The following information was previously provided to subscribers of Premium BDC Reports along with:

BDC target prices/buying points

BDC risk profile, potential credit issues, and overall rankings. Please see BDC Risk Profiles for additional details.

BDC dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

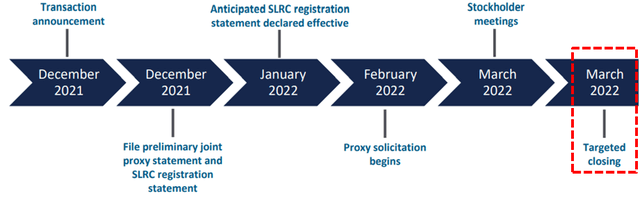

SUNS/SLRC Merger Announcement

This article discusses SLR Senior Investment (SUNS) and SLR Investment (SLRC) which are currently yielding around 8.2% for SUNS (but headed higher) and 8.4% for SLRC (but headed lower). After the markets closed on December 1, 2021, SUNS and SLRC announced that they have entered into an agreement to merge together, with SLRC as the surviving company. Both are managed by SLR Capital Partners and the transaction is expected to close in the “first half of 2022”.

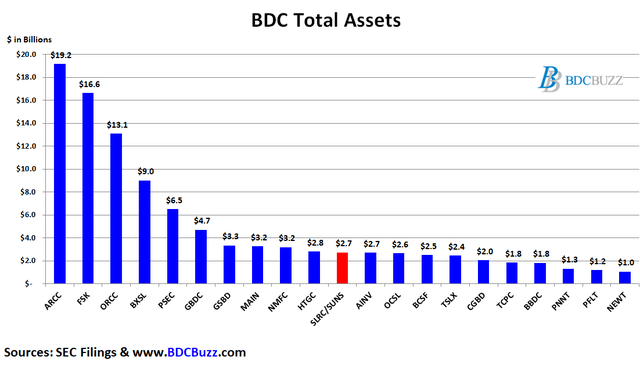

As shown below this would result in SLRC/SUNS being among the largest publicly traded BDCs:

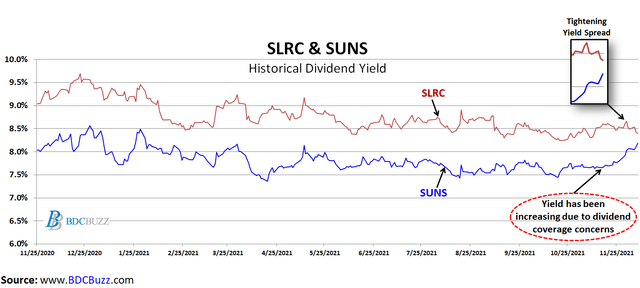

SLRC & SUNS Historical Yields

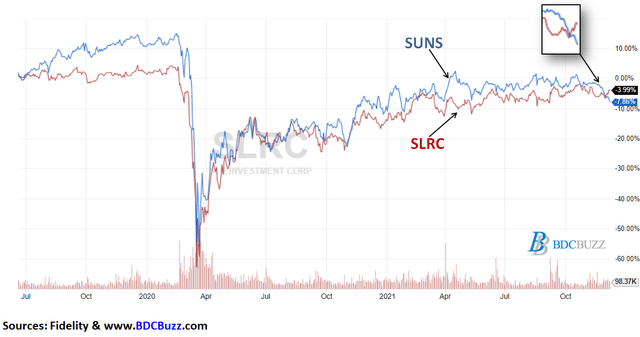

One thing that SLRC and SUNS have in common is that they have seriously underperformed the average BDC from a stock price and total return standpoint. I generally do not suggest that my subscribers own these stocks until they have a clear path to dividend coverage without the need for fee waivers. Most BDCs have easily surpassed their pre-pandemic stock prices while paying much higher dividend yields providing excellent total returns to investors especially compared to equity and mortgage REITs as discussed and shown in “BDCs Vs. REITs: Comparing Returns For Higher-Yield Investors“.

