The following information was previously provided to subscribers of BDC Buzz Premium Reports along with:

- CGBD target prices, buying points, and suggested limit orders (used during market volatility).

- CGBD risk profile, potential credit issues, changes in NAV, and overall rankings. Please see BDC Risk Profiles for additional details.

- CGBD dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

![]()

CGBD Quick Quarterly Update (December 31, 2023)

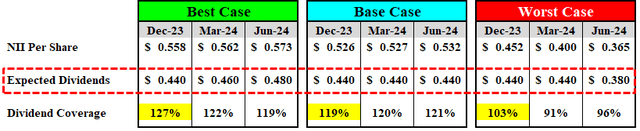

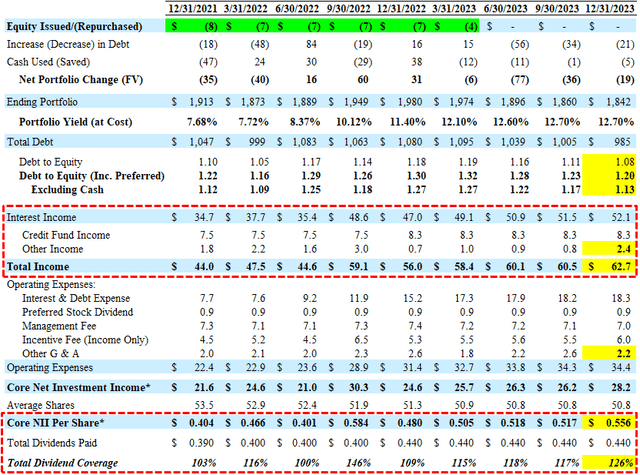

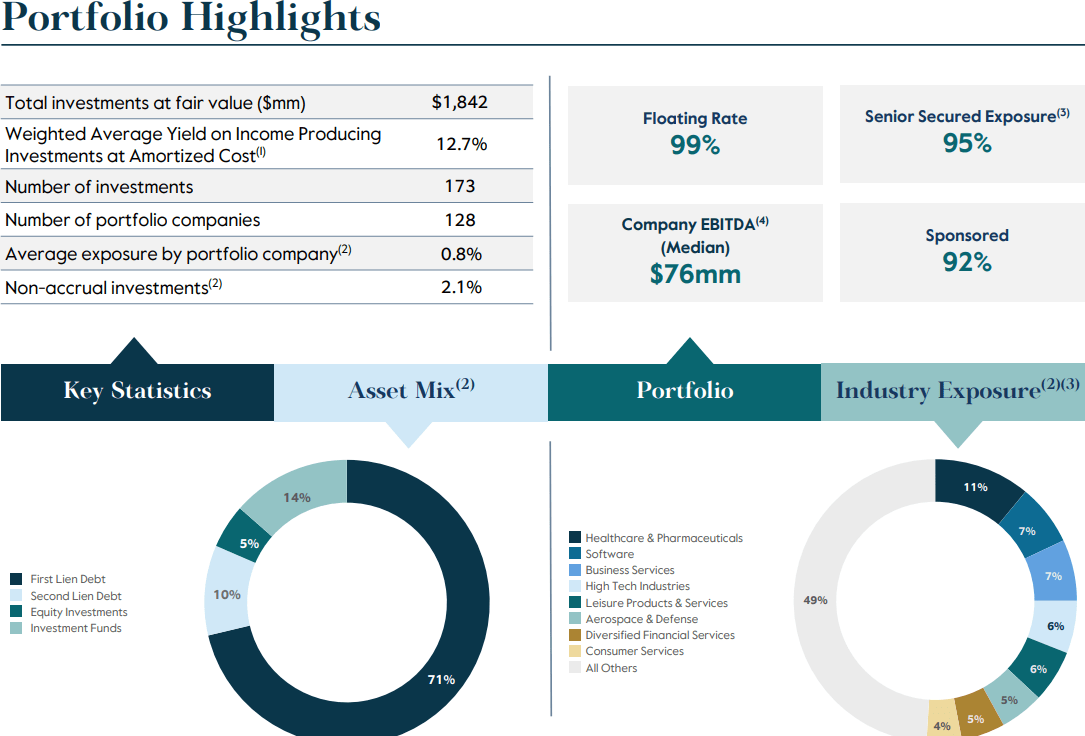

- Earnings: Hit its best-case projections covering its regular and supplemental dividends by 126% due to higher-than-expected other income combined with lower-than-expected ‘Other G&A’. The company maintained its portfolio yield of 12.7% with another decline in leverage (debt-to-equity, net of cash) from 1.17 to 1.13.

- Dividends: Increased its quarterly base dividend from $0.37 to $0.40 plus a supplemental of $0.08 for a total of $0.48 per share for Q1 2024 (above best-case projections).

- NAV Per Share: Increased by $0.13 or 0.8% (from $16.86 to $16.99) due to overearning the dividends by $0.12 per share and unrealized portfolio appreciation.

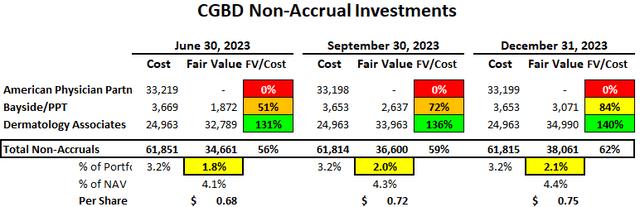

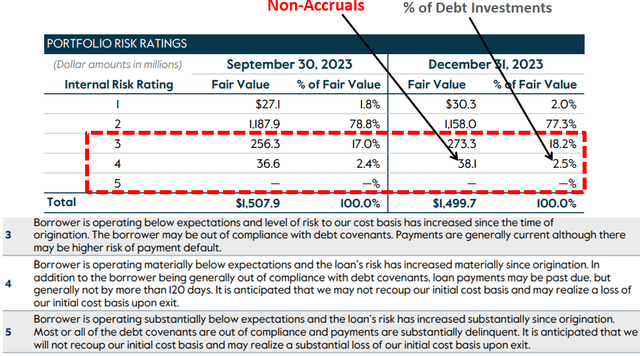

- Credit Quality: Non-accruals increased slightly from 2.0% to 2.1% of the portfolio fair value due to marking up Bayside Parent (Professional Physical Therapy) and Dermatology Associates (same as previous quarter). Investments with a risk rating of 3 and 4 (implies downgraded) increased from 19.4% to 20.7% of total debt investments.

