The following information was previously provided to subscribers of BDC Buzz Premium Reports along with:

- HTGC target prices, buying points, and suggested limit orders (used during market volatility).

- HTGC risk profile, potential credit issues, changes in NAV, and overall rankings. Please see BDC Risk Profiles for additional details.

- HTGC dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

![]()

HTGC Quick Quarterly Update (December 31, 2023)

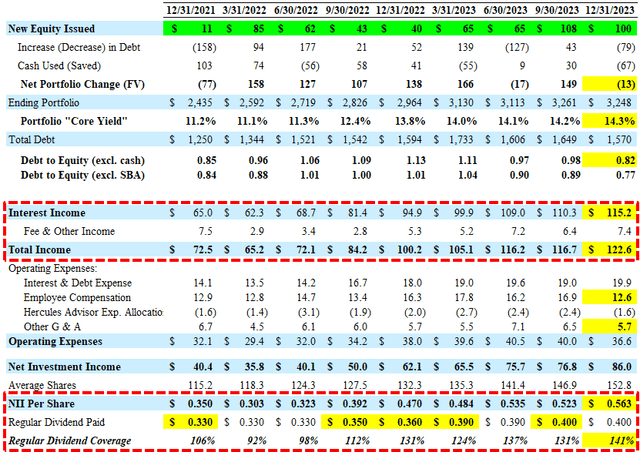

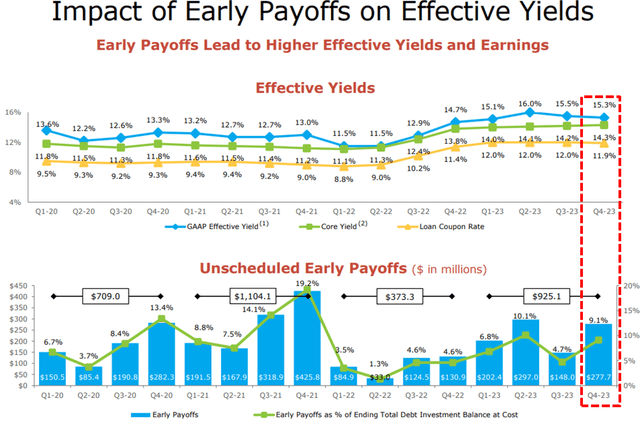

- Earnings: Beat its best-case projected NII covering its regular dividend by 141% mostly due to higher prepayment-related income from $278 million of early loan repayments (compared to $148 million the previous quarter) combined with lower expenses including employee compensation and ‘Other G & A’. Also, there was another quarter of higher-than-expected fee income of over $7 million and increased portfolio yield. HTGC has undistributed earnings of $0.80 per share (previously $1.03 per share) for additional supplemental dividends.

- Subsequent Events: Q1 2024 is off to a strong start as the company has closed new gross debt and equity commitments of $552 million and funded $384 million through February 13, 2024, with pending commitments of $507 million.

- Dividends: Maintained its regular/base dividend of $0.40 per share plus another supplemental of $0.08 per share which was the previous base case projections. The company expects to pay a total of $0.32 per share in supplemental dividends for 2024 which was already taken into account with its ST target price and included in the total yield in the BDC Google Sheets

- Recent Share Issuances: During Q4 2023, the company sold 6.5 million shares under its equity ATM program for net proceeds of $100 million. As of December 31, 2023, approximately 17.3 million shares remain available for issuance and sale.

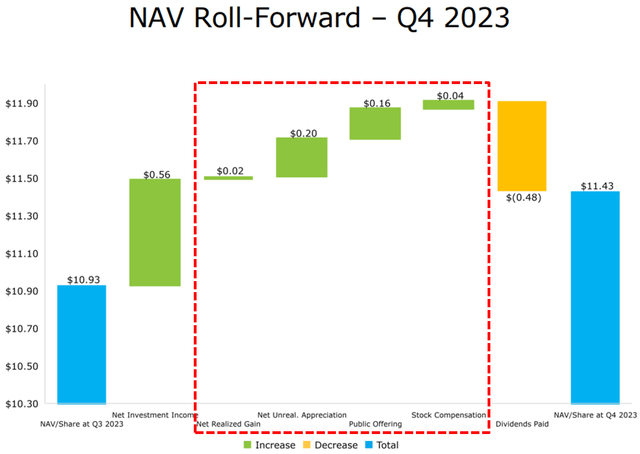

- NAV Per Share: Increased by $0.50 or 4.6% (from $10.93 to $11.43) due to $0.08 per share related to the valuation on publicly traded equity/warrant positions, accretive share issuances adding $0.16 per share, overearning its regular and supplemental dividends by $0.08 per share, and appreciation of other equity and watch list positions.