However, both SLRC and SUNS have not reached their previous levels as well as paying lower-than-average dividend yields.

BDCs are priced based on expected risk and returns. Investors expect higher returns for higher risk. BDC returns are typically through dividends paid to shareholders. Historically, SLRC has yielded around 1.0% more than SUNS.

As shown below, over the last 12 months the average yield for SLRC is much higher than SUNS but has started to tighten over the last few weeks and especially since the merger announcement. There are a few reasons for this including dividend coverage expectations and changes in risk profile and less shareholder-friendly fee agreement as discussed next. This is discussed at the end to help investors understand the recent and likely upcoming changes to stock prices.

BDC Pricing

Why is the yield spread between SUNS and SLRC tightening?

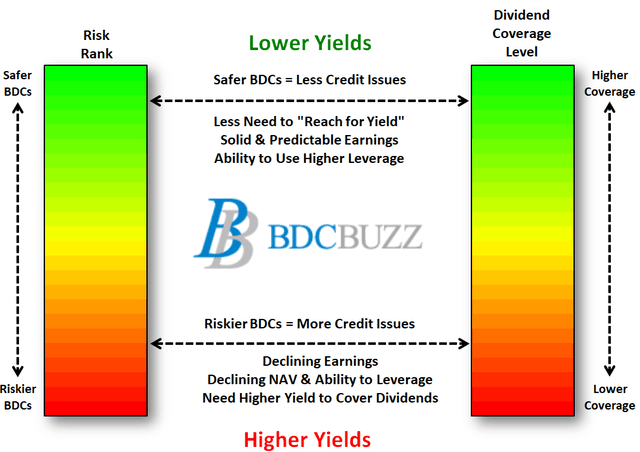

There are very specific reasons for the prices that BDCs trade driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage).

BDCs with higher quality portfolios typically have lower yields.

BDCs with lower expenses and higher potential dividend coverage typically have stable to growing dividends and investors pay higher prices driving lower yields.

This is discussed throughout this article.

SUNS & SLRC Risk Profile Discussion

As mentioned earlier, BDCs with higher quality portfolios typically have lower yields. Interestingly enough this typically applies to the investments within the portfolio as well. This means that safer BDCs generally have lower yield investments – not always but generally.

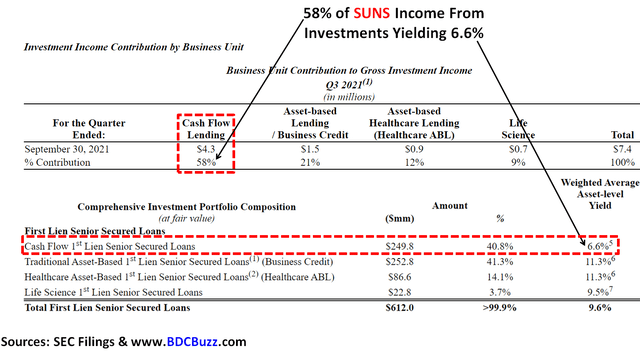

As shown below, 58% of SUN’s income comes from its lower risk ‘cash flow lending’ portfolio with a weighted average yield of 6.6%. To be clear, a 6.6% yield for a BDC loan is considered bank-like quality.

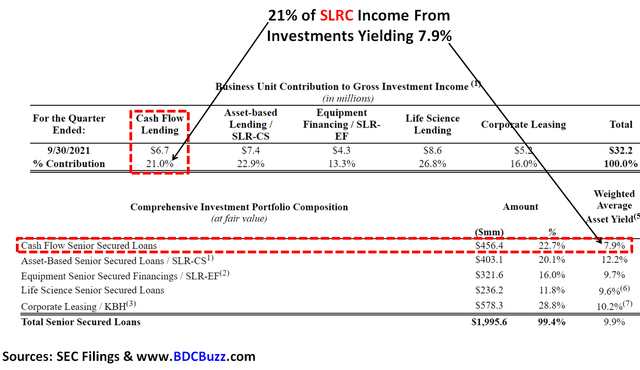

As shown below, only 21% of SLRC’s income comes from its lower risk ‘cash flow lending’ portfolio with a weighted average yield of 7.9%.