- This information will be discussed in the updated CGBD Deep Dive Projection report, along with its overall risk profile, full dividend and financial projections, taking into account discussions with management on the upcoming earnings call.

As discussed in the previous report, there is a good chance that the company will continue to pay additional supplemental dividends each quarter partially supported by previous increases in the underlying rates. The Board increased its quarterly base dividend from $0.37 to $0.40 plus a supplemental of $0.08 for a total of $0.48 per share for Q1 2024, which was above the previous best-case projections, as shown below.

“We are very pleased with our fourth quarter and fiscal year 2023 results, which we believe were due to our ability to capitalize on the breadth and depth of the OneCarlyle platform and drive performance throughout an evolving market environment. Despite the market’s complexity, we remained steadfast in our disciplined approach to deliver steady income and solid credit performance by sourcing transactions during 2023 with pricing, terms and structures that were attractive relative to historical originations. As a result of our continued execution of this strategy, the quality of our portfolio, and confidence in the future, we are increasing our base dividend by $0.03 to $0.40 per share.”

As shown below, non-accruals increased slightly from 2.0% to 2.1% of the portfolio fair value due to marking up (typically a good sign) Bayside Parent (Professional Physical Therapy) and Dermatology Associates (same as the previous quarter).

Investments with a risk rating of 3 and 4 (implies downgraded) increased from 19.4% to 20.7% of total debt investments. Most of the investments previously considered ‘watch list’ are likely investments with risk rating 3, which will be discussed in the updated CGBD Deep Dive Projection report.