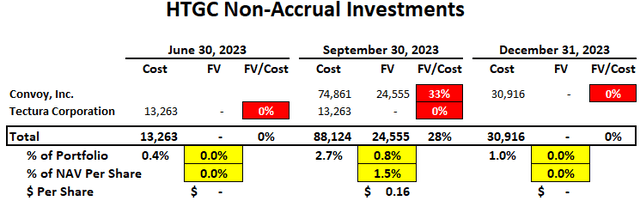

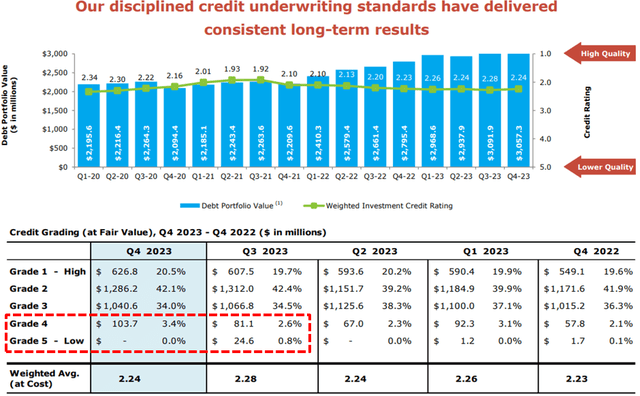

- Credit Quality: Non-accruals declined from 0.8% to 0.0% of the portfolio fair value due to partial repayment of its first-lien position in Convoy, Inc. which remains the only investment on non-accrual but management is expecting to resolve the issue with no further impact to NAV per share (see notes below). The non-accrual PIK portion of its debt position in Tectura Corporation was restructured into a preferred equity position and the non-PIK loan was marked to full value. There was a decrease in the average credit grade of debt investments (from 2.28 to 2.24) and credit quality remains strong with “100% of our debt portfolio companies remain current on contractual payments”.

- This information will be discussed in the updated HTGC Deep Dive Projection report.

“As of our most recent reporting, 100% of our debt portfolio companies remain current on contractual payments to Hercules. Our workout efforts with regards to Convoy remain ongoing and our recovery efforts will likely wrap up early this year, although that situation remains ongoing and fluid.”

“Early loan repayments increased in Q4 to approximately $278 million, which came in above our guidance of $150 million to $250 million. We expect 2024 to be another year with higher-than-normal volatility and a higher-for-longer rate environment, but as we discussed on our last call, we expect the market environment for new originations to improve throughout 2024. We are already seeing this come to fruition in Q1.”

Q. “It’s clearly a record quarter of results, and as you noted, dividend coverage on a core basis totaled 140%. So, it would seem like the starting point for earnings in 2024 is quite a bit higher than the base dividend you announced yesterday. So, could you just walk us through the rationale about maintaining and not increasing the current base dividend?”

A. “I think we’ve been pretty consistent over the course of the last several years in terms of how we manage the base distribution. We never want to set the base distribution at a number that we think would jeopardize our ability to maintain it irrespective of market and rate environment conditions. We set the base distribution based on our outlook for core income, where we essentially back out the benefit of any prepayments and accelerations. We want to continue to take a conservative position. That was the choice that we made with respect to Q4. We are continuing to deliver that out-performance to our shareholders via the supplemental distributions. This is the fourth consecutive year where we’ve been able to enhance the quarterly base distribution with an additional supplemental distribution. And we think that that’s the right way to operate the business in the current environment. It certainly does not mean that that’s not going to change on a go-forward basis. But that was the rationale for the decision to maintain $0.40 and declare a $0.32 supplemental distribution payable $0.08 per quarter in 2024.”

“Our Grade 1 and 2 credits improved to 62.6% compared to 62.1% in Q3. Grade 3 credits were slightly lower at 34% in Q3 versus 34.5% in Q3. Our rated four credits increased moderately to 3.4% from 2.6% in Q3, and we had no rated five credits in Q4. In Q4, the number of loans on nonaccrual decreased by one.”

Portfolio Company IPO and M&A Activity in Q4 2023 and Q1 2024

As of February 13, 2024, Hercules held debt, warrant or equity positions in six (6) portfolio companies that have completed or announced an IPO or M&A event, including:

In November 2023, portfolio company enGene Holdings Inc. (ENGN), a clinical stage biotechnology company pioneering novel non-viral gene therapies for local administration into mucosal tissues, completed its SPAC merger initial listing with Forbion European Acquisition Corp. (FRBN), a special purpose acquisition company. Hercules cumulatively committed $20.0 million in venture debt financing beginning in December 2021 and currently holds warrants for 43,689 shares of common stock as of December 31, 2023.

In November 2023, portfolio company Tact.ai Technologies, Inc., a developer of field engagement and conversational AI technology, announced it has completed the sale of its technology assets to Aktana, Inc., a leader in intelligent customer engagement for the global life sciences industry. Terms of the technology acquisition were not disclosed. Hercules committed $5.0 million in venture debt financing in February 2020.

In November 2023, portfolio company Faction, a multi-cloud data services provider, announced it had been acquired by Tahosa Capital, an investment firm. Terms of the acquisition were not disclosed. Hercules committed $12.5 million in venture debt financing beginning in November 2017.

In February 2024, portfolio company ZeroFox, Inc. (ZFOX) an enterprise software-as-a-service leader in external cybersecurity, announced it has signed a definitive agreement to be acquired by Haveli Investments, a private equity firm that seeks to invest in companies in the technology sector with a focus on software, data, gaming and adjacent industries, for $350 million. The acquisition is subject to customary closing conditions including shareholder approval. Upon completion, ZeroFox’s common stock will no longer be publicly listed on the Nasdaq Global Market and will become a privately held company. Hercules committed $30.0 million in venture debt financing beginning in June 2019 and currently holds 289,992 shares of common stock as of December 31, 2023.

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy-to-digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning, we provide quick updates for the sector, including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on individual BDCs each week prioritized by focusing on buying opportunities and potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Weekly General Updates or Comparison Reports – A series of updates discussing ‘Building a BDC Portfolio’, suggested pricing and limit orders, expense/return ratios, interest rates, leverage, BDC Investment Grade Notes/Baby Bonds, portfolio mix, and potential impacts on dividend coverage and risk.

![]()