SUNS & SLRC Dividend Coverage Discussion

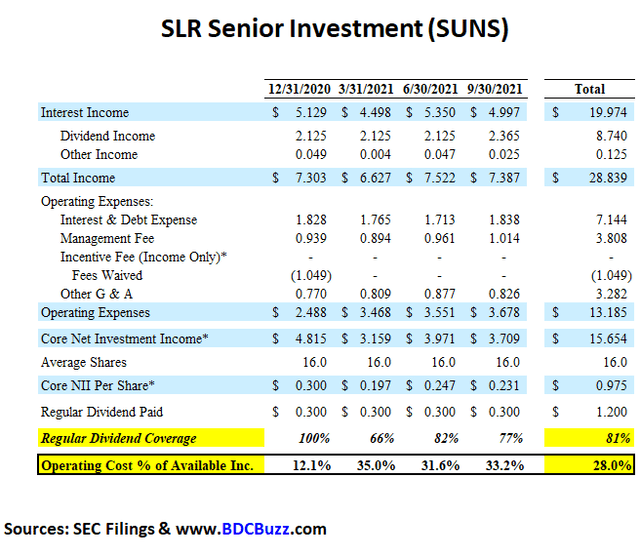

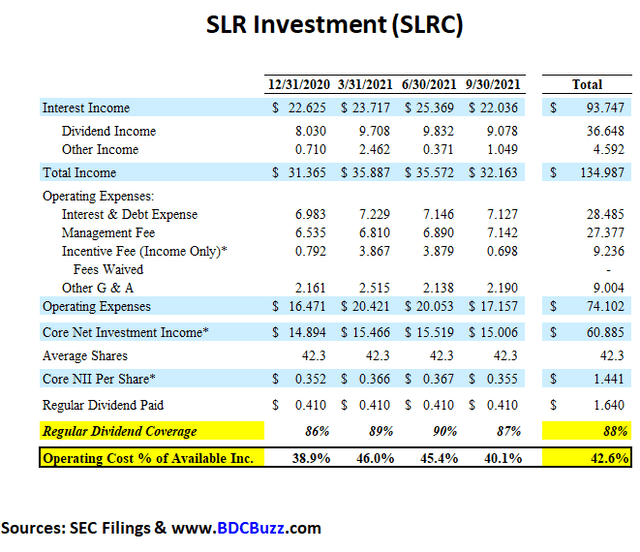

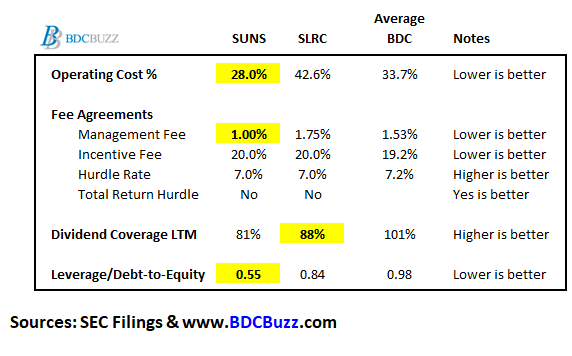

BDCs with lower operating expenses can pay higher amounts to shareholders without investing in riskier assets. The following tables show the recent dividend coverage for SUNS and SLRC along with the “Operating Cost as a Percentage of Available Income” which measures operating, management, and incentive fees compared to available income.

“Available Income” is total income less interest expense from borrowings and is the amount of income that is available to pay operating expenses and shareholder distributions.

However, management is expecting reduced borrowing rates and lower ‘Other G&A’ which I have taken into account with the updated projections along with the previously discussed changes to the fee agreement.

