The following information was previously provided to subscribers of BDC Buzz Premium Reports along with:

- MAIN target prices, buying points, and suggested limit orders (used during market volatility).

- MAIN risk profile, potential credit issues, changes in NAV, and overall rankings. Please see BDC Risk Profiles for additional details.

- MAIN dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

![]()

MAIN Quick Quarterly Update (December 31, 2023)

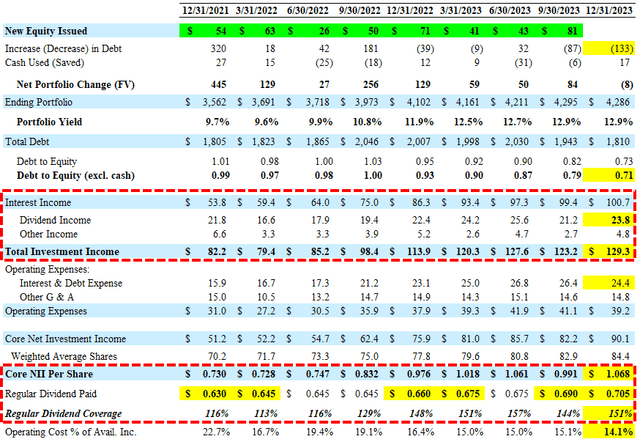

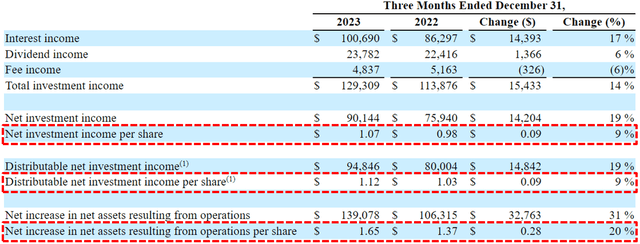

- Earnings: Reported between its base and best-case projections covering its regular dividends by 151% with continued strong dividend income (mostly from its LMM portfolio) and lower-than-expected interest expense (due to lower borrowings on its credit facility, lower portfolio growth, and equity issuances). Recurring interest income has increased by around 17% over the last four quarters.Core NII per share was $1.07 and distributable net investment income (“DNII”) was $1.12 per share, easily covering its Q4 2023 regular and supplemental dividends of $0.98 per share.

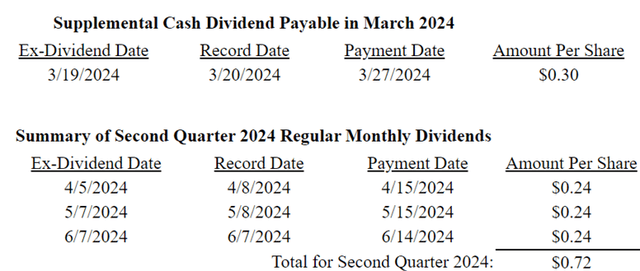

- Dividends: Announced a supplemental dividend of $0.30 per share for Q1 2024 (at the high end of my previous estimates) and reaffirmed its regular monthly dividends of $0.24 per share for April, May, and June 2024 for $0.72 per share for Q2 2024.

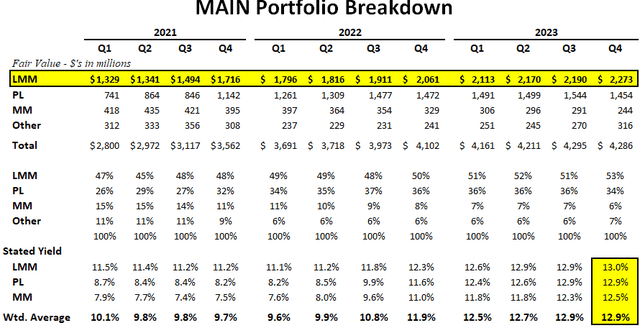

- Credit Quality: Non-accruals decreased from 1.0% to 0.6% of the investment portfolio at fair value and from 3.1% to 2.3% at cost. The company has not released the updated 10-K with the detail needed to assess changes in the portfolio risk profile (including its watch list investments) which will be discussed in the updated projections.

