The following information was previously provided to subscribers of BDC Buzz Premium Reports along with:

- Target prices, buying points, and suggested limit orders (used during market volatility).

- Risk profile, potential credit issues, changes in NAV, and overall rankings. Please see BDC Risk Profiles for additional details.

- Dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

![]()

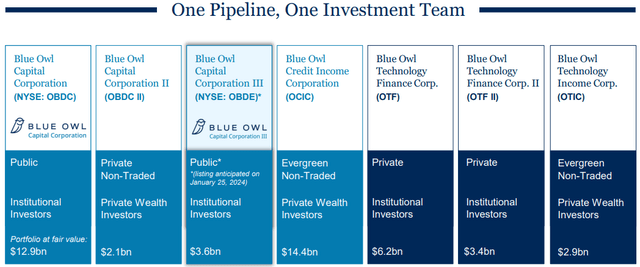

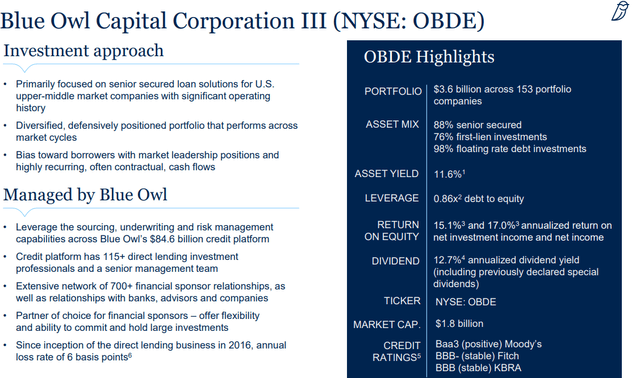

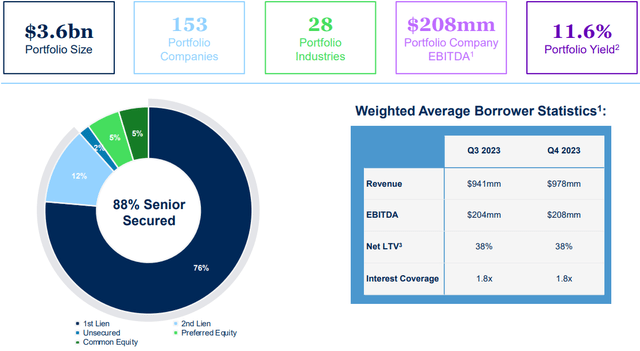

The largest newly public BDC is Blue Owl Capital Corporation III (OBDE) with investments in 153 portfolio companies valued at around $3.6 billion that are 76% first-lien secured debt positions:

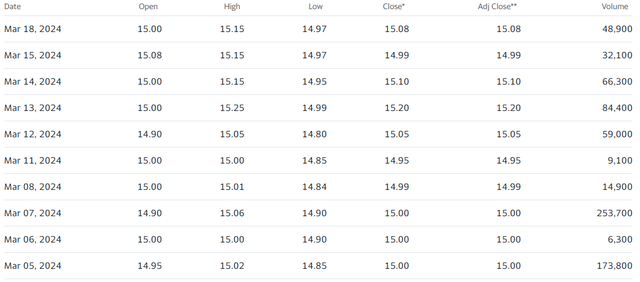

Trading volumes are relatively low but will likely pick up after the expiration of share lock-ups (mentioned later):

OBDE has a relatively higher fee structure with an annual base management fee of 1.50% on average gross assets and an incentive fee of 17.5% over a 6% hurdle rate.