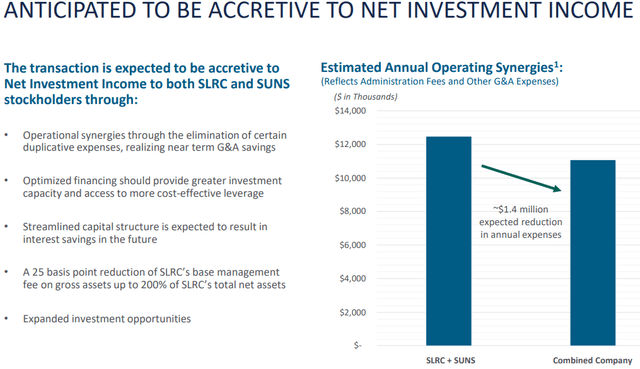

We project the merger should initially generate approximately $1.4 million of annual operating synergies through elimination of certain fixed costs of SUNS and reduction in our debt financing costs through potential interest expense savings.

The total ‘Other G&A’ for both SUNS and SLRC over the last 4 quarters was around $12.3 million and should be closer to $11.0 million annually if these companies are merged. However, this is a small amount compared to almost $40 million of fees paid to management over the last 4 quarters with underleveraged portfolios driving no incentive fees for SUNS. It should be noted almost $37 million of the fees were paid by SLRC compared to under $3 million paid by SUNS during the same period. However, the combined company will adopt a fee structure closer to SLRC as discussed later.

Source: SLR Senior Investment Corp

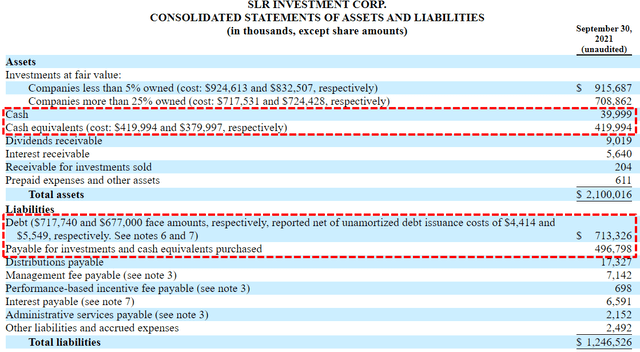

Please note that similar to SUNS, SLRC has $420 million of “cash equivalents” as of September 30, 2021, typically offset by “Payable for investments and cash equivalents purchased” and is not taken into account with the base management fee. However, as of September 30, 2021, there were almost $77 million ofadditional amounts payable for investments purchased even after taking into account $40 million of additional cash. This has been taken into account with the updated projections and leverage ratios.

Source: SEC Filing

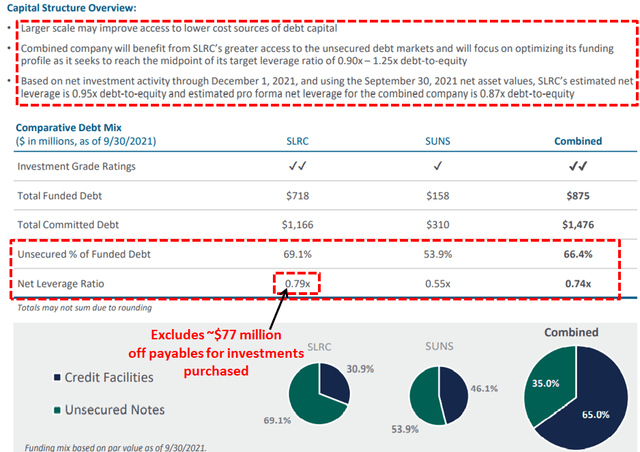

It is important to point out that the transaction will result in higher leverage as well as a more flexible (unsecured) balance sheet for SUNS:

Sources: SLR Senior Investment Corp & BDC Buzz

SUNS & SLRC Fee Agreements

As mentioned earlier, BDCs with lower expenses and higher potential dividend coverage typically have stable to growing dividends and investors pay higher prices driving lower yields.

The base management fee for SUNS is among the lowest in the sector at only 1.00% of gross assets excluding “temporary assets”. However, SLRC’s base management fee is currently 1.75% (1.00% for assets that exceed 200% of net assets).