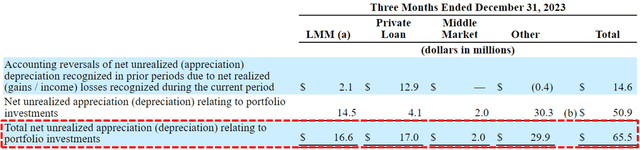

- NAV Per Share: Increased by 3.1% (from $28.33 to $29.20) due to overearning the dividends, accretive share issuances, and net unrealized appreciation which will be discussed after going through the updated 10-K SEC filing.

- Pricing & Recommendations: No change. I will reassess after updating the financial projections assessing portfolio credit quality taking into account management guidance on the earnings call, including dividend potential.

- This information will be discussed in the updated MAIN Deep Dive Projection report.

MAIN remains a ‘Level 1’ dividend coverage BDC, implying the potential for additional dividend increases and/or supplemental dividends, mostly due to continued improvement in net interest margins as well as NAV per share increases and realized gains. As mentioned in previous reports, I am expecting additional dividend increases over the coming quarters due to:

- Continued dividend income from portfolio companies.

- Previous increases in portfolio yield.

- Portfolio growth (increased interest income).

- Higher returns from its asset management business (MSC Income Fund).

MAIN reaffirmed its regular monthly cash dividends of $0.24 per share for April, May, and June 2024 for $0.72 per share for Q2 2024. Also, the company announced a supplemental dividend of $0.30 per share for Q1 2024 which was at the high end of my previous estimates (between $0.25 and $0.30 per share). I was expecting only $0.60 per share of supplemental dividends in the base-case projections and $1.00 in the best-case projections for 2024. However, I was also expecting a dividend increase for Q2 2024 (base and best cases) but the company is likely taking a conservative approach to regular dividend increases, similar to other BDCs.

“The continued positive momentum across our platform in 2023 allowed us to deliver significantly increased value to our shareholders, with a 25% increase in the total dividends paid to our shareholders in 2023. Despite this significant increase, our distributable net investment income exceeded the total dividends paid to our shareholders by over 13% for the fourth quarter and over 17% for the full year. Based upon the continued strength of our performance in the fourth quarter, we recently declared a $0.30 per share supplemental dividend to be paid in March 2024. This represents our tenth consecutive quarterly supplemental dividend, to go with the seven increases to our regular monthly dividends in the same time period, allowing us to deliver significant value to our shareholders, while continuing to maintain a conservative dividend policy and retaining a portion of our income for the future benefit of our stakeholders.”

In January 2024, MAIN issued $350 million of 6.95% unsecured notes due March 1, 2029, which have been added to the BDC Google Sheets.

“With the continued support from our long-term lender relationships, and the benefits of our recent investment grade debt offering in January 2024, we enter 2024 with very strong liquidity and a conservative leverage profile and are excited about the prospects for significant growth in both our lower middle market and private loan investment strategies. We appreciate the hard work and efforts of the management teams and employees at our portfolio companies and continue to be encouraged by the favorable performance of the companies in our diversified lower middle market and private loan investment portfolios and remain confident that these strategies, together with the benefits of our asset management business and our cost efficient operating structure, will allow us to continue to deliver superior results for our shareholders.”

The increase in NAV per share was due to the net fair value increases from the unrealized appreciation especially in the LMM, Private Loan, and other portfolios, the accretive impact from equity issuances, and higher earnings which exceeded the dividends.

