The following information was previously provided to subscribers of BDC Buzz Premium Reports along with:

- TSLX target prices, buying points, and suggested limit orders (used during market volatility).

- TSLX risk profile, potential credit issues, changes in NAV, and overall rankings. Please see BDC Risk Profiles for additional details.

- TSLX dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

![]()

This update discusses Sixth Street Specialty Lending (TSLX) which remains one of the highest-quality BDCs that perform well during distressed environments. Management is very skilled at finding value in the worst-case scenarios, including distressed retail and energy investments.

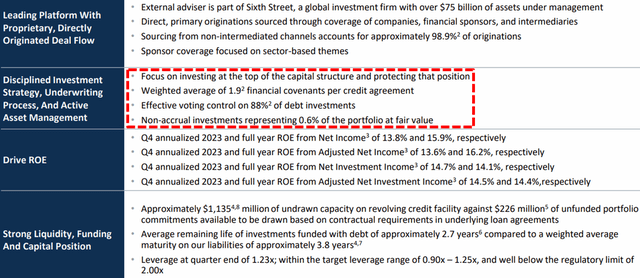

TSLX often lends to companies with an exit strategy of being paid back even through bankruptcy/restructuring and is proficient at stress testing every investment with proper coverage and covenants. Management has prepared for the worst as a general philosophy and historically used it to make superior returns (as shown next). Out of 25 transactions, 9 have gone through the bankruptcy process with no capital losses, with an unlevered return of almost 21%. TSLX’s portfolio is 91% first-lien with an average of 1.9 financial covenants for each debt position, 82% with call protection, and 88% effective voting control.

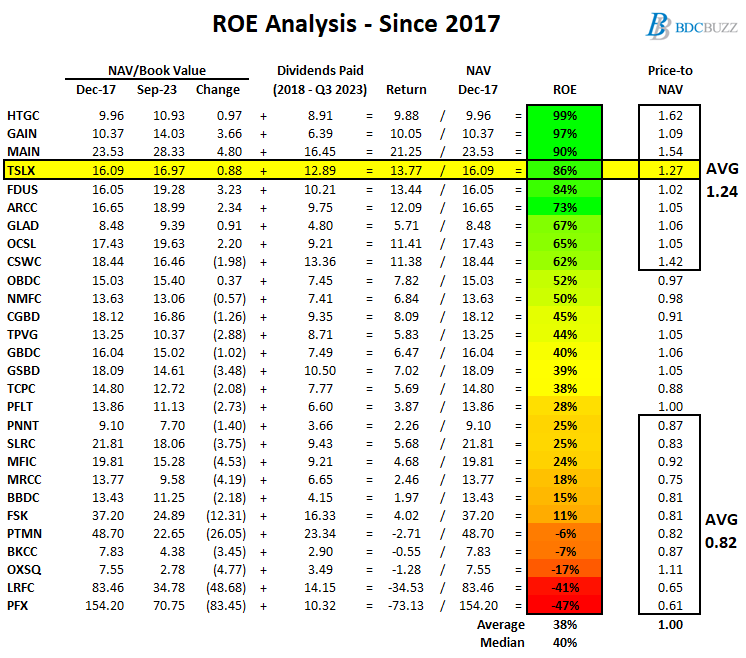

Comparison of Return on Equity (“ROE”)

- This information will be updated to take into account December 31, 2023, results.

