The following information was previously provided to subscribers of BDC Buzz Premium Reports along with:

- PNNT and PFLT target prices, buying points, and suggested limit orders (used during market volatility).

- PNNT and PFLT risk profile, potential credit issues, changes in NAV, and overall rankings. Please see BDC Risk Profiles for additional details.

- PNNT and PFLT dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

![]()

PNNT Quick Quarterly Update (December 31, 2023)

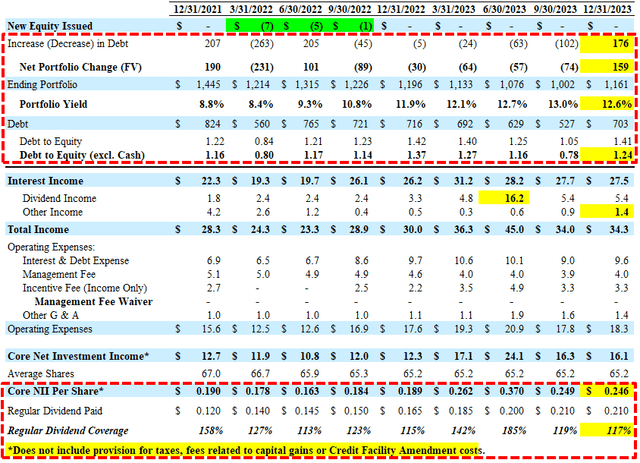

- Earnings: Reported between its base and best-case projections mostly due to higher than expected portfolio growth as well as continued higher dividend and other income partially offset by its portfolio yield declining from 13.0% to 12.6%, driving earnings of $0.246 per share (excluding provision for taxes) covering its dividends by 117%.

- Leverage: Its debt-to-equity increased to 1.24 (net of cash and U.S. Government Securities) due to higher-than-expected net portfolio growth of $160 million.

- Net Realized Gains: $1.8 million or $0.03 per share from exiting equity positions.

- Dividends: Maintained its monthly dividend of $0.07 per share for February 2024 (or $0.21 per share per quarter), which was the previous base case projection, and will announce its March 2024 dividend next month.

- Share Repurchases: No shares were repurchased during calendar Q4 2023.

- Credit Quality: Only Mailsouth remains on non-accrual status which has been written off with no further negative impact on NAV per share.

- NAV Per Share: Decreased by $0.05 (from $7.70 to $7.65) mostly due to marking down its watch list investments in Atlas Purchaser ($0.04 per share impact) and Pragmatic Institute ($0.01 per share impact).

- This information will be discussed in the updated PNNT Deep Dive Projection report, along with its overall risk profile, full dividend, and financial projections, taking into account discussions with management on the upcoming earnings call.

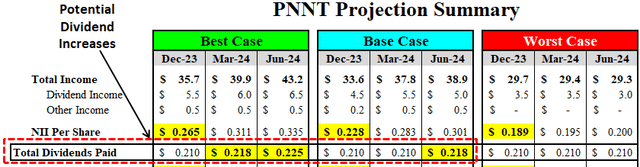

As shown below, I am expecting additional dividend increases for Q2 2024 in the best and base-case projections. The following was from the previous call:

“Obviously, up until this quarter, I’ve raised the dividend for many, many quarters. As our income rose and as our default rate remain very, very limited. We pivoted to a monthly dividend a couple of months ago. So here, this quarter, we earned 24, we’re paying out $0.21 I think for now, we’re just going to let a percolate kind of keep a nice cushion to the monthly $0.07 per share dividend. We’ll come up for air in a couple of months and see how things are looking and see about the trends in the portfolio, see about interest rates. This PSLF JV has been really, really accretive to earnings and hopefully, we’ll continue to be very accretive to earnings. And no decisions, but it’s something we’re watching and we’re focused on.”

Arthur Penn, Chairman and CEO: “We are pleased to announce another quarter of solid net investment income, which is in excess of our dividend by a healthy margin. Our earnings stream continues to be robust and is driven in part by the excellent returns generated by our PSLF Joint Venture.”

For the three months ended December 31, 2023, we invested $231.1 million in 12 new and 32 existing portfolio companies at a weighted average yield on debt investments of 11.9% (excluding U.S. Government Securities). For the three months ended December 31, 2023, sales and repayments of investments totaled $71.0 million (excluding U.S. Government Securities). For the three months ended December 31, 2023, PSLF invested $81.0 million (including $50.8 million were purchased from the Company) in five new and seven existing portfolio companies at weighted average yield interest bearing debt investments of 12.7%. PSLF’s sales and repayments of investments for the same period totaled $29.1 million.