“We are extremely pleased with our performance in the fourth quarter, which closed another record year for Main Street across several key financial metrics. Our fourth quarter performance resulted in a new quarterly record for net investment income per share, distributable net investment income per share equal to our existing quarterly record that was set earlier this year, a new record for net asset value per share for the sixth consecutive quarter and a return on equity of approximately 23% for the fourth quarter. Our strong performance in the fourth quarter continued our positive performance from the first three quarters of 2023 and resulted in new annual records for net investment income per share and distributable net investment income per share and a return on equity of approximately 19% for the full year. These results demonstrate the continued and sustainable strength of our overall platform, the benefits of our differentiated and diversified investment strategies, the unique contributions of our asset management business and the continued underlying strength and quality of our portfolio companies. We are further pleased to be able to generate these returns while intentionally maintaining a very conservative capital structure and liquidity position during 2023.”

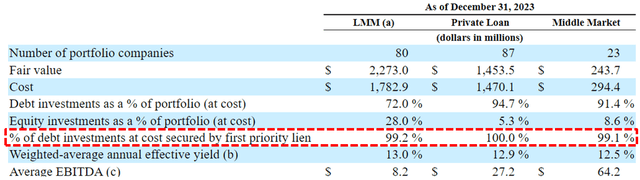

Please keep in mind that the “% of debt investments at cost secured by first priority lien” shown below is only for debt investments (excludes equity positions):

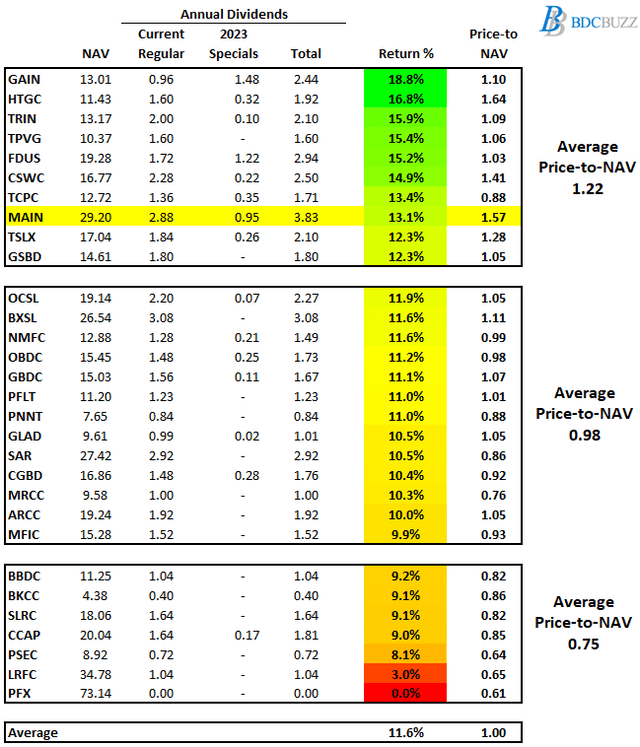

Dividends-to-NAV/Book Value Ratios

The following table shows the current annual dividends divided by NAV per share as a simple proxy for current returns on equity (“ROE”) to shareholders. BDCs with higher-risk portfolios should be able to deliver higher returns through higher portfolio yields. Conversely, lower-risk BDCs have lower portfolio yields due to safer assets/investments responsible for their lower return ratios. However, many of the other BDCs with lower return ratios are due to higher operating costs (including PSEC and MRCC), and/or credit issues driving lower prices paid by investors.

We do not cover most of the lower return and/or lower quality BDCs including PFX, LRFC, CCAP, SLRC, BKCC, and BBDC mostly due to historically providing lower returns to shareholders driving lower price multiples to NAV (current average of 0.75) and less access to additional equity capital to deleverage and/or for opportunistic portfolio growth.

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy-to-digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning, we provide quick updates for the sector, including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on individual BDCs each week prioritized by focusing on buying opportunities and potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Weekly General Updates or Comparison Reports – A series of updates discussing ‘Building a BDC Portfolio’, suggested pricing and limit orders, expense/return ratios, interest rates, leverage, BDC Investment Grade Notes/Baby Bonds, portfolio mix, and potential impacts on dividend coverage and risk.

![]()