On November 2, 2023, the Board approved the extension of its stock repurchase program through November 5, 2024, which was previously increased to $200 million, providing an incremental $50 million of repurchasing capacity. During Q3 2023, there were no shares repurchased likely due to the stock price trading closer to NAV:

From previous call: “On the share repurchases, we take a close look at where our current trading price is and that’s certainly a big factor in evaluating the level of repurchases. You can see this last quarter, we’re trading up in the 90%, 95% of NAV territory. We’ve stated in the past that if we got that level, we’d certainly look to curtail the buybacks, and that’s certainly what you saw this past quarter. We’ll continue to evaluate where the stock is trading as well as looking importantly at our overall flow, that’s something we keep a close eye on and we want to be mindful of. When we talk to investors, some of them say, hey, get those buybacks. Yes, depending on level accretion, but we also want to make sure we’ve got good float in that stock. So historically, we’ve purchased over $150 million. We’ve been very supportive over the years. I think based on the current level of trading, we’re certainly going to look to mitigate that a little — maybe go over a little bit smaller just based on the current trading levels.”

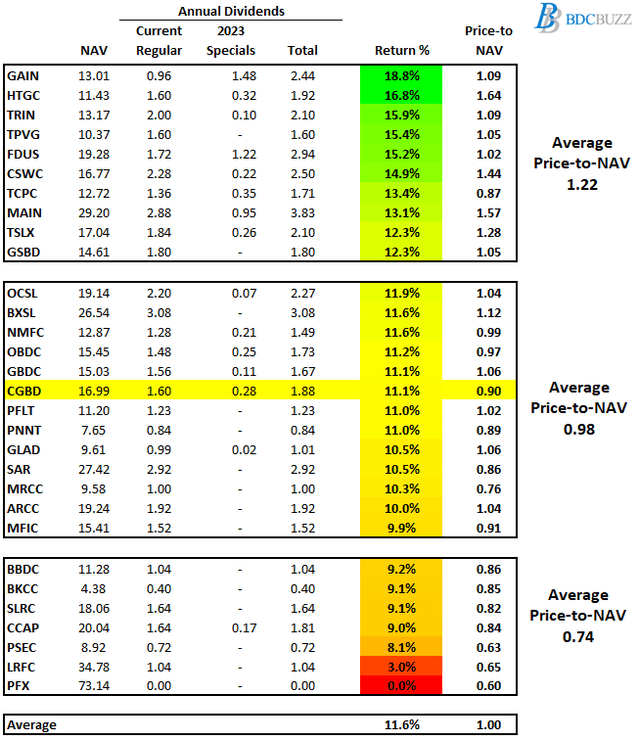

Dividends-to-NAV/Book Value Ratios

The following table shows the current annual dividends divided by NAV per share as a simple proxy for current returns on equity (“ROE”) to shareholders. BDCs with higher-risk portfolios should be able to deliver higher returns through higher portfolio yields. Conversely, lower-risk BDCs have lower portfolio yields due to safer assets/investments responsible for their lower return ratios. However, many of the other BDCs with lower return ratios are due to higher operating costs (including PSEC and MRCC), and/or credit issues driving lower prices paid by investors.

We do not cover most of the lower return and/or lower quality BDCs including PFX, LRFC, CCAP, SLRC, BKCC, and BBDC mostly due to historically providing lower returns to shareholders driving lower price multiples to NAV (current average of 0.74) and less access to additional equity capital to deleverage and/or for opportunistic portfolio growth.

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy-to-digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning, we provide quick updates for the sector, including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on individual BDCs each week prioritized by focusing on buying opportunities and potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Weekly General Updates or Comparison Reports – A series of updates discussing ‘Building a BDC Portfolio’, suggested pricing and limit orders, expense/return ratios, interest rates, leverage, BDC Investment Grade Notes/Baby Bonds, portfolio mix, and potential impacts on dividend coverage and risk.

![]()