Management has agreed to reduce the fee to 1.50% for the combined company. Also, the base management for assets that exceed 200% of net assets will be the lower 1.00%.

Source: SLR Senior Investment Corp

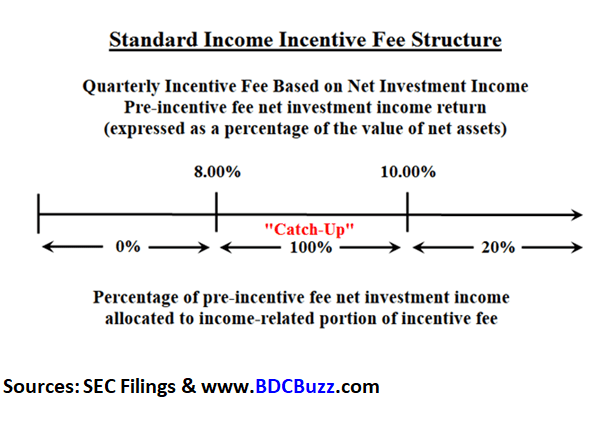

Most BDCs have an income incentive fee with a hurdle rate that requires a minimum return on net assets to be at least 7% to 8% (higher is better) annually before paying incentives to the advisor. Once this hurdle is reached, the advisor is entitled to 100% of the income up to a certain point. This is called a ‘catch-up’ provision that catches up the incentives to 20% of pre-incentive fee net investment income and then the advisor is paid 20% after the ‘catch-up’ as shown in the diagram below.

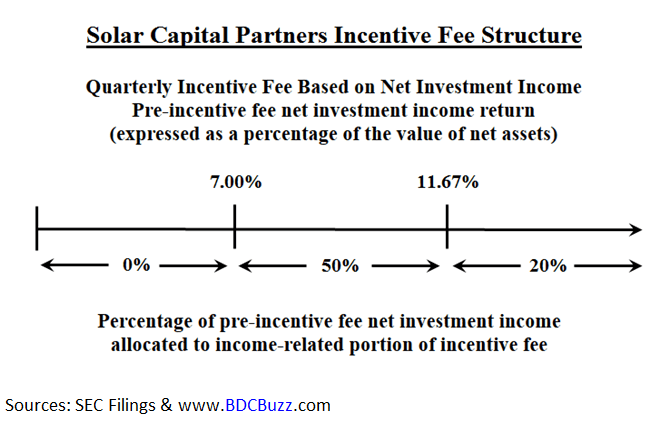

SLRC has a similar incentive fee agreement with a 7.00% hurdle which is not ideal as it results in lower dividend coverage.

However, SUNS investors only pay 50% of income over its 7.00% hurdle up to another hurdle of 11.67% and then 20% after that. This is a good thing for shareholders.

However, this feature will not be included in the new fee agreement:

The incentive fee payable by the combined company will remain consistent with SLRC’s existing fee structure.”

This is very important to management over the coming quarters as they will receive 100% of the cost savings from lower ‘Other G&A’ and reduced borrowing rates up to a certain point.

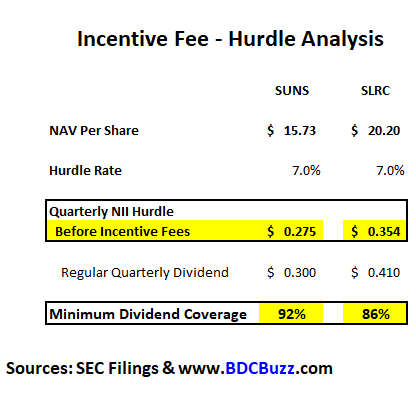

The following table shows the “pre-incentive fee net investment income” per share beforemanagement earns income incentive fees based on “net assets”. SUNS will likely earn around $0.275 per share each quarter before paying management incentive fees covering around 92% which is ‘math’ driven by an annual hurdle rate of 7% on equity. As shown in the previous financial results, there were no incentive fees paid. It is important to note that the calculation is based on the net asset values from the previous quarter and SUNScould have lower earnings per share over the coming quarters due to being underleveraged but management will not earn an incentive fee.

