The following information was previously provided to subscribers of BDC Buzz Premium Reports along with:

- TCPC target prices, buying points, and suggested limit orders (used during market volatility).

- TCPC risk profile, potential credit issues, changes in NAV, and overall rankings. Please see BDC Risk Profiles for additional details.

- TCPC dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

![]()

On September 29, 2023, I sold my position in BlackRock TCP Capital Corp (TCPC) at $11.93 mostly related to having a higher amount of investments considered ‘watch list’. As mentioned in many previous reports, one of my primary concerns includes its portfolio companies that sell products through Amazon, including Thrasio, Whele (Perch), and Razor Group. These investments remain on its watch list which is among the highest in the sector. Also, the upcoming merger with BKCC is likely a negative for TCPC shareholders.

TCPC Quick Quarterly Update (December 31, 2023)

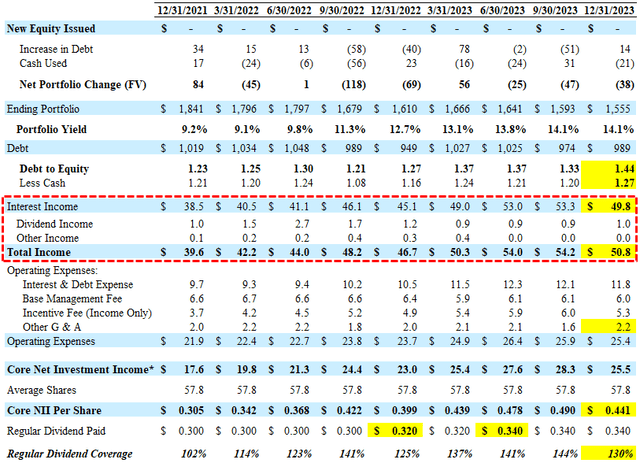

- Earnings: Reported between its worst and base case projections due to increased non-accruals and higher ‘Other G & A’. TCPC has covered its regular dividends by around 138% over the last four quarters.

- Non-Cash/PIK Income: Decreased from 6.5% to 2.7% of total income.

- Dividends: Maintained its regular quarterly dividend of $0.34 per share for Q1 2024 which was the previous worst-case projection.

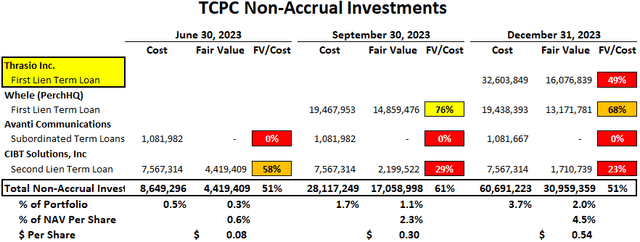

- NAV Per Share: Decreased by $0.82 or 6.4% (from $12.72 to $11.90) due to the special dividend of $0.25 per share and another markdown of Edmentum, Inc. (by $13.8 million or $0.24 per share) and some of its watch list investments including Thras.io (by $8.6 million or $0.15 per share), Aventiv/Securus (by $5.4 million or $0.09 per share), Khoros, Whele (Perch), CIBT, Astra Acquisition and Magenta (McAfee) partially offset by overearning the regular dividends. It is important to note that NAV would have declined by 2.6% excluding the impact of the special dividend and Edmentum (equity position) but has declined by 17% over the last two years.

- Credit Quality: Non-accruals increased from 1.1% to 2.0% of the portfolio at fair value (3.7% at cost) due to adding Thras.io as predicted in the previous report.

- Pricing: Its ST target price of $12.50 already takes into account additional credit issues. I will reassess after updating the projections and risk profile using guidance from management including from the recent earnings call.

- Merger Update: The merger is currently anticipated to close during the first quarter of 2024, subject to stockholder approval, customary regulatory approvals, and other closing conditions.

- Share Repurchases: During Q4 2023, there were no shares were repurchased.

- This information will be discussed in the updated TCPC Deep Dive Projection report.

“We generated solid net investment income in the fourth quarter, culminating a strong year in which we grew NII 20% and delivered a 14.5% net investment income return on equity. Our proven track record of delivering consistent results across market cycles has enabled us to consistently out-earn our dividend and drive outstanding long-term results on behalf of our shareholders. We also are confident in our ability to close our proposed merger with BlackRock Capital Investment Corporation this year as planned. This is a transformational combination that we believe will create substantial scale, operational cost synergies, and better access to capital on improved terms. We also anticipate that the transaction will be accretive to NII and further bolster the earnings power of the combined company.”

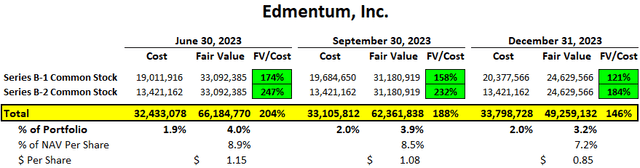

As discussed in previous reports, Edmentum, Inc. is a provider of online learning programs that was acquired by Vistria Group. TCPC chose to re-invest a meaningful portion of the proceeds and “remain a significant shareholder of Edmentum, due to strong conviction in the continued growth”. As shown below, TCPC’s investment in Edmentum declined again but remains around $49 million and still accounts for over 3% of the portfolio.

“During the fourth quarter, we did report a decline in NAV, the largest driver of which was unrealized losses on three positions in our portfolio. It’s important to emphasize that these companies’ challenges are idiosyncratic in nature and not indicative of broader issues in our portfolio. Our overall credit quality is solid, and we are well-positioned to further execute our strategy of selectively investing in compelling, new opportunities.”

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy-to-digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning, we provide quick updates for the sector, including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on individual BDCs each week prioritized by focusing on buying opportunities and potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Weekly General Updates or Comparison Reports – A series of updates discussing ‘Building a BDC Portfolio’, suggested pricing and limit orders, expense/return ratios, interest rates, leverage, BDC Investment Grade Notes/Baby Bonds, portfolio mix, and potential impacts on dividend coverage and risk.

![]()