PFLT Quick Quarterly Update (December 31, 2023)

- Suggested Pricing: No change. I will reassess after updating the projections using guidance from management.

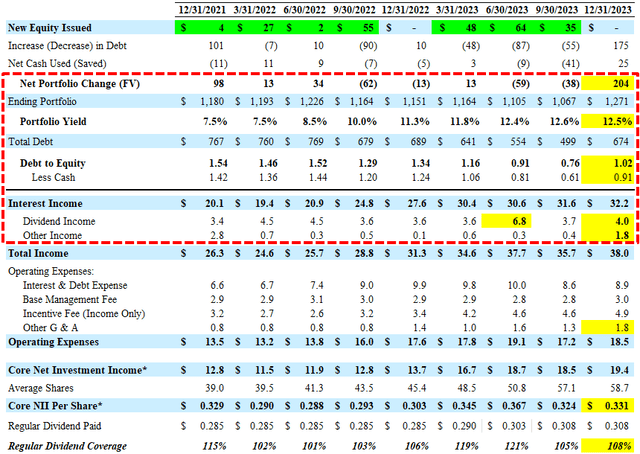

- Earnings: Reported between its base and best-case projections mostly due to much higher than expected portfolio growth, higher other income and dividend income from its PennantPark Senior Secured Loan Fund (“PSSL”), partially offset by higher ‘Other G&A’ and a slight decline in portfolio yield (from 12.6% to 12.5%), covering its dividends by 108%.

- Leverage: Its debt-to-equity increased from 0.61 to 0.91 (net of cash) due to much higher-than-expected new investments of $303 million during the quarter.

- Subsequent Events: Through February 2, 2024, PFLT invested another $103 million in 4 new and 23 existing portfolio companies at a weighted average yield of 13.0%. This is good news and will be taken into account with the updated projections.

- Dividends: Maintained its monthly dividend of $0.1025 per share for February 2024, which was the previous base case projection, and will announce its March 2024 dividend next month.

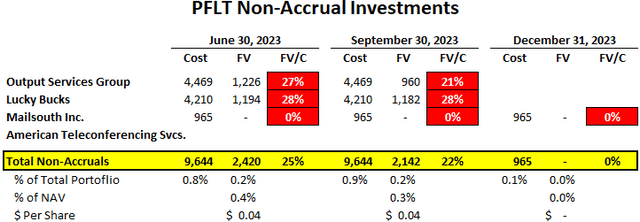

- Credit Quality: Non-accruals declined from 0.2% to 0.0% of the portfolio fair value due to restructuring Output Services Group and Lucky Bucks. Only its second lien position in Mailsouth remains on non-accrual status which has been written off with no further negative impact on NAV per share.

- Net Realized Losses: $3.1 million or $0.05 per share due to restructuring Output Services Group and Lucky Bucks.

- NAV Per Share: Increased by $0.07 or 0.6% (from $11.13 to $11.20) mostly due to unrealized portfolio appreciation which included some of its watch list investments being marked higher and the equity position of its PSSL as well as overearning the dividends.

- This information will be discussed in the updated PFLT Deep Dive Projection report, along with its overall risk profile, full dividend, and financial projections, taking into account discussions with management on the upcoming earnings call.

Art Penn, Chairman/CEO: “We are pleased to have another quarter of solid performance from both a NAV and net investment income perspective. We are actively investing in this excellent vintage of new core middle market loans. Through the growing balance sheets of PFLT and our PSSL joint venture, we are driving meaningfully increased income.”

“For the three months ended December 31, 2023, we invested $302.6 million in 13 new and 34 existing portfolio companies at a weighted average yield on debt investments of 11.9%. Sales and repayments of investments for the same period totaled $103.8 million.”

As of December 31, 2023, our portfolio totaled $1,270.9 million, and consisted of $1,090.5 million of first lien secured debt (including $210.1 million in PSSL), $0.2 million of second lien secured debt and $180.3 million of preferred and common equity (including $52.1 million in PSSL). Our debt portfolio consisted of approximately 100% variable-rate investments. As of December 31, 2023, we had one portfolio company on non-accrual, representing 0.1% and zero percent of our overall portfolio on a cost and fair value basis, respectively.

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy-to-digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning, we provide quick updates for the sector, including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on individual BDCs each week prioritized by focusing on buying opportunities and potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Weekly General Updates or Comparison Reports – A series of updates discussing ‘Building a BDC Portfolio’, suggested pricing and limit orders, expense/return ratios, interest rates, leverage, BDC Investment Grade Notes/Baby Bonds, portfolio mix, and potential impacts on dividend coverage and risk.

![]()