SLRC is paying a higher dividend relative to its NAV per share which will result in lower dividend coverage during periods of lower earnings likely due to being underleveraged as discussed later.

Merger Specifics

The Board intends to declare and pay its regular monthly distributions of $0.10 per month for the first fiscal quarter of 2022, including the March 2022 distribution, which will be declared and paid just prior to the anticipated closing of the transaction. Also, SUNS investors could receive a special dividend if there is any “undistributed taxable income” but I would not expect much if anything as the company will likely not fully cover its dividend over the next two quarters.

Additionally, the SUNS Board of Directors intends to declare a special distribution that represent any previously undistributed taxable income. This distribution will help ensure that SUNS maintains its RIC status and avoids paying excise tax.

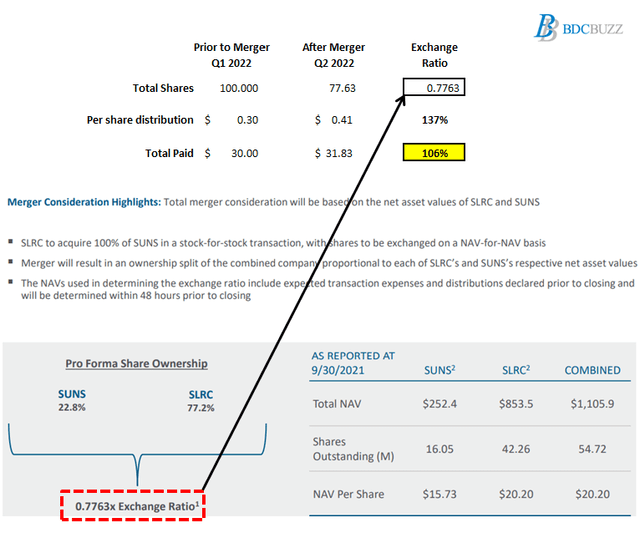

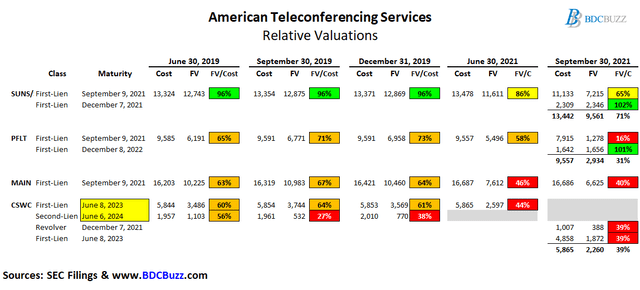

As shown below, SUNS investors could receive an increase of around 6% to their current distribution depending on the final exchange rate of shares from SUNS to SLRC which is based on net asset value. However, there is a chance for upcoming NAV declines for SUNS due to American Teleconferencing Services as discussed below.

The current exchange ratio is 0.7763 taking into account September 30, 2021, results are shown below:

Sources: SLR Senior Investment Corp & BDC Buzz

As predicted in a public article from October 2019 “Time To Sell SUNS”, SUNS finally placed American Teleconferencing Services (“ATS”) on non-accrual status which currently accounts for $9.6 million or 2.5% of the portfolio. This was the primary reason for the recent NAV per share decline of 0.9% during calendar Q3 2021.

ATS is an investment also held by PFLT, MAIN, and CSWC that operates as a subsidiary of Premiere Global Services (“PGi”), offering conference call and group communication services. On June 4, 2021, S&P announced that PGi was downgraded to CCC-, from CCC+, with a negative outlook, with the rating agency citing “significantly” deteriorating operating performance over the past quarter. Also downgraded was the company’s senior secured debt to CCC-, from CCC+ due to declining operating performance “increases the likelihood that [PGi] will default or undertake a distressed exchange” in the next six months unless the company’s private equity sponsor injects equity. PGi previously defaulted on positions held by CSWC with maturity dates of June 2023 and June 2024 but there are still other tranches maturing this year currently on non-accrual.

