The following information was previously provided to subscribers of Premium BDC Reports along with:

- TCPC target prices/buying points

- TCPC risk profile, potential credit issues, and overall rankings

- TCPC dividend coverage projections and worst-case scenarios

TCPC Dividend Coverage Update

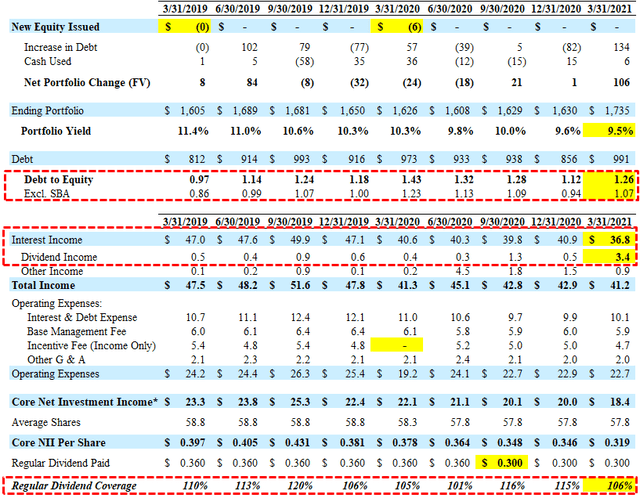

For Q1 2021, TCPC slightly beat its base-case projections due to much higher-than-expected dividend income partially offset by lower portfolio yield and only $0.01 per share of prepayment-related driving lower interest income. Payment-in-kind (“PIK”) income continues to decline from 7.6% in Q2 2020 to 3.2% in Q1 2021 the lowest level of PIK income in three years.

“Investment income for the three months ended March 31, 2021 included $0.01 per share from prepayment premiums and related accelerated original issue discount and exit fee amortization, $0.03 per share from recurring original issue discount and exit fee amortization, $0.02 per share from interest income paid in kind, $0.06 per share of dividend income and $0.02 per share in other income. Notably, this was our lowest level of PIK income in more than 3 years. Origination, structuring, closing, commitment, and similar upfront fees received in connection with the outlay of capital are generally amortized into interest income over the life of the debt investment.”

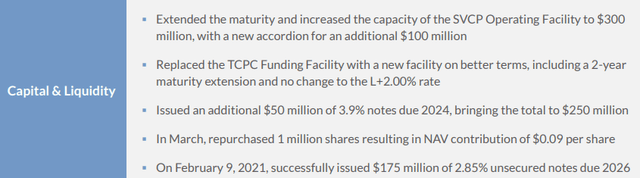

Similar to most BDCs, TCPC continues to improve or at least maintain its net interest margin through reducing its borrowing rates including its SVCP Credit Facility reduced to L+1.75% announced on June 24, 2021, and $175 million of 2.850% notes due 2026 issued on February 9, 2021. Both Fitch and Moody’s reaffirmed the Company’s investment-grade rating with stable outlook during Q1 2021.

I am expecting higher amounts of dividend income partially related to Edmentum, Inc. but not as much as there was in Q1 2021. Management discussed the recurring amount of dividend income on the recent call:

“Dividend income in the first quarter included $1.3 million or $0.02 per share of recurring dividend income on our equity investment in Edmentum. I would say I would note that, that is — we view it as recurring dividend income. We had about $0.5 million from Iracore this quarter. We also had about, I think, $800,000 from 36th Street and then some other income from Amtech dividend income this quarter, about $800 million from Amtech as well. I would say most of that should be recurring. 36th Street, as you know, has a preferred rate contractual, and then we have a participation in dividend income a majority split, which has actually been — we’re well into that each quarter, and it’s growing. So that is actually partly recurring and then the variable component actually takes us up quite a bit over the recurring amount, which we like. So the majority — I would say the majority of it is recurring, but then where it’s not, we’re actually seeing good, consistent variable income that has actually been growing as it ties to 36th Street.”

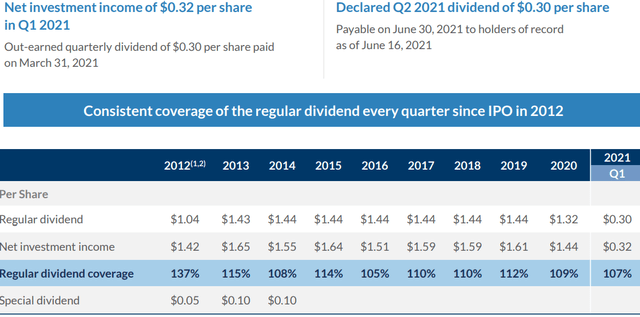

Previous reports correctly predicted the reduction of TCPC’s quarterly dividend from $0.36 to $0.30 which was at the top of my estimated range of $0.28 to $0.30. At the time, the company had spillover or undistributed taxable income (“UTI”) of around $0.78 per share. However, this is typically used for temporary dividend coverage issues. Please do not rely on UTI as an indicator of a ‘safe’ dividend.

The previously projected lower dividend coverage was mostly due to lower LIBOR and portfolio yield combined with management keeping lower leverage to retain its investment-grade rating.

