based on the most recent 5-day trading price. This could be another way for management to issue additional shares below NAV.

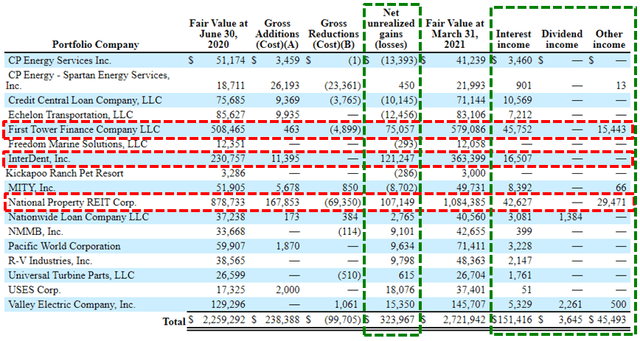

As shown in the following table, a good portion of the recent unrealized gains, as well as over $200 million of income, has come from its control investments over the last nine months which includes a large portion of the ‘other income’:

Full BDC Reports

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.