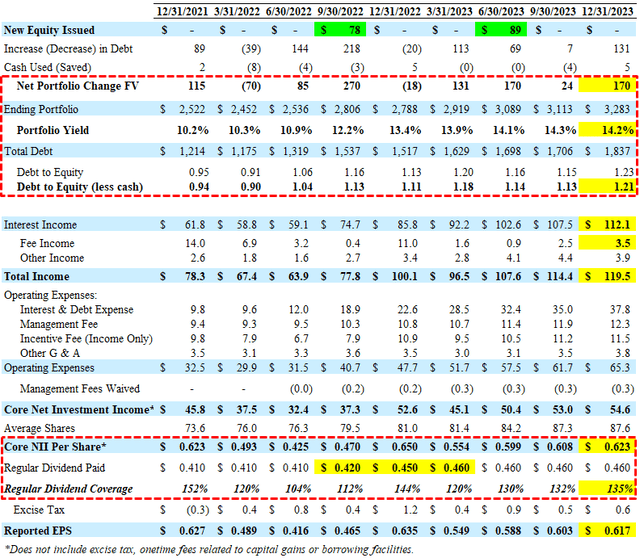

The following table shows the changes in NAV per share and dividends paid between December 31, 2017, and September 30, 2023, as a simple proxy for return on equity (“ROE”) to shareholders. It is important to note that many BDCs prefer not to pay special or supplemental dividends unless necessary because they directly reduce NAV per share. Also, some BDCs purposely pay lower dividends relative to their earnings, which contribute to higher NAV per share. However, this table takes these into account along with the current price-to-NAV ratios, showing that investors pay higher multiples for BDCs that deliver higher returns to shareholders.

Most BDCs with higher ROEs have historically held higher amounts of equity investments, especially HTGC, GAIN, MAIN, FDUS, ARCC, GLAD, and CSWC. However, TSLX has relatively lower amount amounts of equity positions and a much higher first-lien currently around 91% but has still delivered higher returns to investors as shown below.

TSLX Quick Quarterly Update (December 31, 2023)

- Earnings: Beat its best-case projections covering its regular dividend by 137% (excluding tax accrual) due to higher than expected portfolio growth and higher fee and prepayment-related income, including accelerated original issue discount (“OID”) accretion partially offset by a slight decline in the overall portfolio yield from 14.3% to 14.2%. Leverage increased due to portfolio growth and no shares issued through its ATM with a current debt-to-equity of 1.21 (net of cash).

- Dividends: Maintained its base dividend of $0.46 plus another supplemental dividend of $0.08 for a total of $0.54 per share paid in Q1 2024, which was above the previous best-case projections of $0.53 per share.

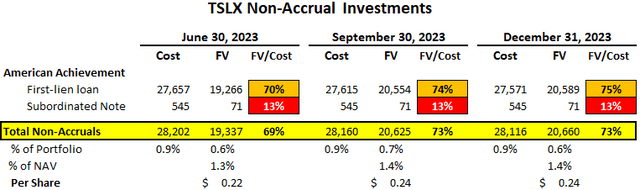

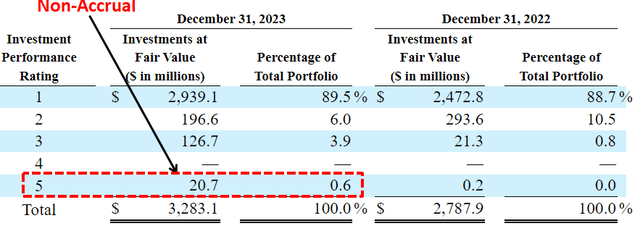

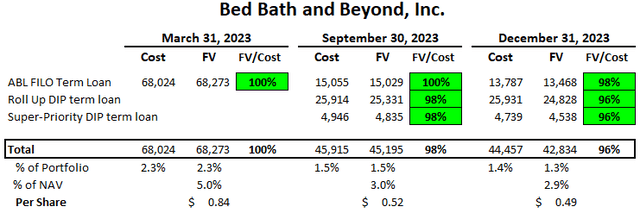

- Credit Quality: Only American Achievement remains on non-accrual status at 0.6% of the portfolio fair value with almost 96% of the portfolio fair value rated 1 or 2 (strongest credit quality). It should be noted that its debt position in Bed Bath and Beyond remains almost fully valued, implying confidence from management,as discussed in the previous report. TSLX management is very skilled at finding value in the worst-case scenarios, including distressed retail ABL and energy investments.

- NAV Per Share: Increased by another 0.4% (from $16.97 to $17.04) due to overearning the dividends and accretive share issuances through the DRIP.

- Other: Recently issued $350 million of 6.125% unsecured notes due March 2029, as the company is continuing to strengthen its balance sheet with more unsecured borrowings.

- This information will be discussed in the updated TSLX Deep Dive Projection report.

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy-to-digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning, we provide quick updates for the sector, including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on individual BDCs each week prioritized by focusing on buying opportunities and potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Weekly General Updates or Comparison Reports – A series of updates discussing ‘Building a BDC Portfolio’, suggested pricing and limit orders, expense/return ratios, interest rates, leverage, BDC Investment Grade Notes/Baby Bonds, portfolio mix, and potential impacts on dividend coverage and risk.

![]()