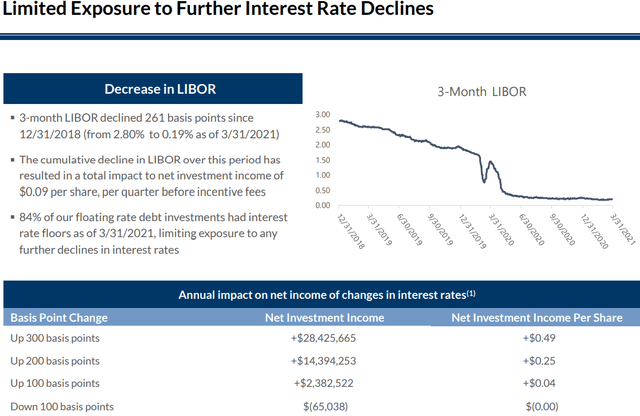

The previous declines in interest rates (LIBOR) were mostly responsible for the decline in portfolio yield with “limited exposure to any further declines”.

“Since December 31, 2018, LIBOR has declined 261 basis points or by 94%, which has put pressure on our portfolio yield. However, our portfolio is largely protected from any further declines in interest rates as 84% of our floating rate loans are currently operating with LIBOR floors.”

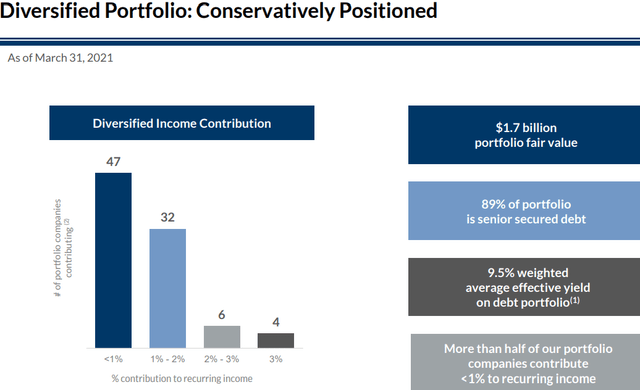

As shown below, TCPC’s portfolio is highly diversified by borrower and sector with only 4 portfolio companies that contribute 3% or more to dividend coverage:

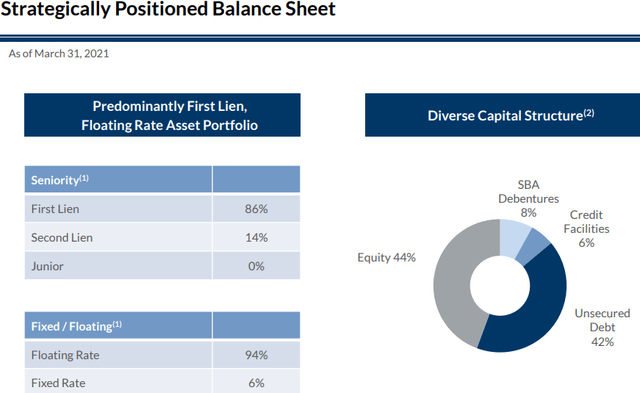

“As the chart on the left side of Slide 6 of the presentation illustrates, our recurring income is spread broadly across our portfolio and is not reliant on income from any 1 portfolio company. In fact, over half of our portfolio companies each contribute less than 1% to our recurring income. 94% of our debt investments are floating rate. Additionally, 86% of our debt investments are first lien.”

Historically, the company has consistently over-earned its dividend with undistributed taxable income. Management will likely retain the spillover income and use for reinvestment and growing NAV per share and quarterly NII rather than special dividends.

On the previous earnings call, management was asked about resetting the dividend higher (closer to the previous level) and mentioned the lumpy nature of fee, dividend, and prepayment-related income, “investors take comfort from dividend stability” and “great pride and comfort from knowing that we’ve got good dividend coverage”. I agree.

Q. “Knowing that you folks never like to do anything in a herky jerky way and having just trimmed your dividend from 36 to 30 last year for reasons that are understandable kind of in the middle of the lockdowns. And so I’m just kind of wondering, again, not for the next quarter, two or three. But just philosophically, what would you be looking forward to or is it a goal to get back to the prior distribution?”

A “I just want to remind you of something that we had said earlier about a decrease in LIBOR, which basically cost $0.09 a share. So yes, we did this during the lockdown. But we were also reacting to the very significant change in LIBOR, and the math is set out. And so when we made that decision, it was really primarily looking at LIBOR as opposed to events in the portfolio. We’re very proud of having earned our dividend every quarter. We think investors take comfort from dividend stability, knowing that it’s well-earned and appropriately covered. And that’s really been our focus. I think the other thing is, as you look at our earnings, we benefited from prepayment fees. And as we discussed earlier on the call, those are lumpy. We’ve had significant prepayment fees the last couple of quarters. We don’t always — we did into Q1 of last year. In fact, we had very few of them. And Q1 tends to be a seasonally slower quarter. Paul pointed out, we hadn’t received any in a material way yet this quarter. We take great pride and comfort from knowing that we’ve got good dividend coverage. But we also know that there’s a certain lumpiness to the extra earnings from additional fees, dividends and prepayments and the more unusual items.”

Full BDC Reports

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). This means investors need to do their due diligence before buying.