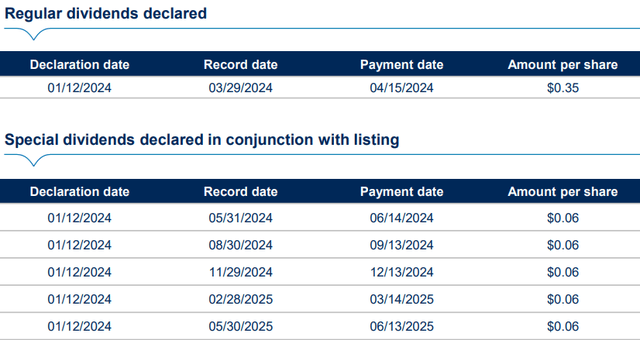

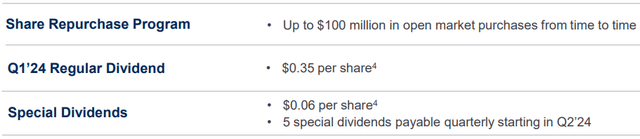

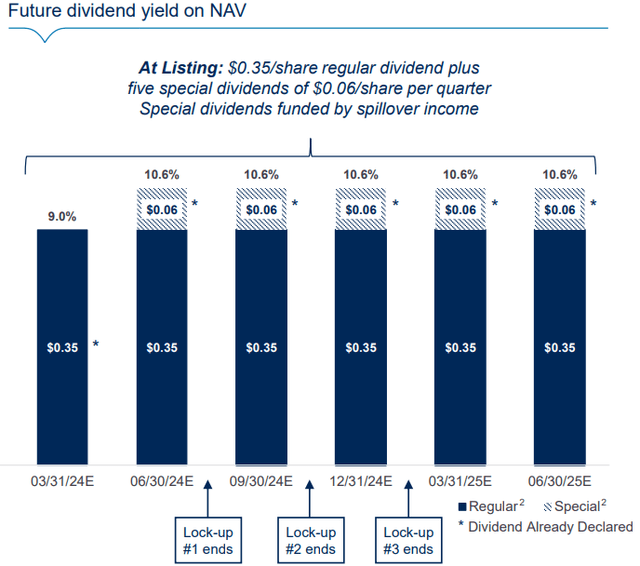

The Board previously declared a first-quarter 2024 regular dividend of $0.35 per share for stockholders of record as of March 29, 2024, payable on April 15, 2024. In conjunction with the listing, the Board declared five special dividends of $0.06 per share, payable quarterly:

The Board approved a share repurchase program of up to $100 million for the common stock at prices below NAV.

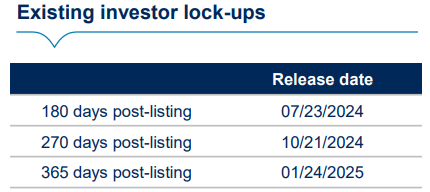

OBDE’s charter included trading restrictions on 100% of OBDE’s shares outstanding after a liquidity event such as the listing. In connection with the listing, our Board of Directors (the “Board”) waived this restriction for approximately 5% of each investor’s position, which became freely tradeable at time of listing. This represents approximately 5.9 million shares of initial float. Each investor’s remaining shares will become available via the expiration of a series of lock-ups, the first of which is July 23, 2024:

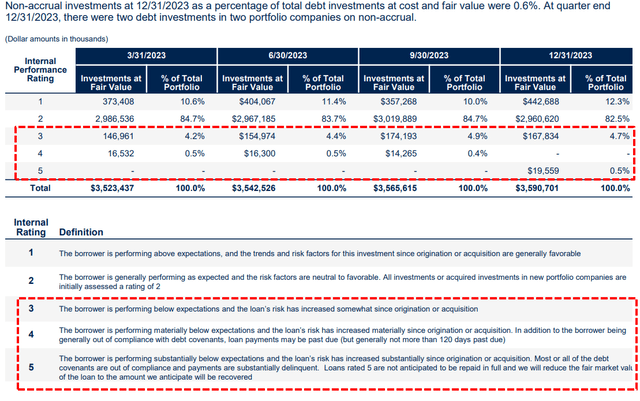

Two portfolio companies on non-accrual, representing 0.6% of the total debt portfolio at fair value and cost. Since its inception, OBDE’s annual net loss rate has been only 0.06%.

Based on the visibility we have today into the favorable positioning of our borrowers, we expect that the vast majority of our portfolio companies will maintain solid coverage metrics and adequate liquidity through this period. We believe any challenges ultimately will be manageable across our portfolio as a whole.

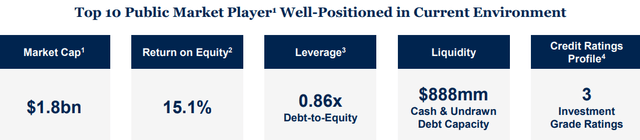

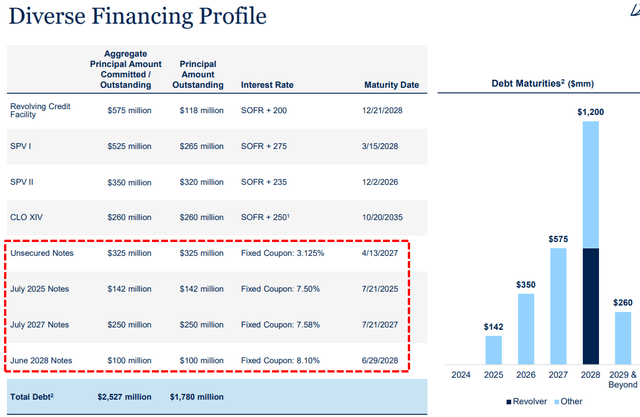

The debt funding mix comprised 46% unsecured debt (based on outstanding debt) with a weighted average debt maturity of approximately 4.7 years and no debt maturities until 2025. Similar to OBDC, management is targeting upper leverage (debt-to-equity) of 1.25:

We believe there is further earnings upside in 2024 as we are able to increase leverage towards the higher end of our target range of 0.90x – 1.25x. As noted in our listing presentation, when we are able to achieve target leverage, run-rate ROE should increase by approximately 50 bps, adding roughly $0.02 per share to quarterly NII, all else equal.

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy-to-digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning, we provide quick updates for the sector, including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on individual BDCs each week prioritized by focusing on buying opportunities and potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Weekly General Updates or Comparison Reports – A series of updates discussing ‘Building a BDC Portfolio’, suggested pricing and limit orders, expense/return ratios, interest rates, leverage, BDC Investment Grade Notes/Baby Bonds, portfolio mix, and potential impacts on dividend coverage and risk.

![]()