The following information was previously provided to subscribers of BDC Buzz Premium Reports along with:

- We will likely hold off from covering PSBD due to its higher use of leverage, NAV volatility, lower trading volume, and lack of response from management.

- Target prices, buying points, and suggested limit orders (used during market volatility).

- Risk profile, potential credit issues, changes in NAV, and overall rankings. Please see BDC Risk Profiles for additional details.

- Dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

![]()

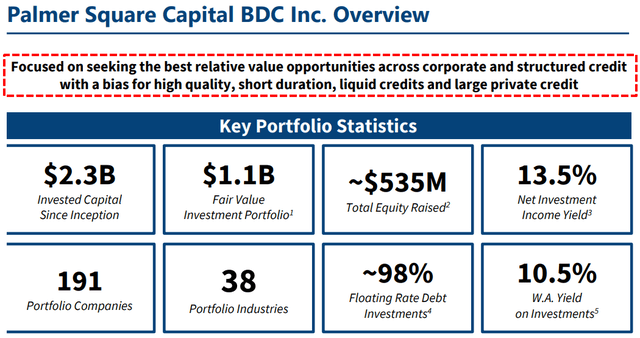

Palmer Square Capital (PSBD) went public at $16.45 per share and is the smallest of the recent IPOs focused on shorter duration and structured credits which are generally more liquid and in larger companies:

Palmer Square has established its reputation in the global corporate and structured credit market as the top-ranked CLO issuer by deal volume in 2023. This strong performance during a difficult environment for CLO issuance demonstrates our ability to find attractive opportunities and deliver for our investors across market conditions. Palmer Square’s platform is focused on corporate and structured credit across three significant strategies, opportunistic, income short duration; and finally, private and structured credit. PSBD was launched in 2019, and we started investing in early 2020. Unlike traditional direct lending models, we believe our model offers investors attractive risk-adjusted returns through a more liquid and transparent strategy, given our ability to invest across the syndicated and direct lending markets.

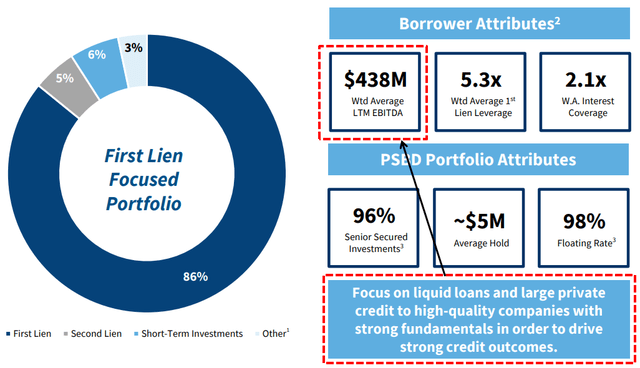

It should be noted that PSBD has a higher portion of its portfolio in broadly syndicated loans:

Specifically, our team has the ability to identify the best relative value in the larger, more liquid parts of the market in both the broadly syndicated market and private credit. We’ve already seen private credit issuers return to the broadly syndicated mode market to refinance the tighter spreads. We focus on investing in large, broadly syndicated loans and large private credit.”

“We’ve certainly seen a pretty significant pickup in activity in the syndicated loan market really starting in the fourth quarter of 2023 and certainly continuing this year for January and February. I’d say we’ve seen a few of the larger private credit transactions coming back to our market. There’s been a couple of larger syndicated transactions that were rumored to be going to the private credit markets that came to the syndicated market.”

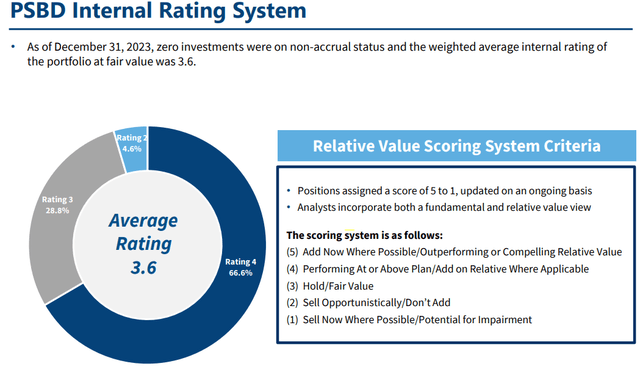

As of December 31, 2023, there were no investments were on non-accrual status with a weighted average internal rating of the portfolio of 3.6:

The Board approved a share repurchase program of up to $20 million for the common stock at prices below NAV.

Subsequent to the IPO, we have 32,552,794 shares of common stock outstanding. Sales of substantial amounts of our common stock, or the availability of such shares for sale, could adversely affect the prevailing market prices for our common stock.

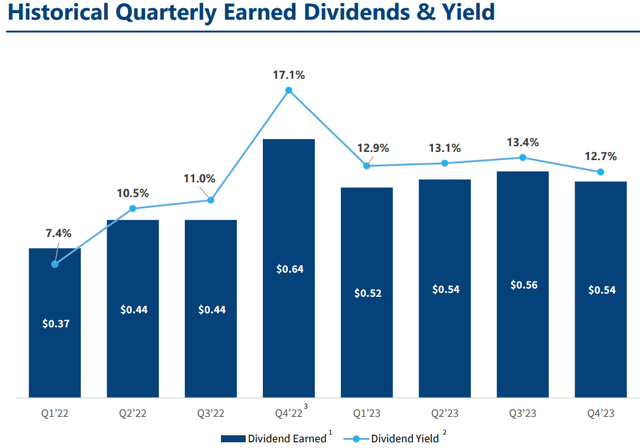

For Q4 2023, PSBD paid a dividend of $0.535 per share and will announce its Q1 2024 dividend over the coming weeks:

Q. “Just curious if you could give an update on your view on the distribution policy going forward? Do you expect that to be slowing related to your net investment income per share? Or do you expect to hold a relatively stable level of regular dividend and pay supplemental in addition to that?

A. “Our Board has continued to evaluate a go-forward dividend policy, and we’ll be updating shareholders on that front at quarter end.”

PSBD has a higher dividend yield due to paying higher amounts relative to NAV with the highest leverage (1.38 net of cash).

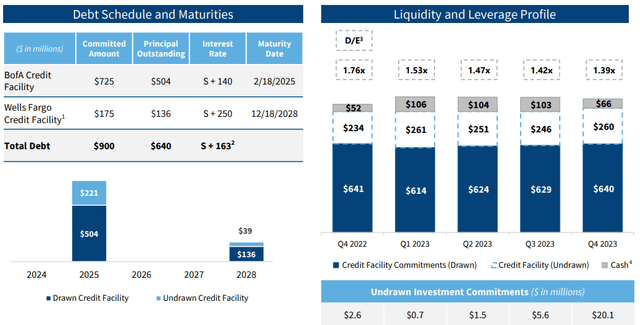

It should be noted that 100% of its borrowings are secured credit facilities (less flexible) at floating rates:

We reached out to management in January 2024 but they have not responded. Also, the trading volumes have fallen off quite a bit:

We will likely hold off from covering this BDC due to its higher use of leverage, NAV volatility, lower trading volume, and lack of response from management.

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy-to-digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning, we provide quick updates for the sector, including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on individual BDCs each week prioritized by focusing on buying opportunities and potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Weekly General Updates or Comparison Reports – A series of updates discussing ‘Building a BDC Portfolio’, suggested pricing and limit orders, expense/return ratios, interest rates, leverage, BDC Investment Grade Notes/Baby Bonds, portfolio mix, and potential impacts on dividend coverage and risk.

![]()