SUNS has consistently had aggressive valuations for ATS relative to other BDCs with similar positions especially PFLT and MAIN that also have a first-lien position at L+650 maturing on September 9, 2021. Investors should be prepared for additional NAV declines if PGi is not able to restructure and/or improve performance. Also, management is paid a base management fee on total assets which is directly impacted by the fair value marked on assets which results in lower earnings compared to BDCs with conservative valuations.

ATS was discussed on a previous CSWC call:

Previous CSWC call: “This company has experienced softness in their post-COVID performance and is currently engaged in an active restructuring conversations. We have decided to place this loan on nonaccrual pending more clarity on the loan terms and company performance post restructuring.”

Article Summary & Recommendations

Clearly, SUNS has a more shareholder-friendly fee agreement with a lower-than-average base management fee of 1.00% and incentive fees at only 50% of income over its 7.00% hurdle up to another hurdle of 11.67%. This is partially responsible for its lower “Operating Cost %”. Again, BDCs with lower operating expenses can pay higher amounts to shareholders without investing in riskier assets. SLRC has a higher-yielding portfolio which is likely why management is using the higher expense management fee agreement.

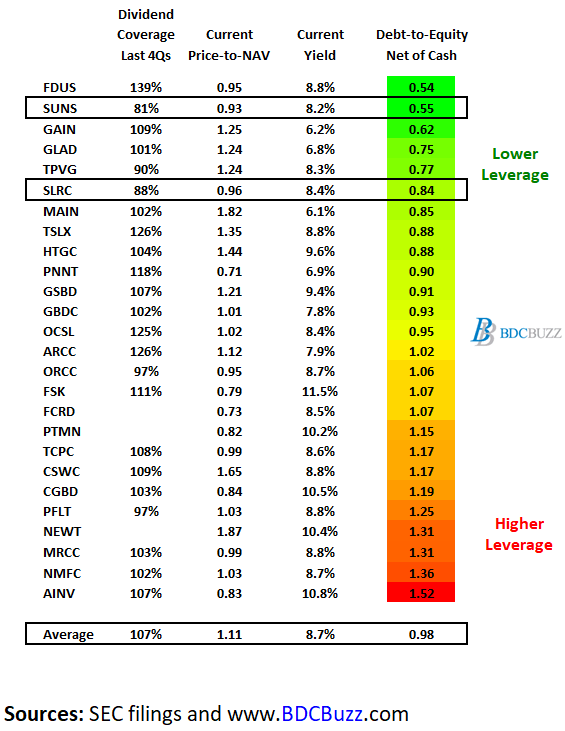

The “dividend coverage LTM” in the previous table shows the average dividend coverage over the last 12 months (four quarters) but please keep in mind that SUNS has much lower leverage with higher portfolio growth potential to improve dividend coverage over the coming quarters. As shown below, SUNS has among the lowest leverage (debt-to-equity net of cash) in the sector:

On December 2, 2021, SUNS and SLRC held a joint conference call to discuss the transaction. One of the analysts asked the following:

Q. “And just another higher-level question with the merger. SUNS, I know they converged recently, but SUNS has traditionally traded at a higher multiple than SLRC, has a better fee structure and so forth. So why didn’t SUNS acquire Solar? Why did you do it this way?”

A. “Well, SUNS is 1/4 of the size, so that makes it very difficult to do that. And in terms of valuation, today, they are — prior to the announcement, they were trading within 1% of each other. They’ve traded within typically 3% to 5% with each other. So they have always traded very tightly. And for the SUNS shareholders, which clearly we had an independent committee on both sides, so this was obviously a critical consideration. They’re stepping into an entity that gives them a 6% greater distribution day 1, a company that’s a higher ROE, and frankly, higher ROE growth potential and expand liquidity, and eventually a lower cost of capital as well.”

Again, SUNS has lower leverage contributing to its smaller portfolio and I’m not sure size is as important as which fee agreement was adopted for the combined company. Clearly, management will be making higher amounts of fees over the coming quarters through the 1.50% management fee with increased leverage on SUNS’s equity capital but also from the 100% ‘catch-up’ provision on the incentive fee. This is a big win for management especially as the reduced ‘Other G&A’ and borrowing rates will first benefit management as they will receive 100% up to a certain point as discussed earlier.

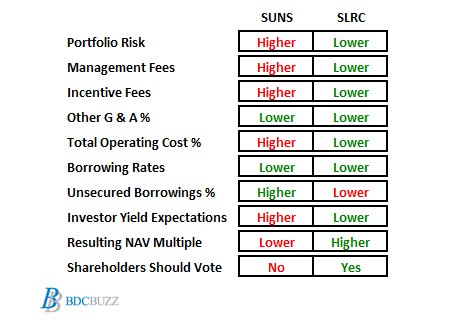

The following table shows exactly why SUNS stock has declined and SLRC stock has increased since the merger announcement:

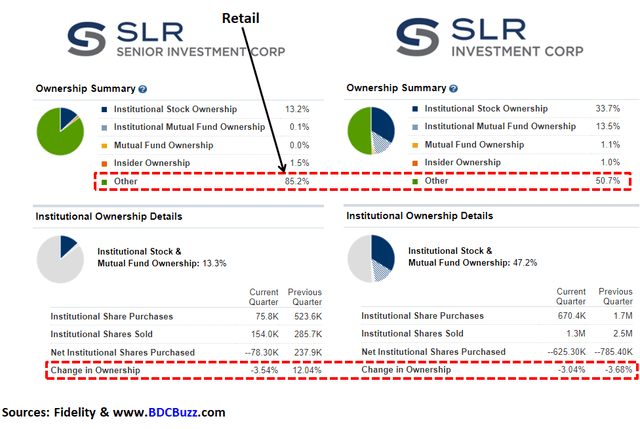

As shown below, SUNS is mostly retail owned which means they can vote down this proposal or at least call Investor Relations and ask for some of the items listed below.

Here are a few suggestions to make the merger more equitable to SUN’s shareholders:

Post-merger fee waivers for full dividend coverage until leverage is closer to mid-target similar to many BDCs after their mergers.

Base management fee to 1.00% similar to many lower risk BDCs.

Incentive fees of 50% of income over its 7.00% hurdle up to another hurdle of 11.67% and then 20% after that.

Include a ‘total return hurdle’ similar to almost EVERY new fee agreement to keep management and shareholder interest aligned.

Please keep in mind that this list is exactly what the other BDCs have provided when asking for shareholder approval especially if it includes an increase in management fees which I think is a first for the sector. Most BDCs are reducing fee structures and adding items for increased shareholder alignment.

Investors expect lower yields (pay a higher multiple) for BDCs with investor-friendly fee agreements which will benefit the company as it can easily access the equity markets as well as IG debt markets for lower rates on unsecured borrowings. Win-win.

One analyst on the call mentioned the following:

I appreciate you taking my questions and good luck on closing this deal, which looks like a good deal all around.”

I actually like this analyst but respectfully disagree from the standpoint of SUNS investors which I am urging them to vote NO.

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy to digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

Monday Morning Update – Before the markets open each Monday morning we provide quick updates for the sector including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

Deep Dive Projection Reports – Detailed reports on at least two BDCs each week prioritized by focusing on ‘buying opportunities’ as well as potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

Friday Comparison or Baby Bond Reports – A series of updates comparing expense/return ratios, leverage, Baby Bonds, portfolio mix, with discussions of impacts to dividend coverage and risk.

This information was previously made available to subscribers of Premium BDC Reports. BDCs trade within a wide range of multiples driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential(not necessarily historical coverage). This means investors need to do their due diligence before buying including setting target prices using the portfolio detail shown in this article (at a minimum) as well as financial dividend coverage projections over the next three quarters as discussed earlier.